|

市場調査レポート

商品コード

1773474

肋骨骨折修復システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Rib Fracture Repair Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 肋骨骨折修復システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

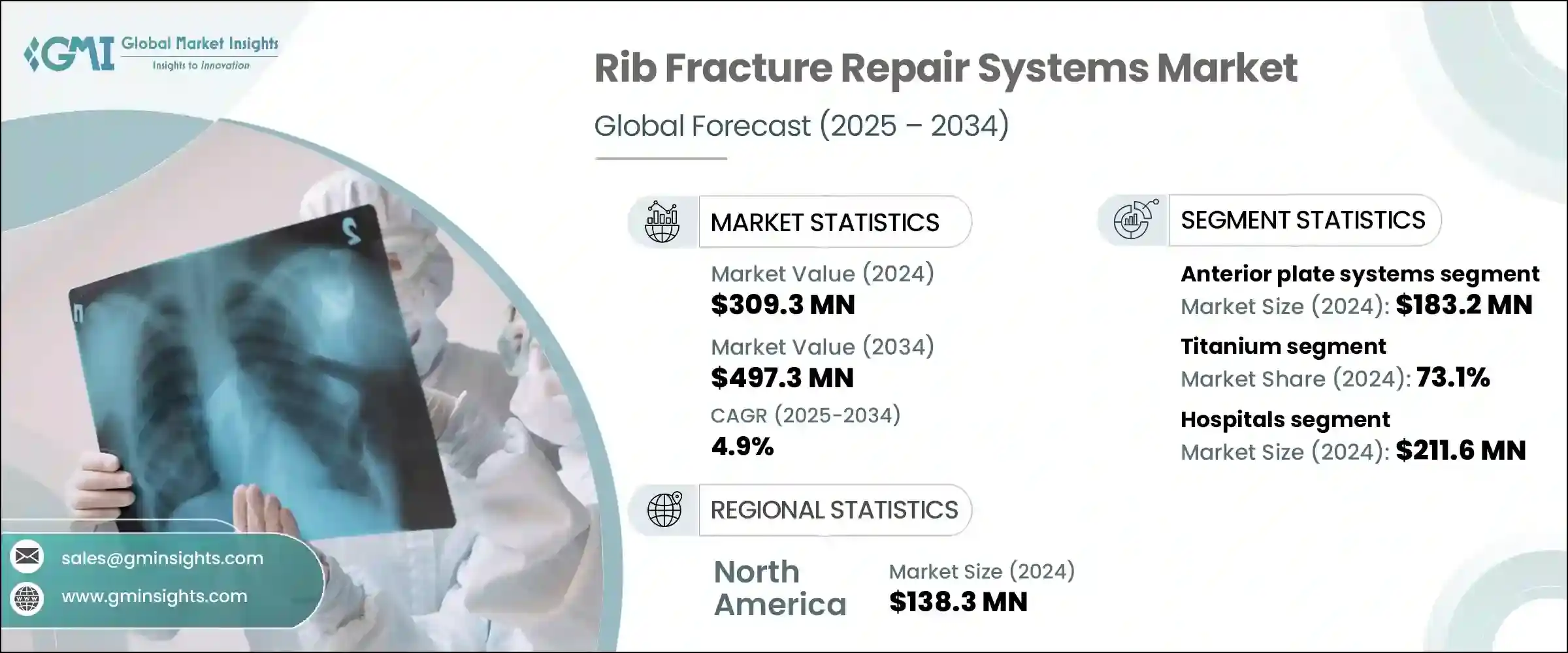

肋骨骨折修復システムの世界市場は、2024年に3億930万米ドルと評価され、CAGR 4.9%で成長し、2034年には4億9,730万米ドルに達すると予測されています。

骨折した肋骨を安定させ、整復するように設計されたこれらのシステムは、世界中で外傷関連の負傷が増加し続けているため、需要が拡大しています。自動車事故、スポーツ関連傷害、転倒に起因する事故は、特に高齢者の間で、信頼性の高い胸部外傷介入の必要性を高めています。ヘルスケアプロバイダーが早期回復と術後合併症の軽減を優先するにつれ、高度な肋骨固定技術への注目が高まっています。病院や外傷部門は、手術時間を最短にするだけでなく、患者の回復結果を改善する低侵襲システムに投資しています。解剖学的形状のプレートや薄型のチタン製システムなど、改良されたインプラントの設計により、手術の精度が向上し、痛みや入院期間が短縮されています。

デジタル画像技術の進歩と最先端の手術器具の組み合わせは、肋骨修復システムの使用を加速する上で重要な役割を果たしています。これらの技術革新は、外科医に手術中の精度の向上とより良い可視化を提供し、患者の転帰の改善と回復時間の短縮につながっています。その結果、肋骨骨折の修復は、外傷治療だけでなく、整形外科や胸部外科でも好まれるソリューションになりつつあります。リアルタイム画像と改良されたインプラント設計に支えられた低侵襲手技への信頼の高まりが、市場拡大をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3億930万米ドル |

| 予測金額 | 4億9,730万米ドル |

| CAGR | 4.9% |

前方プレートシステム分野の2024年の市場規模は1億8,320万米ドルでした。人気が高まっているのは、解剖学的な形状により、組織への刺激を最小限に抑え、術後の合併症の可能性を減らすことができるからです。これらのインプラントは、より高い快適性を必要とする患者や、審美性を重視する患者に好まれています。外科医が機能性と快適性のバランスが取れた効率的な固定システムを求める中、ルーチン手術でも緊急手術でも前方プレートが選択されることが多くなっています。

チタンベースのシステム・セグメントは2024年に73.1%のシェアを獲得したが、これは主にこの材料の比類なき強度対重量比によるものです。チタンは、余分なハードウェアの嵩張ることなく剛性を提供し、呼吸中の肋骨の自然な動きをサポートします。胸郭構造への適応性と証明された機械的一貫性は、治癒過程を通じて肋骨のアライメントを効果的に維持するのに役立ちます。チタンの卓越した生体適合性と免疫反応や炎症を引き起こす可能性の低さは、外科的修復における安全な長期的ソリューションであり、肋骨骨折修復ソリューションにおけるチタンの継続的優位性を後押ししています。

米国肋骨骨折修復システム米国は、胸部外傷の発生率が高く、ヘルスケアインフラが発達しているため、2024年の市場規模は1億2,480万米ドルと評価されました。自動車の衝突事故、加齢に伴う転倒、スポーツ外傷による負傷が頻発していることが、肋骨固定ソリューションに対する病院や外傷センターの需要を促進しています。3D画像システム、低侵襲インプラントなど、ハイエンドの外科技術が広く普及している米国の医療機関は、最先端の肋骨安定化技術をいち早く採用しています。このような環境は、手術センター全体にチタンベースの精密工学インプラントを継続的に組み込むことをサポートし、国内市場の拡大に貢献しています。

この市場に参入している主要企業には、エイブル・メディカル・デバイス、アキュメッド、アーストレックス、ジールメディカル、ジョンソン・エンド・ジョンソン、KLSマーティン、メドトロニック、ニューロ・フランス・インプラント、オルソフィックス、オステオメッド、セレクティブ・サージカル、スミス・アンド・ネフュー、ストライカー、ワストン・メディカル、ジマー・バイオメットなどがあります。この分野の有力企業は、外科医の嗜好と患者固有の解剖学的要件の両方を満たす、革新的で薄型のインプラントデザインの開発に力を注いでいます。

また、チタンやハイブリッド合金のような生体適合性と耐久性に優れた素材を製造するための研究開発にも力を入れています。外傷センターや教育病院との戦略的パートナーシップは、早期導入とフィードバック主導型の製品改良を後押ししています。企業は、FDAやCE承認を通じて世界の足跡を拡大し、新たな地域市場での低侵襲インプラントへのアクセスを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 胸部外傷の発生率の上昇

- 外科固定システムの技術的進歩

- 外来および通院手術に対する好みの増加

- 新興市場におけるヘルスケア費支出とインフラ開発の増加

- 業界の潜在的リスク&課題

- 外科手術とインプラントシステムの高コスト

- 肋骨固定ソリューションの認知度と入手のしやすさが限られている

- 市場機会

- 外傷発生率の高い未参入市場への進出

- 3Dプリントとパーソナライズされたインプラント技術の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 特許分析

- 価格分析

- 製品タイプ別

- 地域別

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021 –2034

- 主要動向

- 前方プレートシステム

- Uプレートシステム

第6章 市場推計・予測:材料別、2021 –2034

- 主要動向

- チタン

- ポリエーテルエーテルケトン(PEEK)

- その他の材料

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Able Medical Devices

- Acumed

- Arthrex

- Jeil Medical

- Johnson &Johnson

- KLS Martin

- Medtronic

- Neuro France Implants

- Orthofix

- OsteoMed

- Selective Surgical

- Smith &Nephew

- Stryker

- Waston Medical

- Zimmer Biomet

The Global Rib Fracture Repair Systems Market was valued at USD 309.3 million in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 497.3 million by 2034. These systems, designed to stabilize and realign fractured ribs, are seeing growing demand as trauma-related injuries continue to rise across the globe. Incidents stemming from vehicular accidents, sports-related injuries, and falls-particularly among the elderly-are increasing the need for reliable chest trauma interventions. As healthcare providers prioritize quicker recovery and reduced post-operative complications, the focus on advanced rib fixation techniques is intensifying. Hospitals and trauma units are investing in minimally invasive systems that not only minimize surgical duration but also improve patient recovery outcomes. Enhanced implant designs, such as anatomically shaped plates and low-profile titanium systems, are improving surgical precision while reducing pain and hospital stays.

Advancements in digital imaging technologies combined with state-of-the-art surgical instruments are playing a crucial role in accelerating the use of rib repair systems. These innovations provide surgeons with enhanced precision and better visualization during procedures, which leads to improved patient outcomes and shorter recovery times. As a result, rib fracture repair is becoming a preferred solution not only in trauma care but also within orthopedic and thoracic surgery units. The growing confidence in minimally invasive techniques, supported by real-time imaging and improved implant designs, is further driving market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $309.3 Million |

| Forecast Value | $497.3 Million |

| CAGR | 4.9% |

The anterior plate systems segment was valued at USD 183.2 million in 2024. Their growing popularity comes from their anatomical shaping, which helps minimize tissue irritation and reduce the chance of post-surgical complications. These implants are preferred in patients who require enhanced comfort or for those where aesthetics is a consideration. With surgeons seeking efficient fixation systems that balance functionality and comfort, anterior plates are increasingly selected for both routine and emergency procedures.

The titanium-based systems segment captured a 73.1% share in 2024, largely due to the material's unmatched strength-to-weight ratio. Titanium offers rigidity without excess hardware bulk, supporting the rib's natural motion during respiration. Its adaptability to the thoracic structure and proven mechanical consistency help maintain rib alignment effectively throughout the healing process. Titanium's exceptional biocompatibility and low likelihood of causing immune responses or inflammation make it a safe long-term solution in surgical repairs, fueling its continued dominance in rib fracture repair solutions.

United States Rib Fracture Repair Systems Market was valued at USD 124.8 million in 2024 due to its high rate of chest trauma cases and its advanced healthcare infrastructure. Frequent injuries caused by motor vehicle collisions, aging-related falls, and sports trauma are driving hospital and trauma center demand for rib fixation solutions. With the widespread adoption of high-end surgical technologies, including 3D imaging systems and minimally invasive implants, U.S. institutions are early adopters of cutting-edge rib stabilization technologies. This environment supports the continuous integration of titanium-based, precision-engineered implants throughout surgical centers, contributing to national market expansion.

Key players involved in the market include Able Medical Devices, Acumed, Arthrex, Jeil Medical, Johnson & Johnson, KLS Martin, Medtronic, Neuro France Implants, Orthofix, OsteoMed, Selective Surgical, Smith & Nephew, Stryker, Waston Medical, Zimmer Biomet. Prominent companies in this space are intensifying their focus on developing innovative, low-profile implant designs that meet both surgeon preferences and patient-specific anatomical requirements.

They are also emphasizing R&D to produce biocompatible and durable materials like titanium and hybrid alloys. Strategic partnerships with trauma centers and teaching hospitals help drive early adoption and feedback-driven product refinement. Firms are expanding their global footprint through FDA and CE approvals, enhancing access to minimally invasive implants in new regional markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chest trauma injuries

- 3.2.1.2 Technological advancements in surgical fixation systems

- 3.2.1.3 Growing preference for outpatient and ambulatory surgical procedures

- 3.2.1.4 Increased healthcare spending and infrastructure development in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical procedures and implant systems

- 3.2.2.2 Limited awareness and availability of rib fixation solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into underpenetrated markets with high trauma incidence

- 3.2.3.2 Integration of 3D printing and personalized implant technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anterior plate systems

- 5.3 U-plate systems

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Other materials

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profile

- 9.1 Able Medical Devices

- 9.2 Acumed

- 9.3 Arthrex

- 9.4 Jeil Medical

- 9.5 Johnson & Johnson

- 9.6 KLS Martin

- 9.7 Medtronic

- 9.8 Neuro France Implants

- 9.9 Orthofix

- 9.10 OsteoMed

- 9.11 Selective Surgical

- 9.12 Smith & Nephew

- 9.13 Stryker

- 9.14 Waston Medical

- 9.15 Zimmer Biomet