|

市場調査レポート

商品コード

1773465

獣医神経変性疾患診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Veterinary Neurodegenerative Disease Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 獣医神経変性疾患診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月26日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

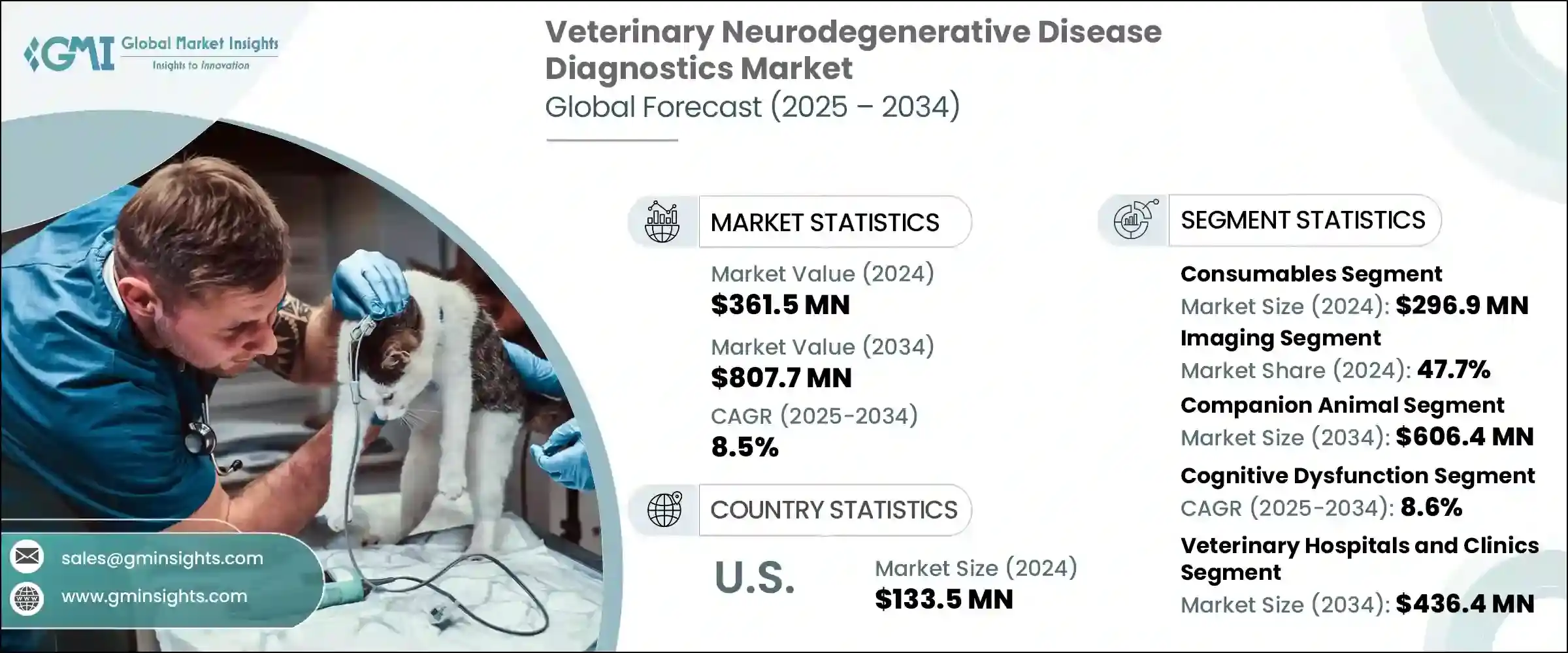

獣医神経変性疾患診断の世界市場は、2024年には3億6,150万米ドルとなり、CAGR 8.5%で成長し、2034年には8億770万米ドルに達すると予測されています。

2025年から2034年にかけてCAGR 8.5%で発生するこの成長は、いくつかの重要な要因によって牽引されています。動物の神経疾患の増加は、ペットの飼育や動物ヘルスケアへの支出の急増と相まって、正確で利用しやすい診断ツールの需要を押し上げています。コンパニオンアニマルも家畜動物も世界中で個体数が急増しており、高度な獣医学的診断の必要性がこれまで以上に高まっています。獣医神経学における技術の進歩もまた、診断アプローチの再構築において重要な役割を果たしています。画像診断、バイオマーカー検査、高感度診断キットの開発における革新は、疾病検出の精度を著しく向上させています。

アジア太平洋、ラテンアメリカ、アフリカの一部の新興国では、動物病院や移動診療ユニットの設立が顕著に増加しています。これらの施設にはCTやMRIといった最先端の神経学的診断ツールが装備されるようになってきており、診断精度と治療成績の向上に役立っています。動物の健康と疾病予防に焦点を当てた政府の支援政策も、官民の投資を後押ししています。動物用ヘルスケア分野の大手企業は、サービスネットワークを拡大し、リファレンスラボと戦略的パートナーシップを結ぶことで、十分なサービスを受けていない地域での診断の利用可能性を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 3億6,150万米ドル |

| 予測金額 | 8億770万米ドル |

| CAGR | 8.5% |

獣医神経変性疾患診断は、アッセイ、試薬、キット、その他のサポートコンポーネントを含む幅広い機器と消耗品で構成されています。これらは、動物の神経疾患の同定とモニタリングに役立つ診断ソリューションの開発と応用に使用されます。市場は製品タイプ別に消耗品と機器に区分され、2024年には消耗品カテゴリーが2億9,690万米ドルの評価額でリードしています。消耗品はあらゆる診断手順で使用されるため、常に補充が必要です。このような繰り返し使用により、安定した収益が確保され、これらの製品に対する需要が強化されています。使い捨てであること、獣医学的ワークフローへの統合が容易であること、標準化されたフォーマットであることは、利便性、一貫性、信頼性を提供します。

検査タイプ別では、市場は画像診断、バイオマーカー診断検査、その他の方法に分類されます。画像診断は2024年に47.7%と圧倒的な市場シェアを占めています。画像診断は、脊髄変性症や脳機能障害のような疾患に関連する構造的問題を視覚的に把握することで、神経学的異常を特定する上で重要な役割を果たしています。獣医学的環境におけるCTとMRI技術の統合が進むにつれ、これらの診断法の利用可能性と有効性が向上し、市場全体における画像診断の優位性に寄与しています。

動物の種類別に見ると、市場はコンパニオンアニマルと畜産動物に区分されます。コンパニオンアニマルセグメンテーションは2024年に市場をリードし、2034年には6億640万米ドルに達すると予測されています。このセグメントは、ペット飼育数の増加、動物の神経疾患に対する意識の高まり、ペット飼育者の専門診断への投資傾向の高まりから利益を得ています。加齢に伴う神経障害がペットで認識されるようになるにつれ、正確かつ早期発見の必要性が高まり、高度な診断ソリューションの利用がさらに促進されています。

適応症別に分析すると、認知機能障害分野は2034年までCAGR 8.6%を記録すると予想され、これは動物における加齢に関連した神経衰弱の発生が増加していることが背景にあります。この疾患は、特に高齢犬において、ペットの飼い主や獣医専門家の間で認知度が高まっています。現在進行中の研究と新しい診断テストの開発により、認知の問題をより迅速かつ正確に特定できるようになり、需要の増加に対応しています。

最終用途の観点から、市場は動物病院・診療所、診断研究所、その他のエンドユーザーに区分されます。動物病院・診療所は2024年に主要セグメントとして浮上し、2034年には4億3,640万米ドルに達すると予測されています。これらの機関は一般的に、高度な診断ツールと大量のサンプルを効率的に処理できる熟練した専門家を備え、十分な資源を有しています。正確でタイムリーな診断を提供する能力により、多くの飼い主にとって頼りになる存在となっています。画像診断システムや神経診断インフラへの投資は、この分野での優位性をさらに強固なものにしています。

地域別では、北米が2024年に40.6%のシェアで世界市場をリードしました。米国だけで、2024年の市場規模は1億3,350万米ドルに達し、前年からの増加傾向が続いています。この地域は、強力な獣医学的インフラ、高いペット飼育率、ペットの健康に関する意識の高まりなどの恩恵を受けています。高度な動物ヘルスケアサービスの存在やペット保険の普及も、この地域の成長を後押しする重要な要因です。さらに、都市部と農村部の両方で獣医施設のネットワークが拡大していることも、市場浸透の拡大に寄与しています。

市場情勢の競合情勢には、世界の大手企業と地域の専門企業が混在しています。IDEXX Laboratories、Merck Animal Health、Virbac、Zoetisなどの主要企業は合計で市場の約45%~50%を占めています。これらの企業の優位性は、幅広い製品ポートフォリオ、世界展開、技術革新への一貫した投資に起因しています。これらの企業は、買収、新製品開発、地理的拡大といった戦略的イニシアティブに注力し、その地位を強化しています。一方、地域や地方のプロバイダーは、手頃な価格の診断ソリューションを提供し、市場でのプレゼンスを拡大するために合併や提携などの成長戦略を採用することで競合を激化させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 動物における神経疾患の発生率の上昇

- 動物神経生物学の理解の向上

- 分子診断および画像診断における技術の進歩

- ペットの飼育数とペットヘルスケア費の増加

- ペット保険の適用範囲拡大

- 業界の潜在的リスク&課題

- 検証済みのバイオマーカーの入手が限られている

- 獣医神経科医と訓練を受けた専門家の不足

- 機会

- 獣医インフラの急速な開発

- 診断におけるAIとデジタルプラットフォームの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021~2034年

- 主要動向

- 消耗品

- 機器

第6章 市場推計・予測:検査の種類別、2021~2034年

- 主要動向

- 画像診断

- MRI(磁気共鳴画像)

- CT(コンピュータ断層撮影)

- その他の画像検査

- バイオマーカー診断検査

- 脳脊髄液(CSF)バイオマーカー

- 血液ベースのバイオマーカー

- その他のバイオマーカー診断検査

- その他の検査の種類

第7章 市場推計・予測:動物の種類別、2021~2034年

- 主要動向

- コンパニオンアニマル

- 犬

- 猫

- 馬

- その他のペット

- 家畜

- 牛

- 羊とヤギ

- その他の家畜

第8章 市場推計・予測:適応症別、2021~2034年

- 主要動向

- 認知機能障害

- 小脳アビオトロフィー

- 海綿状脳症

- その他の適応症

第9章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- 動物病院および診療所

- 診断検査室

- その他の用途

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Antech Diagnostics

- Avacta Animal Health Limited

- ACUVET BIOTECH

- Carestream Health

- IDEXX Laboratories

- Life Diagnostics

- Neurologica Corporation

- Merck Animal Health

- MI:RNA Diagnostics

- Mercodia AB

- Neogen Corporation

- Randox Laboratories

- Siemens Healthineers

- Virbac

- Zoetis

The Global Veterinary Neurodegenerative Disease Diagnostics Market was valued at USD 361.5 million in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 807.7 million by 2034. This growth, occurring at a CAGR of 8.5% from 2025 to 2034, is being driven by several key factors. The rise in neurological disorders among animals, coupled with a surge in pet ownership and spending on animal healthcare, is pushing demand for accurate and accessible diagnostic tools. With both companion and livestock animal populations increasing rapidly across the globe, the need for advanced veterinary diagnostics has become more pressing than ever. Technological advancements in veterinary neurology are also playing a crucial role in reshaping diagnostic approaches. Innovations in imaging, biomarker testing, and the development of highly sensitive diagnostic kits have significantly improved the precision of disease detection.

Emerging economies in Asia-Pacific, Latin America, and parts of Africa are witnessing a notable boost in the establishment of veterinary clinics and mobile care units. These facilities are increasingly equipped with cutting-edge neurological diagnostic tools such as CT and MRI, helping improve diagnostic accuracy and treatment outcomes. Supportive government policies focused on animal health and disease prevention are also encouraging public-private investments. Major corporations in the veterinary healthcare space are expanding their service networks and entering into strategic partnerships with reference laboratories, enhancing the availability of diagnostics in underserved regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $361.5 Million |

| Forecast Value | $807.7 Million |

| CAGR | 8.5% |

Veterinary neurodegenerative disease diagnostics comprise a wide array of instruments and consumables, including assays, reagents, kits, and other supporting components. These are used to develop and apply diagnostic solutions that help in the identification and monitoring of neurological conditions in animals. The market, segmented by product type into consumables and instruments, saw the consumables category leading with a valuation of USD 296.9 million in 2024. Consumables are used in every diagnostic procedure and thus need constant replenishment. This repetitive use ensures a steady revenue stream and strengthens the demand for these products. Their single-use nature, ease of integration into veterinary workflows, and standardized formats offer convenience, consistency, and reliability-key factors that contribute to their widespread adoption in clinics and labs.

On the basis of test type, the market is categorized into imaging, biomarker diagnostic tests, and other methods. Imaging held the dominant market share of 47.7% in 2024. It plays a vital role in identifying neurological abnormalities by providing visual insights into structural issues associated with diseases like spinal degeneration or brain dysfunction. The increasing integration of CT and MRI technologies in veterinary settings has improved the availability and effectiveness of these diagnostic methods, contributing to the dominance of imaging in the overall market.

By animal type, the market is segmented into companion animals and livestock animals. The companion animal segment led the market in 2024 and is projected to reach USD 606.4 million by 2034. This segment benefits from rising pet ownership, increasing awareness of animal neurological conditions, and the growing tendency among pet owners to invest in specialized diagnostics. As age-related neurological disorders become more recognized in pets, the need for precise and early detection continues to grow, prompting further use of advanced diagnostic solutions.

When analyzed by indication, cognitive dysfunction segment is expected to register a CAGR of 8.6% through 2034, driven by the rising occurrence of age-related neurological decline in animals. This condition, particularly in older dogs, is gaining greater awareness among pet owners and veterinary professionals alike. Ongoing research and the development of new diagnostic tests are enabling the identification of cognitive issues with improved speed and accuracy, helping to meet growing demand.

In terms of end use, the market is segmented into veterinary hospitals and clinics, diagnostic laboratories, and other end users. Veterinary hospitals and clinics emerged as the leading segment in 2024 and are anticipated to reach USD 436.4 million by 2034. These institutions are typically well-resourced, with advanced diagnostic tools and skilled professionals capable of processing a high volume of samples efficiently. Their ability to deliver accurate and timely diagnoses makes them the go-to choice for many pet owners. Investments in imaging systems and neurodiagnostic infrastructure further solidify their dominance in this space.

Geographically, North America led the global market with a share of 40.6% in 2024. The United States alone reached a market value of USD 133.5 million in 2024, continuing its upward trend from previous years. The region benefits from strong veterinary infrastructure, high rates of pet ownership, and growing awareness regarding pet health. The presence of advanced animal healthcare services and increasing adoption of pet insurance policies are also important factors fueling regional growth. Additionally, the expanding network of veterinary facilities in both urban and rural areas contributes to broader market penetration.

The competitive landscape in the veterinary neurodegenerative disease diagnostics market features a mix of global giants and regional specialists. Leading companies such as IDEXX Laboratories, Merck Animal Health, Virbac, and Zoetis collectively hold approximately 45%-50% of the market. Their dominance is attributed to broad product portfolios, global reach, and consistent investment in technological innovation. These players are focusing on strategic initiatives like acquisitions, new product development, and geographic expansion to strengthen their positions. Meanwhile, regional and local providers are intensifying competition by offering affordable diagnostic solutions and adopting growth strategies such as mergers and collaborations to expand their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Test type

- 2.2.4 Animal type

- 2.2.5 Indication

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of neurological disorders in animals

- 3.2.1.2 Improved understanding of animal neurobiology

- 3.2.1.3 Technological advancements in molecular and imaging diagnostics

- 3.2.1.4 Growing pet ownership and pet healthcare spending

- 3.2.1.5 Expansion of companion animal insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of validated biomarkers

- 3.2.2.2 Shortage of veterinary neurologists and trained professionals

- 3.2.3 Opportunities

- 3.2.3.1 Rapid veterinary infrastructure development

- 3.2.3.2 Integration of AI and digital platforms in diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Imaging

- 6.2.1 MRI (magnetic resonance imaging)

- 6.2.2 CT (computed tomography)

- 6.2.3 Other imaging tests

- 6.3 Biomarker diagnostic tests

- 6.3.1 CSF (cerebrospinal fluid) biomarkers

- 6.3.2 Blood-based biomarkers

- 6.3.3 Other biomarker diagnostic tests

- 6.4 Other test types

Chapter 7 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Sheep and goats

- 7.3.3 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Cognitive dysfunction

- 8.3 Cerebellar abiotrophy

- 8.4 Spongiform encephalopathies

- 8.5 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Diagnostic laboratories

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Antech Diagnostics

- 11.2 Avacta Animal Health Limited

- 11.3 ACUVET BIOTECH

- 11.4 Carestream Health

- 11.5 IDEXX Laboratories

- 11.6 Life Diagnostics

- 11.7 Neurologica Corporation

- 11.8 Merck Animal Health

- 11.9 MI:RNA Diagnostics

- 11.10 Mercodia AB

- 11.11 Neogen Corporation

- 11.12 Randox Laboratories

- 11.13 Siemens Healthineers

- 11.14 Virbac

- 11.15 Zoetis