航空転用ガスタービンサービスの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Aeroderivative Gas Turbine Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782155

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

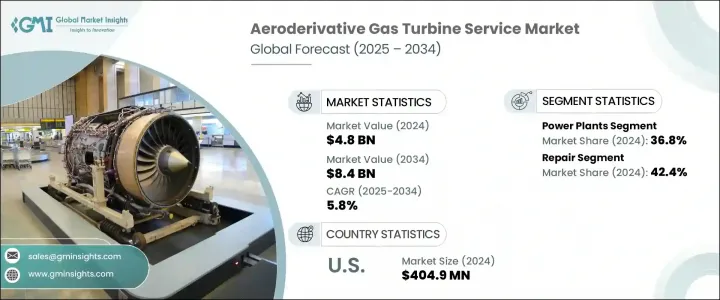

航空転用ガスタービンサービスの世界市場規模は、2024年に48億米ドルとなり、CAGR 9.2%で成長し、2034年には84億米ドルに達すると予測されています。

バイオガスやアンモニアのような低炭素排出燃料によるタービン効率の向上が重視されるようになり、市場の勢いに拍車がかかっています。航空転用タービンは、もともと航空用に設計されたものだが、現在では産業用や発電用に広く転用されており、メンテナンス、オーバーホール、修理などの整備は、タービンの寿命を延ばし、ピーク時の効率を維持するために不可欠です。環境政策が強化され、CO2やNO2の排出量削減が求められる中、事業者は、既存のタービンを完全に交換する代わりに、燃料に柔軟に対応できる燃焼器や低排出ガスバーナーシステムを積極的に導入しています。

長期サービス契約やタービンのリース契約も、事業者の財務リスクを最小化する上で重要な役割を果たしており、予測可能なメンテナンス費用とシステムの稼働時間を保証しています。多くのタービンフリート、特に2005年以前に導入されたタービンの耐用年数は20年を超えており、アップグレード需要の大きな波が押し寄せています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 84億米ドル |

| CAGR | 9.2% |

2024年の発電所セグメントのシェアは36.8%で、2034年までのCAGRは6%と予測されます。特にNOx規制に関連した排出ガスモニタリングと継続的な規制遵守に対する需要の高まりにより、メンテナンス間隔が延長され、サービスニーズが高まっています。タービンの頻繁なサイクル運転、特にピーク負荷運転は、ローターアセンブリや燃料制御システムなどの部品の摩耗を加速させ、さまざまな地域で包括的なサービスサポートの必要性を高めています。

修理サービス分野は2024年に42.4%のシェアを占め、2025年から2034年にかけてCAGR 5.5%で成長すると予測されています。プラズマコーティング、高度な積層造形、精密溶接技術の採用が増加しており、タービンの重要部品の稼働寿命延長に役立っています。これは、耐腐食性部品の需要が急増している海洋・石油・ガス分野で特に重要であり、サービスポートフォリオをさらに強化し、アフターマーケット需要に拍車をかけています。

米国の航空転用ガスタービンサービス市場は2024年に89.6%のシェアを占め、4億490万米ドルを記録しました。人口増加とピーク負荷の増加に伴うエネルギー需要の増加が、多くの場合固定価格保守契約の下で航空転用タービンの展開を加速させています。国の政策支援と、特に政府が支援する主要プログラムの下でエネルギー転換イニシアティブに向けられた資金が、再生可能エネルギー源のバックアップソリューションとして不可欠なこれらのタービンへの関心を高めています。水素燃料およびデュアル燃料タービンプロジェクトの拡大も、技術者トレーニング、燃焼システムのアップグレード、シール交換プログラムへの投資を促し、専門的なタービン整備の需要を強化しています。

主要企業には、Siemens Energy, MAN Energy Solutions, GE Vernova, Ansaldo Energia, and Mitsubishi Heavy Industries. などがあります。市場競争力を強化するため、各社はライフサイクルサポート、イノベーション、ローカライゼーションに重点を置いた多角的戦略を採用しています。大手企業は、タービンのダウンタイムを最小限に抑え、サービス対応力を高めるため、デジタル診断と予知保全プラットフォームに投資しています。グローバルサービスハブを拡大し、リモートモニタリング機能を配備することで、サービス上の問題を迅速に解決することができます。企業はまた、長期サービス契約で事業者と提携し、コストの予測可能性と性能保証を提供しています。専門的な研究開発投資は、クリーンエネルギーの目標に沿うように、低NOx燃焼器、耐腐食性コーティング、燃料柔軟性システムの開発を推進しています。ハイブリッドシステムや水素混合システムの進化する技術的需要に対応するため、人材育成プログラムが強化され、次世代エネルギーインフラへのサービス対応力が確保されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:サービス別、2021年~2034年

- 主要動向

- メンテナンス

- 修理

- オーバーホール

- その他

第6章 市場規模・予測:サービスプロバイダー別、2021年~2034年

- 主要動向

- OEM

- 非OEM

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電所

- 石油・ガス

- プロセスプラント

- 航空

- 海洋

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- オランダ

- フィンランド

- ギリシャ

- デンマーク

- ルーマニア

- ポーランド

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- エジプト

- トルコ

- バーレーン

- イラク

- ヨルダン

- レバノン

- 南アフリカ

- ナイジェリア

- アルジェリア

- ケニア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

- チリ

第9章 企業プロファイル

- Ansaldo Energia

- Centrax Gas Turbines

- Destinus Energy

- EthosEnergy

- GE Vernova

- JSC United Engine

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- MJB International

- MTU Aero Engines

- PROENERGY

- RWG

- Siemens Energy

- Solar Turbines

- Sulzer

- TRS SERVICES

- VERICOR

目次

The Global Aeroderivative Gas Turbine Service Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 8.4 billion by 2034. Growing emphasis on improving turbine efficiency with lower carbon-emission fuels like biogas and ammonia is fueling market momentum. Aeroderivative turbines, originally engineered for aviation, are now widely adapted for industrial and power generation, and their servicing-including maintenance, overhauls, and repairs-is vital to prolong their lifespan and maintain peak efficiency. As tightening environmental policies demand lower CO2 and NO2 emissions, operators are actively retrofitting existing turbines with fuel-flexible combustors and low-emission burner systems instead of replacing units entirely.

Long-term service contracts and turbine leasing arrangements are also playing a significant role in minimizing financial risks for operators, offering predictable maintenance costs and guaranteed system uptime. Many turbine fleets, especially those deployed before 2005, have surpassed two decades of service life, creating a strong wave of upgrade demand that is expected to peak between 2026 and 2030 as global fleets enter critical mid-to-end-of-life cycles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 9.2% |

In 2024, the power plant segment contributed a 36.8% share and is forecast to grow at a CAGR of 6% through 2034. Increasing demand for emission monitoring and ongoing regulatory compliance, particularly related to NOx limits, is extending maintenance intervals and intensifying service needs. Frequent cycling of turbines, especially in peak load operations, is accelerating wear in components like rotor assemblies and fuel control systems, driving up the need for comprehensive service support across various geographies.

The repair services segment held a 42.4% share in 2024 and is anticipated to grow at a CAGR of 5.5% from 2025 to 2034. The rising adoption of plasma coatings, advanced additive manufacturing, and precision welding techniques is helping extend the operational life of critical components in turbines. This is particularly important in the marine and oil & gas sectors, where demand for corrosion-resistant parts is surging, further strengthening the service portfolio and fueling aftermarket demand.

United States Aeroderivative Gas Turbine Service Market held an 89.6% share in 2024 and recorded USD 404.9 million. Rising energy demand tied to population growth and peak load increases has accelerated the deployment of aeroderivative turbines, often under fixed-price maintenance agreements. National policy support and funding directed at energy transition initiatives, especially under major government-backed programs, are driving interest in these turbines as essential backup solutions for renewable sources. The expansion of hydrogen-fueled and dual-fuel turbine projects is also encouraging investment in technician training, combustion system upgrades, and seal replacement programs, strengthening the demand for specialized turbine servicing.

Top industry players include Siemens Energy, MAN Energy Solutions, GE Vernova, Ansaldo Energia, and Mitsubishi Heavy Industries. To enhance their competitiveness in the aeroderivative gas turbine service market, companies are adopting multi-pronged strategies focused on lifecycle support, innovation, and localization. Major players are investing in digital diagnostics and predictive maintenance platforms to minimize turbine downtime and boost service responsiveness. Expanding global service hubs and deploying remote monitoring capabilities allow for quicker resolution of service issues. Firms are also partnering with operators on long-term service contracts to provide cost predictability and performance guarantees. Specialized R&D investments are driving the development of low-NOx combustors, corrosion-resistant coatings, and fuel-flexible systems to align with clean energy goals. Workforce training programs are being ramped up to meet the evolving technical demands of hybrid and hydrogen-blended systems, ensuring service readiness for next-gen energy infrastructures.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Service, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Maintenance

- 5.3 Repair

- 5.4 Overhaul

- 5.5 Others

Chapter 6 Market Size and Forecast, By Service Provider, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 OEM

- 6.3 Non-OEM

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Power plants

- 7.3 Oil & gas

- 7.4 Process plants

- 7.5 Aviation

- 7.6 Marine

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Finland

- 8.3.8 Greece

- 8.3.9 Denmark

- 8.3.10 Romania

- 8.3.11 Poland

- 8.3.12 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Australia

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Thailand

- 8.4.8 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 Bahrain

- 8.5.9 Iraq

- 8.5.10 Jordan

- 8.5.11 Lebanon

- 8.5.12 South Africa

- 8.5.13 Nigeria

- 8.5.14 Algeria

- 8.5.15 Kenya

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Peru

- 8.6.4 Chile

Chapter 9 Company Profiles

- 9.1 Ansaldo Energia

- 9.2 Centrax Gas Turbines

- 9.3 Destinus Energy

- 9.4 EthosEnergy

- 9.5 GE Vernova

- 9.6 JSC United Engine

- 9.7 Kawasaki Heavy Industries

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 MJB International

- 9.11 MTU Aero Engines

- 9.12 PROENERGY

- 9.13 RWG

- 9.14 Siemens Energy

- 9.15 Solar Turbines

- 9.16 Sulzer

- 9.17 TRS SERVICES

- 9.18 VERICOR

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日