持続可能なペット用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Sustainable Pet Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773464

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

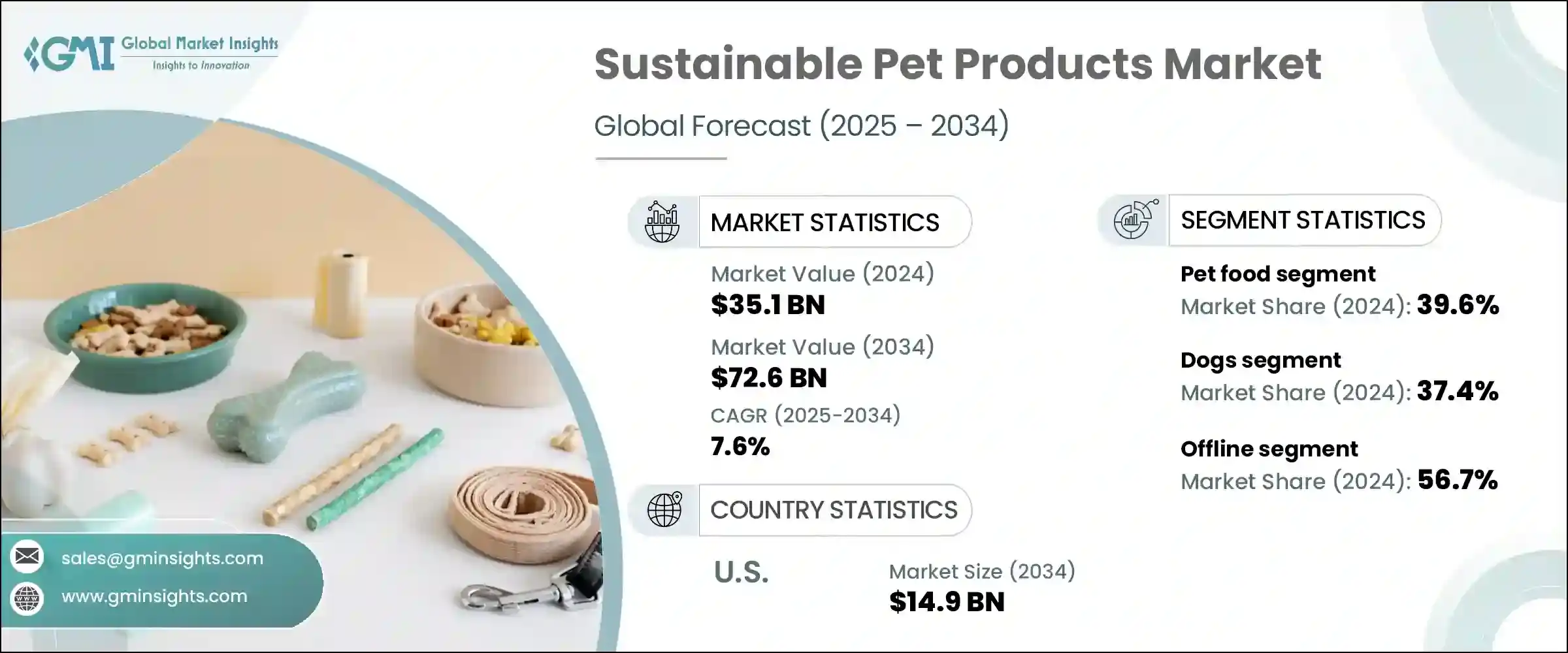

世界の持続可能なペット用品市場は、2024年に351億米ドルと評価され、CAGR 7.6%で成長し、2034年には726億米ドルに達すると推定されています。

この市場拡大の背景には、ペットを家族の一員として扱い、倫理的に生産された高級品への投資を増やす、環境意識の高い飼い主が増えていることがあります。生分解性排泄物袋、プラスチック製でないグルーミング用品、責任を持って調達されたペットフード、リサイクル可能な包装への需要は、環境に優しいペットケアへの幅広いシフトを反映しています。可処分所得の増加は、健康を重視したペット用品への支出を促進し、新興ブランドと既存ブランドの両方が、これらの進化する期待に応えるために、素材、処方、包装の革新を行っています。

この持続可能なペットケアの急増は、健康動向、環境問題、ライフスタイルの変化を核に、業界を再構築しています。消費者は今、自分の価値観とペットのために選ぶ製品を一致させ、健康、倫理的な調達、環境への影響の最小化を優先しています。ペットの飼い主の環境意識が高まるにつれて、従来の製品から、生分解性、無農薬、リサイクル素材から作られた代替品への買い替えが積極的に行われています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 351億米ドル |

| 予測金額 | 726億米ドル |

| CAGR | 7.6% |

さらに、植物ベースの食事、クリーンラベル処方、毒素フリーのグルーミング・ソリューションの人気の高まりは、ホリスティックで意識的な生活への幅広い文化的シフトを反映しています。この変化は単なる一過性のトレンドではなく、ペットケアの購買決定において持続可能性が標準的な期待となり、製品開発、パッケージデザイン、マーケティング戦略に影響を与える長期的な動きを示唆しています。

2024年には、持続可能なペットフード分野は39.6%のシェアを占め、CAGR 8%で成長すると予想されます。ペットの飼い主は、ペットの全体的な健康と幸福をサポートするために、オーガニックで、責任を持って調達された、栄養価の高いフードを選ぶようになってきています。従来の肉食による環境フットプリントへの懸念から、昆虫ベース、植物ベース、ラボ栽培などの代替タンパク質への関心が高まっています。消費者は、透明性のある調達、クリーンな表示、環境に優しい包装を実践しているブランドを高く評価しています。

2024年のペット用品のシェアは犬用が37.4%を占め、2034年までのCAGRは8.2%と予測されます。飼い主と犬との間に強い感情的な結びつきがあることから、生分解性の排泄物袋、植物由来の食品、リサイクル素材や環境に優しい繊維で作られたアクセサリーなど、持続可能な製品への支出が増加しています。この需要は、ペットのヒューマニゼーションというトレンドの高まりと直接結びついています。

米国持続可能なペット用品市場は60.2%のシェアを占め、2034年には149億米ドルに達すると予測されています。ペットの飼育率の高さと、堅調な小売・eコマースチャネルに支えられた環境配慮型製品に対する消費者の関心が、この成長を後押ししています。米国企業は、植物由来のペットフード、生分解性排泄物袋、持続可能なパッケージ商品などを提供し、ペットの親の進化するニーズに応えています。

この分野の大手企業には、West Paw、Pawz、Beco Pets、Kurgo、Ruffwear、Spectrum Brands、Colgate Palmolive、Jiminy's、Petcurean、Freshpet、Petco、Green Pet Shop、RC Pet Products、Purina、Hurttaなどがあります。持続可能なペット用品分野のトップブランドは、消費者のロイヤリティを獲得するために、環境に優しい革新とサプライチェーンの透明性に多額の投資を行っています。植物由来の原料、生分解性素材、リサイクル可能なパッケージなど、ポートフォリオを拡大しています。持続可能な素材サプライヤーや環境認証機関とのパートナーシップは、製品の信頼性を確実なものにしています。多くの企業は、オムニチャネル流通戦略(小売と強力なeコマースを組み合わせた流通戦略)を活用し、より多くの消費者にリーチしています。ソーシャルメディア、インフルエンサーとのコラボレーション、コミュニティとのエンゲージメントを通じたストーリーテリングは、ブランド価値を強調するのに役立ちます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- ペットの人間化のトレンドが増加

- ペットケアへの消費者支出の増加

- 倫理的な慣行に対する消費者の需要

- 循環型経済における経済的機会

- 業界の潜在的リスク&課題

- ペット用品需要の季節性

- 発展途上地域および後発開発地域における意識の欠如と支出の低さ

- ペットケア費用が高め

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制の枠組み

- 規格と認証

- 環境規制

- 輸出入規制

- 貿易統計(HSコード:33051090)

- 主要輸入国

- 主要輸出国

- ポーターのファイブフォース分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- ペットフード

- ペットアクセサリー

- ペットケア製品

- ペットのアパレルと寝具

第6章 市場推計・予測:ペットの種類別、2021-2034

- 主要動向

- 犬

- 猫

- 鳥

- 小動物(ウサギ、ハムスターなど)

- 魚類と爬虫類

- その他(例:エキゾチックペット)

第7章 市場推計・予測:価格別、2021-2034

- 主要動向

- 低

- 中

- 高

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- オンライン小売

- Eコマースプラットフォーム(Amazon、Chewyなど)

- ブランド所有のウェブサイト

- オフライン小売

- ペット専門店

- スーパーマーケットとハイパーマーケット

- 獣医クリニック

- エコ/オーガニックストア

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Beco Pets

- Colgate-Palmolive

- Freshpet

- Green Pet Shop

- Hurtta

- Jiminy's

- Kurgo

- Pawz

- Petco

- Petcurean

- Purina

- RC Pet Products

- Ruffwear

- Spectrum Brands

- West Paw

目次

The Global Sustainable Pet Products Market was valued at USD 35.1 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 72.6 billion by 2034. This expansion is driven by increasingly eco-conscious pet owners who treat their pets as family members and are investing more in premium, ethically produced goods. Demand for biodegradable waste bags, non-plastic grooming items, responsibly sourced pet food, and recyclable packaging reflects a broader shift toward environmentally friendly pet care. Rising disposable incomes are fueling spending on health-focused pet products, and both emerging and established brands are innovating in materials, formulations, and packaging to meet these evolving expectations.

This surge in sustainable pet care is reshaping the industry, with health trends, environmental concerns, and lifestyle changes at its core. Consumers are now aligning their values with the products they choose for their pets, prioritizing wellness, ethical sourcing, and minimal environmental impact. As pet owners become more eco-aware, they are actively replacing conventional products with alternatives made from biodegradable, cruelty-free, or recycled materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.1 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 7.6% |

Additionally, the rising popularity of plant-based diets, clean-label formulations, and toxin-free grooming solutions reflects a broader cultural shift toward holistic, conscious living. This transformation is not just a passing trend-it signals a long-term movement where sustainability becomes a standard expectation in pet care purchasing decisions, influencing product development, packaging design, and marketing strategies across the sector.

In 2024, the sustainable pet food segment held a 39.6% share and is expected to grow at an 8% CAGR. Pet owners are increasingly choosing organic, responsibly sourced, and nutritionally dense food options to support their pets' overall health and well-being. Concerns over the environmental footprint of traditional meat-based diets are boosting interest in alternative proteins like insect-based, plant-based, or lab-grown options. Consumers value brands that practice transparent sourcing, clean labeling, and eco-friendly packaging.

The dog segment dominated pet categories in 2024, capturing 37.4% share, and is forecasted to grow at 8.2% CAGR through 2034. The strong emotional bond between owners and dogs is driving increased spending on sustainable products, including biodegradable waste bags, plant-based foods, and accessories made from recycled materials or eco-friendly textiles. This demand is directly tied to the rising trend of pet humanization.

U.S. Sustainable Pet Products Market held a 60.2% share and is projected to reach USD 14.9 billion by 2034. High pet ownership rates and consumer interest in eco-conscious products-supported by robust retail and e-commerce channels-are propelling this growth. U.S. companies offer plant-based pet foods, biodegradable waste bags, and sustainably packaged goods to meet pet parents' evolving needs.

Leading players in this space include West Paw, Pawz, Beco Pets, Kurgo, Ruffwear, Spectrum Brands, Colgate Palmolive, Jiminy's, Petcurean, Freshpet, Petco, Green Pet Shop, RC Pet Products, Purina, and Hurtta. Top brands in the sustainable pet products arena are investing heavily in eco-friendly innovation and supply chain transparency to capture consumer loyalty. They are expanding their portfolios to include plant-based ingredients, biodegradable materials, and recyclable packaging. Partnerships with sustainable material suppliers and environmental certification bodies ensure product credibility. Many companies are leveraging omnichannel distribution strategies-combining retail presence with strong e-commerce-to reach a wider audience. Storytelling through social media, influencer collaborations, and community engagement helps highlight brand values.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Pet type

- 2.2.3 Price

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing trend of pet humanization

- 3.2.1.2 Higher consumer spending on pet care

- 3.2.1.3 Consumer demand for ethical practices

- 3.2.1.4 Economic opportunities in the circular economy

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Seasonality in pet products demand

- 3.2.2.2 Lack of awareness & low spending in developing and under-developed regions

- 3.2.2.3 High pet care cost

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code: 33051090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Pet food

- 5.3 Pet accessories

- 5.4 Pet care products

- 5.5 Pet apparel and bedding

Chapter 6 Market Estimates & Forecast, By Pet Type, 2021-2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Small animals (e.g., rabbits, hamsters)

- 6.6 Fish & reptiles

- 6.7 Others (e.g., exotic pets)

Chapter 7 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Online retail

- 8.2.1 E-commerce platforms (Amazon, Chewy, etc.)

- 8.2.2 Brand-owned websites

- 8.3 Offline retail

- 8.3.1 Pet specialty stores

- 8.3.2 Supermarkets and hypermarkets

- 8.3.3 Veterinary clinics

- 8.3.4 Eco/organic stores

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beco Pets

- 10.2 Colgate-Palmolive

- 10.3 Freshpet

- 10.4 Green Pet Shop

- 10.5 Hurtta

- 10.6 Jiminy's

- 10.7 Kurgo

- 10.8 Pawz

- 10.9 Petco

- 10.10 Petcurean

- 10.11 Purina

- 10.12 RC Pet Products

- 10.13 Ruffwear

- 10.14 Spectrum Brands

- 10.15 West Paw

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日