スピンオンカーボンの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Spin on Carbon Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773461

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

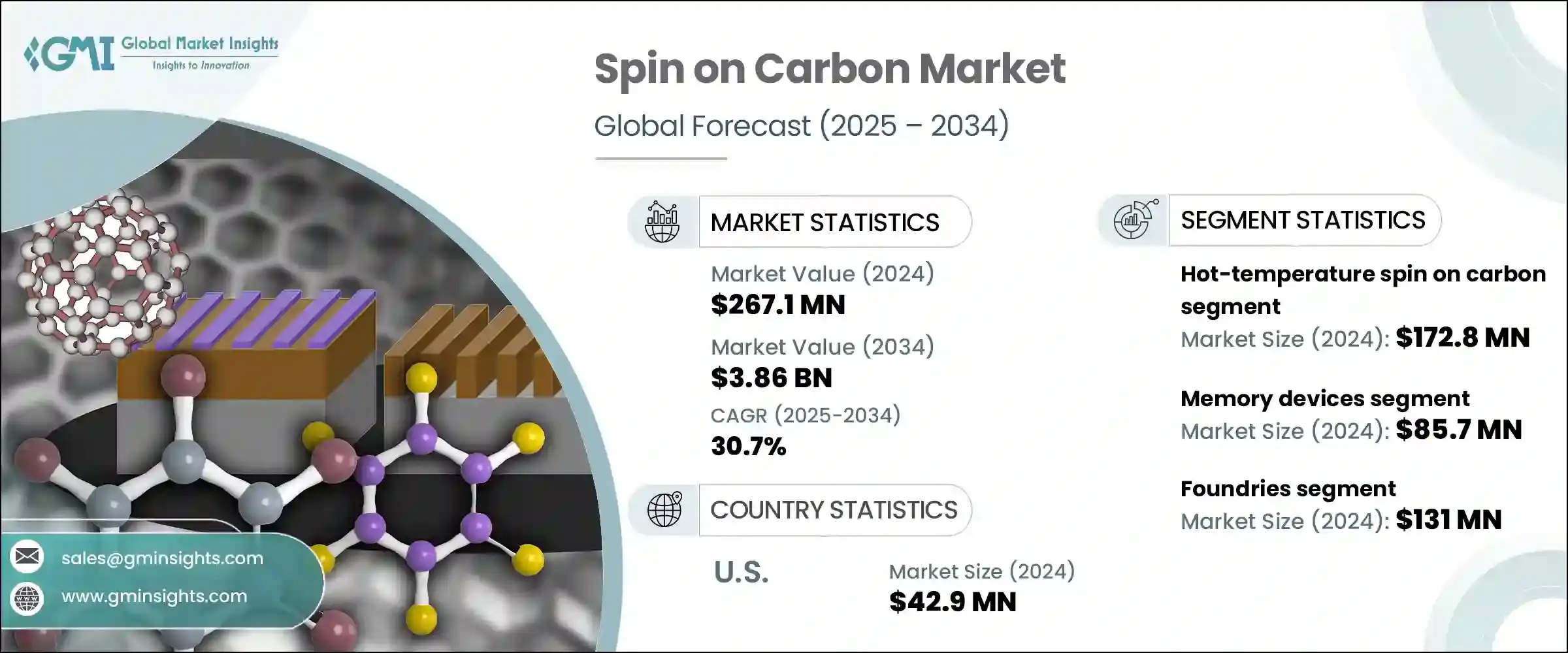

スピンオンカーボンの世界市場規模は、2024年に2億6,710万米ドルとなり、CAGR 30.7%で成長し、2034年には38億6,000万米ドルに達すると予測されています。

この急拡大は、主に鋳造への投資拡大と極端紫外線(EUV)リソグラフィの採用増加によるものです。人工知能、高性能コンピューティング、5Gなどの産業が台頭し続ける中、大手鋳造企業は製造能力を拡大しており、スピンオンカーボンのような材料の需要が高まっています。

SoCは半導体製造、特に先進的なチップ設計において重要な役割を果たし、エッチング耐性を提供し、均一な膜コーティングを可能にします。このようなチップ設計の進化と半導体製造の増加は、市場におけるスピンオンカーボンの需要を促進しています。さらに、半導体製造におけるEUVリソグラフィへのシフトは、超微細形状を形成する能力で知られており、市場の成長をさらに後押ししています。EUVの採用は、より小型で高性能な半導体デバイスの開発に不可欠であり、SoC材料は、正確なパターン転写を可能にし、7nm以下のノードでのエッチング精度を高める上で不可欠であるため、市場の成長に大きく寄与しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2億6,710万米ドル |

| 予測金額 | 38億6,000万米ドル |

| CAGR | 30.7% |

2024年には、高温スピンオンカーボンセグメントが1億7,280万米ドルで最大の市場シェアを占めました。半導体用途、特に高速プロセッサーやメモリーチップでは、より優れた熱安定性と低誘電率が求められるため、高温SoCが勢いを増しています。これらの材料は先進パッケージング技術や3D集積回路に最適であり、劣化することなく高いプロセス温度に耐える材料を必要とします。半導体デバイスの小型化が進んでいることも、特に銅配線技術における高温SoCの需要を後押ししています。

メモリ・デバイス・セグメントは、2024年には8,570万米ドルと評価され、低誘電率絶縁膜と相互接続の製造に不可欠な役割に牽引されています。これらの材料は、クラウドコンピューティング、AI、5Gなど、性能と効率が最重要となる最先端アプリケーションで高速データ転送をサポートするために不可欠です。メモリアーキテクチャの微細化が進み、積層メモリ技術が進化するにつれて、ますます厳しくなる要求を満たすための材料への圧力は高まっています。デバイスがより小さなノードと高密度構成に向かうにつれて、SoC材料の必要性はさらに重要になります。

米国スピンオンカーボン産業は2024年に4,290万米ドルを生み出しました。同国は航空宇宙技術革新におけるリーダー的存在であり、防衛や航空機用途の軽量・高強度部品に使用されるスピンオンカーボンのような先端材料の需要を牽引しています。さらに、風力や太陽光などの再生可能エネルギー源へのシフトが、エネルギー貯蔵システムにおける耐久性が高く軽量な炭素系材料の必要性を高めています。自動車の電動化に向けた動向は、軽量バッテリー部品や熱管理システムにおけるスピンオンカーボンの需要をさらに高めており、米国がこの市場で圧倒的な強さを維持しています。

スピンオンカーボン業界の主要企業には、Brewer Science, Inc.、デュポン、DONGJIN SEMICHEM CO LTD、Applied Materials, Inc.、Merck KGaA、JSR Micro, Inc.、Irresistible Materials、信越化学工業、Nano-C、KOYJ Co.Ltd.、YCCHEM CO.Ltd.、Samsung SDI Co.Ltd.などがあります。市場ポジションを強化するため、スピンオンカーボン業界の各社は技術の進歩と材料の革新に注力しています。

特にサブ7nmのような超先端ノードでの半導体製造プロセスにおけるスピンオンカーボンの性能を向上させるため、研究開発に多額の投資を行っています。また、最新の製造技術との互換性を確保するためには、鋳造メーカーや半導体メーカーとの戦略的パートナーシップも不可欠です。さらに、再生可能エネルギーや航空宇宙など、多様な産業における需要の高まりに対応するため、各社は製品ラインナップを拡充しています。生産プロセスを合理化し、高品質基準を維持しながらコストを削減する努力は、この急速に拡大する市場での競争力強化の中心となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 半導体業界におけるノードサイズの縮小

- EUVリソグラフィーの採用増加

- 増加するファウンドリ投資

- エッチング耐性と膜均一性の向上

- 先進パッケージングにおける利用の増加

- 業界の潜在的リスク&課題

- 高い材料費と加工費

- 環境と廃棄物管理に関する懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:材質別、2021 –2034

- 主要動向

- 高温スピンオンカーボン

- 常温スピンオンカーボン

第6章 市場推計・予測:用途別、2021 –2034

- 主要動向

- ロジックデバイス

- メモリデバイス

- 電源装置

- 微小電気機械システム

- フォトニクス

- 先進パッケージング

- その他

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 鋳造

- 統合デバイスメーカー

- 半導体組立・テストのアウトソーシング

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Applied Materials, Inc.

- Brewer Science, Inc.

- DONGJIN SEMICHEM CO LTD

- DuPont

- Irresistible Materials

- JSR Micro, Inc.

- KOYJ Co., Ltd.

- Merck KGaA

- Nano-C

- Samsung SDI Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- YCCHEM CO.,Ltd.

目次

The Global Spin on Carbon Market was valued at USD 267.1 million in 2024 and is estimated to grow at a CAGR of 30.7% to reach USD 3.86 billion by 2034. This rapid expansion is primarily driven by the growing investments in foundries and the increasing adoption of extreme ultraviolet (EUV) lithography. As industries such as artificial intelligence, high-performance computing, and 5G continue to rise, leading foundries are scaling up their manufacturing capabilities, which increases the demand for materials like spin-on carbon.

SoC serves as a crucial component in semiconductor production, especially in advanced chip designs, providing etch resistance and enabling uniform film coating. This evolution in chip design, paired with rising semiconductor manufacturing, propels the demand for spin-on carbon in the market. Additionally, the shift toward EUV lithography in semiconductor fabrication, known for its ability to create ultra-fine features, further fuels the market growth. The adoption of EUV is critical to developing smaller, more powerful semiconductor devices, and SoC materials are essential in enabling accurate pattern transfer and enhancing etching precision in sub-7nm nodes, thus contributing significantly to the market's growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $267.1 Million |

| Forecast Value | $3.86 Billion |

| CAGR | 30.7% |

In 2024, the hot-temperature spin-on carbon segment accounted for the largest market share, valued at USD 172.8 million. As semiconductor applications, particularly high-speed processors and memory chips, demand better thermal stability and low dielectric constant, hot-temperature SoCs have gained momentum. These materials are ideal for advanced packaging technologies and 3D integrated circuits, which require materials capable of enduring high process temperatures without degradation. The increasing miniaturization of semiconductor devices also drives the demand for hot-temperature SoCs, especially in copper interconnect technologies.

The memory device segment was valued at USD 85.7 million in 2024, driven by their essential role in the fabrication of low-k dielectrics and interconnects. These materials are crucial for supporting high-speed data transfer in cutting-edge applications such as cloud computing, AI, and 5G, where performance and efficiency are paramount. As memory architecture continues to shrink and stacked memory technologies evolve, the pressure on materials to meet increasingly stringent demands has grown. The need for SoC materials becomes even more critical as devices move towards smaller nodes and higher-density configurations.

U.S. Spin on Carbon Industry generated USD 42.9 million in 2024. The country's leadership in aerospace innovation drives the demand for advanced materials like spin-on carbon, used in lightweight, high-strength components for defense and aircraft applications. Additionally, the shift toward renewable energy sources, such as wind and solar, is boosting the need for durable and lightweight carbon-based materials in energy storage systems. The growing trend toward vehicle electrification is further fueling demand for spin-on carbon in lightweight battery components and thermal management systems, ensuring the U.S. remains a dominant force in the market.

Key players in the Spin on Carbon Industry include Brewer Science, Inc., DuPont, DONGJIN SEMICHEM CO LTD, Applied Materials, Inc., Merck KGaA, JSR Micro, Inc., Irresistible Materials, Shin-Etsu Chemical Co., Ltd., Nano-C, KOYJ Co., Ltd., YCCHEM CO., Ltd., Samsung SDI Co., Ltd. To strengthen their market position, companies in the spin-on carbon industry are focusing on technological advancements and material innovations.

They are investing heavily in research and development to improve the performance of spin-on carbon in semiconductor manufacturing processes, particularly in ultra-advanced nodes like sub-7nm. Strategic partnerships with foundries and semiconductor manufacturers are also critical to ensure compatibility with the latest fabrication technologies. Additionally, companies are expanding their product offerings to meet the growing demand across diverse industries, including renewable energy and aerospace. Efforts to streamline production processes and reduce costs while maintaining high-quality standards are central to enhancing competitiveness in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shrinking node sizes in semiconductor industry

- 3.2.1.2 Increased adoption of EUV lithography

- 3.2.1.3 Growing foundry investments

- 3.2.1.4 Enhanced etch resistance and film uniformity

- 3.2.1.5 Rising use in advanced packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material and processing costs

- 3.2.2.2 Environmental and waste management concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ Startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hot-temperature spin on carbon

- 5.3 Normal-temperature spin on carbon

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Logic devices

- 6.3 Memory devices

- 6.4 Power devices

- 6.5 Micro-electromechanical systems

- 6.6 Photonics

- 6.7 Advanced packaging

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Foundries

- 7.3 Integrated device manufacturers

- 7.4 Outsourced semiconductor assembly & test

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Applied Materials, Inc.

- 9.2 Brewer Science, Inc.

- 9.3 DONGJIN SEMICHEM CO LTD

- 9.4 DuPont

- 9.5 Irresistible Materials

- 9.6 JSR Micro, Inc.

- 9.7 KOYJ Co., Ltd.

- 9.8 Merck KGaA

- 9.9 Nano-C

- 9.10 Samsung SDI Co., Ltd.

- 9.11 Shin-Etsu Chemical Co., Ltd.

- 9.12 YCCHEM CO.,Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日