|

市場調査レポート

商品コード

1782094

肝疾患治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Liver Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 肝疾患治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月03日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

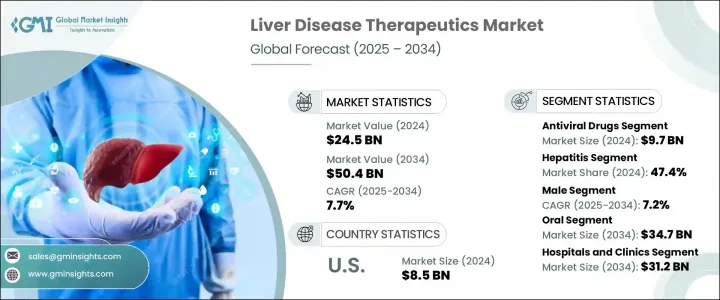

肝疾患治療薬の世界市場は、2024年には245億米ドルと評価され、CAGR 7.7%で成長し、2034年には504億米ドルに達すると推定されています。

肝臓関連の健康状態の有病率が世界的に上昇し続けていることから、市場は力強い成長を遂げています。この成長に拍車をかけている主な要因の一つは、あらゆる年齢層で肝疾患の世界の罹患率が増加していることです。慢性および急性の肝臓疾患は、遺伝的要因、環境要因、生活習慣関連要因の組み合わせにより、より広まりつつあります。

高齢化も肝疾患治療の需要拡大に寄与する重要な要因です。人々が長生きするにつれて、肝機能障害を含む加齢に関連した健康問題がより一般的になってきています。高齢者は、飲酒、処方箋薬の使用、代謝異常などの要因に長期間さらされるため、慢性的な肝障害のリスクが高くなることが多いです。その結果、ヘルスケア業界では、高齢患者の肝疾患に特化した治療オプションに対するニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 245億米ドル |

| 予測金額 | 504億米ドル |

| CAGR | 7.7% |

医療技術の革新もまた、市場の成長を支える上で重要な役割を果たしています。診断ツールの進歩により、患者の予後改善に不可欠な早期発見とタイムリーな介入が可能になりました。肝障害の早期発見を可能にする技術は、より身近で信頼できるものとなりつつあり、効果的な治療への需要を後押ししています。さらに、医薬品開発における継続的な研究により、複雑な肝疾患をより効果的に治療するための高度な治療製剤が生み出されています。このような改良は、より広範な治療法の採用に寄与し、市場規模の拡大に貢献しています。

製品別では、抗ウイルス薬が2024年に97億米ドルを占め、トップの座に躍り出た。ウイルス性肝炎、特にB型肝炎とC型肝炎が蔓延しているためであり、慢性肝障害とそれに伴う合併症の主要な原因となっています。

直接作用型抗ウイルス薬(DAAs)は、高い治癒率と少ない副作用を提供することで、治療状況を大きく変えました。これらの最新の治療法は、効果が高いだけでなく、治療期間が短いため、患者にとって完遂が容易です。より優れた有効性と安全性プロファイルを持つ次世代抗ウイルス薬の発売により、特に感染負荷の高い地域での世界の導入が加速しています。臨床転帰を改善することが証明されていることから、この分野は引き続き市場全体の収益に大きく貢献しています。

疾患タイプ別に見ると、肝疾患治療薬市場は肝炎、自己免疫疾患、非アルコール性脂肪性肝疾患(NAFLD)、がん、遺伝性疾患、その他のカテゴリーに分類されます。肝炎セグメントは2024年に47.4%のシェアを占め、優位を占めています。これは、B型肝炎とC型肝炎の世界の蔓延によるところが大きく、効果的な医療ソリューションが求められ続けています。

現在進行中の薬剤革新により、治療がより利用しやすく効率的になり、製剤の改良により治療期間が短縮され、より安全な治療レジメンが提供されるようになりました。肝炎の最新治療では、投与スケジュールが簡素化され、治癒率が向上した結果、患者のアドヒアランスが改善しました。さらに、機能的な治療法を開発するための継続的な研究により、肝炎分野はより広範な治療薬市場においてリードを維持しています。

性別では、市場は男性グループと女性グループに分けられます。2024年には男性が圧倒的なシェアを占め、CAGR 7.2%で成長すると予想されます。この動向は、女性に比べて男性の肝臓疾患の罹患率が高いことが背景にあります。研究によると、アルコール性肝疾患、NAFLD、肝炎を含む慢性肝疾患と診断される頻度は男性の方が高いです。

この男女差は、生物学的およびホルモンの違いとも関連しています。エストロゲンには肝組織を保護する作用があり、閉経前の女性は重篤な肝障害を経験しにくいと考えられています。一方、男性は脂肪肝から脂肪性肝炎や肝硬変といったより重篤な病態に進行しやすく、この層では医療介入の需要が高まる。

地域別では、米国が世界売上高に最も貢献しています。米国市場は2021年に75億米ドル、2022年に78億米ドル、2023年に81億米ドルと評価され、2024年には85億米ドルに達しました。この一貫した成長は、肝臓関連の健康問題、特に非アルコール性脂肪性肝疾患(NAFLD)とその重症型である非アルコール性脂肪肝炎(NASH)の増加を反映しています。その要因としては、肥満の急増、座りがちなライフスタイル、関連する代謝異常などが挙げられます。

米国のヘルスケア制度は、公的および民間の保険制度を通じて早期診断と高コストの専門治療へのアクセスを支援しており、これが市場の継続的な拡大を後押ししています。認知度の向上、検診の普及、医療インフラの整備はすべて、同国の主導的地位に貢献しています。

世界的に見ると、競合情勢には多国籍大手企業、地域企業、新興企業が混在しています。市場シェアの約45%から50%は主要企業4社が占めており、これらの企業は提携、買収、革新的な治療法の上市を通じて市場でのプレゼンス拡大に積極的に取り組んでいます。これらの企業は、満たされていない臨床ニーズに対応し、患者の転帰を改善するために研究開発に多額の投資を行っており、急成長する業界において戦略的優位性を発揮しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 肝疾患の罹患率の増加

- 診断技術の進歩

- 座りがちな生活習慣、不健康な食生活、アルコール摂取の増加

- 業界の潜在的リスク&課題

- 治療費の高騰(特に生物学的製剤の場合)

- 特定の薬剤の副作用と効果の限界

- 市場機会

- 非アルコール性脂肪肝炎(NASH)および肝がんに関する強力な研究開発パイプライン

- 新興市場への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- パイプライン分析

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 抗ウイルス薬

- ワクチン

- 化学療法

- 標的療法

- 免疫抑制剤

- 免疫グロブリン

- コルチコステロイド

- その他の製品

第6章 市場推計・予測:病気の種類別、2021年~2034年

- 主要動向

- 肝炎

- 自己免疫疾患

- 非アルコール性脂肪性肝疾患(NAFLD)

- がん

- 遺伝性疾患

- その他の病気の種類

第7章 市場推計・予測:男女別、2021年~2034年

- 主要動向

- 男性

- 女性

第8章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 非経口

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Amgen

- AbbVie

- Bristol-Myers Squibb

- Bayer

- GSK plc

- Gilead Sciences

- Hoffmann-La Roche

- Intercept Pharmaceuticals

- Johnson &Johnson Services

- Merck &Co.

- Novartis

- Pfizer

- Sanofi

- Takeda Pharmaceutical Company Limited

- Zydus Lifesciences

The Global Liver Disease Therapeutics Market was valued at USD 24.5 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 50.4 billion by 2034. The market is witnessing robust growth as the prevalence of liver-related health conditions continues to rise worldwide. One of the primary forces fueling this growth is the increasing global incidence of liver diseases across all age groups. Liver conditions, both chronic and acute, are becoming more widespread due to a combination of genetic, environmental, and lifestyle-related factors.

An aging population is another important factor contributing to the expanding demand for liver disease treatments. As people live longer, age-related health issues, including liver dysfunction, are becoming more common. Elderly individuals often face a higher risk of chronic liver problems due to prolonged exposure to factors such as alcohol consumption, use of prescription medications, and metabolic disorders. As a result, the healthcare industry is seeing a greater need for therapeutic options that specifically address liver diseases in older patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.5 Billion |

| Forecast Value | $50.4 Billion |

| CAGR | 7.7% |

Innovations in medical technology have also played a significant role in supporting market growth. Advancements in diagnostic tools have enabled early detection and timely intervention, which are critical for improving patient outcomes. Technologies that allow for early-stage identification of liver disorders are becoming more accessible and reliable, driving the demand for effective treatments. Furthermore, continuous research in pharmaceutical development is leading to the creation of advanced therapeutic formulations designed to treat complex liver conditions more effectively. These improvements are contributing to broader treatment adoption and helping expand the market size.

By product, antiviral drugs emerged as the top-performing segment, accounting for USD 9.7 billion in 2024. The segment dominates due to the widespread occurrence of viral hepatitis, particularly hepatitis B and C, which remain among the leading causes of chronic liver damage and associated complications.

Direct-acting antiviral agents (DAAs) have significantly changed the treatment landscape by offering high cure rates and fewer side effects. These modern therapies are not only more effective but also easier for patients to complete, thanks to their shorter treatment durations. The launch of next-generation antivirals with better efficacy and safety profiles has accelerated global adoption, especially in regions with high infection burdens. Their proven ability to improve clinical outcomes continues to position this segment as a major contributor to overall market revenues.

In terms of disease type, the liver disease therapeutics market is classified into hepatitis, autoimmune disorders, non-alcoholic fatty liver disease (NAFLD), cancer, genetic conditions, and other categories. The hepatitis segment dominated the landscape with a substantial 47.4% share in 2024. This is largely due to the persistent global burden of hepatitis B and C infections, which continue to demand effective medical solutions.

Ongoing drug innovations have made treatment more accessible and efficient, with improved formulations offering shorter and safer therapeutic regimens. Modern treatments for hepatitis feature simplified dosing schedules and increased cure rates, resulting in improved patient adherence. In addition, continuous research to develop functional cures ensures that the hepatitis segment maintains its lead within the broader therapeutics market.

By gender, the market is divided into male and female groups. In 2024, the male population represented the dominant share and is expected to grow at a CAGR of 7.2%. This trend is driven by a higher incidence of liver conditions among men compared to women. Studies show that men are more frequently diagnosed with chronic liver diseases, including alcoholic liver disease, NAFLD, and hepatitis.

This gender disparity is also linked to biological and hormonal differences. Estrogen is thought to have a protective effect on liver tissue, making premenopausal women less likely to experience severe liver damage. Men, on the other hand, are more prone to disease progression from fatty liver to more serious conditions such as steatohepatitis and cirrhosis, which increases the demand for medical intervention in this demographic.

Regionally, the United States is the largest contributor to global revenues. The U.S. market was valued at USD 7.5 billion in 2021, USD 7.8 billion in 2022, USD 8.1 billion in 2023, and reached USD 8.5 billion in 2024. This consistent growth reflects a rising number of liver-related health issues, particularly non-alcoholic fatty liver disease (NAFLD) and its more severe form, non-alcoholic steatohepatitis (NASH). Contributing factors include a surge in obesity, sedentary lifestyles, and associated metabolic disorders.

The healthcare system in the U.S. supports early diagnosis and access to high-cost specialty treatments through public and private insurance programs, which helps fuel continued market expansion. Increasing awareness, widespread screening efforts, and improved healthcare infrastructure all contribute to the country's leading position.

Globally, the competitive landscape features a mix of large multinational firms, regional companies, and emerging players. Approximately 45% to 50% of the market share is held by four leading companies that are actively engaged in expanding their market presence through collaborations, acquisitions, and the launch of innovative therapies. These companies are investing heavily in research and development to address unmet clinical needs and improve patient outcomes, giving them a strategic advantage in a rapidly growing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Disease type

- 2.2.4 Gender

- 2.2.5 Route of administration

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of liver diseases

- 3.2.1.2 Advancements in diagnostic technologies

- 3.2.1.3 Rise in sedentary lifestyles, poor diet, and alcohol use

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment, especially for biologics

- 3.2.2.2 Side effects and limited efficacy of certain drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Strong R&D pipeline for nonalcoholic steatohepatitis (NASH) and liver cancer

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antiviral drugs

- 5.3 Vaccines

- 5.4 Chemotherapy

- 5.5 Targeted therapy

- 5.6 Immunosuppressants

- 5.7 Immunoglobulins

- 5.8 Corticosteroids

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hepatitis

- 6.3 Autoimmune diseases

- 6.4 Non-alcoholic fatty liver disease (NAFLD)

- 6.5 Cancer

- 6.6 Genetic disorders

- 6.7 Other disease types

Chapter 7 Market Estimates and Forecast, By Gender, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Male

- 7.3 Female

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Parenteral

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amgen

- 11.2 AbbVie

- 11.3 Bristol-Myers Squibb

- 11.4 Bayer

- 11.5 GSK plc

- 11.6 Gilead Sciences

- 11.7 Hoffmann-La Roche

- 11.8 Intercept Pharmaceuticals

- 11.9 Johnson & Johnson Services

- 11.10 Merck & Co.

- 11.11 Novartis

- 11.12 Pfizer

- 11.13 Sanofi

- 11.14 Takeda Pharmaceutical Company Limited

- 11.15 Zydus Lifesciences