VHF航空地上通信局の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

VHF Air Ground Communication Stations Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782089

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

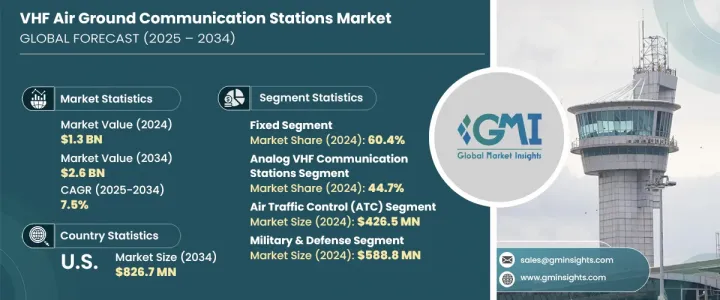

世界のVHF航空地上通信局市場は、2024年には13億米ドルと評価され、CAGR 7.5%で成長し、2034年には26億米ドルに達すると推定されています。

この成長軌道はいくつかの重要な要因によって後押しされているが、その最たるものは国際航空便の継続的な増加です。旅客便や貨物便が世界中で増加するにつれて、パイロットと航空管制官の間のシームレスで中断のない通信に対する需要がますます重要になってきています。信頼性の高い通信システムは、飛行の安全性を維持するだけでなく、地域的・国際的な飛行ネットワークにおける運航効率を確保するためにも不可欠です。航空ネットワークが拡大し、民間および防衛関連の航空運航の頻度が高まるにつれ、各国はインフラのアップグレードに投資せざるを得なくなり、固定式および携帯式のVHF通信システムの機会が生まれています。

世界の航空管制の近代化は、市場情勢の形成に重要な役割を果たしています。各国政府や規制当局は、世界の航空安全基準を満たすため、高度な通信技術の導入を強制する政策を積極的に実施しています。新興経済諸国も、特に空港開発に投資し、旅客数の増加に対応するために航空インフラをアップグレードすることで、市場開拓に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 7.5% |

高信頼性通信ソリューションに対する需要の高まりは、民間航空だけでなく、緊急対応チームや軍隊にも及んでいます。これらの分野では、ポータブルVHFステーションは、迅速な配備、堅牢な接続性、安全な伝送という点で重要な利点を提供し、災害救援任務や戦術的作戦に不可欠なものとなっています。弾力性と柔軟性が戦略的優先事項となるにつれ、拡張性のあるモバイル通信ツールの必要性が高まっています。

製品タイプ別に見ると、市場は固定式と携帯式のVHF航空地上通信システムに区分されます。2024年には、固定システムが世界の売上の60.4%を占め、優位を占めています。これらのシステムは、交通量の多いゾーンや常設施設に適しており、途切れのないカバレッジとインフラグレードの信頼性が不可欠です。各国が空港のキャパシティを拡大し、施設をアップグレードしていることから、固定VHF局の需要は、特に航空が急成長している地域では引き続き堅調に推移すると予想されます。ポータブルシステムは、2024年の市場シェアは39.6%と小さいもの、遠隔地や一時的な運用における汎用性の高さから引き続き注目を集めています。

技術別に見ると、市場にはアナログ、デジタル、ハイブリッド通信局が含まれます。アナログVHFシステムは2024年に44.7%と最大のシェアを占めたが、これは主に既存の広範な展開と旧来の航空システムとの互換性によるものです。多くの小規模空港や地方空港、特に開発途上地域では、アナログ通信局が依然として使用されており、利害関係者はデジタルインフラへの完全移行よりも段階的なアップグレードを選択しています。このため、アナログ・ソリューション、特に保守や交換部品に対する需要が安定しています。

VHF航空地上通信システムの用途は、いくつかの重要な航空機能にまたがっています。これには、航空交通管制(ATC)、航空運航管制(AOC)、飛行情報サービス(FIS)、緊急通信、地上支援など、固定翼機や回転翼機での使用が含まれます。このうち、ATC分野は2024年に4億2,650万米ドルを生み出し、CAGR 8.2%で成長すると予測されています。空の旅が増え続ける中、航空当局は航空交通管理システム内の通信インフラの品質と信頼性の向上に注力しています。運用の効率化と空域の近代化に対するこうした取り組みは、VHF通信局の需要拡大に直結します。

市場はさらに、最終用途に基づいて商業、政府、軍事・防衛分野に区分されます。軍事・防衛分野は2024年に5億8,880万米ドルの市場価値で最大となり、CAGR 8.3%で成長すると予測されています。この成長は、ミッション・クリティカルなシナリオにおいて安全で高性能な通信チャネルが必要とされることに起因しています。戦闘中であれ、兵站中であれ、人道支援中であれ、防衛活動には堅牢な空対地通信機能が必要です。固定式と携帯式のVHFシステムは、現場での連携と指揮を確保する上で不可欠です。

地域別では、北米が2024年の世界市場の35.2%を占め、CAGR 7.3%で拡大すると予測され、市場をリードしています。この地域の成長の原動力は、航空管制システムのアップグレードへの継続的な投資、先進デジタル技術の導入、大手システムインテグレーターの存在です。米国は、インフラのアップグレードと航空分野における近代化イニシアチブの実施に支えられ、2034年までに8億2,670万米ドルに達すると予測されています。

VHF航空地上通信局市場の競争力学に貢献している主な企業は、Thales Group、Honeywell International Inc.、Collins Aerospace、Elbit Systems、General Dynamics Corporation、Leonardo S.p.A.、MORCOM International, Inc.、Rohde &Schwarz、Spectra Groupなどです。これらの企業は技術革新を続け、世界の足跡を拡大しており、市場の長期的な成長の可能性を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の航空交通需要の増加

- 航空管制インフラの近代化

- 厳格な規制と安全基準

- 新興市場における空港ネットワークの拡大

- 防衛および災害対応における柔軟で迅速な展開ソリューションの需要の高まり

- 業界の潜在的リスク&課題

- 初期投資と維持費が高め

- 規制の複雑さとスペクトル管理の課題

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 将来の市場動向

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021-2024)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 固定

- ポータブル

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- アナログVHF通信局

- デジタルVHF通信局

- ハイブリッドVHF通信局

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 航空管制(ATC)

- 航空運航管制(AOC)

- フライト情報サービス(FIS)

- 緊急・災害通信

- 地上支援作戦

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 軍事・防衛

- 政府

- 国土安全保障

- 行政

- 商業用

第9章 市場推計・予測:地域別、2021 -2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- AEROTHAI Business

- Becker Avionics Gmbh

- Collins Aerospace

- Elbit Systems

- General Dynamics Corporation

- Honeywell International Inc

- IACIT

- Jotron

- Leonardo S.p.A.

- MORCOM International, Inc.

- Rohde &Schwarz

- Spectra Group

- Systems Interface Limited

- Thales Group

- Viasat Inc

目次

The Global VHF Air Ground Communication Stations Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 2.6 billion by 2034. This growth trajectory is fueled by several key factors, the foremost being the continued increase in international air travel. As passenger and cargo flights multiply across the globe, the demand for seamless and uninterrupted communication between pilots and air traffic controllers is becoming more critical. Reliable communication systems are essential not only for maintaining flight safety but also for ensuring operational efficiency across regional and international flight networks. As aviation networks expand and the frequency of commercial and defense-related air operations rises, countries are compelled to invest in infrastructure upgrades, creating opportunities for both fixed and portable VHF communication systems.

The modernization of air traffic control frameworks worldwide plays a significant role in shaping the market landscape. Governments and regulatory authorities are actively implementing policies that enforce the deployment of advanced communication technologies to meet global aviation safety standards. Emerging economies are also contributing to market expansion, particularly by investing in airport development and upgrading their aviation infrastructure to accommodate rising passenger volumes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 7.5% |

This growing demand for high-reliability communication solutions extends beyond civilian aviation to include emergency response teams and military forces. In these sectors, portable VHF stations offer critical advantages in terms of quick deployment, robust connectivity, and secure transmissions, making them indispensable for disaster relief missions and tactical operations. As resilience and flexibility become strategic priorities, the need for scalable and mobile communication tools is gaining momentum.

In terms of product types, the market is segmented into fixed and portable VHF air ground communication systems. Fixed systems dominated the landscape in 2024, accounting for 60.4% of the global revenue. These systems are the preferred choice for high-traffic zones and permanent installations, where uninterrupted coverage and infrastructure-grade reliability are essential. With nations expanding airport capacities and upgrading facilities, the demand for fixed VHF stations is expected to remain strong, especially in regions undergoing rapid aviation growth. Portable systems, while representing a smaller market share of 39.6% in 2024, continue to gain attention due to their versatility in remote or temporary operations.

By technology, the market includes analog, digital, and hybrid communication stations. Analog VHF systems held the largest share at 44.7% in 2024, mainly due to their extensive existing deployment and compatibility with older aviation systems. In many smaller and regional airports, particularly in developing regions, analog stations remain in use, with stakeholders opting for phased upgrades over complete transitions to digital infrastructure. This ensures consistent demand for analog solutions, especially for maintenance and replacement parts.

The application of VHF air ground communication systems spans across several critical aviation functions. These include use in fixed-wing and rotary-wing aircraft for air traffic control (ATC), aeronautical operational control (AOC), flight information services (FIS), emergency communications, and ground support. Among these, the ATC segment generated USD 426.5 million in 2024 and is projected to grow at a CAGR of 8.2%. With air travel continuing to rise, aviation authorities are focused on improving the quality and reliability of communication infrastructure within air traffic management systems. This commitment to operational efficiency and airspace modernization directly translates to stronger demand for VHF communication stations.

The market is further segmented based on end use into commercial, government, and military & defense sectors. The military & defense segment emerged as the largest in 2024, with a market value of USD 588.8 million, and is forecast to grow at a CAGR of 8.3%. This growth is attributed to the need for secure and high-performance communication channels in mission-critical scenarios. Defense operations, whether during combat, logistics, or humanitarian support, require robust air-to-ground communication capabilities. Both fixed and portable VHF systems are vital in ensuring coordination and command in the field.

Regionally, North America led the global market in 2024, accounting for 35.2% of the total share and projected to expand at a CAGR of 7.3%. The region's growth is driven by continuous investments in upgrading air traffic control systems, the deployment of advanced digital technologies, and the presence of major system integrators. The United States alone is anticipated to reach USD 826.7 million by 2034, supported by infrastructure upgrades and the implementation of modernization initiatives in the aviation sector.

Key players contributing to the competitive dynamics of the VHF air ground communication stations market include Thales Group, Honeywell International Inc., Collins Aerospace, Elbit Systems, General Dynamics Corporation, Leonardo S.p.A., MORCOM International, Inc., Rohde & Schwarz, and Spectra Group. These companies continue to innovate and expand their global footprint, reinforcing the market's long-term growth potential.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.2 Disruptions

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global air traffic demands

- 3.3.1.2 Modernization of air traffic control infrastructure

- 3.3.1.3 Stringent regulatory and safety standards

- 3.3.1.4 Expansion of airport networks in emerging markets

- 3.3.1.5 Growing need for flexible, rapid-deployment solutions in defense and disaster response

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment and maintenance costs

- 3.3.2.2 Regulatory complexity and spectrum management challenges

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Pricing strategies

- 3.12 Emerging business models

- 3.13 Compliance requirements

- 3.14 Defense budget analysis

- 3.15 Global defense spending trends

- 3.16 Regional defense budget allocation

- 3.16.1 North America

- 3.16.2 Europe

- 3.16.3 Asia Pacific

- 3.16.4 Middle East and Africa

- 3.16.5 Latin America

- 3.17 Key defense modernization programs

- 3.18 Budget forecast (2025-2034)

- 3.18.1 Impact on industry growth

- 3.18.2 Defense budgets by country

- 3.19 Supply chain resilience

- 3.20 Geopolitical analysis

- 3.21 Workforce analysis

- 3.22 Digital transformation

- 3.23 Mergers, acquisitions, and strategic partnerships landscape

- 3.24 Risk assessment and management

- 3.25 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Portable

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Analog VHF communication stations

- 6.3 Digital VHF communication station

- 6.4 Hybrid VHF communication station

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Air traffic control (ATC)

- 7.3 Aeronautical operational control (AOC)

- 7.4 Flight information service (FIS)

- 7.5 Emergency & disaster communication

- 7.6 Ground support operations

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Military & Defense

- 8.3 Government

- 8.3.1 Homeland security

- 8.3.2 Public administration

- 8.4 Commercial

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AEROTHAI Business

- 10.2 Becker Avionics Gmbh

- 10.3 Collins Aerospace

- 10.4 Elbit Systems

- 10.5 General Dynamics Corporation

- 10.6 Honeywell International Inc

- 10.7 IACIT

- 10.8 Jotron

- 10.9 Leonardo S.p.A.

- 10.10 MORCOM International, Inc.

- 10.11 Rohde & Schwarz

- 10.12 Spectra Group

- 10.13 Systems Interface Limited

- 10.14 Thales Group

- 10.15 Viasat Inc

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日