|

市場調査レポート

商品コード

1773470

ペットサービスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Pet Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ペットサービスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月25日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

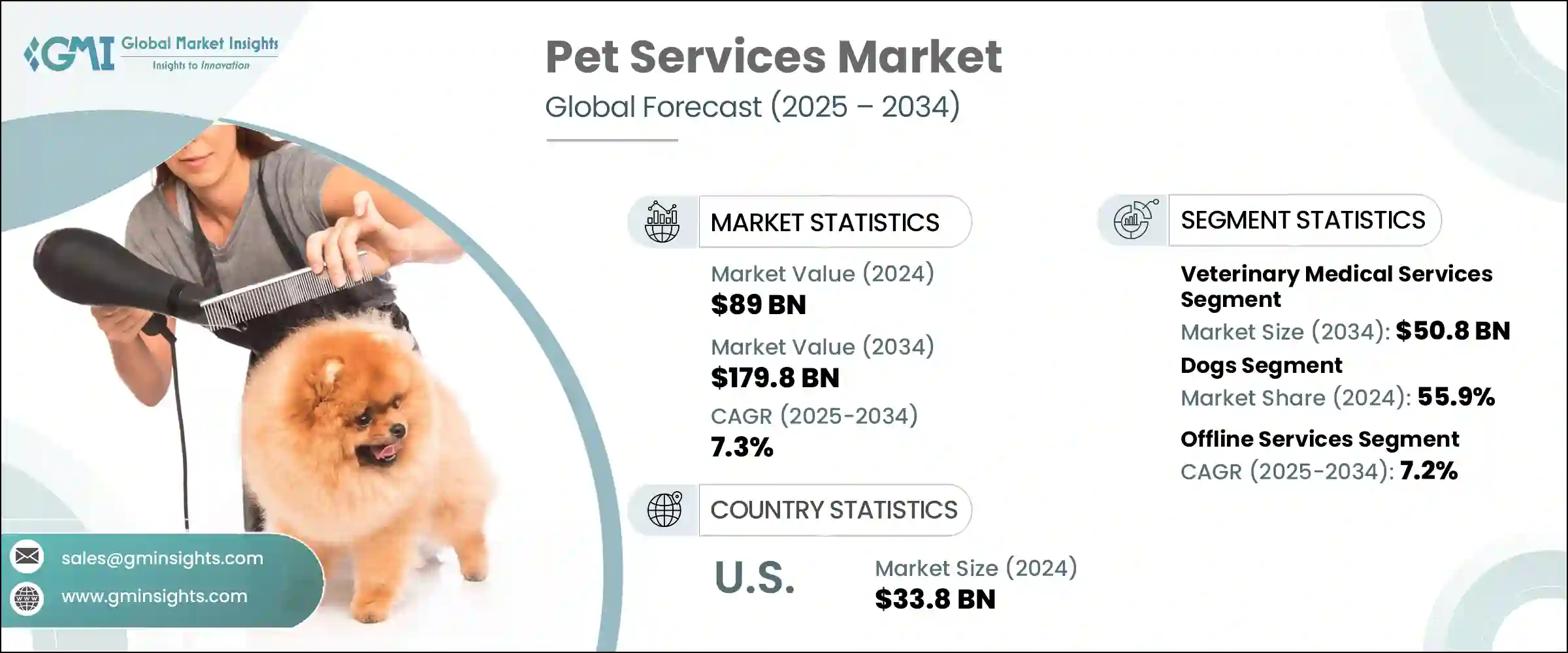

世界のペットサービス市場は、2024年に890億米ドルと評価され、CAGR 7.3%で成長し、2034年には1,798億米ドルに達すると推定されています。

この成長は、関節炎、糖尿病、肥満など、ペットの慢性的な健康問題の発生率が増加していることが主な要因であり、定期検診、リハビリテーションケア、専門治療の需要が高まっています。ペットの飼い主は健康と衛生をより重視するようになり、その結果、専門家によるグルーミング、動物病院への受診、保険への加入が急増しています。

さらに、バーチャル獣医予約やオンライン予約システムといったデジタル・ツールへのシフトが、ケア・サービスへのアクセシビリティを高めています。このような技術主導の変革は、ペット飼育率の上昇やヒューマニゼーションの動向と相まって、世界の市場全体でペットケアサービスのエコシステムを強化しています。ペットサービスは、コンパニオンアニマルのニーズに合わせて、医療・非医療の両面から幅広いサービスを提供しています。グルーミング、獣医療、デイケア、ボーディング、トレーニングなどが含まれます。保険適用範囲の拡大は、プレミアムサービスへのアクセスをさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 890億米ドル |

| 予測金額 | 1,798億米ドル |

| CAGR | 7.3% |

これと並行して、獣医療分野ではデジタル変革が進行しており、医療提供やアクセス方法が再定義されつつあります。遠隔診察の普及は、飼い主の利便性を向上させるだけでなく、特に遠隔地や十分なサービスを受けられない地域において、タイムリーな医療介入を可能にしています。ウェアラブル首輪や埋め込み型センサーを含むスマート健康追跡デバイスは、ペットのバイタルサイン、活動レベル、行動変化をリアルタイムで監視することを可能にし、獣医師と飼い主の双方に実用的な洞察力を与えています。

獣医医療サービス分野は、2024年に264億米ドルを生み出し、2034年には508億米ドルに達し、CAGR 6.8%で成長すると予測されています。このセグメントには、一般医療、専門治療、救急サービスが含まれます。ペット数増加と感染症や慢性疾患の増加が相まって、動物医療の需要が加速しています。さらに、都市部ではペットの人間化が進み、より多くの家庭が高級なペットサービスや製品に予算を割くようになり、支出パターンに影響を与えています。ヘルスケア・インフラの改善により、高度な獣医療がペットの飼い主にとってより利用しやすくなっています。その結果、医療サービスは、ペットの健康に対する意識と投資意欲の高まりに支えられ、市場全体の基礎的な柱であり続けています。

犬セグメントは、コンパニオンアニマルとしての犬の普及とペットと飼い主の間に共有される感情的な絆の増加が燃料となり、2024年には55.9%のシェアを占めました。犬の飼い主は、デイケア、グルーミング、健康診断といった質の高いサービスに支出を増やしており、包括的なペットケアの価値が高まっています。犬種に特化したグルーミング、専門的なトレーニング、高度なヘルスケア・オプションの需要は急増し続けています。さらに、商業ペットケア施設の拡大やデジタルサービスプラットフォームの出現により、犬関連サービスがより便利で利用しやすくなり、世界市場での地位が確固たるものとなっています。

北米ペットサービス市場は、2024年に357億米ドルを生み出し、2034年にはCAGR 6.9%で694億米ドルに達すると予測されています。この地域のリーダーシップは、ペットケアのインフラが高度に発達していること、ペットの所有率が高まっていること、ペットの健康に対する意識が高まっていることに起因しています。この地域の国々は、予防的な獣医学的ケアや個人に合わせたグルーミングなどのハイエンド・サービスへの需要が急増しています。また、近代的な動物病院、プレミアム・サービス・チェーン、デジタル・ペットケア・ソリューションへのアクセスが広がっていることも成長を後押ししています。さらに、ペットの飼い主はテクノロジー主導のプラットフォームに積極的に関与し、サービスのスケジュールや管理を行っています。地域企業はサービス・ポートフォリオを拡大し、消費者の嗜好を活用しており、これが一貫した市場拡大に寄与しています。

世界ペットサービス市場における有力企業には、IDEXX Laboratories、Dogtopia、PetIQ、VIP Petcare、Petfirstヘルスケア、PetSmart、Hartville Group、Vetcor、Anicom Holding、The Barkley Pet Hotel &Day Spa、DogVacay、Mars、K9 Resorts、Rover、Figo Pet Insurance、Hollard、Ethos Veterinary Healthなどがあります。市場のポジショニングを強化するため、ペットサービス分野の企業はサービスの多様化とデジタルトランスフォーメーションに投資しています。

多くはアプリベースのプラットフォームや遠隔医療サービスを採用し、顧客体験を合理化してサービスの利便性を高めています。獣医ネットワーク、保険プロバイダー、ハイテク企業との戦略的パートナーシップは、ケアの質を向上させながら、サービスのフットプリントを拡大するのに役立っています。企業はまた、ウェルネス・プログラムやサブスクリプション・ベース・モデルを立ち上げ、顧客ロイヤルティと経常収益源を強化しています。さらに、獣医師や介護スタッフのための継続的なトレーニングプログラムは、サービス水準を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペット飼育率の上昇

- ペットの人間化のトレンド

- ペット飼い主の健康意識の高まり

- 獣医サービスにおける技術の進歩

- 業界の潜在的リスク&課題

- 高いサービスコスト

- 動物福祉に関する規制上の課題

- 市場機会

- デジタル変革とオンライン予約の成長

- ペット保険の拡大

- 促進要因

- 成長可能性分析

- ペット数統計 2024年

- 規制情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:サービス種別、2021~2034年

- 主要動向

- ペットグルーミング

- ペットの宿泊とデイケア

- ペットトレーニングサービス

- ペット保険

- 獣医医療サービス

- 一般サービス

- 専門サービス

- 緊急サービス

- その他のサービスタイプ

第6章 市場推計・予測:ペットの種類別、2021~2034年

- 主要動向

- 犬

- 猫

- 鳥

- 魚類

- 馬

- その他のペットの種類

第7章 市場推計・予測:提供方法別、2021~2034年

- 主要動向

- オンラインサービス

- オフラインサービス

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Anicom Holding

- Dogtopia

- DogVacay

- Ethos Veterinary Health

- Figo Pet Insurance

- Hartville Group

- Hollard

- IDEXX Laboratories

- K9 Resorts

- Mars

- Petfirst Healthcare

- PetIQ

- PetSmart

- Rover

- The Barkley Pet Hotel &Day Spa

- Vetcor

- VIP Petcare

The Global Pet Services Market was valued at USD 89 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 179.8 billion by 2034. This growth is largely driven by the increasing incidence of chronic health issues in pets, such as arthritis, diabetes, and obesity, which prompts a higher demand for routine check-ups, rehabilitation care, and specialty treatments. Pet owners are placing more importance on wellness and hygiene, resulting in a spike in professional grooming, veterinary visits, and insurance enrollments.

Additionally, the shift toward digital tools-such as virtual vet appointments and online booking systems-has enhanced the accessibility of care services. This tech-driven transformation, combined with rising pet ownership and humanization trends, is strengthening the pet care service ecosystem across global markets. Pet services encompass a wide range of offerings tailored to companion animals' needs, both medical and non-medical. These include grooming, veterinary care, daycare, boarding, and training. Expanding insurance coverage has further boosted access to premium services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $89 Billion |

| Forecast Value | $179.8 Billion |

| CAGR | 7.3% |

In parallel, the veterinary healthcare sector is undergoing a digital transformation that is redefining how pet services are delivered and accessed. The growing integration of teleconsultations is not only improving convenience for pet owners but also ensuring timely medical intervention, especially in remote or underserved areas. Smart health tracking devices, including wearable collars and implantable sensors, are enabling real-time monitoring of pets' vital signs, activity levels, and behavioral changes-empowering both veterinarians and owners with actionable insights.

The veterinary medical services segment generated USD 26.4 billion in 2024 and is projected to reach USD 50.8 billion by 2034, growing at a CAGR of 6.8%. This segment includes general medical care, specialized treatments, and emergency services. A growing population of pets combined with increasing occurrences of both infectious and chronic conditions is accelerating the demand for veterinary care. Additionally, rising pet humanization in urban settings is influencing spending patterns, as more households allocate budgets for premium pet services and products. Improvements in healthcare infrastructure are making advanced veterinary care more accessible to pet owners. As a result, medical services remain a foundational pillar in the overall market, supported by growing awareness and willingness to invest in pet health.

The dogs segment held a 55.9% share in 2024 fueled by the widespread adoption of dogs as companion animals and the increasing emotional bond shared between pets and owners. Dog owners are spending more on high-quality services such as daycare, grooming, and health checkups, reinforcing the value of comprehensive pet care. The demand for breed-specific grooming, specialized training, and advanced healthcare options continues to surge. Additionally, the expansion of commercial pet care establishments and the emergence of digital service platforms have made dog-related services more convenient and accessible, solidifying their position in the global market.

North America Pet Services Market generated USD 35.7 billion in 2024 and is expected to reach USD 69.4 billion by 2034, with a CAGR of 6.9%. The region's leadership stems from its highly developed pet care infrastructure, increasing pet ownership, and heightened awareness about pet well-being. Countries across the region are seeing a surge in demand for high-end services such as preventive veterinary care and personalized grooming. The growth is also propelled by widespread access to modern veterinary clinics, premium service chains, and digital pet care solutions. Moreover, pet owners are actively engaging with technology-driven platforms to schedule and manage services. Regional companies are expanding service portfolios and capitalizing on consumer preferences, which is contributing to consistent market expansion.

Prominent players in the Global Pet Services Market include IDEXX Laboratories, Dogtopia, PetIQ, VIP Petcare, Petfirst Healthcare, PetSmart, Hartville Group, Vetcor, Anicom Holding, The Barkley Pet Hotel & Day Spa, DogVacay, Mars, K9 Resorts, Rover, Figo Pet Insurance, Hollard, Ethos Veterinary Health. To strengthen their market positioning, companies in the pet services space are investing in service diversification and digital transformation.

Many are adopting app-based platforms and telehealth services to streamline customer experiences and increase service convenience. Strategic partnerships with veterinary networks, insurance providers, and tech firms help expand their service footprint while also improving care quality. Firms are also launching wellness programs and subscription-based models to enhance customer loyalty and recurring revenue streams. Moreover, continuous training programs for veterinary and care staff are elevating service standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service type

- 2.2.3 Pet type

- 2.2.4 Delivery mode

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership rate

- 3.2.1.2 Pet humanization trend

- 3.2.1.3 Increasing health awareness among pet owners

- 3.2.1.4 Growing technological advancements in veterinary services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High service costs

- 3.2.2.2 Regulatory challenges on animal welfare

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in digital transformation and online booking

- 3.2.3.2 Expanding pet insurance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pet population statistics 2024

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pet grooming

- 5.3 Pet boarding and daycare

- 5.4 Pet training services

- 5.5 Pet insurance

- 5.6 Veterinary medical services

- 5.6.1 General services

- 5.6.2 Specialty services

- 5.6.3 Emergency services

- 5.7 Other service types

Chapter 6 Market Estimates and Forecast, By Pet Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fishes

- 6.6 Horses

- 6.7 Other pet types

Chapter 7 Market Estimates and Forecast, By Delivery Mode, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Online services

- 7.3 Offline services

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anicom Holding

- 9.2 Dogtopia

- 9.3 DogVacay

- 9.4 Ethos Veterinary Health

- 9.5 Figo Pet Insurance

- 9.6 Hartville Group

- 9.7 Hollard

- 9.8 IDEXX Laboratories

- 9.9 K9 Resorts

- 9.10 Mars

- 9.11 Petfirst Healthcare

- 9.12 PetIQ

- 9.13 PetSmart

- 9.14 Rover

- 9.15 The Barkley Pet Hotel & Day Spa

- 9.16 Vetcor

- 9.17 VIP Petcare