|

市場調査レポート

商品コード

1797699

CXL(Compute Express Link)コンポーネントの市場機会、成長促進要因、業界動向分析、2025~2034年予測Compute Express Link (CXL) Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| CXL(Compute Express Link)コンポーネントの市場機会、成長促進要因、業界動向分析、2025~2034年予測 |

|

出版日: 2025年07月16日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

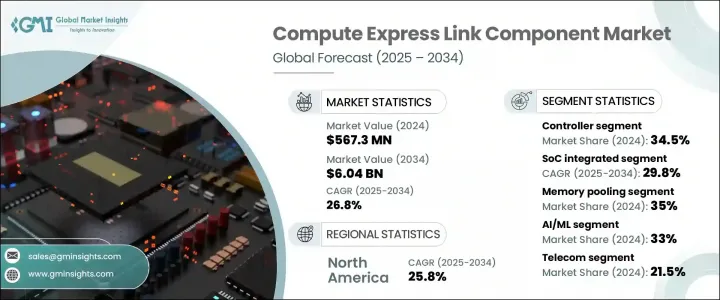

CXL(Compute Express Link)コンポーネントの世界市場規模は、2024年に5億6,731万米ドルとなり、CAGR 26.8%で成長し、2034年には60億4,000万米ドルに達すると予測されています。

この急拡大は、最新のデータセンターにおけるハイパフォーマンスコンピューティング、AI/MLワークロード、メモリ分割に対する需要の急増を反映しています。CXL技術は、柔軟なメモリアーキテクチャとプールアクセスを可能にし、次世代インフラの重要な推進力となっています。企業は冗長性を回避し、ハードウェアコストを削減するために、スケーラブルなメモリ管理を求めるようになっています。CXLのプール・メモリ・モデルは、データセンターがリソースの有効活用を模索する中で、2020年代初頭に登場しました。コンピュートとメモリを切り離すことで、オーバープロビジョニングが不要になり、コスト効率が向上します。CXLによるメモリ階層化とコンポーザブル・サーバ・アーキテクチャの革新は、サーバ設計を再構築し、ノード間でメモリとストレージをダイナミックに共有することを容易にしています。

このテクノロジーは、データセンターのアーキテクチャを再構築し、リソースの最適化、効率性、俊敏性の新たな基準を設定します。メモリーをコンピュート・リソースから切り離すことで、ワークロードの割り当てにおいてかつてないスケーラビリティと柔軟性を実現します。このシフトは、リアルタイムデータ処理、広帯域幅の接続性、システム間での動的なリソース共有をサポートし、レイテンシーとインフラコストを劇的に削減します。また、アイドル状態のリソースを最小限に抑え、運用ワークフローを合理化することで、よりエネルギー効率の高い環境を促進します。企業がイノベーション・サイクルの高速化とリソースのスマートな活用を目指す中、この進歩は次世代のソフトウェア定義型データセンターの基盤となる要素となります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5億6,731万米ドル |

| 予測金額 | 60億4,000万米ドル |

| CAGR | 26.8% |

ネットワークインタフェースコントローラ(NIC)分野は、2024年のシェアは5.9%、3,320万米ドルで、コントローラに比べるとかなり小さいが、急速に拡大しています。NICは、コンポーザブル・システムで低レイテンシの相互接続をサポートするために不可欠です。CXLが普及するにつれて、NICはコンピュート層とメモリ層にまたがるスケーラブルな高スループット接続を実現する上で重要な役割を果たすようになり、最も急成長しているコンポーネント・カテゴリに位置付けられています。

SoC統合コンポーネント・セグメントは2034年までに18億米ドルに達すると予測されており、最も急成長しているフォームファクターとなっています。SoCベースのCXLソリューションは、エッジやクラウドの展開に理想的なコンパクトでエネルギー効率の高いアーキテクチャを提供します。これらの高密度モジュールは、運用効率とスペースの節約を実現し、サイズや消費電力の制約が重要な場合にますます魅力的なものとなり、最新のコンピュートニーズをサポートする合理的なハードウェア構成を可能にします。

米国のCXL(Compute Express Link)コンポーネント市場は、2024年に1億9,080万米ドルを生み出し、2034年まで25.1%のCAGRで成長すると予測されています。クラウドサービスの拡大、高度なコンピューティングとデータ処理の需要が成長を牽引しています。また、米国ではデータセンターの増設やアップグレードが続いており、性能と拡張性のニーズの進化に対応するため、CXLのような高速相互接続技術の需要が高まっています。

CXL(Compute Express Link)コンポーネントの世界市場における主な業界企業には、Intel Corporation、Advanced Micro Devices, Inc.(AMD)、Samsung Electronics Co.Ltd.、Micron Technology, Inc.、SK hynix Inc.、Rambus Inc.、Cadence Design Systems, Inc.、Montage Technology Co.Ltd.、Astera Labs、Mobiveil, Inc.、Marvell Technology, Inc.、Synopsys, Inc.などがあります。CXLコンポーネント市場の主要企業は、市場での存在感を高めるために、オープンな業界標準、戦略的パートナーシップ、製品イノベーションにおけるコラボレーションを優先しています。多くの企業は、ハイパースケールデータセンター事業者やクラウドプロバイダーと提携し、CXL設計の検証や相互運用性の確保に取り組んでいます。研究開発投資は、特にSoC組み込み型CXLソリューションの速度、電力効率、統合機能の強化に重点を置いています。また、各社はM&Aを活用し、ポートフォリオの拡充と技術的アクセスの拡大を図っています。世界な製造能力を拡大し、データセンター・インフラの展開に合わせることで、プロバイダーは需要に応じて規模を拡大することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーン再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- メモリ分散化の需要の高まり

- AIと機械学習ワークロードの加速

- CXL互換サーバープラットフォームの採用

- CXL 2.0および3.0規格の出現

- ハイパースケールおよびHPCインフラストラクチャの成長

- 業界の潜在的リスク&課題

- 高コストとサプライチェーンの複雑さ

- ソフトウェアとエコシステムの準備の遅れ

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- CXLスイッチ

- メモリ拡張器

- コントローラー

- リタイマー

- ネットワークインターフェースカード

- その他

第6章 市場推計・予測:フォームファクター別、2021年~2034年

- 主要動向

- アドインカード

- エンタープライズおよびデータセンターの標準フォームファクター

- SoC統合

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- メモリプーリング

- アクセラレータ

- 階層型メモリアーキテクチャ

- コンポーザブルインフラストラクチャ

- 高速相互接続

- その他

第8章 市場推計・予測:ワークロード別、2021年~2034年

- 主要動向

- AI/機械学習

- 高性能コンピューティング

- データ分析

- クラウドコンピューティング

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信

- ファイナンス

- ヘルスケア

- 石油・ガス

- 航空宇宙

- その他

第10章 市場推計・予測:インフラ別、2021年~2034年

- 主要動向

- CSP/ハイパースケーラー

- ネオクラウド

- エンタープライズデータセンター

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- Advanced Micro Devices, Inc.(AMD)

- Astera Labs

- Cadence Design Systems, Inc.

- Intel Corporation

- Marvell Technology, Inc.

- Micron Technology, Inc.

- Microchip Technology Inc.

- Mobiveil, Inc.

- Montage Technology Co., Ltd.

- Rambus Inc.

- Samsung Electronics Co., Ltd

- SK hynix Inc.

- Synopsys, Inc.

The Global Compute Express Link Component Market was valued at USD 567.31 million in 2024 and is estimated to grow at a CAGR of 26.8% to reach USD 6.04 billion by 2034. This rapid expansion reflects surging demand for high-performance computing, AI/ML workloads, and memory disaggregation in modern data centers. CXL technology enables flexible memory architectures and pooled access, making it a key driver for next-generation infrastructure. Organizations are increasingly seeking scalable memory management to avoid redundancy and reduce hardware costs. CXL's pooled memory models emerged in the early 2020s as data centers sought better resource utilization. By decoupling compute from memory, overprovisioning becomes unnecessary, enabling cost efficiencies. Innovations in memory tiering and composable server architectures powered by CXL are reshaping server design, facilitating dynamic sharing of memory and storage across nodes.

The technology is reshaping data center architecture and setting new standards for resource optimization, efficiency, and agility. By decoupling memory from compute resources, it enables unprecedented scalability and flexibility in workload allocation. This shift supports real-time data processing, high-bandwidth connectivity, and dynamic resource sharing across systems-drastically reducing latency and infrastructure costs. It also fosters more energy-efficient environments by minimizing idle resources and streamlining operational workflows. As organizations strive for faster innovation cycles and smarter resource utilization, this advancement becomes a foundational element of next-generation, software-defined data centers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $567.31 Million |

| Forecast Value | $6.04 Billion |

| CAGR | 26.8% |

The network interface controller (NIC) segment was significantly smaller than controllers in 2024, capturing a 5.9% share with USD 33.2 million, but it is expanding very rapidly. NICs are essential to support low-latency interconnects in composable systems. As CXL becomes widespread, NICs play a vital role in enabling scalable, high-throughput connections across compute and memory tiers, positioning them as the fastest-growing component category.

The SoC-integrated component segment is projected to reach USD 1.8 billion by 2034, making it the fastest-growing form factor. SoC-based CXL solutions offer compact, energy-efficient architectures ideal for edge and cloud deployments. These high-density modules deliver operational efficiency and space savings, making them increasingly attractive where size or power constraints are critical, and enabling streamlined hardware configurations that support modern compute needs.

United States Compute Express Link (CXL) Component Market generated USD 190.8 million in 2024 and is forecast to grow at a CAGR of 25.1% through 2034. Expansion of cloud services and demand for advanced computing and data processing are driving growth. In addition, continued data center buildouts and upgrades in the U.S. are fueling demand for high-speed interconnect technologies like CXL to support evolving performance and scalability needs.

Key industry players in the Global Compute Express Link (CXL) Component Market include Intel Corporation, Advanced Micro Devices, Inc. (AMD), Samsung Electronics Co., Ltd, Micron Technology, Inc., SK hynix Inc., Rambus Inc., Cadence Design Systems, Inc., Montage Technology Co., Ltd., Astera Labs, Mobiveil, Inc., Marvell Technology, Inc., and Synopsys, Inc. Leading companies in the CXL component market are prioritizing collaboration on open industry standards, strategic partnerships, and product innovation to deepen their market presence. Many are forging alliances with hyperscale data center operators and cloud providers to validate CXL designs and ensure interoperability. R&D investments are focused on enhancing speed, power efficiency, and integration capabilities, especially in SoC-embedded CXL solutions. Firms are also leveraging mergers and acquisitions to broaden their portfolio and technological access. Expanding global manufacturing capabilities and aligning with data center infrastructure roll-outs allow providers to scale with demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on Trade

- 3.2.1.1 Trade Volume Disruptions

- 3.2.1.2 Retaliatory Measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side Impact

- 3.2.2.1.1 Price Volatility in Key Components

- 3.2.2.1.2 Supply Chain Restructuring

- 3.2.2.1.3 Production Cost Implications

- 3.2.2.2 Demand-Side Impact (Selling Price)

- 3.2.2.2.1 Price Transmission to End Markets

- 3.2.2.2.2 Market Share Dynamics

- 3.2.2.2.3 Consumer Response Patterns

- 3.2.2.1 Supply-Side Impact

- 3.2.3 Key Companies Impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on Trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising Demand for Memory Disaggregation

- 3.3.1.2 Acceleration of AI and Machine Learning Workloads

- 3.3.1.3 Adoption of CXL-Compatible Server Platforms

- 3.3.1.4 Emergence of CXL 2.0 and 3.0 Standards

- 3.3.1.5 Growth in Hyperscale and HPC Infrastructure

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High Cost and Supply Chain Complexity

- 3.3.2.2 Software and Ecosystem Readiness Lag

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 CXL switches

- 5.3 Memory expanders

- 5.4 Controllers

- 5.5 Retimers

- 5.6 Network interface card

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Form Factor, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Add-in card

- 6.3 Enterprise and datacenter standard form factor

- 6.4 SoC integrated

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Memory-pooling

- 7.3 Accelerators

- 7.4 Tiered memory architecture

- 7.5 Composable infrastructure

- 7.6 High-speed interconnect

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Workload, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 AI/ML

- 8.3 High performance computing

- 8.4 Data analytics

- 8.5 Cloud computing

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Telecom

- 9.3 Finance

- 9.4 Healthcare

- 9.5 Oil & Gas

- 9.6 Aerospace

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Infrastructure, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 CSP/Hyperscalers

- 10.3 Neoclouds

- 10.4 Enterprise datacenters

- 10.5 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Advanced Micro Devices, Inc. (AMD)

- 12.2 Astera Labs

- 12.3 Cadence Design Systems, Inc.

- 12.4 Intel Corporation

- 12.5 Marvell Technology, Inc.

- 12.6 Micron Technology, Inc.

- 12.7 Microchip Technology Inc.

- 12.8 Mobiveil, Inc.

- 12.9 Montage Technology Co., Ltd.

- 12.10 Rambus Inc.

- 12.11 Samsung Electronics Co., Ltd

- 12.12 SK hynix Inc.

- 12.13 Synopsys, Inc.