推力ベクトル制御の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Thrust Vector Control Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782095

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

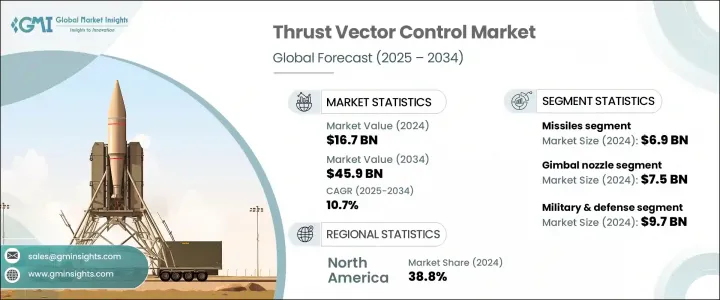

推力ベクトル制御の世界市場規模は、2024年に167億米ドルとなり、CAGR 10.7%で成長し、2034年には459億米ドルに達すると予測されています。

航空宇宙・防衛産業全体で先進推進システムの採用が増加していることが、この市場の成長を促進する主な要因です。世界中の政府や防衛機関は、ミサイルの精度、発射の柔軟性、飛行中の機動性を高める技術への投資を増やしています。各国が近代的な戦争能力と宇宙探査プログラムを優先し続ける中、効率的で応答性の高い飛行制御システムへの需要が高まっています。エンジンの推力をリアルタイムで方向転換できるTVCシステムは、大気圏内および大気圏外ミッションの両方で不可欠となっています。

この成長を支える大きな力のひとつは、精密誘導弾と高速飛行能力を重視し続けることです。現代の戦争では、敵の防衛網を回避して正確に攻撃できる、高速で応答性の高いミサイルシステムへの依存度が高まっています。推力ベクトル制御技術は、飛行中の方向転換、軌道調整、空力性能の向上を可能にすることで、これらの能力を可能にしています。さらに、人工衛星の配備や軌道ミッションへの民間セクターの参入が増加しているため、ステージ分離や軌道投入精度をTVCに大きく依存する打ち上げシステムへの需要が高まっています。航空宇宙推進における技術革新もまた、空気抵抗を低減し、燃料効率を高め、厳しい条件下でより優れた航行制御を提供する、より洗練されたベクタリング技術の採用をメーカーに促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 167億米ドル |

| 予測金額 | 459億米ドル |

| CAGR | 10.7% |

2024年には、ミサイルが69億米ドルを占め、市場最大のアプリケーションセグメントとなります。標的との正確な交戦、大気圏再突入時の制御改善、次世代迎撃システムの配備に対するニーズの高まりが、ミサイルプラットフォームにおけるTVC機構の使用を加速させています。これらのシステムは、空対空、地対空、地上発射の発射体において、迅速な方向転換と適応的な動きを可能にします。また、戦闘シナリオにおけるミサイルの生存性と応答性を高め、戦略的・戦術的防衛作戦に不可欠なものとなっています。

発射体は、予測期間中最も速いCAGR 12.4%で拡大すると予想されています。商業衛星や政府が支援する衛星ミッションの増加により、推力管理に高い精度が要求される打ち上げシステムの配備が進んでいます。スラストベクタリングは、マルチペイロードのハンドリング、正確な軌道アライメント、ミッション固有の軌道構成の達成を保証する上で不可欠です。特に、小型衛星の配備と再使用可能なロケットの台頭により、ベクトル制御ソリューションは、ペイロードダイナミクスとミッションの敏捷性における新たな要件を満たすために進化しています。

技術別では、ジンバルノズルセグメントが2024年の世界市場を独占し、75億米ドルの収益を上げました。ジンバルノズルは、エンジンの推力を方向転換するために旋回することで動作し、飛行体の方向と姿勢を微調整する上で重要な役割を果たします。機械的にシンプルで精密な制御が可能なため、垂直発射や高速ミサイルの操縦に最適です。柔軟で正確な飛行システムに対する要求が高まるにつれ、これらのノズルは新たに開発された航空宇宙および防衛プログラムにおいて、より大きな支持を得ています。動的安定性、軌道修正、高度制御において重要な利点を提供します。

最終用途は主に宇宙機関と軍事・防衛機関に分かれています。軍事・防衛部門は、2024年に97億米ドルと評価され、主要セグメントとして浮上しました。世界中の軍隊が戦略的近代化プログラムを強化しており、その中には応答時間の短縮、目標適応性の向上、任務成果の改善のための先進的TVCシステムの統合が含まれています。高速迎撃ミサイルから次世代戦闘プラットフォームまで、正確な打撃能力と作戦の柔軟性を可能にするTVCの役割は拡大し続けています。特に、進化する脅威は、防衛メーカーに高度な推力ベクトリング・ソリューションに大きく依存する適応推進システムを組み込むよう促しています。

地域別では、北米が圧倒的な市場シェアを維持し、2024年の世界売上高の38.8%を占めました。これは、強固な航空宇宙製造インフラ、着実な研究開発資金、大手防衛関連企業の存在に支えられています。この地域は、大規模な調達プログラムや、優れた操縦性と推力制御を必要とする次世代航空機プラットフォームの採用によって、CAGR 10.8%で拡大すると予測されています。米国は単独で最大の市場を維持し、2024年には57億米ドルに達します。同国が先進的な航空・宇宙戦闘システムの構築に注力していることが、TVC市場の成長に大きく寄与しています。

推力ベクトル制御分野の主要な業界企業には、BAE Systems、BPS Space、Collins Aerospace、Honeywell International、JASC Corporation、Moog、Parker Hannifinなどがあります。これらの企業は、制御精度、信頼性、複数のプラットフォームへの統合の柔軟性を向上させる次世代TVCシステムに一貫して投資しています。航空宇宙と防衛の展望が進化し続ける中、情勢技術の役割は、ミッションの成功と作戦の優位性において、引き続き中心的な役割を果たすことが期待されます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- ミサイルシステムへの防衛費の増加

- LEOでの衛星打ち上げ活動の増加

- 航空宇宙推進技術の進歩

- 航空宇宙推進アーキテクチャの電動化への移行

- 無人航空機と自律プラットフォームの出現

- 業界の潜在的リスク&課題

- 高い開発コストと長期にわたる認証サイクル

- レガシープラットフォームとの統合の複雑さ

- 市場機会

- レガシーシステム向けの電気機械式アクチュエータの改造

- AI対応制御システム統合

- モジュール式航空宇宙プラットフォームのTVC標準化

- 軽量複合ノズル材料

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的パートナーシップの情勢

- リスク評価と管理

- 主要契約の締結(2021-2024)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ジンバルノズル

- フレックスノズル

- スラスター

- 回転ノズル

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 打ち上げロケット

- ミサイル

- 衛星

- 戦闘機

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 宇宙機関

- 軍事・防衛

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- BAE Systems

- BPS Space

- Collins Aerospace

- Honeywell International

- JASC Corporation

- Moog

- Parker Hannifin

- SABCA

- Wickman Spacecraft and Propulsion Company

- Woodward

目次

The Global Thrust Vector Control Market was valued at USD 16.7 billion in 2024 and is estimated to grow at a CAGR of 10.7% to reach USD 45.9 billion by 2034. The increasing adoption of advanced propulsion systems across the aerospace and defense industries is a primary factor driving the growth of this market. Governments and defense agencies worldwide are increasing their investments in technologies that enhance missile precision, launch flexibility, and in-flight maneuverability. As countries continue to prioritize modern warfare capabilities and space exploration programs, the demand for efficient and responsive flight control systems has intensified. TVC systems, which allow for real-time redirection of engine thrust, are becoming essential in both atmospheric and exo-atmospheric missions.

One of the significant forces behind this growth is the continued emphasis on precision-guided munitions and high-speed flight capabilities. Modern warfare increasingly relies on fast, responsive missile systems that can evade enemy defenses and strike with accuracy. Thrust vector control technologies make these abilities possible by allowing mid-flight directional changes, trajectory adjustments, and improved aerodynamic performance. Additionally, growing private sector participation in satellite deployment and orbital missions has fueled demand for launch systems that rely heavily on TVC for stage separation and orbital insertion accuracy. Innovations in aerospace propulsion are also pushing manufacturers to adopt more sophisticated vectoring technologies that reduce drag, enhance fuel efficiency, and provide greater navigational control in challenging conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.7 Billion |

| Forecast Value | $45.9 Billion |

| CAGR | 10.7% |

In 2024, missiles represented the largest application segment in the market, accounting for USD 6.9 billion. The increasing need for accurate target engagement, improved control during atmospheric reentry, and the deployment of next-gen interceptor systems is accelerating the use of TVC mechanisms in missile platforms. These systems enable fast redirection and adaptive movement in air-to-air, surface-to-air, and ground-launched projectiles. They also enhance missile survivability and responsiveness in combat scenarios, making them indispensable in strategic and tactical defense operations.

Launch vehicles are anticipated to expand at the fastest CAGR of 12.4% over the forecast period. The growing number of commercial and government-backed satellite missions has resulted in the deployment of launch systems that demand high precision in thrust management. Thrust vectoring is essential in ensuring multi-payload handling, accurate trajectory alignment, and achieving mission-specific orbital configurations. Especially with the rise of small satellite deployments and reusable rockets, vector control solutions are evolving to meet new requirements in payload dynamics and mission agility.

By technology, the gimbal nozzle segment dominated the global market in 2024, generating USD 7.5 billion in revenue. Gimbal nozzles, which operate by pivoting to redirect engine thrust, play a critical role in fine-tuning the direction and attitude of flight vehicles. Their mechanical simplicity and ability to offer precise control make them ideal for both vertical launches and high-speed missile maneuvers. As demand increases for flexible and accurate flight systems, these nozzles are gaining more traction in newly developed aerospace and defense programs. They provide key advantages in dynamic stability, trajectory correction, and altitude control.

The end-use landscape is primarily split between space agencies and military & defense institutions. The military & defense sector emerged as the leading segment, valued at USD 9.7 billion in 2024. Armed forces worldwide are ramping up strategic modernization programs that include the integration of advanced TVC systems for faster response times, greater target adaptability, and improved mission outcomes. From high-speed interceptors to next-generation combat platforms, the role of TVC in enabling precise strike capabilities and operational flexibility continues to grow. In particular, evolving threats are pushing defense manufacturers to incorporate adaptive propulsion systems that rely heavily on advanced thrust vectoring solutions.

Regionally, North America maintained the dominant market share, accounting for 38.8% of global revenue in 2024, supported by robust aerospace manufacturing infrastructure, steady research and development funding, and the presence of major defense contractors. The region is projected to expand at a CAGR of 10.8%, driven by large-scale procurement programs and the adoption of next-generation aircraft platforms that require superior maneuverability and thrust control. The United States remained the single largest market, reaching USD 5.7 billion in 2024. The country's focus on building advanced air and space combat systems is a major contributor to TVC market growth.

Key industry players in the thrust vector control space include BAE Systems, BPS Space, Collins Aerospace, Honeywell International, JASC Corporation, Moog, and Parker Hannifin. These companies are consistently investing in next-gen TVC systems that offer improved control precision, reliability, and integration flexibility across multiple platforms. As the aerospace and defense landscape continues to evolve, the role of thrust vector control technologies is expected to remain central to mission success and operational superiority.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Application trends

- 2.2.3 End Use trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased defense spending on missile systems

- 3.2.1.2 Growing satellite launch activities in LEO

- 3.2.1.3 Advancements in aerospace propulsion technologies

- 3.2.1.4 Shift toward electrification in aerospace propulsion architectures

- 3.2.1.5 Emergence of unmanned aerial vehicles and autonomous platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs and prolonged certification cycles

- 3.2.2.2 Integration complexity with legacy platforms

- 3.2.3 Market opportunities

- 3.2.3.1 Electromechanical actuator retrofits for legacy systems

- 3.2.3.2 AI-enabled control system integration

- 3.2.3.3 TVC standardization for modular aerospace platforms

- 3.2.3.4 Lightweight composite nozzle materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Gimbal nozzle

- 5.3 Flex nozzle

- 5.4 Thrusters

- 5.5 Rotating nozzle

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Launch vehicles

- 6.3 Missiles

- 6.4 Satellites

- 6.5 Fighter aircraft

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Space agencies

- 7.3 Military & defense

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BAE Systems

- 9.2 BPS Space

- 9.3 Collins Aerospace

- 9.4 Honeywell International

- 9.5 JASC Corporation

- 9.6 Moog

- 9.7 Parker Hannifin

- 9.8 SABCA

- 9.9 Wickman Spacecraft and Propulsion Company

- 9.10 Woodward

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日