ジェネレーティブAIソリューションの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Generative AI solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 187 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782131

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

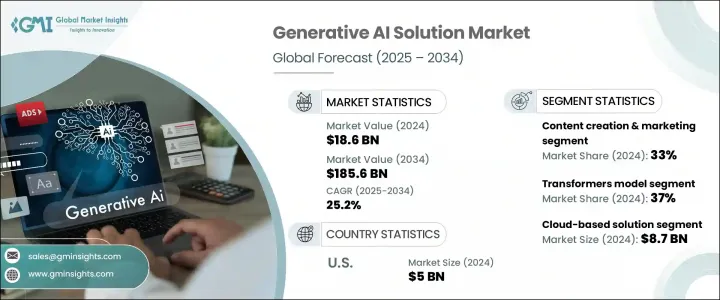

ジェネレーティブAIソリューションの世界市場規模は、2024年に186億米ドルとなり、CAGR 25.2%で成長し、2034年には1,856億米ドルに達すると予測されています。

この市場拡大は、メディア、ヘルスケア、自動車、企業向けソフトウェアなどの業界において、超パーソナライゼーション、自動化、創造的なコンテンツ生成に対する需要が高まっていることが背景にあります。GAN、拡散ネットワーク、大規模言語モデルなど、かつては研究室や創造的なニッチに限られていた生成モデルは、企業のイノベーション努力の中心となっています。厳格なルールに従った従来のAIは、人間のようなテキスト、画像、音声、コードを生成できる生成システムに取って代わられつつあります。この進化は効率化を促進し、設計プロセスを強化し、製品体験を豊かにしています。アプリケーションに特化した企業と大手AI研究所とのコラボレーションが、採用を加速させています。

その結果、明確な業界の課題に合わせた業界別ソリューションが主流になりつつあり、分野に合わせたAI実装へのシフトを示唆しています。この増加傾向は、精密性、関連性、実世界での適用性を求める幅広い業界の需要を反映しており、画一的なモデルではもはや複雑な業務ニーズに対応できなくなっています。組織は、規制環境、データの種類、顧客の期待に密接に合致するAIツールを優先する傾向が強まっています。金融、ヘルスケアから小売、製造に至るまで、これらのドメインに最適化されたAIシステムは、より迅速な展開、意思決定の強化、投資収益率の向上を可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 186億米ドル |

| 予測金額 | 1,856億米ドル |

| CAGR | 25.2% |

トランスフォーマーベースのモデルセグメントは、2024年に37%のシェアを占め、2034年まで26%のCAGRで成長すると予測されます。これらのアーキテクチャは、GPT、PaLM、LLaMA、Claudeなど、ほぼすべての最新のジェネレーティブソリューションを支えています。そのスケーラビリティ、柔軟性、パフォーマンスにより、業界全体で広く採用されています。Transformersは現在、オフィスソフトウェア、コード生成ツール、法律、金融、マーケティングなどの分野におけるエンタープライズアプリケーションのAIコパイロットを駆動しており、ジェネレーティブAIのバックボーンとしての地位を確固たるものにしています。

コンテンツ作成とマーケティングは2024年に33%のシェアを占め、2025年から2034年にかけてCAGR 25%で成長すると予測されています。SEOに最適化されたブログ記事、広告キャンペーン、商品説明、電子メールコンテンツ、販促用マルチメディアを大規模に作成するために、企業はますますジェネレーティブツールに依存しています。これらのシステムは、マーケティング担当者がブランドトーンを維持しながらワークフローを自動化し、消費者インサイトに基づいてカスタマイズされたメッセージを配信するのに役立ちます。このシフトにより、ブランドは増大するコンテンツ需要に効率的に対応し、エンゲージメントを向上させ、キャンペーンパフォーマンスを最適化することができます。

米国のジェネレーティブAIソリューション市場は85%のシェアを占め、2024年には50億米ドルを生み出します。このリーダーシップは、豊富な技術インフラ、先進的な学術・企業研究環境、官民による多額の投資に起因します。米国には主要なAIイノベーターが本社を構え、世界トップクラスの大学、新興企業、研究ハブによって支えられているため、米国は大規模な生成トランスフォーマーの開発と展開の最前線にあり続けています。

この市場の主要企業には、 Google, NVIDIA, Adobe, Amazon Web Services, Microsoft, IBM, and OpenAI.が含まれます。これらの企業はイノベーションを推進し、業界の戦略的方向性を定めています。市場の優位性を確固たるものにするため、ジェネレーティブAI分野の主要企業はいくつかの中核戦略を追求しています。第一に、テキスト、画像、音声、動画機能を融合した次世代アーキテクチャやマルチモーダルモデルの研究開発を積極的に拡大しています。第二に、業界に特化したリーダー企業とのパートナーシップにより、ヘルスケア診断から自動車設計に至るまで、各業界のニーズに合わせたソリューションを実現しています。第三に、オープンAPI、開発者向けプラットフォーム、フリーミアムサービスの提供など、AIへのアクセスを民主化する取り組みが、ユーザーのエンゲージメントを広げ、普及を加速させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 電子部品サプライヤー

- 機器メーカー

- サービスプロバイダー

- システムインテグレーター

- 最終用途

- コスト構造

- 利益率

- 各段階での付加価値

- サプライチェーンに影響を与える要因

- 破壊者

- サプライヤーの情勢

- 影響要因

- 促進要因

- 自動化と効率化に対する企業の需要の高まり

- マーケティングと顧客体験におけるハイパーパーソナライゼーション

- 企業機能全体にわたるAIエージェントとコパイロットの拡張

- モデル機能の進歩

- クラウドの可用性と戦略的パートナーシップ

- 業界の潜在的リスク&課題

- ハルシネーションと不正確な出力

- データのプライバシーとセキュリティリスク

- 市場機会

- 垂直特化型大規模言語モデル(LLM)

- マルチモーダルジェネレーティブAIソリューション(テキスト+ 画像+ 音声+ ビデオ)

- 中小企業におけるSaaSベースのGenAI導入

- AIを活用したコード生成とDevOps自動化

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術

- トランスフォーマーベースの大規模言語モデル(LLM)

- 生成的敵対ネットワーク(GAN)

- 拡散モデル

- 変分オートエンコーダ(VAE)

- 新興技術

- マルチモーダルジェネレーティブAIソリューション

- 検索拡張生成(RAG)システム

- ローコード/ノーコードGenAI開発プラットフォーム

- 安全性、アライメント、評価ツールキット

- 現在の技術

- 特許分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- コスト内訳分析

- 持続可能性分析

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- 技術の進化とイノベーションのロードマップ

- ファンデーションモデルと大規模言語モデル(LLM)

- マルチモーダルAIシステム

- 特殊なGENAIアプリケーション

- 新興技術と将来の発展

- 価格モデルと収益化戦略

- GenAIの価格モデルの進化

- サブスクリプションベースの価格分析

- フリーミアムと無料層戦略

- エンタープライズライセンシングとカスタム価格設定

- 収益の最適化と収益化の動向

- 価格競争分析

- 将来の価格モデルの進化

- 企業での導入と実装

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- トランスフォーマーモデル

- テキスト生成

- コード生成

- 要約

- 質問回答(Q&A)

- マルチモーダルトランスフォーマー(テキスト+画像/ビデオ)

- 生成的敵対ネットワーク(GAN)

- 画像生成

- ビデオ生成

- 条件付き

- 超解像度

- スタイルの転送

- 拡散モデル

- 画像合成

- ビデオ合成

- テキストから画像への拡散

- インペインティング/編集ツール

- クリエイティブデザインモデル

- 変分オートエンコーダ(VAE)

- 潜在空間生成

- セマンティックデータモデリング

- 異常検出生成

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コンテンツ作成とマーケティング

- デジタルマーケティングと広告

- ソーシャルメディアコンテンツ生成

- ブログや記事の執筆

- クリエイティブデザインとメディア制作

- カスタマーサービスとサポート

- AIチャットボットとバーチャルアシスタント

- 自動応答システム

- 顧客からの問い合わせ解決

- 多言語サポートソリューション

- ソフトウェア開発とIT

- コード生成と補完

- バグの検出と解決

- ドキュメント生成

- API開発とテスト

- 調査と分析

- データ分析と洞察の生成

- 科学調査支援

- 市場調査と競合情報

- 財務分析と報告

- 教育と訓練

- 評価ツール

- 専門スキル開発

- その他

第7章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

- ハイブリッド

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- ヘルスケアとライフサイエンス

- 医薬品の発見と開発

- 医療画像診断

- 臨床文書と記録

- 患者ケアと遠隔医療

- 金融サービスと銀行

- リスク評価と管理

- 不正行為の検出と防止

- 投資調査と分析

- 顧客サービスの自動化

- 教育とeラーニング

- パーソナライズされた学習プラットフォーム

- コンテンツ作成とカリキュラム開発

- 学生の評価と評価

- 管理プロセスの自動化

- メディアとエンターテイメント

- コンテンツの作成と制作

- ゲームとインタラクティブメディア

- 音楽とオーディオの生成

- 視覚効果とアニメーション

- 法律および専門サービス

- 契約書の作成と管理

- コンプライアンスと規制サポート

- 小売業とeコマース

- 顧客体験のパーソナライゼーション

- マーケティングと広告の最適化

- 製造業と工業

- 品質管理と検査

- 予測保守ソリューション

- その他

第9章 市場推計・予測:組織規模別、2021 -2034

- 主要動向

- 大企業

- 中小企業

第10章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Adobe

- Amazon Web Services(AWS)

- Apple

- Anthropic

- Baidu

- DeepMind

- Genie AI

- IBM

- Intel

- Meta

- Microsoft

- MOSTLY AI

- NVIDIA

- OpenAI

- Oracle

- Salesforce

- SAP

- Synthesia

- UiPath

- Unity Technologies

目次

The Global Generative AI solution Market was valued at USD 18.6 billion in 2024 and is estimated to grow at a CAGR of 25.2% to reach USD 185.6 billion by 2034. The expansion is driven by increased demand for hyper-personalization, automation, and creative content generation across industries like media, healthcare, automotive, and enterprise software. Generative models, once confined to labs and creative niches-such as GANs, diffusion networks, and large language models-have become central to corporate innovation efforts. Traditional AI that followed rigid rules is being replaced by generative systems capable of producing human-like text, images, audio, and code. This evolution is driving efficiency, enhancing design processes, and enriching product experiences. Collaborations between application-focused firms and leading AI labs are accelerating adoption.

As a result, vertical-specific solutions tailored to distinct industry challenges are becoming the norm, signaling a shift towards sector-tailored AI implementations. This growing trend reflects a broader industry demand for precision, relevance, and real-world applicability, where one-size-fits-all models no longer meet complex operational needs. Organizations are increasingly prioritizing AI tools that align closely with their regulatory environments, data types, and customer expectations. From finance and healthcare to retail and manufacturing, these domain-optimized AI systems are enabling faster deployment, enhanced decision-making, and better return on investment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.6 Billion |

| Forecast Value | $185.6 Billion |

| CAGR | 25.2% |

The transformer-based models segment held a 37% share in 2024 and is expected to grow at a CAGR of 26% through 2034. These architectures underpin nearly all modern generative solutions, such as GPT, PaLM, LLaMA, and Claude. Their scalability, flexibility, and performance have enabled widespread adoption across industries. Transformers now power AI copilots in office software, code generation tools, and enterprise applications in sectors such as legal, finance, and marketing, cementing their position as the backbone of generative AI.

Content creation and marketing held a 33% share in 2024 and is forecast to grow at a CAGR of 25% from 2025 to 2034. Businesses increasingly rely on generative tools to produce SEO-optimized blog posts, ad campaigns, product descriptions, email content, and promotional multimedia at scale. These systems help marketers automate workflows while maintaining brand tone and delivering tailored messaging based on consumer insights. This shift is helping brands efficiently meet growing content demands, improve engagement, and optimize campaign performance.

U.S. Generative AI Solution Market held 85% share and generated USD 5 billion in 2024. This leadership stems from a rich tech infrastructure, advanced academic and corporate research environments, and substantial public-private investment. With major AI innovators headquartered in the U.S., supported by world-class universities, startups, and research hubs, the country remains at the forefront of generative transformer development and deployment at scale.

Leading firms in this market include Google, NVIDIA, Adobe, Amazon Web Services, Microsoft, IBM, and OpenAI. These companies are driving innovation and setting strategic direction for the industry. To solidify their market dominance, major players in the generative AI space are pursuing several core strategies. First, they are aggressively expanding R&D into next-generation architectures and multimodal models that fuse text, image, audio, and video capabilities. Second, partnerships with industry-specific leaders enable tailored solutions that meet vertical needs, from healthcare diagnostics to automotive design. Third, efforts to democratize AI access, such as offering open APIs, developer platforms, and freemium services, are widening user engagement and accelerating adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 Deployment

- 2.2.5 End use industry

- 2.2.6 Organization size

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Electronic component suppliers

- 3.1.1.2 Equipment manufacturers

- 3.1.1.3 Service providers

- 3.1.1.4 System integrators

- 3.1.1.5 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising enterprise demand for automation and efficiency

- 3.2.1.2 Hyper personalization in marketing and customer experience

- 3.2.1.3 Expansion of AI agents and Copilots across enterprise functions

- 3.2.1.4 Advancements in model capabilities

- 3.2.1.5 Cloud availability and strategic partnerships

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Hallucinations and inaccurate output

- 3.2.2.2 Data privacy and security risks

- 3.2.3 Market Opportunities

- 3.2.3.1 Vertical-specific large language models (LLMs)

- 3.2.3.2 Multimodal Generative AI solution (Text + Image + Audio + Video)

- 3.2.3.3 SaaS-based GenAI adoption among SMEs

- 3.2.3.4 AI-powered code generation & DevOps automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.1.1 Transformer-based large language models (LLMs)

- 3.6.1.2 Generative adversarial networks (GANs)

- 3.6.1.3 Diffusion models

- 3.6.1.4 Variational autoencoders (VAEs)

- 3.6.2 Emerging technologies

- 3.6.2.1 Multimodal Generative AI solution

- 3.6.2.2 Retrieval-Augmented Generation (RAG) Systems

- 3.6.2.3 Low-Code/No-Code GenAI Development Platforms

- 3.6.2.4 Safety, Alignment & Evaluation Toolkits

- 3.6.1 Current technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Cost breakdown analysis

- 3.10 Sustainability analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Technology evolution and innovation roadmap

- 3.11.1 Foundation models and large language models (LLMs)

- 3.11.2 Multimodal AI systems

- 3.11.3 Specialized GENAI applications

- 3.11.4 Emerging technologies and future developments

- 3.12 Pricing models and monetization strategies

- 3.12.1 GenAI pricing model evolution

- 3.12.2 Subscription-based pricing analysis

- 3.12.3 Freemium and free tier strategies

- 3.12.4 Enterprise licensing and custom pricing

- 3.12.5 Revenue optimization and monetization trends

- 3.12.6 Pricing competitive analysis

- 3.12.7 Future pricing model evolution

- 3.13 Enterprise adoption and implementation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Transformers model

- 5.2.1 Text generation

- 5.2.2 Code generation

- 5.2.3 Summarization

- 5.2.4 Question answering (Q&A)

- 5.2.5 Multimodal transformers (text+ image/video)

- 5.3 Generative adversarial networks (GAN)

- 5.3.1 Image generation

- 5.3.2 Video generation

- 5.3.3 Conditional

- 5.3.4 Super resolution

- 5.3.5 Style transfer

- 5.4 Diffusion models

- 5.4.1 Image synthesis

- 5.4.2 Video synthesis

- 5.4.3 Text-to-image diffusion

- 5.4.4 Inpainting/ editing tools

- 5.4.5 Creative design models

- 5.5 Variational autoencoders (VAEs)

- 5.5.1 Latent space generation

- 5.5.2 Semantic data modelling

- 5.5.3 Anomaly detection generation

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Content creation and marketing

- 6.2.1 Digital marketing and advertising

- 6.2.2 Social media content generation

- 6.2.3 Blog and article writing

- 6.2.4 Creative design and media production

- 6.3 Customer service and support

- 6.3.1 AI chatbots and virtual assistants

- 6.3.2 Automated response systems

- 6.3.3 Customer query resolution

- 6.3.4 Multilingual support solutions

- 6.4 Software development and IT

- 6.4.1 Code Generation and Completion

- 6.4.2 Bug Detection and Resolution

- 6.4.3 Documentation Generation

- 6.4.4 API development and testing

- 6.5 Research and analytics

- 6.5.1 Data analytics and insights generation

- 6.5.2 Scientific research assistance

- 6.5.3 Market research and competitive intelligence

- 6.5.4 Financial analysis and reporting

- 6.6 Education and training

- 6.6.1 Assessment and evaluation tools

- 6.6.2 Professional skills development

- 6.6.3 Others

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Healthcare and life sciences

- 8.2.1 Drug discovery and development

- 8.2.2 Medical imaging and diagnostics

- 8.2.3 Clinical documentation and records

- 8.2.4 Patient care and telemedicine

- 8.3 Financial services and banking

- 8.3.1 Risk assessment and management

- 8.3.2 Fraud detection and prevention

- 8.3.3 Investment research and analysis

- 8.3.4 Customer service automation

- 8.4 Education and E-learning

- 8.4.1 Personalized learning platforms

- 8.4.2 Content creation and curriculum development

- 8.4.3 Student assessment and evaluation

- 8.4.4 Administrative process automation

- 8.5 Media and entertainment

- 8.5.1 Content creation and production

- 8.5.2 Gaming and interactive media

- 8.5.3 Music and audio generation

- 8.5.4 Visual effects and animation

- 8.6 Legal and professional services

- 8.6.1 Contract generation and management

- 8.6.2 Compliance and regulatory support

- 8.7 Retail and E-commerce

- 8.7.1 Customer experience personalization

- 8.7.2 Marketing and advertising optimization

- 8.8 Manufacturing and Industrial

- 8.8.1 Quality control and inspection

- 8.8.2 Predictive maintenance solutions

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Large Enterprises

- 9.3 Small and Medium Enterprises (SMEs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 South Korea

- 10.3.5 Australia

- 10.3.6 Singapore

- 10.3.7 Malaysia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Adobe

- 11.2 Amazon Web Services (AWS)

- 11.3 Apple

- 11.4 Anthropic

- 11.5 Baidu

- 11.6 DeepMind

- 11.7 Genie AI

- 11.8 Google

- 11.9 IBM

- 11.10 Intel

- 11.11 Meta

- 11.12 Microsoft

- 11.13 MOSTLY AI

- 11.14 NVIDIA

- 11.15 OpenAI

- 11.16 Oracle

- 11.17 Salesforce

- 11.18 SAP

- 11.19 Synthesia

- 11.20 UiPath

- 11.21 Unity Technologies

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 187 Pages

- 納期

- 2~3営業日