|

市場調査レポート

商品コード

1797703

外用薬パッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Topical Drugs Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 外用薬パッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月31日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

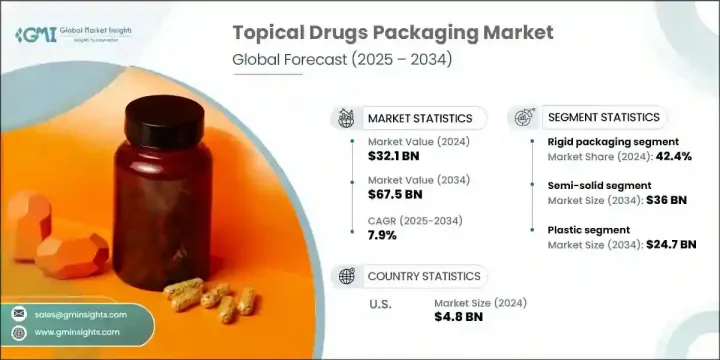

世界の外用薬パッケージング市場は、2024年に321億米ドルと評価され、CAGR 7.9%で成長し、2034年には675億米ドルに達すると推定されています。

皮膚疾患の増加と、オンラインを中心とした消費者直販チャネルの拡大が主な成長要因のひとつです。eコマースの活況は、製薬会社、特に外用ソリューションを提供する製薬会社に、より多くの人々に直接アプローチする新たな道を開いた。

にきび、湿疹、乾癬のようなスキン疾患がますます蔓延する中、製薬会社はより身近で効果的な外用治療に力を入れており、その結果、安全で革新的な包装への需要が高まっています。QR認証、改ざん防止シール、追跡機能など、パッケージングにおけるデジタル技術の採用は、高価値のOTC皮膚科製品で支持を集めています。持続可能性が包装の選択を変え続けています。医薬品セクターにおける消費者や規制当局の期待の変化を反映し、市場関係者はリサイクル可能なプラスチック、詰め替えシステム、生分解性フィルムなど、環境に配慮したソリューションを取り入れています。こうした持続可能なパッケージングの革新は、環境負荷の低減に役立つだけでなく、ブランドの評判や消費者の信頼を高めることにもつながっています。企業は、製品のライフサイクルを通じて廃棄物を最小限に抑える、軽量で資源効率の高い素材の開発にますます投資するようになっています。リサイクルしやすい単一素材構造の採用や、カーボンフットプリントの少ない包装工程は、業界全体で一般的になりつつあります。さらに、使用済み包装を回収して新しい製品に再加工するクローズド・ループ・システムの推進も高まっています。こうした取り組みは、倫理的で環境に配慮したヘルスケアソリューションに対する需要の高まりに対応しつつ、世界の持続可能性の目標に沿ったものです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 321億米ドル |

| 予測金額 | 675億米ドル |

| CAGR | 7.9% |

2024年には、リジッドフォーマットが42.4%のシェアを占める。ボトル、ガラス容器、瓶は、製品の保護、品質保持、保存安定性を提供するため、高級治療薬や処方箋皮膚治療薬に広く使用されています。これらの容器は、粘性の高い製剤を扱い、繊細な用途のために構造的完全性を維持する能力があるため、特に好まれています。

液体製品セグメントは、2025年から2034年にかけてCAGR 7.9%で成長すると予測されています。防腐剤や薬用スプレーを含む液剤は、有効成分の保存と投与精度をサポートしながら、こぼれや汚染を防ぐ精密で安全な包装が求められます。

北米外用薬パッケージング市場は2024年に37.6%のシェアを占め、2025年から2034年にかけてCAGR 6.9%で成長します。強力な医薬品インフラ、OTC薬への嗜好、セルフケア習慣の高まりが、この地域のパッケージング革新を促進しています。eコマースへの依存の高まりと、安全性とコンプライアンスを確保するユーザーフレンドリーなパッケージングが、米国とカナダの需要状況を形成し続けています。

外用薬パッケージング市場の主要企業には、West Pharmaceutical Services、Schott、AptarGroup、Gerresheimer、Amcorなどがあります。先進パッケージング企業は、持続可能な素材、デジタルセキュリティ、高度な調剤システムなどに多額の投資を行い、消費者と製薬企業の双方の進化するニーズに応えています。各ブランドは、環境規制や消費者の嗜好に合わせるため、詰め替え可能な容器、生分解性包装フィルム、低炭素製造などの技術革新を進めています。製品の差別化は、不正開封防止のクロージャー、人間工学に基づいたデザイン、トレーサビリティと消費者の信頼を高めるシリアル化技術によって強化されています。また、開発企業は製薬メーカーと戦略的パートナーシップを結び、特殊な皮膚科学製品に合わせた包装形態を共同開発しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 皮膚疾患および皮膚科疾患の有病率の上昇

- 便利で使いやすいパッケージ形式への需要の高まり

- 市販外用薬の拡大

- eコマースと消費者直販の医薬品販売の成長

- 単位用量および制御投与システムにおける革新

- 業界の潜在的リスク&課題

- 厳格な規制遵守と承認プロセス

- 子供が開けにくく、高齢者にも優しいパッケージ設計の複雑さ

- 市場機会

- 皮膚科のニーズが十分に満たされていない新興市場への進出

- 認証と患者エンゲージメントのためのスマートパッケージングテクノロジーの統合

- 持続可能かつ生分解性の包装ソリューションへの投資が増加しています

- 小売薬局チェーンによるプライベートブランドの局所用製品ラインの成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 過去の価格分析(2021-2024)

- 価格動向の要因

- 地域による価格差

- 価格予測(2025-2034)

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 持続可能な材料の評価

- カーボンフットプリント分析

- 循環型経済の実現

- 持続可能性の認証と基準

- 持続可能性ROI分析

- 世界の消費者感情分析

- 特許分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:パッケージング形態別、2021年~2034年

- 主要動向

- 軟包装

- 硬包装

- 半硬包装

第6章 市場推計・予測:パッケージング材料別、2021年~2034年

- 主要動向

- プラスチック

- ガラス

- 金属

- 紙

- アルミニウム

- その他

第7章 市場推計・予測:商品タイプ別、2021年~2034年

- 主要動向

- ボトル

- キャップとクロージャー

- 吸入器

- チューブ

- ジャー

- その他

第8章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- 液体

- 半固体

- 固体

- 経皮

第9章 市場推計・予測:クロージャタイプ別、2021年~2034年

- 主要動向

- スクリューキャップ

- フリップトップキャップ

- ポンプディスペンサー

- スポイト

- ノズル

第10章 市場推計・予測:投与方法別、2021年~2034年

- 主要動向

- 眼科使用

- 経鼻使用

- 経皮使用

第11章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 皮膚科

- 眼科

- その他

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- 世界の主要企業

- Amcor

- AptarGroup

- Gerresheimer

- Schott

- West Pharmaceutical Services

- 地域の主要企業

- 北米

- Catalent

- WestRock

- Sonoco Products

- ProAmpac

- Silgan Holdings

- 欧州

- Bormioli Pharma

- Constantia Flexibles

- Mondi

- SGD Pharma

- アジア太平洋地域

- Huhtamaki

- Nipro

- EPL Limited

- 北米

- ニッチ企業/ディスラプター

- CCL Industries

- LOG Pharma Primary Packaging

- Nelipak

The Global Topical Drugs Packaging Market was valued at USD 32.1 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 67.5 billion by 2034. Rising skin conditions and growing direct-to-consumer sales channels, particularly online, are among the primary growth drivers. The boom in e-commerce has opened new pathways for pharmaceutical companies, especially those offering topical solutions, to reach broader audiences directly.

With skin conditions like acne, eczema, and psoriasis becoming increasingly prevalent, pharmaceutical firms are focusing more on accessible and effective topical treatments, which in turn boosts demand for safe and innovative packaging. Digital tech adoption in packaging-such as QR verification, tamper-proof seals, and track-and-trace capabilities-is gaining traction in high-value and OTC dermatology products. Sustainability continues to reshape packaging choices. Market players are integrating eco-conscious solutions, including recyclable plastics, refill systems, and biodegradable films, reflecting shifting consumer and regulatory expectations in the pharmaceutical sector. These sustainable packaging innovations are not only helping reduce environmental impact but also enhancing brand reputation and consumer trust. Companies are increasingly investing in the development of lightweight, resource-efficient materials that minimize waste throughout the product lifecycle. The use of mono-material structures for easier recyclability, along with reduced carbon footprint packaging processes, is becoming more common across the industry. Additionally, there's a growing push for closed-loop systems, where used packaging is collected and reprocessed into new products. Such initiatives align with global sustainability goals while meeting the rising demand for ethical and environmentally responsible healthcare solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.1 Billion |

| Forecast Value | $67.5 Billion |

| CAGR | 7.9% |

In 2024, the rigid formats segment held a 42.4% share. Bottles, glass containers, and jars are widely used for premium and prescription skin treatments as they offer protection, preserve product quality, and support storage stability. These containers are particularly favored for their ability to handle viscous formulations and maintain structural integrity for sensitive applications.

The liquid product segment is forecasted to grow at a CAGR of 7.9% from 2025 to 2034. Liquids, including antiseptics and medicated sprays, demand precise, secure packaging that prevents spills and contamination while supporting active ingredient preservation and dosing accuracy.

North America Topical Drugs Packaging Market held 37.6% share in 2024 and is set to grow at a CAGR of 6.9% throughout 2025-2034. Strong pharmaceutical infrastructure, a preference for OTC medication, and growing self-care habits are advancing packaging innovation in this region. Increased reliance on e-commerce and user-friendly packaging that ensures safety and compliance continues to shape the demand landscape in the US and Canada.

Leading companies in Topical Drugs Packaging Market include West Pharmaceutical Services, Schott, AptarGroup, Gerresheimer, and Amcor. Topical drug packaging companies are investing heavily in sustainable materials, digital security, and advanced dispensing systems to cater to the evolving needs of both consumers and pharmaceutical clients. Brands are innovating with refillable containers, biodegradable packaging films, and low-carbon manufacturing to align with environmental regulations and consumer preferences. Product differentiation is being enhanced through tamper-proof closures, ergonomic design, and serialization technologies that add traceability and consumer confidence. Companies are also forming strategic partnerships with pharmaceutical manufacturers to co-develop packaging formats tailored to specialized dermatological products.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Packaging material trends

- 2.2.3 Product types trends

- 2.2.4 Drug type trends

- 2.2.5 Closure type trends

- 2.2.6 Mode of administration trends

- 2.2.7 Application trends

- 2.2.8 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of skin diseases and dermatological disorders

- 3.2.1.2 Growing demand for convenient and user-friendly packaging formats

- 3.2.1.3 Expansion of over-the-counter (OTC) topical drug products

- 3.2.1.4 Growth of e-commerce and direct-to-consumer pharmaceutical sales

- 3.2.1.5 Innovation in unit dose and controlled-dispensing systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance and approval processes

- 3.2.2.2 Complexities in designing child-resistant yet senior-friendly packaging

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with underserved dermatological needs.

- 3.2.3.2 Integration of smart packaging technologies for authentication and patient engagement.

- 3.2.3.3 Rising investment in sustainable and biodegradable packaging solutions.

- 3.2.3.4 Growth of private-label topical product lines by retail pharmacy chains.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price Forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability ROI Analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Flexible packaging

- 5.3 Rigid packaging

- 5.4 Semi-rigid packaging

Chapter 6 Market Estimates and Forecast, By Packaging Material, 2021 - 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Glass

- 6.4 Metal

- 6.5 Paper

- 6.6 Aluminium

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Product Types, 2021 - 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Caps & closures

- 7.4 Inhalers

- 7.5 Tubes

- 7.6 Jars

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Drug Type, 2021 - 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Liquid

- 8.3 Semi-solid

- 8.4 Solid

- 8.5 Transdermal

Chapter 9 Market Estimates and Forecast, By Closure Type, 2021 - 2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 Screw cap

- 9.3 Flip-top cap

- 9.4 Pump dispenser

- 9.5 Dropper

- 9.6 Nozzle

Chapter 10 Market Estimates and Forecast, By Mode of Administration, 2021 - 2034 (USD Million & Kilo Tons)

- 10.1 Key trends

- 10.2 Ophthalmic usage

- 10.3 Nasal usage

- 10.4 Dermal usage

Chapter 11 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Kilo Tons)

- 11.1 Key trends

- 11.2 Dermatology

- 11.3 Ophthalmology

- 11.4 Others

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Amcor

- 13.1.2 AptarGroup

- 13.1.3 Gerresheimer

- 13.1.4 Schott

- 13.1.5 West Pharmaceutical Services

- 13.2 Regional Key Players

- 13.2.1 North America

- 13.2.1.1 Catalent

- 13.2.1.2 WestRock

- 13.2.1.3 Sonoco Products

- 13.2.1.4 ProAmpac

- 13.2.1.5 Silgan Holdings

- 13.2.2 Europe

- 13.2.2.1 Bormioli Pharma

- 13.2.2.2 Constantia Flexibles

- 13.2.2.3 Mondi

- 13.2.2.4 SGD Pharma

- 13.2.3 APAC

- 13.2.3.1 Huhtamaki

- 13.2.3.2 Nipro

- 13.2.3.3 EPL Limited

- 13.2.1 North America

- 13.3 Niche Players / Disruptors

- 13.3.1 CCL Industries

- 13.3.2 LOG Pharma Primary Packaging

- 13.3.3 Nelipak