|

市場調査レポート

商品コード

1773471

コンパニオンアニマル診断市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Companion Animal Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンパニオンアニマル診断市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

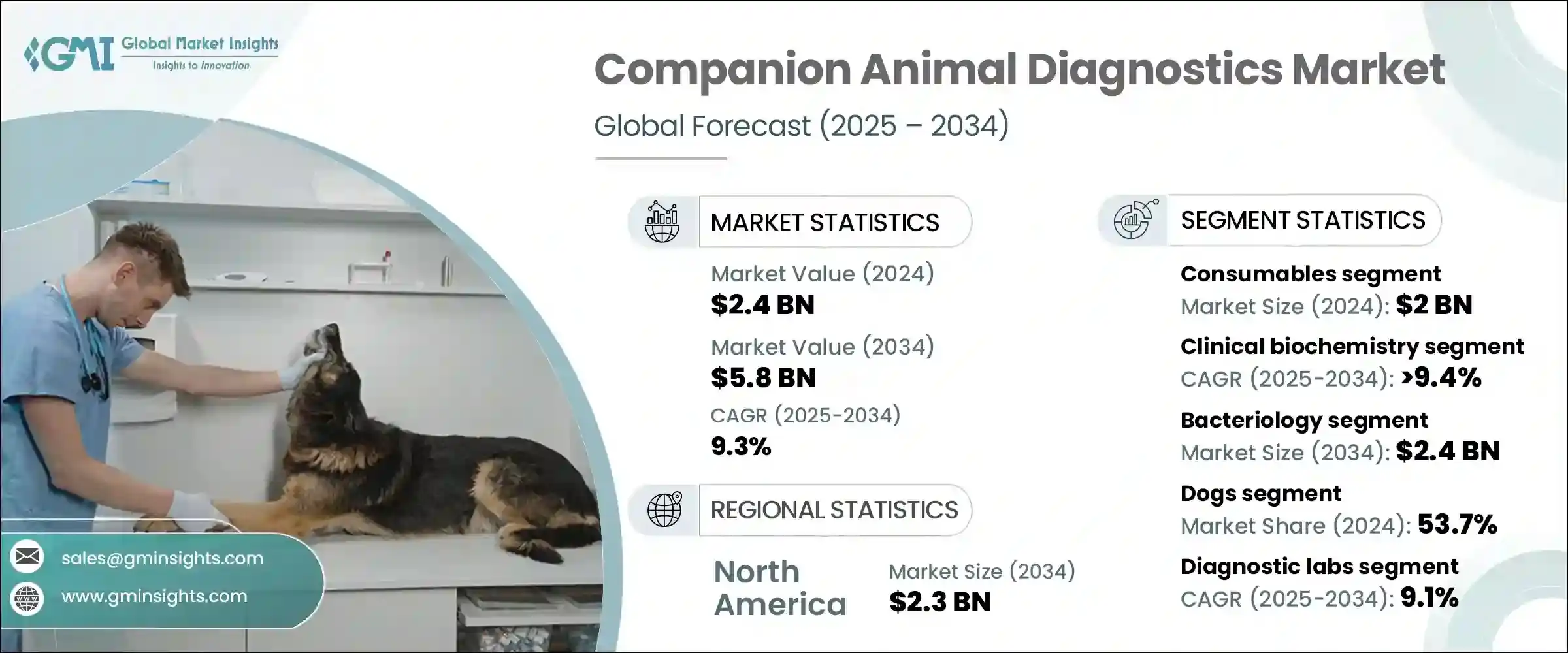

世界のコンパニオンアニマル診断市場は、2024年には24億米ドルと評価され、CAGR 9.3%で成長し、2034年には58億米ドルに達すると推定されています。

この成長の原動力は、世界のペット飼育者数の増加、ペット同伴への志向の高まり、動物の慢性・感染症診断の急増です。ペットの世話が家庭の不可欠な一部となり、獣医サービスへの支出は増加の一途をたどっています。ペットの飼い主は、動物を家族の一員として扱うようになり、その結果、定期的な健康診断、予防医療、タイムリーな診断が行われるようになっています。このような文化的変化によって、動物の健康がより重視されるようになり、高度な診断ツールやサービスに対する需要を大幅に押し上げています。

市場の拡大は、人獣共通感染症に対する意識の高まりと、合併症を回避するための早期診断の重要性にも支えられています。獣医の専門家は、臓器機能不全、代謝問題、感染症などの状態を評価するために診断に頼るようになっており、これがこの分野の成長をさらに後押ししています。さらに、技術の進歩は、迅速かつ正確で、侵襲性の低い診断技術を可能にすることで、この分野を再構築しています。獣医学的診断における革新は、より迅速な納期と治療戦略とのより良い統合を可能にし、診断を動物ヘルスケアにおける重要な要素にしています。獣医医療のインフラが世界的に強化されるにつれ、診断製品およびサービスに対する需要は増加基調を維持すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 58億米ドル |

| CAGR | 9.3% |

製品セグメンテーションでは、市場は機器と消耗品に分けられます。2024年には、消耗品セグメントが20億米ドルで優位を占める。この優位性は、各診断プロセスにおいて試薬、検査キット、スライド、チューブなどの消耗品が不可欠な役割を果たすためです。機器とは異なり、消耗品は検査のたびに必要とされるため、定期的な購入が必要となり、安定した市場収益が得られます。動物検査の頻度が診療所や病院全体で増加するにつれ、消耗品の需要もそれに追随すると予想されます。定期検診や予防検診の動向は、使用量をさらに押し上げます。さらに、より多くの診断手順が迅速かつポイントオブケア形式へと移行しているため、シングルユースアプリケーション用に調整された消耗品が標準となりつつあり、セグメント成長を後押ししています。

アプリケーション別に分析すると、細菌学セグメントは2024年に主要カテゴリーに浮上し、2034年には24億米ドルに達すると予想されています。このセグメントは、コンパニオンアニマルの細菌感染を検出する上で重要な役割を果たしており、それは幅広い健康状態にわたって一般的に見られます。皮膚や泌尿器の感染から呼吸器や胃腸の問題に至るまで、細菌病原体の正確な同定は治療計画に不可欠です。培養方法の改善や迅速な抗原検出など、細菌学的診断における現代の進歩は、診断効率を著しく高めています。このような技術が中央検査室とポイントオブケア施設の両方で利用可能になりつつあることは、診断学における細菌学の地位を強化しています。

動物の種類別では、イヌが2024年に53.7%の圧倒的なシェアで市場をリードしました。この優位性は、コンパニオンアニマルとして犬が広く飼われていることと、犬のヘルスケアへの投資が増加していることに起因しています。犬の慢性疾患の頻度が高いため、糖尿病、腎臓疾患、関節炎、心血管疾患などの診断検査に対する需要が増加しています。定期診断が犬の疾病管理に不可欠となり、この分野の需要をさらに押し上げています。

最終用途に関しては、診断ラボが2024年に最大の市場シェアを占め、2025年から2034年にかけてCAGR 9.1%で拡大すると予測されています。これらのラボにはハイエンドの診断システムが装備され、訓練を受けた専門家が常駐しているため、大量のサンプルを効率的に扱うことができます。正確で迅速かつ包括的な結果を提供する能力により、信頼できる診断サポートを求める獣医師に好まれています。ペットの飼い主が増え、動物の定期的な健康診断を選ぶ人が増えるにつれ、診断ラボの役割はさらに重要になっています。

地域別では、北米が2024年に10億米ドルで世界のコンパニオンアニマル診断市場をリードし、2034年には23億米ドルに達し、CAGR 8.8%で成長すると予測されています。2024年には米国だけで8億9,330万米ドルを占める。ペットの飼育率が高く、最先端の診断サービスが広く普及していることが、この地域の需要を牽引しています。さらに、強力な獣医ヘルスケアネットワークと動物の健康に対する消費者の支出の増加が、北米の市場業績を引き続き強化しています。

競合情勢は、いくつかの世界的・地域的企業によって形成されており、IDEXX Laboratories、Thermo Fisher Scientific、Zoetis、Heska Corporationなどの主要企業が、世界市場の約60%から65%を占めています。これらの企業は、幅広い製品ポートフォリオ、地理的なリーチ、研究開発への継続的な投資を通じてリーダーシップを維持しています。その一方で、数多くの地元企業がコスト効率の高い診断ソリューションを提供し、提携、買収、新製品開発を通じて製品ラインを拡大することで競合を激化させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ペット動物を飼う傾向が増加

- 感染症および人獣共通感染症の蔓延率の上昇

- 政府の好ましい取り組み

- コンパニオン診断の進歩

- ペット保険の導入増加

- 業界の潜在的リスク&課題

- 動物実験に伴う法外なコスト

- 獣医治療にかかる自己負担額が低い

- 市場機会

- 技術の進歩とポイントオブケア分子ツール

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 消耗品

- 機器

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 臨床生化学

- 血糖モニタリング

- 血液ガスおよび電解質分析

- その他の臨床生化学検査

- 免疫診断

- ラテラルフローアッセイ

- ELISA

- 免疫測定分析装置

- その他の免疫診断検査

- 分子診断

- PCR

- マイクロアレイ

- その他の分子診断検査

- 血液学

- 尿検査

- その他の技術

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 細菌学

- 病理学

- 寄生虫学

- その他の用途

第8章 市場推計・予測:動物の種類別、2021-2034

- 主要動向

- 犬

- 猫

- 馬

- その他の動物の種類

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 動物病院および診療所

- 診断ラボ

- 在宅ケア環境

- その他の用途

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ポーランド

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- フィリピン

- タイ

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- ペルー

- チリ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- エジプト

- イスラエル

第11章 企業プロファイル

- bioMerieux

- BioNote

- Bio-Rad Laboratories

- Boehringer Ingelheim International

- Heska Corporation(Mars)

- Idexx laboratories

- KogeneBiotech

- Median Diagnostics

- Neogen Corporation

- Randox

- Thermo Fischer Scientific

- Virbac

- VetAll Laboratories

- Qiagen

- Zoetis

The Global Companion Animal Diagnostics Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 5.8 billion by 2034. This growth is driven by a rising number of pet owners worldwide, a growing inclination toward pet companionship, and a surge in the diagnosis of chronic and infectious diseases in animals. With pet care becoming an integral part of households, spending on veterinary services continues to climb. Pet owners are increasingly treating animals as part of the family, which results in regular health checks, preventive care, and timely diagnosis. This cultural shift has led to a stronger focus on animal wellness, significantly pushing up the demand for advanced diagnostic tools and services.

The market expansion is also underpinned by the increasing awareness of zoonotic diseases and the importance of early diagnosis in avoiding complications. Veterinary professionals are relying more on diagnostics to assess conditions like organ dysfunction, metabolic issues, and infections, which has further fueled the growth of this sector. Moreover, technological advancements are reshaping the landscape by enabling fast, accurate, and less invasive diagnostic techniques. Innovations in veterinary diagnostics are allowing faster turnaround times and better integration with treatment strategies, making diagnostics a critical component of animal healthcare. As veterinary care infrastructure strengthens globally, the demand for diagnostic products and services is expected to remain on an upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 9.3% |

In terms of product segmentation, the market is divided into instruments and consumables. In 2024, the consumables segment dominated with a value of USD 2 billion. This dominance is due to the essential role of consumables like reagents, testing kits, slides, and tubes in each diagnostic process. Unlike instruments, consumables are required for every test, resulting in recurring purchases and consistent market revenue. As the frequency of animal testing increases across clinics and hospitals, the demand for consumables is expected to follow suit. The trend toward regular checkups and preventive screenings further boosts usage. Additionally, with more diagnostic procedures moving toward rapid and point-of-care formats, consumables tailored for single-use applications are becoming standard, pushing segmental growth.

When analyzed by application, the bacteriology segment emerged as the leading category in 2024 and is expected to reach USD 2.4 billion by 2034. This segment plays a crucial role in detecting bacterial infections in companion animals, which are commonly seen across a wide range of health conditions. From skin and urinary infections to respiratory and gastrointestinal issues, accurate identification of bacterial pathogens is essential for treatment planning. Modern advancements in bacteriological diagnostics, including improved culturing methods and rapid antigen detection, have significantly elevated diagnostic efficiency. The increasing availability of such technologies at both central labs and point-of-care facilities strengthens the position of bacteriology in the diagnostics landscape.

Based on animal type, the dogs segment led the market with a commanding share of 53.7% in 2024. This dominance is attributed to the widespread ownership of dogs as companion animals and the rising investment in their healthcare. The higher frequency of chronic diseases in dogs has resulted in increased demand for diagnostic tests for conditions such as diabetes, kidney disorders, arthritis, and cardiovascular problems. Routine diagnostics have become essential for disease management in dogs, further driving the demand within this segment.

Regarding end use, diagnostic labs held the largest market share in 2024 and are anticipated to expand at a CAGR of 9.1% from 2025 to 2034. These labs are equipped with high-end diagnostic systems and staffed with trained professionals, allowing them to handle large sample volumes efficiently. Their ability to deliver accurate, quick, and comprehensive results makes them a preferred choice for veterinarians seeking reliable diagnostic support. As the number of pet owners increases and more people opt for regular health assessments for their animals, the role of diagnostic labs becomes even more central.

Regionally, North America led the global companion animal diagnostics market with a value of USD 1 billion in 2024, projected to reach USD 2.3 billion by 2034, growing at a CAGR of 8.8%. The U.S. alone accounted for USD 893.3 million in 2024. High pet ownership rates and the widespread availability of cutting-edge diagnostic services drive demand in the region. Additionally, a strong veterinary healthcare network and rising consumer expenditure on animal wellness continue to bolster market performance in North America.

The competitive landscape is shaped by several global and regional players, with key companies such as IDEXX Laboratories, Thermo Fisher Scientific, Zoetis, and Heska Corporation collectively holding around 60% to 65% of the global market. These firms maintain their leadership through broad product portfolios, geographic reach, and continuous investment in research and development. Alongside them, numerous local players are intensifying competition by offering cost-effective diagnostic solutions and expanding their product lines through partnerships, acquisitions, and new product development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Animal type

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing trend of adopting pet animals

- 3.2.1.2 Rising prevalence of infectious and zoonotic diseases

- 3.2.1.3 Favorable government initiatives

- 3.2.1.4 Advancements in companion diagnostics

- 3.2.1.5 Increasing adoption of pet insurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibitive cost associated with animal tests

- 3.2.2.2 Low out of pocket expenditure on veterinary care

- 3.2.3 Market opportunities

- 3.2.3.1 Technological advancements and point-of-care molecular tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical biochemistry

- 6.2.1 Glucose monitoring

- 6.2.2 Blood gas and electrolyte analysis

- 6.2.3 Other clinical biochemistry tests

- 6.3 Immunodiagnostics

- 6.3.1 Lateral flow assays

- 6.3.2 ELISA

- 6.3.3 Immunoassay analyzers

- 6.3.4 Other immunodiagnostic tests

- 6.4 Molecular diagnostics

- 6.4.1 PCR

- 6.4.2 Microarrays

- 6.4.3 Other molecular diagnostic tests

- 6.5 Hematology

- 6.6 Urinalysis

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Bacteriology

- 7.3 Pathology

- 7.4 Parasitology

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Horses

- 8.5 Other animal types

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Diagnostic labs

- 9.4 Home care settings

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.5.5 Peru

- 10.5.6 Chile

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

- 10.6.5 Egypt

- 10.6.6 Israel

Chapter 11 Company Profiles

- 11.1 bioMerieux

- 11.2 BioNote

- 11.3 Bio-Rad Laboratories

- 11.4 Boehringer Ingelheim International

- 11.5 Heska Corporation (Mars)

- 11.6 Idexx laboratories

- 11.7 KogeneBiotech

- 11.8 Median Diagnostics

- 11.9 Neogen Corporation

- 11.10 Randox

- 11.11 Thermo Fischer Scientific

- 11.12 Virbac

- 11.13 VetAll Laboratories

- 11.14 Qiagen

- 11.15 Zoetis