|

市場調査レポート

商品コード

1782162

炎症性腸疾患治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Inflammatory Bowel Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 炎症性腸疾患治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月08日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

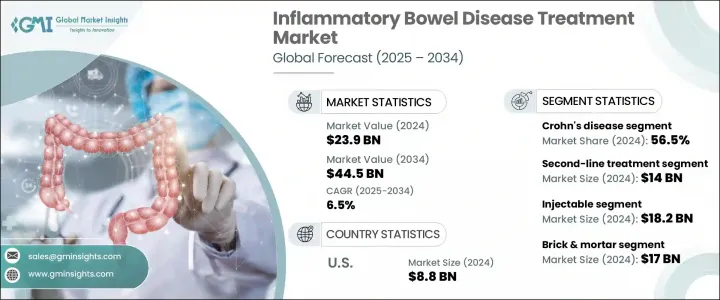

炎症性腸疾患(IBD)治療の世界市場規模は2024年に239億米ドルとなり、CAGR 6.5%で成長し、2034年には445億米ドルに達すると推定されます。

この成長の主な要因は、クローン病や潰瘍性大腸炎を含むIBDの世界の有病率の上昇と、早期診断・治療へのアクセスの拡大です。食生活の変化、座りがちなライフスタイル、環境要因が、特に先進国におけるIBD患者数の増加に寄与しています。啓蒙キャンペーンの強化やより有利な診療報酬体系により、診断率や患者のアドヒアランスが向上しています。

標的生物学的製剤や低分子化合物などの治療アプローチの革新により、治療成績が著しく向上し、治療に関連する合併症が減少しています。公的資金や迅速な薬事審査といった形での開発支援も、次世代療法の開発と普及を後押ししています。患者数が着実に増加する中、QOLを改善し、疾患の再燃を抑える長期的で効果的な解決策に対する需要は高まり続けています。これらの要因が相まって、IBD治療は今後10年間、強固でダイナミックな市場環境を形成することになります。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 239億米ドル |

| 予測金額 | 445億米ドル |

| CAGR | 6.5% |

2024年、クローン病分野は56.5%のシェアを占め、2025~2034年のCAGRは6.3%と予測されます。この拡大は、特に北米と欧州で若年層の間で新たに診断された症例が増加していることが主因です。クローン病は、潰瘍性大腸炎よりも複雑で長期的な治療アプローチを必要とする傾向があります。その結果、ヘルスケアプロバイダーは免疫抑制剤や生物学的製剤といった高価値の治療薬を利用するようになってきています。ヤヌスキナーゼ阻害薬や抗インテグリン薬などの先進的な治療薬クラスの採用が増加していることは、この疾患の管理方法を再定義し、セグメントの成長に大きく寄与しています。

注射療法分野は2024年に182億米ドルと最も高い収益を上げ、2034年までCAGR 6.4%を維持すると予想されています。この分野は、生物製剤、特にモノクローナル抗体の普及が牽引しており、一般に注射によって投与されます。これらの治療薬は、炎症経路を正確に標的とすることで、中等度から重度のIBD治療の基礎となっています。分子レベルで免疫活性を調節する薬剤は、特に従来の薬物療法に反応しない患者において、寛解の維持と疾患の再発の抑制に非常に有効であることが証明されています。長時間作用型の注射剤は、コンプライアンス率の向上や患者の満足度向上にも貢献しています。

米国の炎症性腸疾患治療2024年の市場規模は88億米ドル。クローン病と潰瘍性大腸炎の罹患率が多様な層で上昇していることが、同市場の成長を牽引しています。診断能力の向上、専門医へのアクセス強化、標的治療の拡大などが市場開発を加速させています。長時間作用型の皮下注射剤や徐放性製剤などの革新的なドラッグデリバリー技術が利用可能になったことで、治療のアドヒアランスが向上しています。こうした進歩により、患者は病状を管理しやすくなり、長期的な寛解を維持しやすくなっているため、先進的な治療薬に対する需要がさらに高まっています。

世界の炎症性腸疾患治療市場で事業を展開する主要企業には、Pfizer, Biogen, Takeda, Dr Falk, Johnson & Johnson, CELLTRION, AbbVie, Ferring, Merck, UCB, Novartis, Tillotts Pharma, Lilly, and Amgen.などがあります。これらの企業は、戦略的投資と革新的な医薬品開発を通じて、市場の方向性に影響を与え続けています。IBD治療領域におけるプレゼンスを強化するため、大手製薬企業は研究主導型のイノベーション、規制当局との関与、共同パートナーシップを通じて多面的なアプローチを進めています。

各社は、有効性が向上し副作用の少ない新規の生物学的製剤や低分子を開発するため、臨床試験に多額の投資を行っています。ライセンス契約、合併、買収を通じて製品パイプラインを拡大することも、一般的な戦略となっています。多くの企業が医療当局と緊密に連携し、早期承認の確保と幅広い償還アクセスの確保に努めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- IBDの有病率の増加

- 技術的進歩

- 有利な償還ポリシー

- IBD症状の認識の高まりと早期診断

- 業界の潜在的リスク&課題

- 厳しい規制シナリオ

- 治療費が高め

- 市場機会

- 生物学的製剤と標的療法の採用増加

- 新興市場への拡大

- 促進要因

- 成長可能性分析

- 償還シナリオ

- 規制情勢

- パイプライン分析

- 投資シナリオの見通し

- 治療の切り替えパターンまたは順序の動向

- 疫学的シナリオ

- 将来の市場動向/主な市販治療法

- ブランド分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 企業マトリックス分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:治療の種類別、2021年~2034年

- 主要動向

- クローン病

- 潰瘍性大腸炎

第6章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- 第一選択治療

- アミノサリチル酸塩

- コルチコステロイド

- 第二選択治療

- TNF阻害剤

- IL阻害剤

- JAK阻害剤

- 抗インテグリン

- 併用療法

- TNF阻害剤+ チオプリン

- その他の併用療法

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 注射剤

- 経口

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 店舗

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AbbVie

- Amgen

- Biogen

- CELLTRION

- Dr Falk

- Ferring

- Johnson &Johnson

- Lilly

- Merck

- Novartis

- Pfizer

- Takeda

- Tillotts Pharma

- UCB

The Global Inflammatory Bowel Disease Treatment Market was valued at USD 23.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 44.5 billion by 2034. This growth is primarily driven by a rising global prevalence of IBD, including Crohn's disease and ulcerative colitis, as well as expanding access to early diagnosis and treatment. Changing diets, sedentary lifestyles, and environmental factors are contributing to the increasing number of IBD cases, especially in developed nations. Enhanced awareness campaigns and more favorable reimbursement structures are improving diagnosis rates and patient adherence.

Innovation in treatment approaches-such as targeted biologics and small molecules-has significantly advanced therapeutic outcomes and reduced treatment-related complications. Government support in the form of public funding and faster regulatory reviews is also encouraging the development and uptake of next-generation therapies. With the patient population growing steadily, demand continues to rise for long-term, effective solutions that improve quality of life and reduce disease flare-ups. Collectively, these factors are shaping a robust and dynamic market environment for IBD therapies over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.9 Billion |

| Forecast Value | $44.5 Billion |

| CAGR | 6.5% |

In 2024, the Crohn's disease segment held a 56.5% share and is forecasted to grow at a CAGR of 6.3% during 2025-2034. This expansion is largely attributed to an uptick in newly diagnosed cases among younger individuals, particularly across North America and Europe. Crohn's disease tends to require more complex and long-term treatment approaches than ulcerative colitis, given that it can affect any part of the gastrointestinal tract and penetrate deeper layers of tissue. As a result, healthcare providers are increasingly utilizing high-value therapies such as immunosuppressants and biologics. The growing adoption of advanced treatment classes, including Janus kinase inhibitors and anti-integrin agents, has redefined how the disease is managed and significantly contributed to segment growth.

The injectable therapies segment generated the highest revenue in 2024, valued at USD 18.2 billion, and is expected to maintain a CAGR of 6.4% through 2034. This category is led by the widespread use of biologics, particularly monoclonal antibodies, which are generally delivered via injection. These therapies have become the cornerstone for treating moderate to severe IBD by offering precision targeting of inflammation pathways. Agents that modulate immune activity at the molecular level are proving highly effective in maintaining remission and minimizing disease recurrence, especially for patients unresponsive to traditional medications. Long-acting injectables also contribute to higher compliance rates and improved patient satisfaction.

U.S. Inflammatory Bowel Disease Treatment Market was valued at USD 8.8 billion in 2024. Growth in this market is driven by a rising incidence of both Crohn's disease and ulcerative colitis across diverse demographics. Improved diagnostic capabilities, enhanced access to specialists, and expanding use of targeted therapies are all accelerating market development. The availability of innovative drug delivery technologies, such as long-acting subcutaneous injectables and sustained-release formulations, has improved treatment adherence. These advancements are making it easier for patients to manage their conditions and maintain long-term remission, further boosting demand for advanced therapeutics.

Key players operating in the Global Inflammatory Bowel Disease Treatment Market include Pfizer, Biogen, Takeda, Dr Falk, Johnson & Johnson, CELLTRION, AbbVie, Ferring, Merck, UCB, Novartis, Tillotts Pharma, Lilly, and Amgen. These companies continue to influence market direction through strategic investments and innovative drug development. To strengthen their presence in the IBD treatment space, leading pharmaceutical firms are advancing a multi-pronged approach that includes research-driven innovation, regulatory engagement, and collaborative partnerships.

Companies are investing significantly in clinical trials to develop novel biologics and small molecules with improved efficacy and fewer side effects. Expanding product pipelines through licensing deals, mergers, and acquisitions has also become a common strategy. Many are working closely with health authorities to secure accelerated approvals and ensure broad reimbursement access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of IBD

- 3.2.1.2 Technological advancements

- 3.2.1.3 Favorable reimbursement policies

- 3.2.1.4 Growing awareness and early diagnosis of IBD symptoms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of biologics and targeted therapies

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.6 Pipeline analysis

- 3.7 Investment scenarios outlook

- 3.8 Treatment switching patterns or sequencing trends

- 3.9 Epidemiological scenario

- 3.10 Future market trends/ Key marketed therapies

- 3.11 Brand analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Company matrix analysis

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Crohn's disease

- 5.3 Ulcerative colitis

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 First-line treatment

- 6.2.1 Aminosalicylates

- 6.2.2 Corticosteroids

- 6.3 Second-line treatment

- 6.3.1 TNF inhibitors

- 6.3.2 IL inhibitors

- 6.3.3 JAK inhibitors

- 6.3.4 Anti-integrin

- 6.4 Combination therapy

- 6.4.1 TNF inhibitors + thiopurines

- 6.4.2 Other combination therapies

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Brick & mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 Biogen

- 10.4 CELLTRION

- 10.5 Dr Falk

- 10.6 Ferring

- 10.7 Johnson & Johnson

- 10.8 Lilly

- 10.9 Merck

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Takeda

- 10.13 Tillotts Pharma

- 10.14 UCB