シリコン電池市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Silicon Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797696

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

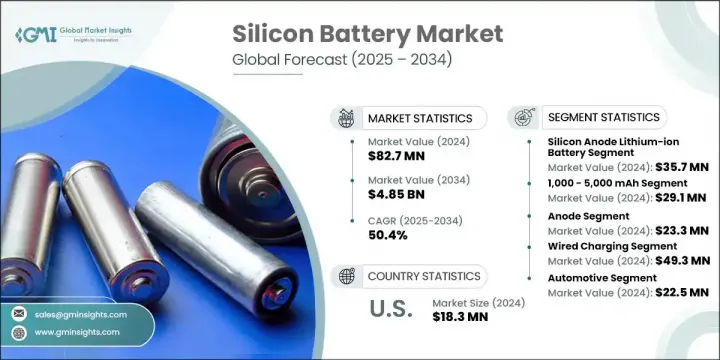

シリコン電池の世界市場規模は、2024年に8,270万米ドルとなり、CAGR 50.4%で成長し、2034年には48億5,000万米ドルに達すると予測されています。

この成長の主な原動力の1つは、エネルギー密度とバッテリー効率が重要な電気自動車(EV)の需要の増加です。シリコン負極は最大3,600 mAh/gの電力を供給でき、標準的なグラファイト負極の372 mAh/gに比べ10倍近く向上しています。この進歩により、航続距離の延長とバッテリーの小型化が可能になり、性能と車両設計が最適化されます。EVの普及が進むと同時に、低排出ガス基準を強化する世界の政策や、重量やコストを増やすことなくバッテリーのスペックを向上させるメーカー主導の取り組みが、シリコンベースのエネルギー・ソリューションへのシフトを加速させています。シリコン電池テクノロジーは、EVから携帯電子機器に至るまで、さまざまな分野のエネルギー貯蔵を再構築する能力として、その認知度を高めています。既存のリチウムイオンインフラストラクチャとの互換性を維持しながら、コンパクトで大容量のエネルギーソリューションを提供できるこの技術は、次世代エネルギー貯蔵の重要な進歩として位置づけられています。

負極セグメントは2024年に3,570万米ドルを生み出しました。この勢いの背景には、既存のリチウムイオン生産システムへのシームレスな統合があります。自動車、家電、据置型エネルギー貯蔵の各分野のメーカーは、現在の製造体制を崩すことなくサイクル寿命やエネルギー密度などの性能指標を向上させるため、シリコン負極に注目しています。最近のシリコンとグラファイトのハイブリッド負極の開発動向は、よりスムーズな商業的スケーラビリティを可能にし、さまざまな分野での市場拡大と応用の可能性を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8,270万米ドル |

| 予測金額 | 48億5,000万米ドル |

| CAGR | 50.4% |

1,000~5,000mAhの電池が2024年に最大のシェアを占め、2,910万米ドルを生み出しました。このセグメントは、スマートフォン、タブレット、スマートウォッチなどの消費者向け機器における軽量かつコンパクトなパワーソリューションに対する需要の高まりにより、成長を続けています。これらのミッドレンジ・シリコンバッテリーは、スペース効率が重要な現代の電子機器に最適で、洗練された製品設計の中で信頼性の高い性能と優れた携帯性を提供します。

米国のシリコン電池市場は、2024年に1,830万米ドルと評価されました。この地域のリーダーシップは、支援的なイノベーション・エコシステム、強固な資金調達チャネル、商業化前の展開のパイプラインが拡大していることに起因しています。この地域のメーカーは、電動モビリティや家電のアプリケーションで全体的な重量を減らしながらエネルギー密度を高めるためのシリコン電池技術を積極的に評価しています。従来の自動車メーカーや新興ハイテクメーカーがバッテリーの技術革新に多額の投資を行う中、次世代シリコン負極ソリューションへのシフトが本格化しています。

シリコン電池市場で事業を展開する主な業界企業には、BYD Company Ltd.、日立製作所、LG Energy Solution、Maxell Holdings, Ltd.、Nanograf Corporation、Nexeon Ltd.、Panasonic Holdings Corporation、Samsung SDI、StoreDot Ltd.、Solid Power, Inc.、Targray Technology International、Toshiba Corporation、QuantumScape Corporation、Novonix Ltd.、OneD Battery Sciences、Group14 Technologies、Enovix Corporation、Sila Nanotechnologies、XNRGI、Enevate Corporationなどがあります。シリコン電池市場での地位を固めるため、企業はいくつかの戦略的イニシアチブを実行しています。その多くは、シリコン負極の化学的性質を改善するための研究開発投資を強化しており、電池寿命と充電保持時間の延長に注力しています。自動車メーカーやエレクトロニクスメーカーとの提携により、市場への浸透と長期的なサプライチェーンの統合が可能になっています。さらに、各社は大量生産に向けた生産ラインの最適化を進める一方で、既存のリチウムイオン電池システムとの互換性を維持し、採用の合理化を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- シリコン陽極の高エネルギー密度

- 電気自動車(EV)の需要急増

- スタートアップ企業と巨大テック企業による商業化

- 先進的エネルギー貯蔵に対する政府のインセンティブ

- VR/ARおよびAI対応トレーニングシステムの導入

- 業界の潜在的リスク&課題

- 体積膨張とサイクル安定性の問題

- 高い製造コスト

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中分析

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- デジタル変革イニシアチブ

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:タイプ別、2021年~2034年

- シリコンアノードリチウムイオン電池

- シリコン固体電池

- シリコングラフェン複合電池

第6章 市場推計・予測:容量範囲別、2021年~2034年

- 1,000mAh未満

- 1,000~5,000mAh

- 5,000~10,000mAh

- 10,000mAh以上

第7章 市場推計・予測:コンポーネント別、2021年~2034年

- カソード

- アノード

- 電解質

- セパレーター

- その他

第8章 市場推計・予測:充電タイプ別、2021年~2034年

- 有線充電

- ワイヤレス充電

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 自動車

- エレクトロニクス

- エネルギーと電力

- ヘルスケア

- 航空宇宙および防衛

- 産業機器

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- BYD Company Ltd.

- Enovix Corporation

- Enevate Corporation

- Group14 Technologies

- Hitachi Ltd.

- LG Energy Solution

- Maxell Holdings Ltd.

- Nanograf Corporation

- Nexeon Ltd.

- Novonix Ltd.

- OneD Battery Sciences

- Panasonic Holdings Corporation

- QuantumScape Corporation

- Samsung SDI

- Sila Nanotechnologies

- Solid Power, Inc.

- StoreDot Ltd.

- Targray Technology International

- Toshiba Corporation

- XNRGI

目次

The Global Silicon Battery Market was valued at USD 82.7 million in 2024 and is estimated to grow at a CAGR of 50.4% to reach USD 4.85 billion by 2034. One of the primary forces behind this growth is the increasing demand for electric vehicles (EVs), where energy density and battery efficiency are crucial. Silicon anodes can deliver up to 3,600 mAh/g, a nearly tenfold boost over standard graphite anodes rated at 372 mAh/g. This advancement enables a greater range and reduced battery size, optimizing performance and vehicle design. Alongside rising EV adoption, global policies enforcing low-emission standards and manufacturer-led efforts to improve battery specs without adding weight or cost are accelerating the shift toward silicon-based energy solutions. Silicon battery technology is increasingly recognized for its capacity to reshape energy storage across multiple sectors, from EVs to portable electronics. The technology's ability to offer compact, high-capacity energy solutions while maintaining compatibility with existing lithium-ion infrastructure positions it as a vital advancement in next-generation energy storage.

The anode segment generated USD 35.7 million in 2024. The reason behind this momentum lies in its seamless integration into existing lithium-ion production systems. Manufacturers across automotive, consumer electronics, and stationary energy storage segments are turning to silicon anodes to enhance performance metrics like cycle life and energy density without disrupting current manufacturing setups. Recent developments in hybrid silicon-graphite anodes are also enabling smoother commercial scalability, helping expand market reach and application potential across various sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $82.7 million |

| Forecast Value | $4.85 billion |

| CAGR | 50.4% |

The batteries within the 1,000 to 5,000 mAh range represented the largest share in 2024, generating USD 29.1 million. This segment continues to thrive due to rising demand for lightweight and compact power solutions in consumer devices like smartphones, tablets, and smartwatches. These mid-range silicon batteries are ideal for modern electronics where space efficiency is critical, offering reliable performance and excellent portability within sleek product designs.

United States Silicon Battery Market was valued at USD 18.3 million in 2024. This regional leadership can be attributed to its supportive innovation ecosystem, robust funding channels, and a growing pipeline of pre-commercial deployments. Local manufacturers are actively assessing silicon battery technologies to enhance energy density while reducing overall weight in electric mobility and consumer electronics applications. As legacy automotive players and emerging tech manufacturers invest heavily in battery innovation, the shift toward next-generation silicon anode solutions is gaining serious traction.

Key industry players operating in the Silicon Battery Market include BYD Company Ltd., Hitachi, Ltd., LG Energy Solution, Maxell Holdings, Ltd., Nanograf Corporation, Nexeon Ltd., Panasonic Holdings Corporation, Samsung SDI, StoreDot Ltd., Solid Power, Inc., Targray Technology International, Toshiba Corporation, QuantumScape Corporation, Novonix Ltd., OneD Battery Sciences, Group14 Technologies, Enovix Corporation, Sila Nanotechnologies, XNRGI, and Enevate Corporation. To solidify their position in the Silicon Battery Market, companies are executing several strategic initiatives. Many are ramping up R&D investments to improve silicon anode chemistry, focusing on increasing battery life and charge retention. Partnerships with automotive and electronics manufacturers are enabling deeper market penetration and long-term supply chain integration. In addition, companies are optimizing production lines for mass-scale manufacturing, while maintaining compatibility with existing lithium-ion battery systems to streamline adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Capacity range trends

- 2.2.3 Component trends

- 2.2.4 Charging type trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High Energy Density of Silicon Anodes

- 3.2.1.2 Surging Demand for Electric Vehicles (EVs)

- 3.2.1.3 Commercialization by Startups and Tech Giants

- 3.2.1.4 Government Incentives for Advanced Energy Storage

- 3.2.1.5 Adoption of VR/AR and AI-enabled training systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volumetric Expansion and Cycle Stability Issues

- 3.2.2.2 High Manufacturing Costs

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Consumer sentiment analysis

- 3.13 Patent and IP analysis

- 3.14 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Silicon anode lithium-ion batteries

- 5.2 Silicon solid-state batteries

- 5.3 Silicon-graphene composite batteries

Chapter 6 Market estimates & forecast, By Capacity Range, 2021 - 2034 (USD Million)

- 6.1 Below 1,000 mAh

- 6.2 1,000-5,000 mAh

- 6.3 5,000-10,000 mAh

- 6.4 Above 10,000 mAh

Chapter 7 Market estimates & forecast, By Component, 2021 - 2034 (USD Million)

- 7.1 Anode

- 7.2 Cathode

- 7.3 Electrolyte

- 7.4 Separator

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Charging Type, 2021 - 2034 (USD Million)

- 8.1 Wired charging

- 8.2 Wireless charging

Chapter 9 Market estimates & forecast, By End Use Industry, 2021 - 2034 (USD Million)

- 9.1 Automotive

- 9.2 Electronics

- 9.3 Energy & power

- 9.4 Healthcare

- 9.5 Aerospace & defense

- 9.6 Industrial equipment

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 BYD Company Ltd.

- 11.2 Enovix Corporation

- 11.3 Enevate Corporation

- 11.4 Group14 Technologies

- 11.5 Hitachi Ltd.

- 11.6 LG Energy Solution

- 11.7 Maxell Holdings Ltd.

- 11.8 Nanograf Corporation

- 11.9 Nexeon Ltd.

- 11.10 Novonix Ltd.

- 11.11 OneD Battery Sciences

- 11.12 Panasonic Holdings Corporation

- 11.13 QuantumScape Corporation

- 11.14 Samsung SDI

- 11.15 Sila Nanotechnologies

- 11.16 Solid Power, Inc.

- 11.17 StoreDot Ltd.

- 11.18 Targray Technology International

- 11.19 Toshiba Corporation

- 11.20 XNRGI

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日