|

|

市場調査レポート

商品コード

1782099

磁歪材料の市場機会、成長促進要因、産業動向分析、2025~2034年予測Magnetostrictive Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 磁歪材料の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年07月01日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

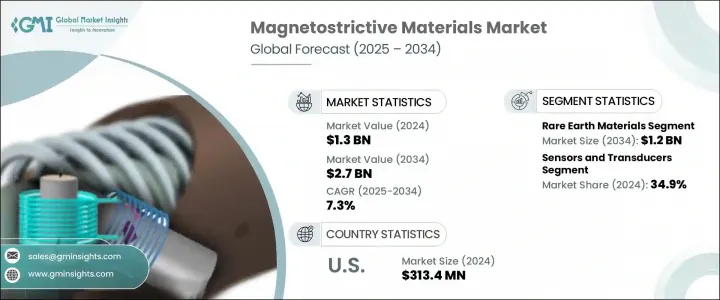

磁歪材料の世界市場は、2024年には13億米ドルとなり、CAGR 7.3%で成長し、2034年には27億米ドルに達すると予測されています。

磁歪材料の需要は、磁界を受けると形状やサイズが変化するユニークな能力により高まっており、先端技術アプリケーションに不可欠なものとなっています。その用途は、自動車、ヘルスケア、航空宇宙、家電など様々な分野に及んでいます。自動車分野では、センサーやアクチュエータ、特にパワーステアリングシステムに不可欠な材料として、自動車の性能、効率、安全性を高めています。

電気自動車やハイブリッド車の成長が、この市場をさらに後押ししています。ヘルスケア・アプリケーションは、その卓越した精度から大きな恩恵を受けており、より正確な診断や患者の転帰を改善する標的治療を可能にしています。一方、航空宇宙産業は、効果的な振動制御と継続的な構造健全性監視のためにこれらの材料を利用し、重要な部品の安全性と性能を確保しています。このように、各分野にまたがる二重の有用性は、その応用範囲を広げるだけでなく、業界が進化する技術的課題に対応するための信頼性の高い高性能ソリューションを求めているため、市場の需要を大幅に増幅しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 27億米ドル |

| CAGR | 7.3% |

希土類材料セグメントは、2024年に5億8,950万米ドルを生み出し、2034年には12億米ドルに達すると予測されています。テルビウムのような希土類元素が優れた磁気特性と高い磁気係数を提供するため、このセグメントが優位を占めています。これらの特性により、センサー、アクチュエータ、変圧器など、精度と効率が要求される用途に最適です。自動車、航空、家電の各分野で先端技術の採用が増加していることが、希土類ベースの磁歪材料の成長を後押ししています。

センサーとトランスデューサーは2024年に34.9%のシェアを占め、最大の用途分野となっています。磁歪材料は、磁気エネルギーを機械エネルギーに変換する能力、またはその逆の能力で珍重され、センサーやトランスデューサの製造に最適です。高感度、高耐久性、高精度であるため、自動車や民生用電子機器に不可欠な部品となっています。

米国の磁歪材料市場は2024年に3億1,340万米ドルを生み出しました。この成長の原動力は、センサー、アクチュエータ、変圧器など、さまざまな産業用途でこれらの材料の使用が増加していることです。製造、自動車、航空宇宙などの業界では、操作の正確性と効率を向上させるために磁歪材料を利用しています。産業オートメーションでは、磁歪センサーが精密な位置や変位の測定に広く使用されています。自動化への継続的な注力と高度なセンシング技術への需要が、予測期間を通じて市場の成長を後押しすると予想されます。

磁歪材料市場の主要企業には、Cedrat Technologies、TdVib LLC、Grirem Advanced Materials Co.Ltd.、Metglas Inc.、Aperam S.A.などがあります。市場での地位を強化し競争上の優位性を獲得するため、これらのメーカーは革新的な製品の発売、生産能力の拡大、M&Aなどの戦略を追求しています。

足場を固め、市場でのプレゼンスを拡大するため、磁歪材料分野の企業はいくつかの主要な戦略的アプローチに注力しています。これには、進化する業界のニーズに対応する革新的で高性能な素材を導入するための研究開発への多額の投資が含まれます。また、特に自動車や航空宇宙のような急速に発展している分野からの需要の増加に対応するために、生産能力の拡大を優先しています。M&Aは、各社の製品ポートフォリオと地理的範囲を広げるのに役立ち、戦略的パートナーシップは、新しい技術と市場へのアクセスを可能にします。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場規模・予測:材料別、2021年~2034年

- 主要動向

- 希土類材料

- テルフェノール-D(Tb-Dy-Fe)

- サマリウム鉄化合物

- その他の希土類元素

- 鉄基合金

- ガルフェノール(Fe-Ga)

- アルフェノール(Fe-Al)

- その他の鉄基合金

- ニッケル基合金

- ニッケル鉄合金

- その他のニッケル基合金

- コバルト基合金

- その他の材料

第6章 市場規模・予測:形態別、2021年~2034年

- 主要動向

- バルク材料

- ロッド

- プレート

- ブロック

- その他のバルク形態

- 薄膜

- 複合材料

- 粒子複合材料

- 積層複合材

- その他の複合形

- 粉末

- その他の形態

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- センサーとトランスデューサー

- 力とトルクセンサー

- 位置および変位センサー

- 応力および歪みセンサー

- 磁場センサー

- 音響および超音波トランスデューサー

- その他のセンサーとトランスデューサー

- アクチュエータとモーションコントロール

- リニアアクチュエータ

- ロータリーアクチュエータ

- 精密測位システム

- 振動制御システム

- その他のアクチュエータ用途

- エネルギーハーベスティングシステム

- 振動エネルギーハーベスター

- 音響エネルギーハーベスター

- その他のエネルギーハーベスター用途

- ソナーと水中音響

- 構造健全性モニタリング

- その他の用途

第8章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- エンジンおよびパワートレイン用途

- サスペンションおよびシャーシ用途

- センサー用途

- その他の自動車用途

- 航空宇宙および防衛

- 航空機システム

- 防衛用途

- 宇宙用途

- その他の航空宇宙および防衛用途

- エネルギーと電力

- エネルギーハーベスティング

- 発電

- その他のエネルギーおよび電力用途

- 産業

- 製造設備

- プロセス制御

- その他の産業用途

- 家電

- ヘルスケアと医療

- 海洋

- その他

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東およびアフリカ

第10章 企業プロファイル

- TdVib

- Grirem Advanced Materials

- Metglas

- Cedrat Technologies

- Aperam

- Arnold Magnetic Technologies

- Sensor Technology

- AK Steel Holding Corporation

- Xinetics

The Global Magnetostrictive Materials Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 2.7 billion by 2034. Demand for magnetostrictive materials is rising due to their unique ability to change shape or size when subjected to magnetic fields, making them indispensable in advanced technological applications. Their usage spans a variety of sectors such as automotive, healthcare, aerospace, and consumer electronics. In the automotive field, these materials enhance vehicle performance, efficiency, and safety by being integral in sensors and actuators, particularly in power steering systems.

The growth of electric and hybrid vehicles is further propelling this market. Healthcare applications benefit greatly from their exceptional precision, enabling more accurate diagnostics and targeted treatments that improve patient outcomes. Meanwhile, aerospace companies rely on these materials for effective vibration control and continuous structural health monitoring, ensuring safety and performance in critical components. This dual utility across sectors not only broadens their application scope but also significantly amplifies market demand as industries seek reliable, high-performance solutions to meet evolving technological challenges.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 7.3% |

The rare earth materials segment generated USD 589.5 million in 2024 and is expected to reach USD 1.2 billion by 2034. This segment dominates because rare earth elements like terbium provide superior magnetic properties and high magnetic coefficients. These qualities make them ideal for applications requiring precision and efficiency, including sensors, actuators, and transformers. The increasing adoption of advanced technology in the automotive, aviation, and consumer electronics sectors fuels the growth of rare earth-based magnetostrictive materials.

The sensors and transducers accounted for a 34.9% share in 2024, making this the largest application segment. Magnetostrictive materials are prized for their ability to convert magnetic energy into mechanical energy and vice versa, lending themselves perfectly to sensor and transducer manufacturing. Their high sensitivity, durability, and accuracy make them essential components in automotive and consumer electronics devices.

United States Magnetostrictive Materials Market generated USD 313.4 million in 2024. This growth is driven by the increased use of these materials in various industrial applications, including sensors, actuators, and transformers. Industries such as manufacturing, automotive, and aerospace rely on magnetostrictive materials to improve operational accuracy and efficiency. In industrial automation, magnetostrictive sensors are widely used for precise position and displacement measurements. The ongoing focus on automation and the demand for advanced sensing technologies are expected to boost market growth throughout the forecast period.

Leading companies in the Magnetostrictive Materials Market include Cedrat Technologies, TdVib LLC, Grirem Advanced Materials Co., Ltd., Metglas Inc., and Aperam S.A. To strengthen their market positions and gain competitive advantages, these manufacturers pursue strategies such as launching innovative products, expanding production capacity, and engaging in mergers and acquisitions.

To solidify their foothold and expand market presence, companies in the magnetostrictive materials sector focus on several key strategic approaches. These include investing heavily in research and development to introduce innovative, higher-performance materials that meet evolving industry needs. They also prioritize capacity expansion to handle growing demand, especially from rapidly developing sectors like automotive and aerospace. Mergers and acquisitions help companies broaden their product portfolios and geographic reach, while strategic partnerships enable access to new technologies and markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Rare earth materials

- 5.2.1 Terfenol-D (Tb-Dy-Fe)

- 5.2.2 Samarium-iron compounds

- 5.2.3 Other rare earth materials

- 5.3 Iron-based alloys

- 5.3.1 Galfenol (Fe-Ga)

- 5.3.2 Alfenol (Fe-Al)

- 5.3.3 Other iron-based alloys

- 5.4 Nickel-based alloys

- 5.4.1 Nickel-iron alloys

- 5.4.2 Other nickel-based alloys

- 5.5 Cobalt-based alloys

- 5.6 Other materials

Chapter 6 Market Size and Forecast, By Form, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Bulk materials

- 6.2.1 Rods

- 6.2.2 Plates

- 6.2.3 Blocks

- 6.2.4 Other bulk forms

- 6.3 Thin films

- 6.4 Composites

- 6.4.1 Particulate composites

- 6.4.2 Laminated composites

- 6.4.3 Other composite forms

- 6.5 Powders

- 6.6 Other forms

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Sensors and transducers

- 7.2.1 Force and torque sensors

- 7.2.2 Position and displacement sensors

- 7.2.3 Stress and strain sensors

- 7.2.4 Magnetic field sensors

- 7.2.5 Acoustic and ultrasonic transducers

- 7.2.6 Other sensors and transducers

- 7.3 Actuators and motion control

- 7.3.1 Linear actuators

- 7.3.2 Rotary actuators

- 7.3.3 Precision positioning systems

- 7.3.4 Vibration control systems

- 7.3.5 Other actuator applications

- 7.4 Energy harvesting systems

- 7.4.1 Vibration energy harvesters

- 7.4.2 Acoustic energy harvesters

- 7.4.3 Other energy harvesting applications

- 7.5 Sonar and underwater acoustics

- 7.6 Structural health monitoring

- 7.7 Other applications

Chapter 8 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.2.1 Engine and powertrain applications

- 8.2.2 Suspension and chassis applications

- 8.2.3 Sensor applications

- 8.2.4 Other automotive applications

- 8.3 Aerospace and defense

- 8.3.1 Aircraft systems

- 8.3.2 Defense applications

- 8.3.3 Space applications

- 8.3.4 Other aerospace and defense applications

- 8.4 Energy and power

- 8.4.1 Energy harvesting

- 8.4.2 Power generation

- 8.4.3 Other energy and power applications

- 8.5 Industrial

- 8.5.1 Manufacturing equipment

- 8.5.2 Process control

- 8.5.3 Other industrial applications

- 8.6 Consumer electronics

- 8.7 Healthcare and medical

- 8.8 Marine

- 8.9 Others

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 TdVib

- 10.2 Grirem Advanced Materials

- 10.3 Metglas

- 10.4 Cedrat Technologies

- 10.5 Aperam

- 10.6 Arnold Magnetic Technologies

- 10.7 Sensor Technology

- 10.8 AK Steel Holding Corporation

- 10.9 Xinetics