照射装置の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Irradiation Apparatus Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773456

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

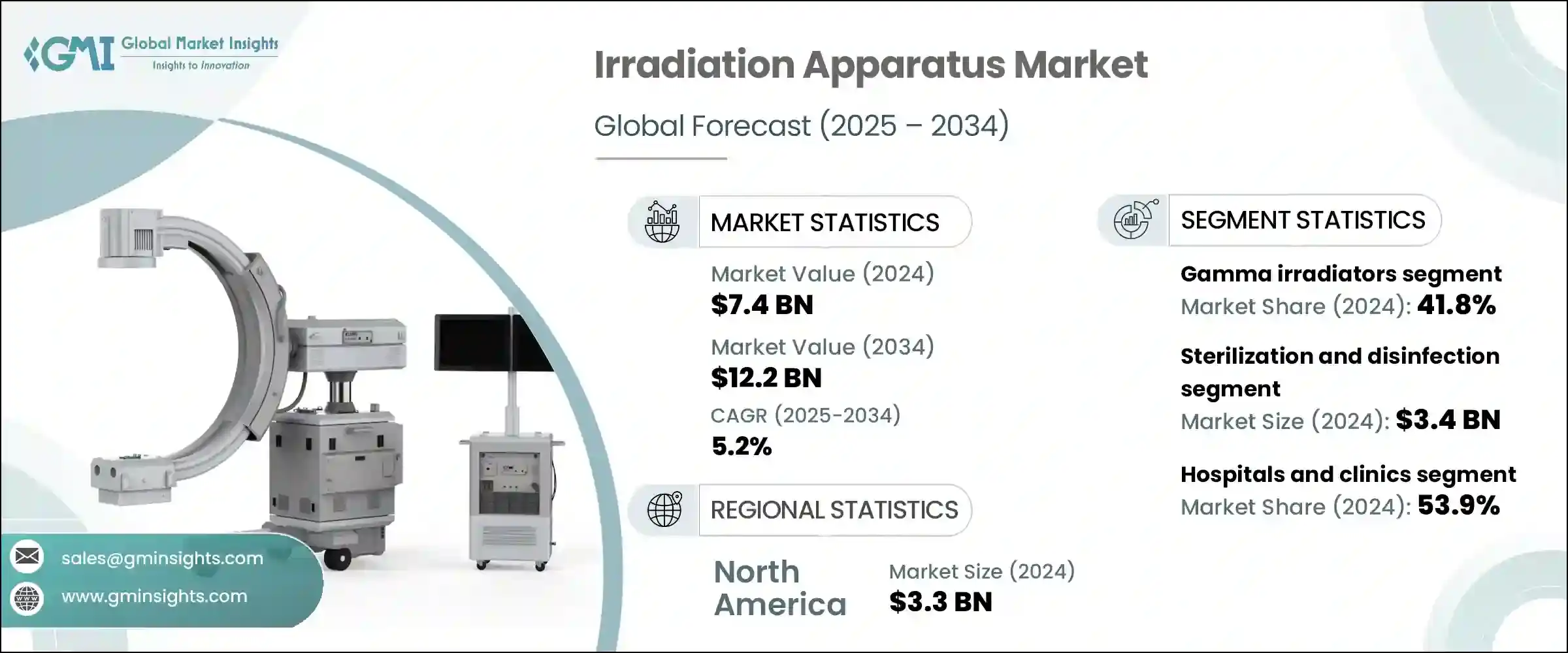

照射装置の世界市場は、2024年には74億米ドルと評価され、CAGR 5.2%で成長し、2034年には122億米ドルに達すると推定されています。

この成長を牽引しているのは、医療用と産業用の両方で電離放射線と非電離放射線の利用が増加していることです。これらのシステムは主に診断、治療、滅菌、研究目的で導入されています。

がん治療における放射線治療の採用が増加していることは、市場成長を促進する重要な要因です。早期発見と即時介入への強い後押しが、ブラキセラピー装置やリニアックなどの装置への投資を増加させています。腫瘍クリニックや専門医療センターが世界的に拡大する中、先進的な照射システムの導入は増加の一途をたどっており、効率的で利用しやすいがん治療技術への需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 74億米ドル |

| 予測金額 | 122億米ドル |

| CAGR | 5.2% |

画像誘導放射線治療とAI対応システムにおける最新の技術革新が、照射装置の展望を再構築しています。ロボット制御やリアルタイム画像処理と統合されたこれらのプラットフォームは、周辺組織を保護しながら腫瘍に正確な線量を照射します。リニアックや画像誘導放射線治療などの技術は、現在、より高い精度と合併症リスクの低減を実現し、ヘルスケア施設に広く採用されています。

治療成績の向上、回復時間の短縮、副作用の最小化が、病院や診療所の次世代システムへの移行を促しています。新興地域では、官民双方からの投資拡大がヘルスケア・インフラのアップグレードを支え、治療へのアクセス格差の解消に貢献しています。治療と滅菌の両分野で放射線ベースのソリューションへの需要が高まる中、世界市場はヘルスケア改革と技術主導の改善によって活性化しています。

2024年には、ガンマ線照射器セグメントが41.8%で最大の市場シェアを占めています。使い捨て医療製品の消費拡大がガンマ線ベースの滅菌システムの大きな原動力となっています。ガンマ線は熱に弱く、化学的にデリケートな品目を効果的に滅菌することができるため、注射器、カテーテル、手術用手袋の滅菌にこの方式を採用するメーカーが増えています。

ガンマ線を使用した滅菌処理は有害な残留物を残さないため、規制された医療環境において信頼性の高いソリューションを提供します。これらのシステムは、輸血後の有害反応を防ぐための血液成分の処理にも不可欠です。感染制御と無菌性保証が世界の規制機関によって重視されるようになる中、ガンマ線照射装置は重要なヘルスケア機器と消耗品の製造と処理において好ましいソリューションであり続けています。

2024年の市場シェアは病院・診療所が53.9%でトップでした。これらの施設は照射装置の主要ユーザーであり、画像診断や治療介入に幅広く活用しています。X線装置、CTシステム、透視装置などの機器は、患者の状態を非侵襲的に評価する上で極めて重要な役割を果たしています。

さらに、ヘルスケア関連感染と闘うために、病院は侵襲的医療器具の照射ベースの滅菌に目を向けており、患者の安全性と衛生規制の遵守の両方を確保しています。熱や化学薬品による滅菌に比べ、照射は手術器具やその他の再使用可能な部品の滅菌に、より迅速で信頼性の高い方法を提供します。診断精度と感染予防の組み合わせにより、照射装置は現代のヘルスケア施設に欠かせないものとなっています。

米国の照射装置市場は2024年に30億米ドルと評価され、2034年には49億米ドルに達すると予測されています。慢性疾患、特にがんの蔓延が、先進的な放射線治療ソリューションの需要を全国的に押し上げています。同時に、外来手術センターや外来診療所のような分散型の治療環境を重視する米国ヘルスケア業界では、コンパクトで効率的な滅菌システムのニーズが加速しています。

このような小規模施設では、ハイスループットで省スペースなソリューションが求められており、モジュール式照射システムは、そのスピード、信頼性、機器の完全性を維持する能力により、非常に魅力的なものとなっています。このような費用対効果の高い分散型ヘルスケアモデルへのシフトにより、照射技術は都市部と農村部の両方で力強い成長を維持すると予想されます。

照射装置領域の大手企業は、先進的な画像誘導システムやAI統合型放射線システムを通じて、製品ポートフォリオの拡充に注力しています。多くの企業は、治療の精度を高め、ワークフローを自動化し、安全性を高めるために研究開発に多額の投資を行っています。がん治療センターやヘルスケア機関とのコラボレーションは、進化する臨床ニーズにマッチしたソリューションのカスタマイズに役立っています。世界の需要、特に十分なサービスを受けていない地域の需要に対応するため、企業は設置の複雑さを軽減するモジュール式で費用対効果の高いシステムを開発しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- がんや慢性疾患の発生率の上昇

- 画像診断装置および放射線治療装置の技術的進歩

- ヘルスケアインフラへの投資の増加

- 血液の安全性に対する意識の高まり

- 業界の潜在的リスク&課題

- 高額な資本投資と維持費

- 厳格な規制承認とコンプライアンス要件

- 市場機会

- 画像システムにおけるAIと自動化の導入

- 非化学殺菌の需要の加速

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- ポーター分析

- PESTEL分析

- 消費者行動分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ガンマ線照射装置

- X線照射装置

- 紫外線(UV)および中性子照射装置

- 電子線照射装置

- その他のタイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 診断画像

- 治療/放射線療法

- 滅菌と消毒

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 研究ラボおよび機関

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Accuray

- Canon Medical Systems

- Elekta

- GE HealthCare

- Hitachi

- Koninklijke Philips

- Mevion Medical Systems

- Mindray

- Neusoft Medical Systems

- Panacea Medical Technologies

- Shinva Medical

- Siemens Healthineers

- Sumitomo Heavy Industries

- ViewRay

目次

The Global Irradiation Apparatus Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.2 billion by 2034. This growth is driven by the increasing utilization of ionizing and non-ionizing radiation across both medical and industrial applications. These systems are primarily deployed for diagnostics, therapeutic use, sterilization, and research purposes.

The rising adoption of radiotherapy in cancer care is a significant factor propelling the market growth, as precision-targeted irradiation systems improve both outcomes and patient experiences. A strong push toward early detection and immediate intervention is increasing investments in devices such as brachytherapy equipment and linear accelerators. With oncology clinics and specialized medical centers expanding globally, the adoption of advanced irradiation systems continues to rise, underscoring the demand for efficient and accessible cancer treatment technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.2% |

Modern innovations in image-guided radiation therapy and AI-enabled systems are reshaping the landscape of irradiation apparatus. Integrated with robotic control and real-time imaging, these platforms provide accurate dose delivery to tumors while safeguarding surrounding tissues. Technologies such as linear accelerators and image-guided radiotherapy are now delivering higher levels of precision and lower complication risks, leading to widespread adoption across healthcare facilities.

Enhanced therapeutic outcomes, reduced recovery times, and minimized side effects are encouraging hospitals and clinics to transition to next-generation systems. In emerging regions, increased investments from both public and private sectors are supporting healthcare infrastructure upgrades, helping close treatment accessibility gaps. As demand grows for radiation-based solutions in both treatment and sterilization, the global market is being fueled by healthcare reforms and technology-driven improvements.

In 2024, the gamma irradiator segment accounted for the largest market share at 41.8%. The growing consumption of disposable medical products has been a major driver for gamma-based sterilization systems. As gamma radiation enables effective sterilization of heat-sensitive and chemically delicate items, manufacturers are increasingly relying on this method for syringes, catheters, and surgical gloves.

Sterilization processes using gamma rays leave no harmful residue, offering a reliable solution in regulated medical environments. These systems are also essential in treating blood components to prevent adverse post-transfusion reactions. With infection control and sterility assurance gaining focus across global regulatory bodies, gamma irradiators continue to be a preferred solution in the manufacture and processing of critical healthcare equipment and supplies.

The hospitals and clinics segment led the market in 2024 with a share of 53.9%. These facilities are primary users of irradiation apparatus, utilizing them extensively for diagnostic imaging and therapeutic interventions. Equipment like X-ray units, CT systems, and fluoroscopy machines play a pivotal role in evaluating patient conditions non-invasively.

Moreover, to combat healthcare-associated infections, hospitals are turning to irradiation-based sterilization for invasive medical tools, ensuring both patient safety and compliance with hygiene regulations. Compared to heat or chemical alternatives, irradiation offers a faster and more dependable method for sterilizing surgical instruments and other reusable components. The combination of diagnostic accuracy and infection prevention is making irradiation apparatus indispensable across modern healthcare facilities.

U.S. Irradiation Apparatus Market was valued at USD 3 billion in 2024 and is estimated to reach USD 4.9 billion by 2034. A growing prevalence of chronic illnesses-particularly cancer-is pushing demand for advanced radiation therapy solutions across the country. In tandem, the U.S. healthcare industry's emphasis on decentralized treatment settings like ambulatory surgical centers and outpatient clinics is accelerating the need for compact, efficient sterilization systems.

As these smaller facilities look for high-throughput and space-saving solutions, modular irradiation systems have become highly attractive due to their speed, reliability, and ability to preserve equipment integrity. This shift toward cost-effective and distributed healthcare models is expected to sustain robust growth for irradiation technologies across both urban and rural settings.

Key industry participants shaping the competitive landscape of the Irradiation Apparatus Market include GE HealthCare, Elekta, Siemens Healthineers, Mindray, Canon Medical Systems, NPB Ion Beam Technology, Neusoft Medical Systems, Accuray, ViewRay, Hitachi, Sumitomo Heavy Industries, Shinva Medical, Koninklijke Philips, Mevion Medical Systems, and Panacea Medical Technologies. These companies continue to set benchmarks through product innovation and strategic expansion.

Leading players in the irradiation apparatus space are focusing on product portfolio expansion through advanced imaging-guided and AI-integrated radiation systems. Many companies are heavily investing in R&D to boost treatment accuracy, automate workflows, and enhance safety. Collaborations with cancer treatment centers and healthcare institutions are helping tailor solutions that match evolving clinical needs. To address global demand, especially in underserved regions, firms are developing modular and cost-effective systems that reduce installation complexity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cancer and chronic diseases

- 3.2.1.2 Technological advancements in imaging and radiotherapy equipment

- 3.2.1.3 Growing investments in healthcare infrastructure

- 3.2.1.4 Increased awareness of blood safety

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment and maintenance costs

- 3.2.2.2 Strict regulatory approvals and compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI and automation in imaging systems

- 3.2.3.2 Accelerated demand for non-chemical sterilization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gamma irradiators

- 5.3 X-ray irradiators

- 5.4 Ultraviolet (UV) and neutron irradiators

- 5.5 Electron-beam irradiators

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic imaging

- 6.3 Therapy/radiotherapy

- 6.4 Sterilization and disinfection

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Research laboratories and institutes

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Canon Medical Systems

- 9.3 Elekta

- 9.4 GE HealthCare

- 9.5 Hitachi

- 9.6 Koninklijke Philips

- 9.7 Mevion Medical Systems

- 9.8 Mindray

- 9.9 Neusoft Medical Systems

- 9.10 Panacea Medical Technologies

- 9.11 Shinva Medical

- 9.12 Siemens Healthineers

- 9.13 Sumitomo Heavy Industries

- 9.14 ViewRay

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日