腸溶性空カプセルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Enteric Empty Capsules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782113

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

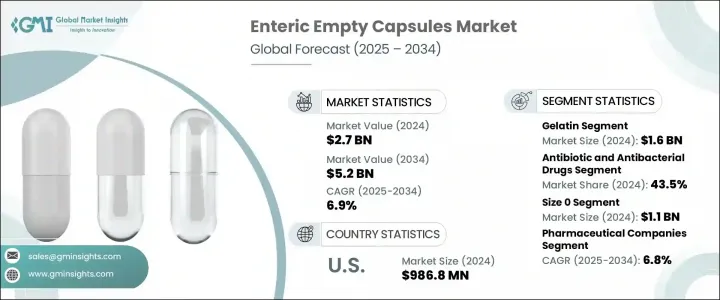

世界の腸溶性空カプセル市場は、2024年には27億米ドルと評価され、CAGR 6.9%で成長し、2034年には52億米ドルに達すると推定されています。

この急成長の背景には、医薬品や栄養補助食品の活性化合物の標的を絞った遅延放出を確実にする高度なドラッグデリバリーシステムに対するニーズの高まりがあります。胃酸から敏感な成分を保護し、腸に直接送達する腸溶性カプセルは、胃腸薬や酸に敏感な治療にとって重要です。その汎用性は抗生物質、制酸剤、酵素治療にも及び、最新の製剤には欠かせない要素となっています。

個別化医療と患者中心の設計の急速な成長は、製剤の柔軟性と多様な有効成分との適合性のおかげで、需要をさらに押し上げています。拡大する栄養補助食品の分野では、腸溶性カプセル(特にHPMCベースのビーガン対応タイプ)がプロバイオティクス、酵素、ハーブサプリメントの送達にますます支持されています。クリーンラベルで植物由来の選択肢が好まれるため、製造業者はシリコーンを含まないベジタリアン用カプセルへの投資を促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 27億米ドル |

| 予測金額 | 52億米ドル |

| CAGR | 6.9% |

ゼラチンセグメントは2024年に16億米ドルを生み出しました。その手頃な価格、フィルム形成の品質、製造の容易さにより、大規模カプセル製造、特に非ベジタリアン製剤が許容される場合のデフォルトの選択肢となっています。その規制上の利便性と様々な原薬との適合性により、多くの医薬品・サプリメント製造業者にとって最良の選択肢となっています。

腸溶性空カプセルは、2024年に43.5%のシェアを占める抗生物質・抗菌薬セグメントに採用されています。これらのカプセルは酸に弱い抗生物質を胃での分解から守り、腸での最適な吸収を保証します。また、副作用を最小限に抑え、特定の薬剤の不快な味をマスキングし、患者の服薬アドヒアランスと治療の成功を向上させる。

米国の腸溶性空カプセル2024年の市場規模は9億8,680万米ドルで、何千万人もの人々に影響を及ぼしている胃腸疾患の広がりと、成人のサプリメント摂取の堅調さに牽引されています。FDA(米国食品医薬品局)やUSDA(米国農務省)などの機関による規制の明確化が、pH依存性および遅延放出カプセル技術の迅速な開発と採用を後押ししています。

この業界の主要メーカーには、Lonza、Roquette Freres、Chemcaps、Bright Pharma Caps、Qingdao Yiqing、ACG Worldwide、Natural Capsules、Yiyang Pharma、Capsuline、Shaoxing Zhongya Capsule、Fortcaps Healthcare、CapsCanada、Suheung、Zhejiang Huili Capsulesなどがあります。市場ポジションを強化するため、腸溶性空カプセル分野の主要メーカーはいくつかの重要な戦略を展開しています。HPMCや植物由来ポリマーなど、健康志向の消費者にアピールし、規制基準を満たす革新的なカプセル素材を開発するため、研究開発に投資しています。

製薬会社や栄養補助食品会社との戦略的パートナーシップは、特定の原薬や送達システムに合わせたカスタマイズソリューションの共同開発を促進しています。多くの企業は、サプライチェーンの効率を向上させるため、生産能力を拡大し、地域のハブにより近い場所に施設を設立しています。クリーンラベル、ビーガンフレンドリー認証、透明性の高い製造工程を重視することで、倫理的で安全な製品を求める消費者の要望に応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 標的ドラッグデリバリーの需要増加

- ベジタリアンカプセル代替品への移行が増加

- 個別化医療ソリューションの拡大

- カプセルコーティング技術の進歩

- 業界の潜在的リスク&課題

- 腸溶製剤の規制の複雑さ

- 高い製造コストとコーティングコスト

- 市場機会

- 栄養補助食品の消費が世界的に増加

- 新興経済諸国における市販薬とサプリメントの需要増加

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 消費者行動分析

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ゼラチンカプセル

- 非ゼラチンカプセル

- HPMC(ヒドロキシプロピルメチルセルロース)

- プルランカプセル

- デンプンベースのカプセル

- その他の非ゼラチンカプセル

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 制酸剤および整腸剤

- 抗生物質および抗菌薬

- その他の用途

第7章 市場推計・予測:カプセルサイズ別、2021年~2034年

- 主要動向

- サイズ00

- サイズ0

- サイズ1

- その他のカプセルサイズ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬会社

- 栄養補助食品メーカー

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ACG Worldwide

- Bright Pharma Caps

- CapsCanada

- Capsuline

- Chemcaps

- Fortcaps Healthcare

- Lonza

- Natural Capsules

- Qingdao Yiqing

- Roquette Freres

- Shaoxing Zhongya Capsule

- Suheung

- Yiyang Pharma

- Zhejiang Huili Capsules

目次

The Global Enteric Empty Capsules Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 5.2 billion by 2034. This surge is being driven by the increasing need for advanced drug delivery systems that ensure targeted, delayed release of active pharmaceutical and nutraceutical compounds. By shielding sensitive ingredients from stomach acidity and delivering them directly to the intestines, enteric capsules are critical for gastrointestinal medications and acid-sensitive therapies. Their versatility extends to antibiotics, antacids, and enzyme treatments, making them an essential component of modern formulations.

The rapid growth of personalized medicine and patient-centric design is further boosting demand, thanks to formulation flexibility and compatibility with diverse active ingredients. In the expanding nutraceutical arena, enteric capsules-especially HPMC-based, vegan-friendly types-are increasingly favored for probiotic, enzyme, and herbal supplement delivery. The preference for clean-label, plant-based options is prompting manufacturers to invest in silicone-free, vegetarian capsule alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 6.9% |

The Gelatin segment generated USD 1.6 billion in 2024. Its affordability, film-forming quality, and ease of production make it the default choice for large-scale capsule manufacturing, especially where non-vegetarian formulations are acceptable. Its regulatory convenience and compatibility with a variety of APIs make it a top choice for many pharmaceutical and supplement producers.

Enteric empty capsules are employed in the antibiotic and antibacterial drugs segment, which held a 43.5% share in 2024. These capsules protect acid-sensitive antibiotics from gastric degradation, ensuring optimal absorption in the intestines. They also help minimize side effects and mask the unpleasant taste of certain medications, improving patient adherence and treatment success.

U.S. Enteric Empty Capsules Market accounted for USD 986.8 million in 2024, driven by widespread gastrointestinal conditions affecting tens of millions of people, and a robust supplement intake among adults. Regulatory clarity from agencies like the FDA and USDA supports fast-track development and adoption of pH-dependent and delayed-release capsule technologies.

Key manufacturers in this industry include Lonza, Roquette Freres, Chemcaps, Bright Pharma Caps, Qingdao Yiqing, ACG Worldwide, Natural Capsules, Yiyang Pharma, Capsuline, Shaoxing Zhongya Capsule, Fortcaps Healthcare, CapsCanada, Suheung, and Zhejiang Huili Capsules. To bolster their market position, leading manufacturers in the enteric empty capsules space are deploying several key strategies. They're investing in R&D to develop innovative capsule materials-such as HPMC and plant-based polymers-that appeal to health-conscious consumers and meet regulatory standards.

Strategic partnerships with pharmaceutical and nutraceutical firms facilitate the co-development of customized solutions tailored to specific APIs and delivery systems. Many companies are expanding production capacities and establishing facilities closer to regional hubs to improve supply chain efficiency. Emphasis on clean-label, vegan-friendly certification, and transparent manufacturing processes addresses consumer demand for ethical and safe products.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Capsule size

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for targeted drug delivery

- 3.2.1.2 Growing shift toward vegetarian capsule alternatives

- 3.2.1.3 Expansion of personalized medicine solutions

- 3.2.1.4 Advancements in capsule coating technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexity for enteric formulations

- 3.2.2.2 High production and coating costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing consumption of nutraceutical globally

- 3.2.3.2 Increasing demand for over-the-counter medications and supplements in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Consumer behaviour analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East and Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gelatin capsules

- 5.3 Non-gelatin capsules

- 5.3.1 HPMC (hydroxypropyl methylcellulose)

- 5.3.2 Pullulan capsules

- 5.3.3 Starch-based capsules

- 5.3.4 Other non-gelatin capsules

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Antacid and antiflatulent preparations

- 6.3 Antibiotic and antibacterial drugs

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By Capsule Size, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Size 00

- 7.3 Size 0

- 7.4 Size 1

- 7.5 Other capsule size

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical companies

- 8.3 Nutraceutical manufacturers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ACG Worldwide

- 10.2 Bright Pharma Caps

- 10.3 CapsCanada

- 10.4 Capsuline

- 10.5 Chemcaps

- 10.6 Fortcaps Healthcare

- 10.7 Lonza

- 10.8 Natural Capsules

- 10.9 Qingdao Yiqing

- 10.10 Roquette Freres

- 10.11 Shaoxing Zhongya Capsule

- 10.12 Suheung

- 10.13 Yiyang Pharma

- 10.14 Zhejiang Huili Capsules

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日