|

市場調査レポート

商品コード

1773475

カルコゲニドの市場機会、成長促進要因、産業動向分析、2025~2034年予測Chalcogenides (MoS2, WS2, WSe2) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カルコゲニドの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

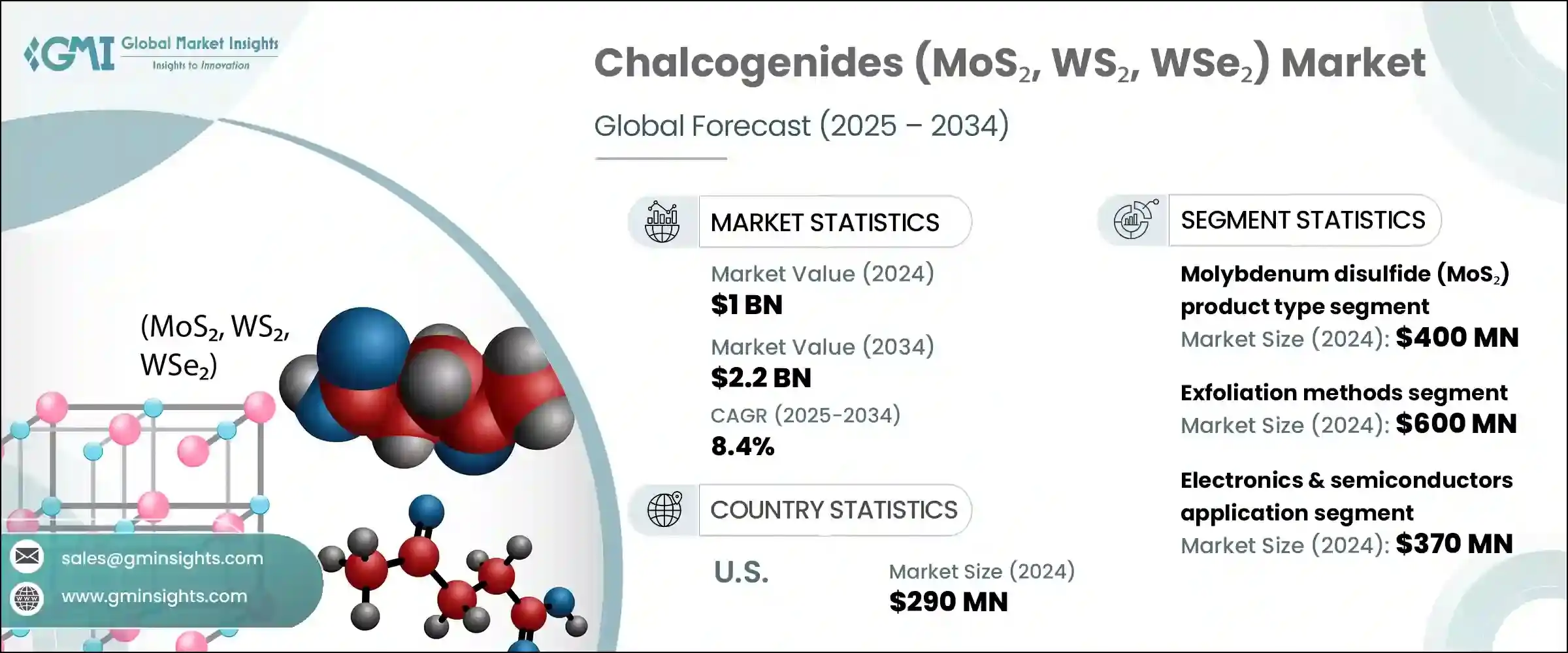

カルコゲニド(MoS2、WS2、WSe2)の世界市場は、2024年には10億米ドルと評価され、CAGR 8.4%で成長し、2034年には22億米ドルに達すると推定されています。

この着実な成長は、ナノテクノロジーの開発と、複数の業界にわたる高性能でエネルギー効率の高いソリューションへの需要の高まりによって推進されている先端材料分野の幅広い勢いを反映しています。これらの層状遷移金属ジカルコゲナイドは、その卓越した電気的、機械的、光学的挙動により、将来のエレクトロニクスにおける重要なイネーブラとなっています。従来のシリコンをベースとする技術が物理的・スケーリング的な限界に直面する中、これらの二次元材料は、小型化エレクトロニクス、フレキシブル・デバイス、高速トランジスタなどの用途において、有望な代替材料として台頭してきています。コンパクトで電力効率の高いハードウェアへの関心の高まりは、特に航空宇宙、防衛、通信、医療機器などの分野に関連しています。

米国、アジア太平洋、EUなど、各地域で政府が支援する研究開発イニシアティブは、次世代材料の技術革新を推進するために重要な財政的・制度的支援を提供しています。これには、ナショナル・イノベーション・センターの設立、パイロット製造ハブへの資金提供、ラボ規模の研究の商業化支援などが含まれます。官民パートナーシップは、特に半導体と再生可能エネルギーの領域で強化されつつあり、そこでは2D半導体のフレキシブル基板への統合がより現実的になりつつあります。MoS2やWS2のような材料は、その調整可能なバンドギャップと優れたキャリア移動度により、従来の材料よりもかなりの性能上の利点を提供します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 10億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 8.4% |

製造技術のうち、剥離法セグメントは2024年に6億米ドルを生み出し、2034年までCAGR 7.9%で成長すると予測されています。剥離法は依然として研究グレードの材料やプロトタイプに不可欠ですが、化学気相成長法(CVD)は、商業グレードの半導体プロセスに適合する均一で高品質な薄膜を得る能力があるため、スケーラブルな生産を支配するようになってきています。CVDは、精密な層制御、幅広い基板適合性、工業的生産量での再現性を可能にし、研究開発から高スループット電子機器製造への移行に最適な技術として位置づけられています。多くの製造ラボやパイロット施設がCVDを採用しており、ラボの技術革新をナノ材料の商業規模の応用につなげる上で極めて重要な役割を担っています。

エレクトロニクス・半導体セグメントは2024年に顕著な収益を上げました。ナノ材料のユニークなバンド構造と半導体特性は、先進的な電界効果トランジスタ、メモリーデバイス、薄膜論理回路の優れた候補となります。これらの材料は前例のない柔軟性と超薄型アーキテクチャを可能にし、次世代ウェアラブル技術、集積フォトニクス、ソフトロボティクスにとって非常に望ましいものとなっています。研究者らはすでに、スケーリングされたシリコンベースのデバイスに匹敵するか、それを上回るスイッチング動作やしきい値性能を報告しており、大手半導体メーカーがムーアの法則後の設計時代に近づくにつれて、こうした2D代替材料の探求を後押ししています。

米国カルコゲニド(MoS2、WS2、WSe2)市場は、2025~2034年の間に顕著なCAGRで成長すると推定され、特に量子技術や防衛グレード半導体への応用のための研究開発が牽引しています。MoS2やWSe2のようなバルク材料は主にアジアから輸入されていますが、米国は川下の開発と統合でリードしており、付加価値の高い派生品を国際市場に輸出しています。米国のハイテク産業は、これらの材料を最先端のプロトタイピングに活用し、オプトエレクトロニクス、フォトニクス、次世代トランジスタアーキテクチャの限界を押し広げています。ACS Material社や2D Tech社などの企業は、国内の研究努力を可能にする上で重要な役割を果たしており、一方、大規模な防衛請負業者や電子機器メーカーは、これらの高性能ナノ材料の需要を牽引しています。

世界のカルコゲニド(MoS2, WS2, WSe2)市場で事業を展開する著名な業界企業には、SixCarbon Technology社、Graphene Laboratories Inc.社、American Elements社、ACS Material LLC社、XFNANO Materials Tech Co.これらの企業は、材料合成とサプライチェーン開発の両方に不可欠な存在です。カルコゲナイド業界の大手企業は、市場での地位を向上させ、世界のリーチを拡大するために、いくつかの戦略を活用しています。これらの企業は、高精度の材料特性評価とカスタマイズへの投資を続けながら、増大する工業用および商業用の需要に対応するために生産能力を拡大しています。学術機関や国立研究所との協力は、特に量子応用やフレキシブル・エレクトロニクスなどの最先端技術革新を促進するのに役立っています。また、主なプレーヤーはデバイスメーカーと戦略的パートナーシップを結び、2D材料を使用した特定用途向けソリューションを共同開発しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材質別、2021~2034年

- 主要動向

- 二硫化モリブデン(MoS2)

- 二硫化タングステン(WS2)

- 二セレン化タングステン(WSe2)

- ヘテロ構造とハイブリッド

- その他

第6章 市場推計・予測:合成・製造技術別、2021~2034年

- 主要動向

- 角質除去方法

- 機械的剥離

- 液相剥離

- 電気化学的剥離

- インターカレーション補助角質除去

- その他

- 化学蒸着(CVD)

- 従来のCVDプロセス

- 金属有機CVD(MOCVD)

- 物理蒸着(PVD)

- スパッタリング技術

- パルスレーザー蒸着

- スケーラブルな生産方法

- 化学合成経路

- その他

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- エレクトロニクスおよび半導体

- 電界効果トランジスタ(FET)

- 論理ゲートと回路

- メモリデバイス

- フレキシブルエレクトロニクス

- その他

- オプトエレクトロニクスとフォトニクス

- 光検出器

- 発光ダイオード(LED)

- 発光デバイス

- 太陽電池

- その他

- エネルギー貯蔵と変換

- 充電式電池

- スーパーキャパシタ

- 水素発生反応(HER)触媒

- CO2還元触媒

- 熱電デバイス

- 燃料電池

- その他

- センサーと検出器

- ガスセンサー

- バイオセンサー

- 圧力およびひずみセンサー

- その他

- 量子技術

- トライボロジーと潤滑剤

- バイオメディカルアプリケーション

- その他

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第9章 企業プロファイル

- 2D Semiconductors

- 6Carbon Technology

- ACS Material, LLC

- Applied Nanolayers B.V.

- Grolltex Inc.

- HQ Graphene

- Muke Nano

- Nanoshel LLC

- SixCarbon Technology

- Ossila Ltd.

- SVT Associates, Inc.

- Tungsten Compounds GmbH

- XFNANO Materials Tech Co., Ltd.

- Intelligent Materials Pvt. Ltd.

- American Elements

- Graphene Laboratories Inc.

- MSE Supplies LLC

- Sigma-Aldrich(Merck KGaA)

- Stanford Advanced Materials

- Edgetech Industries LLC

The Global Chalcogenides (MoS2, WS2, WSe2) Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 2.2 billion by 2034. This steady growth reflects broader momentum in the advanced materials sector, which is being propelled by developments in nanotechnology and the increasing demand for high-performance, energy-efficient solutions across several verticals. These layered transition metal dichalcogenides have become key enablers in future electronics due to their exceptional electrical, mechanical, and optical behavior. As traditional silicon-based technologies encounter physical and scaling limitations, these 2D materials are emerging as promising alternatives in applications such as miniaturized electronics, flexible devices, and high-speed transistors. The growing interest in compact and power-efficient hardware is particularly relevant in sectors like aerospace, defense, telecommunications, and medical devices.

Government-backed R&D initiatives across regions, including the US, Asia-Pacific, and the EU, are providing crucial financial and institutional support to push next-generation material innovation. This includes establishing national innovation centers, funding pilot manufacturing hubs, and supporting the commercialization of lab-scale research. Public-private partnerships are intensifying, particularly in the semiconductor and renewable energy domains, where the integration of 2D semiconductors into flexible substrates is becoming more feasible. The industry is responding to the growing demand for faster, smaller, and energy-optimized chips, where materials such as MoS2 and WS2 offer considerable performance advantages over legacy materials due to their tunable bandgap and superior carrier mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 billion |

| Forecast Value | $2.2 billion |

| CAGR | 8.4% |

Among fabrication techniques, the exfoliation methods segment generated USD 0.6 billion in 2024 and is predicted to grow at a CAGR of 7.9% through 2034. While exfoliation remains critical for research-grade materials and prototypes, chemical vapor deposition (CVD) is increasingly dominating scalable production due to its ability to yield uniform and high-quality thin films compatible with commercial-grade semiconductor processes. CVD enables precise layer control, broad substrate compatibility, and reproducibility at industrial volumes, which positions it as the technology of choice for transitioning from R&D to high-throughput electronics manufacturing. Many fabrication labs and pilot facilities have adopted CVD, underlining its pivotal role in bridging lab innovations with commercial-scale applications in nanomaterials.

The electronics & semiconductor segment generated notable revenues in 2024. Their unique band structure and semiconducting properties make them excellent candidates for advanced field-effect transistors, memory devices, and thin-film logic circuits. These materials allow for unprecedented flexibility and ultra-thin architectures, making them highly desirable for next-gen wearable technology, integrated photonics, and soft robotics. Researchers have already reported switching behaviors and threshold performances that match or exceed those of scaled silicon-based devices, which is pushing major semiconductor manufacturers to explore these 2D alternatives as they approach post-Moore's Law design eras.

United States Chalcogenides (MoS2, WS2, and WSe2) Market is estimated to grow at a notable CAGR during 2025-2034, driven by R&D, especially for applications in quantum technology and defense-grade semiconductors. Although bulk materials like MoS2 and WSe2 are largely imported from Asia, the U.S. leads in downstream development and integration, exporting value-added derivatives to international markets. High-tech industries in the U.S. utilize these materials in cutting-edge prototyping, pushing boundaries in optoelectronics, photonics, and next-generation transistor architecture. Companies such as ACS Material and 2D Tech play a critical role in enabling domestic research efforts, while large defense contractors and electronics manufacturers drive demand for these high-performance nanomaterials.

Prominent industry players operating in the Global Chalcogenides (MoS2, WS2, WSe2) market include SixCarbon Technology, Graphene Laboratories Inc., American Elements, ACS Material LLC, and XFNANO Materials Tech Co., Ltd. These companies are integral to both material synthesis and supply chain development. To enhance their market position and expand global reach, leading firms in the chalcogenides industry are leveraging several strategies. They are scaling up production capabilities to meet growing industrial and commercial demand while continuing to invest in high-precision material characterization and customization. Collaborations with academic institutions and national laboratories help foster cutting-edge innovation, particularly in quantum applications and flexible electronics. Key players are also entering strategic partnerships with device manufacturers to co-develop application-specific solutions using 2D materials.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Molybdenum Disulfide (MoS2)

- 5.3 Tungsten Disulfide (WS2)

- 5.4 Tungsten Diselenide (WSe2)

- 5.5 Heterostructures & Hybrids

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Synthesis & Manufacturing Technologies, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Exfoliation methods

- 6.2.1 Mechanical exfoliation

- 6.2.2 Liquid-phase exfoliation

- 6.2.3 Electrochemical exfoliation

- 6.2.4 Intercalation-assisted exfoliation

- 6.2.5 Others

- 6.3 Chemical vapor deposition (CVD)

- 6.3.1 Conventional CVD processes

- 6.3.2 Metal-organic CVD (MOCVD)

- 6.4 Physical vapor deposition (PVD)

- 6.4.1 Sputtering techniques

- 6.4.2 Pulsed laser deposition

- 6.4.3 Scalable production methods

- 6.5 Chemical synthesis routes

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Electronics & semiconductors

- 7.2.1 Field-effect transistors (FETs)

- 7.2.2 Logic gates & circuits

- 7.2.3 Memory devices

- 7.2.4 Flexible electronics

- 7.2.5 Others

- 7.3 Optoelectronics & photonics

- 7.3.1 Photodetectors

- 7.3.2 Light-emitting diodes (LEDs)

- 7.3.3 Electroluminescent devices

- 7.3.4 Solar cells / photovoltaics

- 7.3.5 Others

- 7.4 Energy storage & conversion

- 7.4.1 Rechargeable batteries

- 7.4.2 Supercapacitors

- 7.4.3 Hydrogen evolution reaction (HER) catalysts

- 7.4.4 Co2 reduction catalysts

- 7.4.5 Thermoelectric devices

- 7.4.6 Fuel cells

- 7.4.7 Others

- 7.5 Sensors & detectors

- 7.5.1 Gas sensors

- 7.5.2 Biosensors

- 7.5.3 Pressure & strain sensors

- 7.5.4 Others

- 7.6 Quantum technologies

- 7.7 Tribology & lubricants

- 7.8 Biomedical applications

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 2D Semiconductors

- 9.2 6Carbon Technology

- 9.3 ACS Material, LLC

- 9.4 Applied Nanolayers B.V.

- 9.5 Grolltex Inc.

- 9.6 HQ Graphene

- 9.7 Muke Nano

- 9.8 Nanoshel LLC

- 9.9 SixCarbon Technology

- 9.10 Ossila Ltd.

- 9.11 SVT Associates, Inc.

- 9.12 Tungsten Compounds GmbH

- 9.13 XFNANO Materials Tech Co., Ltd.

- 9.14 Intelligent Materials Pvt. Ltd.

- 9.15 American Elements

- 9.16 Graphene Laboratories Inc.

- 9.17 MSE Supplies LLC

- 9.18 Sigma-Aldrich (Merck KGaA)

- 9.19 Stanford Advanced Materials

- 9.20 Edgetech Industries LLC