|

市場調査レポート

商品コード

1773472

無乳糖プロバイオティクスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Lactose-Free Probiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 無乳糖プロバイオティクスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

無乳糖プロバイオティクスの世界市場は、2024年には158億米ドルと評価され、CAGR 7%で成長し、2034年には297億米ドルに達すると推定されています。

これらのプロバイオティクスは、乳糖を含まずに消化と免疫の健康をサポートするため、乳糖不耐症の人、乳製品にアレルギーのある人、植物ベースの食生活を送る人に理想的です。拡大する機能性食品および栄養補助食品セクターは、腸の健康に対する消費者の関心と乳糖吸収不良の蔓延により、このカテゴリーを受け入れています。ヨーグルト、飲料、サプリメント、スナック菓子などの製品は、消化不良を起こすことなくプロバイオティクスの恩恵を受けることができます。北米とアジア太平洋の消費者は、乳製品を含まないヘルシーな代替食品を求めるようになっており、各ブランドはアーモンド、大豆、オート麦、ココナッツなどの植物性ベースを使用して革新を進めています。また、ラクトバチルス・アシドフィルスやビフィドバクテリウム3乳酸菌などの菌株を使った保存可能なカプセルや粉末も伸びています。クリーンラベル、アレルゲンフリーの選択肢、個別化された栄養の台頭が需要を促進しています。

健康に対する意識が高まるにつれ、健康志向の消費者にとって無乳糖プロバイオティクスは欠かせないものとなっています。これらの製品は、乳糖不耐症の人に対応するだけでなく、乳製品に関連する不快感を感じることなく、消化器系のサポートや免疫系への効果、腸全体の健康を積極的に求める人たちにもアピールしています。消費者は、クリーン・ラベルの製品と天然成分をますます優先するようになっており、無乳糖プロバイオティクスを毎日の栄養摂取における好ましい選択肢にしています。予防ヘルスケアや機能性食品の動向は、プロバイオティクスをバランスの取れたライフスタイルの基礎的な部分と考える人が増えていることから、この需要にさらに拍車をかけています。植物由来でアレルゲンを含まない代替食品への関心が高まる中、無乳糖プロバイオティクスは現代の食生活における重要な要素として位置づけられており、年齢層を超えてより包括的で健康志向の食品選択へのシフトを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 158億米ドル |

| 予測金額 | 297億米ドル |

| CAGR | 7% |

乳製品ベースの無乳糖プロバイオティクスセグメントは、2024年に38.2%のシェアを占め、60億米ドルに達します。このセグメントには、ヨーグルトやケフィアのような伝統的な乳製品の無乳糖バージョンが含まれ、ラクトバチルス・アシドフィルスやビフィドバクテリウム・ラクティスのような有益な菌株で強化された馴染みのある食感や風味を提供します。消費者は、味を犠牲にすることなく消化に良いという理由で、こうした選択肢を選ぶことが多いです。

乳酸菌株セグメントは、2024年に65億米ドル(41.1%)を生み出しました。この優位性は、消化器系の健康効果が証明されていることと、乳製品を含まないヨーグルト、飲料、サプリメント製品に広く使用されていることに起因しています。乳酸菌はその品種の中でも、腸の健康をサポートし、乳糖に敏感な人の消化を助けることで特に人気があります。

アジア太平洋市場は2024年に38.6%を占め、乳糖不耐症の蔓延、腸の健康に対する意識の高まり、都市化の進展、可処分所得の増加などに後押しされています。この地域の国々は、栄養研究と製品開発、特にプロバイオティクスが豊富な食品と乳児栄養への投資を進めています。科学的イノベーション、規制上のインセンティブ、消費者需要の組み合わせにより、この地域は無乳糖プロバイオティクスの成長の最前線に位置しています。

この業界の主要企業には、Danone S.A.、Probi AB、Nestle S.A.、Chr.Hansen Holding A/S.、ヤクルト本社などがあり、いずれも製品革新と流通におけるリーダーシップで知られています。無乳糖プロバイオティクス市場の主要企業は、イノベーション、ポートフォリオの拡大、戦略的パートナーシップを追求し、足跡を強化しています。各社は研究開発に投資し、植物由来のヨーグルト、そのまま飲める製剤、環境に配慮した包装など、クリーンラベルや個別化された栄養の需要に応える新しい系統や供給形態を開発しています。研究機関や臨床試験との連携は、健康強調表示を検証し、消費者の信頼を高めるのに役立ちます。メーカーはまた、小売業者や消費者直販チャネルと提携を結び、市場アクセスを拡大しています。新興市場への地理的拡大は、ローカライズされた製品ラインと文化に合わせたマーケティングによって支えられています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 乳製品ベースの無乳糖プロバイオティクス

- ヨーグルト

- ケフィア

- チーズ

- アイスクリーム

- その他

- 植物由来のプロバイオティクス

- 大豆ベース

- アーモンドベース

- ココナッツベース

- オート麦ベース

- その他

- フルーツベースのプロバイオティクス

- ジュース

- スムージー

- その他

- プロバイオティクスサプリメント

- カプセル

- タブレット

- 粉末

- 液体

- その他

第6章 市場推計・予測:プロバイオティクス菌株別、2021-2034

- 主要動向

- 乳酸菌

- L.アシドフィルス

- L.ラムノサス

- L.プランタラム

- その他

- ビフィズス菌

- B.ビフィダム

- B.ロンガム

- B.ラクティス

- その他

- 連鎖球菌

- S.サーモフィルス

- その他

- バチルス

- B.コアグランス

- バチルス・サブチリス

- その他

- サッカロミセス

- S.ボウラルディ

- その他

- その他

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- スーパーマーケットとハイパーマーケット

- 専門店

- 薬局・ドラッグストア

- オンライン小売

- その他

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 乳糖不耐症の人

- 健康志向の消費者

- 高齢者人口

- 子供と乳児

- その他

第9章 市場推計・予測:用途別、2021-2034

- 主要動向

- 消化器系の健康

- 免疫サポート

- 体重管理

- 女性の健康

- 小児の健康

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Nestle S.A.

- Danone S.A.

- Yakult Honsha Co., Ltd.

- Chr. Hansen Holding A/S

- Probi AB

- BioGaia AB

- Lifeway Foods, Inc.

- General Mills, Inc.(Yoplait)

- Fonterra Co-operative Group

- Kerry Group

- Lallemand Inc.

- DSM

- DuPont(IFF)

- Morinaga Milk Industry Co., Ltd.

- Bifodan A/S

- Probiotical S.p.A.

- Winclove Probiotics

- Biosearch Life

- Culturelle(i-Health, Inc.)

- GoodBelly(NextFoods, Inc.)

- Ganeden, Inc.(Kerry)

- Attune Foods

- Valio Ltd.

- Arla Foods

- Organic Valley

- Stonyfield Farm, Inc.

- Meiji Holdings Co., Ltd.

- Chobani, LLC

- Yili Group

- Mengniu Dairy

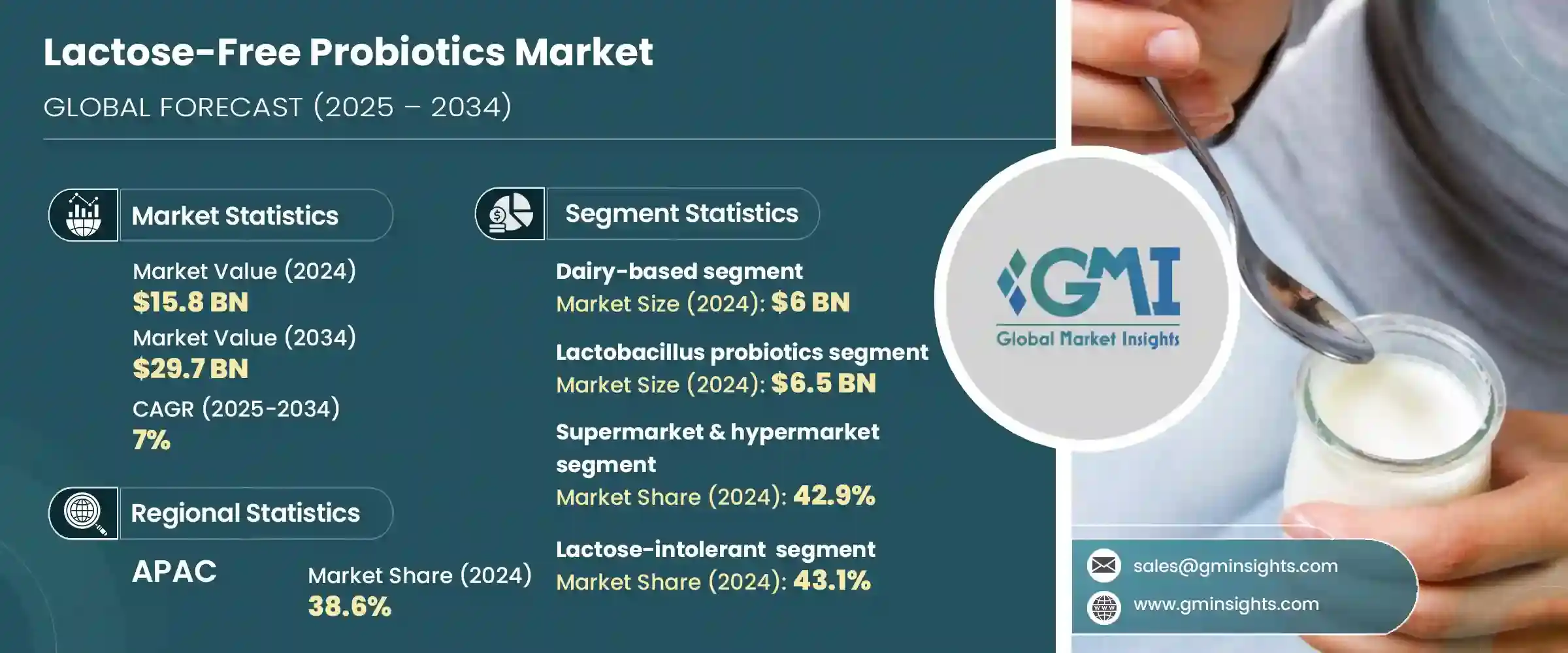

The Global Lactose-Free Probiotics Market was valued at USD 15.8 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 29.7 billion by 2034. These probiotics support digestive and immune health without containing lactose, making them ideal for lactose-intolerant individuals, those allergic to dairy, or people following plant-based diets. The expanding functional food and nutraceutical sector has embraced this category due to consumer interest in gut health and the prevalence of lactose malabsorption. Products such as yogurts, beverages, supplements, and snacks offer probiotic benefits without digestive discomfort. With consumers in North America and Asia-Pacific increasingly demanding healthy, dairy-free alternatives, brands are innovating using plant-based bases like almond, soy, oat, and coconut. There's also growth in shelf-stable capsules and powders featuring strains such as Lactobacillus acidophilus and Bifidobacterium3lactis. The rise of clean-label, allergen-free options, and personalized nutrition is fueling demand.

As awareness around health grows, lactose-free probiotics are becoming essential for wellness-focused consumers. These products not only cater to individuals with lactose intolerance but also appeal to those actively seeking digestive support, immune system benefits, and overall gut health without the discomfort associated with dairy. Consumers are increasingly prioritizing clean-label products and natural ingredients, making lactose-free probiotics a preferred option in daily nutrition. The trend toward preventive healthcare and functional foods has further fueled this demand, as more people view probiotics as a foundational part of a balanced lifestyle. With rising interest in plant-based and allergen-free alternatives, lactose-free probiotics are positioned as a key element in modern dietary habits, reflecting a shift toward more inclusive and health-conscious food choices across age groups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.8 Billion |

| Forecast Value | $29.7 Billion |

| CAGR | 7% |

Dairy-based lactose-free probiotics segment held a 38.2% share in 2024, representing USD 6 billion. This segment includes lactose-free versions of traditional dairy products like yogurt and kefir, offering familiar textures and flavors enhanced with beneficial strains like Lactobacillus acidophilus and Bifidobacterium lactis. Consumers often choose these options because they provide digestive benefits without sacrificing taste.

The Lactobacillus strain segment generated USD 6.5 billion or 41.1% in 2024. This dominance stems from its proven digestive health benefits and its extensive use in dairy-free yogurts, beverages, and supplement products. Among its varieties, Lactobacillus acidophilus is especially popular for supporting gut wellness and aiding digestion in lactose-sensitive individuals.

Asia-Pacific Lactose-Free Probiotics Market held 38.6% in 2024, propelled by widespread lactose intolerance and growing awareness of gut health, rising urbanization, and increased disposable income. Countries in this region are investing in nutritional research and product development, especially in probiotic-rich foods and baby nutrition. The combination of scientific innovation, regulatory incentives, and consumer demand has positioned the region at the forefront of lactose-free probiotic growth.

Key players in the industry include Danone S.A., Probi AB, Nestle S.A., Chr. Hansen Holding A/S, and Yakult Honsha Co., Ltd., are all known for their leadership in product innovation and distribution. Leading companies in the lactose-free probiotics market are pursuing innovation, portfolio expansion, and strategic partnerships to enhance their footprint. Firms are investing in R&D to develop new strains and delivery formats-such as plant-based yogurts, ready-to-drink formulations, and eco-friendly packaging-to meet clean-label and personalized nutrition demands. Collaboration with research institutions and clinical trials helps validate health claims, strengthening consumer trust. Manufacturers are also forging alliances with retailers and direct-to-consumer channels to expand market access. Geographic expansion into emerging markets is supported by localized product lines and culturally tailored marketing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based lactose-free probiotics

- 5.2.1 Yogurt

- 5.2.2 Kefir

- 5.2.3 Cheese

- 5.2.4 Ice cream

- 5.2.5 Others

- 5.3 Plant-based probiotics

- 5.3.1 Soy-based

- 5.3.2 Almond-based

- 5.3.3 Coconut-based

- 5.3.4 Oat-based

- 5.3.5 Others

- 5.4 Fruit-based probiotics

- 5.4.1 Juices

- 5.4.2 Smoothies

- 5.4.3 Others

- 5.5 Probiotic supplements

- 5.5.1 Capsules

- 5.5.2 Tablets

- 5.5.3 Powders

- 5.5.4 Liquids

- 5.5.5 Others

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.2.1 L. acidophilus

- 6.2.2 L. rhamnosus

- 6.2.3 L. plantarum

- 6.2.4 Others

- 6.3 Bifidobacterium

- 6.3.1 B. bifidum

- 6.3.2 B. longum

- 6.3.3 B. lactis

- 6.3.4 Others

- 6.4 Streptococcus

- 6.4.1 S. thermophilus

- 6.4.2 Others

- 6.5 Bacillus

- 6.5.1 B. coagulans

- 6.5.2 B. subtilis

- 6.5.3 Others

- 6.6 Saccharomyces

- 6.6.1 S. boulardii

- 6.6.2 Others

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets & hypermarkets

- 7.3 Specialty stores

- 7.4 Pharmacies & drugstores

- 7.5 Online retail

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Lactose-intolerant individuals

- 8.3 Health-conscious consumers

- 8.4 Elderly population

- 8.5 Children & infants

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Digestive health

- 9.3 Immune support

- 9.4 Weight management

- 9.5 Women's health

- 9.6 Pediatric health

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 Danone S.A.

- 11.3 Yakult Honsha Co., Ltd.

- 11.4 Chr. Hansen Holding A/S

- 11.5 Probi AB

- 11.6 BioGaia AB

- 11.7 Lifeway Foods, Inc.

- 11.8 General Mills, Inc. (Yoplait)

- 11.9 Fonterra Co-operative Group

- 11.10 Kerry Group

- 11.11 Lallemand Inc.

- 11.12 DSM

- 11.13 DuPont (IFF)

- 11.14 Morinaga Milk Industry Co., Ltd.

- 11.15 Bifodan A/S

- 11.16 Probiotical S.p.A.

- 11.17 Winclove Probiotics

- 11.18 Biosearch Life

- 11.19 Culturelle (i-Health, Inc.)

- 11.20 GoodBelly (NextFoods, Inc.)

- 11.21 Ganeden, Inc. (Kerry)

- 11.22 Attune Foods

- 11.23 Valio Ltd.

- 11.24 Arla Foods

- 11.25 Organic Valley

- 11.26 Stonyfield Farm, Inc.

- 11.27 Meiji Holdings Co., Ltd.

- 11.28 Chobani, LLC

- 11.29 Yili Group

- 11.30 Mengniu Dairy