|

市場調査レポート

商品コード

1782097

ゴム-金属接合品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Rubber-To-Metal Bonded Articles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ゴム-金属接合品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月02日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

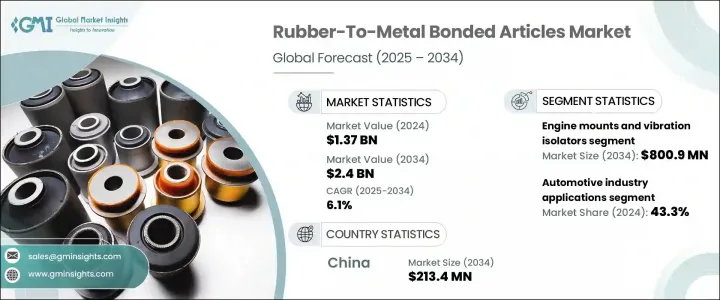

ゴム-金属接合品の世界市場規模は、2024年に13億7,000万米ドルとなり、CAGR 6.1%で成長し、2034年には24億米ドルに達すると予測されています。

この力強い勢いは、産業機械、航空宇宙、自動車など、さまざまな最終用途産業で需要が伸びていることに起因しており、これらの部品は騒音を最小限に抑え、衝撃を吸収し、振動を和らげるために不可欠です。自動車産業は、燃費効率と排ガス規制への適合をサポートする高性能で軽量な部品への嗜好の高まりにより、需要を牽引する支配的な力となっています。

特に排出ガスと自動車の安全性に関する規制が強化されるにつれて、メーカーは進化する規格に対応するために高度な接合ソリューションに傾倒しています。航空宇宙産業もまた、重要な構造・機能分野でこうした接合部品の利用を拡大しています。さらに、建設、ヘルスケア、エレクトロニクスなどの分野でも新たな応用の道が生まれつつあり、多様な成長パターンを示しています。接着技術、特にシアノアクリレート系接着剤の技術革新は、すでに市場の40%以上を占めており、さらなる追い風となっています。しかし、原材料とエネルギー価格の上昇は、特に小規模な市場企業にとって課題となっています。大企業がサプライチェーンの垂直統合と安定化を目指す中、統合の動きが加速する可能性があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 13億7,000万米ドル |

| 予測金額 | 24億米ドル |

| CAGR | 6.1% |

エンジンマウントと防振装置分野は、2024年に4億4,030万米ドルを生み出し、2034年には8億90万米ドルに成長すると予測され、CAGR 6.2%で成長します。これらの部品は、構造的安定性の維持とエンジンに関連する振動の最小化が不可欠な自動車や産業機械の用途で重要な役割を果たしています。軽量化とNVH(騒音・振動・ハーシュネス)特性の改善が優先される電気自動車やハイブリッド車では、その重要性が高まる。

2024年には、サスペンション・ブッシュ、防振システム、排気ブラケットのような結合部品が広く使用されているため、自動車分野が43.3%と最大の市場シェアを占めました。インド、ドイツ、中国、米国などの地域での市場拡大により、高性能で耐久性のある部品の需要が増加しています。開発中の自動車技術が製品要件を再構築しており、メーカー各社は最新の安全基準や排出ガス基準に適合する、より統合された効率的な部品を開発する必要に迫られています。

中国ゴム-金属接合品2024年の市場規模は1億1,430万米ドルで、CAGR6.5%で成長し、2034年には2億1,340万米ドルに達すると予測されます。輸入の落ち込みにもかかわらず、この地域は依然として世界最大の消費地であり、現地の需要は引き続き増加しています。有利な貿易政策とインフラ投資が国内生産へのシフトを促し、中国がこの産業で自立に近づくことを可能にしています。一方、米国は同期間に大きな市場成長を遂げました。

ゴム-金属接合品市場の主要企業には、Continental AG、Hutchinson SA、Trelleborg AB、住友理工、Vibracoustic GmbHなどがあります。ゴム-金属接合品市場における地位を強化するため、トップ企業はいくつかのコア戦略に注力しています。各社は、電気自動車やハイブリッド車プラットフォームの進化するニーズに応える高度で軽量な接合ソリューションを生み出すために、研究開発に多額の投資を行っています。戦略的なM&Aは、サプライチェーンをよりよくコントロールし、市場シェアを拡大するために進められています。主要企業はまた、製造能力を強化し、自動化を活用して効率を向上させています。さらに、安定した需要を確保し、世界のプレゼンスを強化するために、多くの企業がOEMと長期契約を結んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- エンジンマウントと振動アイソレーター

- 自動車用エンジンマウント

- 乗用車用エンジンマウント

- 商用車用エンジンマウント

- 電気自動車専用マウント

- 産業用振動絶縁装置

- 機械マウントおよびアイソレーター

- HVACシステムアイソレーター

- ポンプとコンプレッサーのマウント

- 航空宇宙用エンジンマウント

- 航空機エンジンマウント

- ヘリコプターの振動システム

- UAVおよびドローンアプリケーション

- 自動車用エンジンマウント

- ブッシングとサスペンション部品

- 自動車用ブッシング

- コントロールアームブッシング

- スタビライザーブッシュ

- ストラットマウントブッシング

- リーフスプリングブッシング

- 工業用ブッシング

- 機械用ブッシング

- コンベアシステムコンポーネント

- 重機用ブッシング

- 船舶およびオフハイウェイ用ブッシング

- 船舶用エンジンマウント

- 建設機械用ブッシング

- 農業機械部品

- 自動車用ブッシング

- シールとガスケット

- 自動車用シール

- エンジンシールとガスケット

- トランスミッションシール

- デファレンシャルシール

- 航空宇宙用シール

- 航空機エンジンシール

- 油圧システムシール

- 環境制御システムシール

- 工業用シール

- ポンプとバルブのシール

- パイプラインシール

- プロセス機器シール

- 自動車用シール

- カップリングとフレキシブルコネクタ

- 自動車用駆動カップリング

- CVジョイントブーツ

- ドライブシャフトカップリング

- トランスミッションカップリング

- 産業用フレキシブルカップリング

- モーターカップリング

- ポンプカップリング

- 発電機カップリング

- 海洋および航空宇宙用カップリング

- プロペラシャフトカップリング

- 航空機システムカップリング

- 特殊接着部品

- 自動車用駆動カップリング

- 防振パッドとマウント

- ショックアブソーバーとダンパー

- フレキシブルジョイントとコネクタ

- カスタムエンジニアリングソリューション

第6章 市場推計・予測:ボンディングテクノロジー別、2021年~2034年

- 主要動向

- 化学結合技術

- 接着剤ベースの接着システム

- エポキシ系接着剤

- ポリウレタン接着剤

- シリコンベースのシステム

- 特殊化学接着剤

- 加硫接着

- 硫黄加硫システム

- 過酸化物加硫

- 放射線加硫

- 金属酸化物加硫

- プライマーおよびコーティングシステム

- 金属表面プライマー

- ゴムに適合するコーティング

- 多層接着システム

- 接着剤ベースの接着システム

- 機械的接合技術

- オーバーモールドプロセス

- インサート成形アプリケーション

- 2ショット成形システム

- マルチマテリアル成形

- カプセル化技術

- 完全なカプセル化システム

- 部分的なカプセル化方法

- 選択的結合領域

- 機械的な連動

- テクスチャ表面の接着

- 機械的締結システム

- ハイブリッドボンディングアプローチ

- オーバーモールドプロセス

- 高度な接合技術

- プラズマ治療接合

- 大気プラズマシステム

- 低圧プラズマ治療

- コロナ治療アプリケーション

- レーザーアシストボンディング

- レーザー表面活性化

- レーザー溶接の用途

- 選択的レーザー加工

- ナノテクノロジー強化接合

- ナノ粒子強化接着剤

- カーボンナノチューブの応用

- グラフェンベースのシステム

- プラズマ治療接合

- 新たな接合技術

- 自己修復接着システム

- スマート接着技術

- バイオベースの接着システム

- リサイクル可能な接着ソリューション

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自動車産業向け用途

- 乗用車

- エンジンおよびパワートレイン部品

- サスペンションとシャーシシステム

- ボディおよび内装用途

- 電気自動車専用部品

- 商用車

- 大型トラック用途

- バスと長距離バスのシステム

- 特殊車両部品

- オートバイおよび二輪車用アプリケーション

- エンジンマウントシステム

- サスペンション部品

- 振動制御システム

- 自動車アフターマーケット

- 交換部品市場

- パフォーマンスアップグレードコンポーネント

- メンテナンスおよび修理アプリケーション

- 乗用車

- 航空宇宙および防衛産業

- 商用航空

- エンジンマウントシステム

- 着陸装置の部品

- キャビンおよび内装用途

- 環境制御システム

- 軍用機および防衛機

- 戦闘機の部品

- 輸送航空機システム

- ヘリコプターの用途

- UAVおよびドローンシステム

- 宇宙および衛星アプリケーション

- 打ち上げロケットのコンポーネント

- 衛星システム

- 宇宙ステーションのアプリケーション

- 航空宇宙アフターマーケット

- メンテナンス、修理、オーバーホール(MRO)

- 部品交換市場

- アップグレードおよび近代化プログラム

- 商用航空

- 産業機械および装置

- 製造設備

- 工作機械アプリケーション

- 自動化システムコンポーネント

- ロボット工学アプリケーション

- プロセス産業

- 化学処理装置

- 石油・ガス産業向けアプリケーション

- 発電システム

- 建設・鉱山機械

- 重機部品

- 土木機械

- 鉱山機械アプリケーション

- 海洋およびオフショア

- 船舶エンジンマウント

- オフショアプラットフォームコンポーネント

- 船舶推進システム

- 製造設備

- インフラと建設

- 建築・建設

- HVACシステムコンポーネント

- エレベーターとエスカレーターシステム

- 構造振動制御

- 交通インフラ

- 鉄道システムコンポーネント

- 橋梁およびトンネルへの応用

- 空港インフラ

- 公益事業とエネルギー

- 発電所のコンポーネント

- 再生可能エネルギーシステム

- 送電と配電

- 建築・建設

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- 3M Company

- BASF SE

- Bridgestone Corporation

- Continental AG

- Cooper Standard

- ElringKlinger AG

- Freudenberg Group

- H.B. Fuller Company

- Henkel AG &Co. KGaA

- Hutchinson SA

- Parker Hannifin Corporation

- Sumitomo Riko Company Limited

- Trelleborg AB

- Vibracoustic

- ZF Friedrichshafen AG

The Global Rubber-To-Metal Bonded Articles Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 2.4 billion by 2034. This strong momentum is attributed to the growing demand across a range of end-use industries, including industrial machinery, aerospace, and automotive, where these components are essential in minimizing noise, absorbing shocks, and dampening vibrations. The automotive sector continues to be a dominant force in driving demand, owing to the increasing preference for high-performance, weight-saving components that support fuel efficiency and emissions compliance.

As regulations tighten, especially around emissions and vehicle safety, manufacturers are leaning into advanced bonding solutions to meet evolving standards. The aerospace industry is also expanding its use of these bonded parts in critical structural and functional areas. Additionally, sectors such as construction, healthcare, and electronics are creating new pathways for application, signaling a diversified growth pattern. Innovations in bonding technologies, especially with cyanoacrylate adhesives-which already command over 40% of the market-are providing a further lift. However, rising raw material and energy prices pose challenges, particularly for smaller market players. This may accelerate consolidation efforts, as larger firms look to integrate and stabilize their supply chains vertically.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 6.1% |

The engine mounts and vibration isolators segment generated USD 440.3 million in 2024 and is projected to grow to USD 800.9 million by 2034, growing at a CAGR of 6.2%. These components are critical across automotive and industrial machinery applications, where maintaining structural stability and minimizing engine-related vibrations are essential. Their relevance is heightened in both electric and hybrid models, where manufacturers prioritize reduced weight and improved NVH (Noise, Vibration, and Harshness) characteristics.

In 2024, the automotive segment held the largest market share at 43.3%, owing to the extensive usage of bonded components like suspension bushings, anti-vibration systems, and exhaust brackets. Market expansion in regions such as India, Germany, China, and the United States has led to increased demand for high-performance, durable components. Emerging vehicle technologies are reshaping product requirements, pushing manufacturers to develop more integrated, efficient parts that align with updated safety and emissions standards.

China Rubber-To-Metal Bonded Articles Market generated USD 114.3 million in 2024 and is forecasted to grow at a CAGR of 6.5%, to reach USD 213.4 million by 2034. Despite a dip in imports, the region remains the largest global consumer, with local demand continuing to rise. Favorable trade policies and infrastructure investment are driving a shift toward domestic production, allowing China to move closer to self-reliance in this industry. Meanwhile, the United States experienced significant market growth during the same period.

Leading players in the Rubber-To-Metal Bonded Articles Market include Continental AG, Hutchinson SA, Trelleborg AB, Sumitomo Riko Co., Ltd., and Vibracoustic GmbH. To strengthen their position in the rubber-to-metal bonded articles market, top companies are focusing on several core strategies. They are heavily investing in research and development to create advanced, lightweight bonding solutions that cater to the evolving needs of electric and hybrid vehicle platforms. Strategic mergers and acquisitions are being pursued to gain better control of supply chains and expand market share. Key players are also enhancing their manufacturing capabilities and leveraging automation to improve efficiency. Furthermore, many are entering long-term contracts with OEMs to ensure consistent demand and strengthen their global presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.7 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Engine mounts and vibration isolators

- 5.2.1 Automotive engine mounts

- 5.2.1.1 Passenger vehicle engine mounts

- 5.2.1.2 Commercial vehicle engine mounts

- 5.2.1.3 Electric vehicle specialized mounts

- 5.2.2 Industrial vibration isolators

- 5.2.2.1 Machinery mounts and isolators

- 5.2.2.2 Hvac system isolators

- 5.2.2.3 Pump and compressor mounts

- 5.2.3 Aerospace engine mounts

- 5.2.3.1 Aircraft engine mounts

- 5.2.3.2 Helicopter vibration systems

- 5.2.3.3 Uav and drone applications

- 5.2.1 Automotive engine mounts

- 5.3 Bushings and suspension components

- 5.3.1 Automotive bushings

- 5.3.1.1 Control arm bushings

- 5.3.1.2 Sway bar bushings

- 5.3.1.3 Strut mount bushings

- 5.3.1.4 Leaf spring bushings

- 5.3.2 Industrial bushings

- 5.3.2.1 Machinery bushings

- 5.3.2.2 Conveyor system components

- 5.3.2.3 Heavy equipment bushings

- 5.3.3 Marine and off-highway bushings

- 5.3.3.1 Marine engine mounts

- 5.3.3.2 Construction equipment bushings

- 5.3.3.3 Agricultural machinery components

- 5.3.1 Automotive bushings

- 5.4 Seals and gaskets

- 5.4.1 Automotive seals

- 5.4.1.1 Engine seals and gaskets

- 5.4.1.2 Transmission seals

- 5.4.1.3 Differential seals

- 5.4.2 Aerospace seals

- 5.4.2.1 Aircraft engine seals

- 5.4.2.2 Hydraulic system seals

- 5.4.2.3 Environmental control system seals

- 5.4.3 Industrial seals

- 5.4.3.1 Pump and valve seals

- 5.4.3.2 Pipeline seals

- 5.4.3.3 Process equipment seals

- 5.4.1 Automotive seals

- 5.5 Couplings and flexible connectors

- 5.5.1 Automotive drive couplings

- 5.5.1.1 Cv joint boots

- 5.5.1.2 Driveshaft couplings

- 5.5.1.3 Transmission couplings

- 5.5.2 Industrial flexible couplings

- 5.5.2.1 Motor couplings

- 5.5.2.2 Pump couplings

- 5.5.2.3 Generator couplings

- 5.5.3 Marine and aerospace couplings

- 5.5.3.1 Propeller shaft couplings

- 5.5.3.2 Aircraft system couplings

- 5.5.3.3 Specialty bonded components

- 5.5.1 Automotive drive couplings

- 5.6 Anti-vibration pads and mounts

- 5.6.1 Shock absorbers and dampers

- 5.6.2 Flexible joints and connectors

- 5.6.3 Custom engineered solutions

Chapter 6 Market Estimates and Forecast, By Bonding Technology, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Chemical bonding technologies

- 6.2.1 Adhesive-based bonding systems

- 6.2.1.1 Epoxy-based adhesives

- 6.2.1.2 Polyurethane adhesives

- 6.2.1.3 Silicone-based systems

- 6.2.1.4 Specialty chemical adhesives

- 6.2.2 Vulcanization bonding

- 6.2.2.1 Sulfur vulcanization systems

- 6.2.2.2 Peroxide vulcanization

- 6.2.2.3 Radiation vulcanization

- 6.2.2.4 Metal oxide vulcanization

- 6.2.3 Primer and coating systems

- 6.2.3.1 Metal surface primers

- 6.2.3.2 Rubber-compatible coatings

- 6.2.3.3 Multi-layer bonding systems

- 6.2.1 Adhesive-based bonding systems

- 6.3 Mechanical bonding technologies

- 6.3.1 Overmolding processes

- 6.3.1.1 Insert molding applications

- 6.3.1.2 Two-shot molding systems

- 6.3.1.3 Multi-material molding

- 6.3.2 Encapsulation technologies

- 6.3.2.1 Complete encapsulation systems

- 6.3.2.2 Partial encapsulation methods

- 6.3.2.3 Selective bonding areas

- 6.3.3 Mechanical interlocking

- 6.3.3.1 Textured surface bonding

- 6.3.3.2 Mechanical fastening systems

- 6.3.3.3 Hybrid bonding approaches

- 6.3.1 Overmolding processes

- 6.4 Advanced bonding technologies

- 6.4.1 Plasma treatment bonding

- 6.4.1.1 Atmospheric plasma systems

- 6.4.1.2 Low-pressure plasma treatment

- 6.4.1.3 Corona treatment applications

- 6.4.2 Laser-assisted bonding

- 6.4.2.1 Laser surface activation

- 6.4.2.2 Laser welding applications

- 6.4.2.3 Selective laser processing

- 6.4.3 Nanotechnology-enhanced bonding

- 6.4.3.1 Nanoparticle-enhanced adhesives

- 6.4.3.2 Carbon nanotube applications

- 6.4.3.3 Graphene-based systems

- 6.4.1 Plasma treatment bonding

- 6.5 Emerging bonding technologies

- 6.5.1 Self-healing bonding systems

- 6.5.2 Smart adhesive technologies

- 6.5.3 Bio-based bonding systems

- 6.5.4 Recyclable bonding solutions

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Automotive industry applications

- 7.2.1 Passenger vehicles

- 7.2.1.1 Engine and powertrain components

- 7.2.1.2 Suspension and chassis systems

- 7.2.1.3 Body and interior applications

- 7.2.1.4 Electric vehicle specific components

- 7.2.2 Commercial vehicles

- 7.2.2.1 Heavy-duty truck applications

- 7.2.2.2 Bus and coach systems

- 7.2.2.3 Specialty vehicle components

- 7.2.3 Motorcycle and two-wheeler applications

- 7.2.3.1 Engine mount systems

- 7.2.3.2 Suspension components

- 7.2.3.3 Vibration control systems

- 7.2.4 Automotive aftermarket

- 7.2.4.1 Replacement parts market

- 7.2.4.2 Performance upgrade components

- 7.2.4.3 Maintenance and repair applications

- 7.2.1 Passenger vehicles

- 7.3 Aerospace and defense industry

- 7.3.1 Commercial aviation

- 7.3.1.1 Engine mount systems

- 7.3.1.2 Landing gear components

- 7.3.1.3 Cabin and interior applications

- 7.3.1.4 Environmental control systems

- 7.3.2 Military and defense aircraft

- 7.3.2.1 Fighter aircraft components

- 7.3.2.2 Transport aircraft systems

- 7.3.2.3 Helicopter applications

- 7.3.2.4 Uav and drone systems

- 7.3.3 Space and satellite applications

- 7.3.3.1 Launch vehicle components

- 7.3.3.2 Satellite systems

- 7.3.3.3 Space station applications

- 7.3.4 Aerospace aftermarket

- 7.3.4.1 Maintenance, repair, and overhaul (MRO)

- 7.3.4.2 Component replacement market

- 7.3.4.3 Upgrade and modernization programs

- 7.3.1 Commercial aviation

- 7.4 Industrial machinery and equipment

- 7.4.1 Manufacturing equipment

- 7.4.1.1 Machine tool applications

- 7.4.1.2 Automation system components

- 7.4.1.3 Robotics applications

- 7.4.2 Process industries

- 7.4.2.1 Chemical processing equipment

- 7.4.2.2 Oil and gas industry applications

- 7.4.2.3 Power generation systems

- 7.4.3 Construction and mining equipment

- 7.4.3.1 Heavy machinery components

- 7.4.3.2 Earth moving equipment

- 7.4.3.3 Mining machinery applications

- 7.4.4 Marine and offshore

- 7.4.4.1 Ship engine mounts

- 7.4.4.2 Offshore platform components

- 7.4.4.3 Marine propulsion systems

- 7.4.1 Manufacturing equipment

- 7.5 Infrastructure and construction

- 7.5.1 Building and construction

- 7.5.1.1 Hvac system components

- 7.5.1.2 Elevator and escalator systems

- 7.5.1.3 Structural vibration control

- 7.5.2 Transportation infrastructure

- 7.5.2.1 Railway system components

- 7.5.2.2 Bridge and tunnel applications

- 7.5.2.3 Airport infrastructure

- 7.5.3 Utilities and energy

- 7.5.3.1 Power plant components

- 7.5.3.2 Renewable energy systems

- 7.5.3.3 Transmission and distribution

- 7.5.1 Building and construction

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 BASF SE

- 9.3 Bridgestone Corporation

- 9.4 Continental AG

- 9.5 Cooper Standard

- 9.6 ElringKlinger AG

- 9.7 Freudenberg Group

- 9.8 H.B. Fuller Company

- 9.9 Henkel AG & Co. KGaA

- 9.10 Hutchinson SA

- 9.11 Parker Hannifin Corporation

- 9.12 Sumitomo Riko Company Limited

- 9.13 Trelleborg AB

- 9.14 Vibracoustic

- 9.15 ZF Friedrichshafen AG