材料収縮低減剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Material Shrinkage-Reducing Agents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773454

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

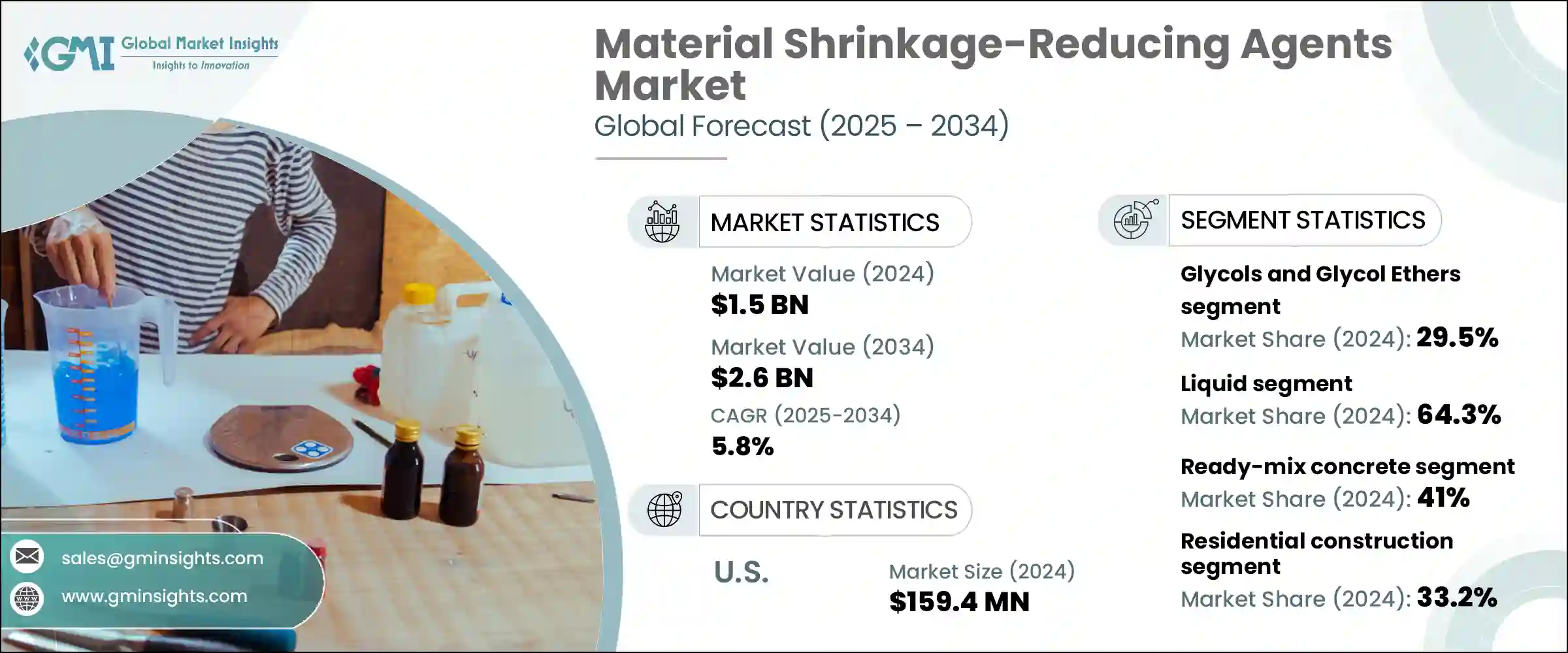

世界の材料収縮低減剤市場は、2024年に15億米ドルと評価され、CAGR 5.8%で成長し、2034年には26億米ドルに達すると推定されています。

建築基準が構造耐力と長期性能を優先するように進化するにつれ、収縮低減剤(SRA)は単なる添加剤から高性能コンクリートミックスに不可欠な成分へと変遷してきました。これらの化学溶液は、収縮に関連するひび割れを最小限に抑え、コンクリート強度を維持し、耐久性を向上させる上で重要な役割を果たしています。以前は、収縮の懸念は配合比を変更することで対処していたが、インフラや住宅建設における高度な材料に対する今日の需要が、世界市場でのSRA採用に拍車をかけています。

この成長は、急速な工業化と都市開発に牽引されたアジア太平洋地域で特に顕著です。持続可能性の重視と次世代混和剤へのシフトがSRAの使用を加速しており、特にひび割れ防止が長期的なメンテナンスコストの低減に不可欠な大規模プロジェクトではその傾向が顕著です。トンネル、高層構造物、モジュール設計など、コンクリートの用途が多様化するにつれて、SRAは環境応力や荷重下で性能を維持しながら構造物の寿命を延ばすための重要な役割を果たすと見なされるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 5.8% |

液状SRAの2024年のシェアは64.3%で、コンクリート混合物への組み込みの容易さから強い勢いを示しています。効果的な分散性と生コンとの適合性により、インフラや大量の住宅建設で最良の選択肢となっています。これらの薬剤は一貫した収縮緩和を保証し、商業不動産や公共部門工事を含む現場と工場の両方で広く採用されています。

生コンクリートは2024年の市場全体の41%を占め、SRAの主要な消費者として際立っています。これらの薬剤は、特に都市部の住宅や商業開発で使用される生コンにおいて、硬化過程における表面ひび割れや内部応力のリスクを低減するために不可欠です。プレキャストコンクリートの分野では、SRAは寸法精度を維持し、材料の収縮によって生じる可能性のある組み立てのずれを防止するために不可欠となっています。

米国の材料収縮低減剤市場は1億5,940万米ドルで85%のシェアを占めています。その主導的地位は、堅調なインフラ活動と持続可能な建設慣行への注目の高まりに起因します。橋梁、政府複合施設、交通インフラなどの公共資産の改修に対する政府主導の投資は、耐久性がありひび割れに強いコンクリートへの需要を引き続き促進しています。このため、補修・維持コストを最小限に抑えつつコンクリート構造物のライフサイクルを延ばそうとする建設業者の間で、SRAの採用が広がっています。また、環境に配慮した建築慣行への取り組みも、高度な混和剤技術へのシフトを加速させています。

材料収縮低減剤市場で事業を展開している著名な企業には、BASF SE、Mapei S.p.A.、GCP Applied Technologies(サンゴバン)、Fosroc International Ltd.、Sika AGなどがあります。材料収縮低減剤市場の企業は、技術革新、地域拡大、持続可能性を活用し、市場での地位を確保しています。大手企業は、グリーンビルディング認証に適合し、構造耐久性を高める環境に優しいSRAの開発に注力しています。建設会社やインフラ開発業者との戦略的提携により、これらの企業は自社製品を長期プロジェクトに直接組み込むことができます。研究開発投資は、様々な環境条件下での配合効率と性能の向上を目標としています。多くの企業はまた、都市建設需要の増加に対応するため、アジア太平洋のような高成長地域で生産能力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 高性能コンクリートの需要増加

- インフラ開発プロジェクトの増加

- 耐久性とひび割れ防止への注目の高まり

- 混和剤配合における技術的進歩

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 厳格な規制要件

- 技術的専門知識の要件

- 代替収縮制御方法との競合

- 市場機会

- 環境に優しい収縮低減剤の開発

- 新興市場への拡大

- スマートコンクリート技術との統合

- 特殊な建設分野における応用

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 液体収縮抑制剤

- 粉末収縮低減剤

- その他

第6章 市場推計・予測:化学複合材料別、2021年~2034年

- 主要動向

- ポリエーテル

- 多価アルコール

- グリコールおよびグリコールエーテル

- 界面活性剤

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 生コンクリート

- プレキャストコンクリート

- 自己充填コンクリート

- 高性能コンクリート

- 吹付コンクリート

- モルタルとグラウト

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 住宅建設

- 商業建設

- インフラ開発

- 産業建設

- 水封構造物

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- BASF SE

- Cementaid International Group

- Cemex S.A.B. de C.V.

- Euclid Chemical Company

- Fosroc International Ltd.

- GCP Applied Technologies(now part of Saint-Gobain)

- Imerys S.A.

- Mapei S.p.A.

- Nippon Shokubai Co., Ltd.

- RPM International Inc.

- Sika AG

- Sobute New Material Co., Ltd.

- W. R. Grace &Co.(now part of Standard Industries)

目次

The Global Material Shrinkage-Reducing Agents Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 2.6 billion by 2034. As construction standards evolve to prioritize structural resilience and long-term performance, shrinkage-reducing agents (SRAs) have transitioned from simple additives to essential components in high-performance concrete mixes. These chemical solutions play a critical role in minimizing shrinkage-related cracks, preserving concrete strength, and enhancing durability. Previously, shrinkage concerns were managed by altering mix ratios, but today's demand for advanced materials in infrastructure and residential construction is fueling SRA adoption across global markets.

This growth is especially prominent in the Asia-Pacific region, driven by rapid industrialization and urban development. Rising emphasis on sustainability and the shift toward next-generation admixtures are accelerating the use of SRAs, particularly in large-scale projects where crack prevention is essential to lower long-term maintenance costs. As concrete applications continue to diversify across tunnels, high-rise structures, and modular designs, SRAs are increasingly seen as key to extending structural life while maintaining performance under environmental stress and load.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.8% |

The liquid SRAs segment made up 64.3% share in 2024, showing strong momentum due to their ease of integration with concrete mixtures. Their effective dispersion and compatibility with ready-mix applications make them a top choice in infrastructure and high-volume residential construction. These agents ensure consistent shrinkage mitigation and are widely adopted in both on-site and factory settings, including commercial real estate and public sector works.

Ready-mix concrete contributed 41% to the total market in 2024, standing out as a major consumer of SRAs. These agents are essential in reducing the risk of surface cracks and internal stress during the curing process, especially in ready-mix systems used in urban housing and commercial developments. In the precast concrete segment, SRAs have become crucial for maintaining dimensional accuracy and preventing assembly misalignments, which can arise due to material contraction.

U.S. Material Shrinkage-Reducing Agents Market held an 85% share, valued at USD 159.4 million. Its leadership position stems from robust infrastructure activity and increased focus on sustainable construction practices. Government-led investments in rehabilitating public assets such as bridges, government complexes, and transport infrastructure continue to drive demand for durable, crack-resistant concrete. This has led to the widespread adoption of SRAs among contractors seeking to extend the lifecycle of concrete structures while minimizing repair and upkeep costs. The country's commitment to eco-conscious building practices has also accelerated the shift toward advanced admixture technologies.

Prominent companies operating in the Material Shrinkage-Reducing Agents Market include BASF SE, Mapei S.p.A., GCP Applied Technologies (Saint-Gobain), Fosroc International Ltd., and Sika AG. Companies in the material shrinkage-reducing agents market are leveraging innovation, regional expansion, and sustainability to secure their market positions. Leading firms are focusing on developing eco-friendly SRAs that comply with green building certifications and enhance structural durability. Strategic alliances with construction firms and infrastructure developers allow these companies to embed their products directly into long-term projects. R&D investments are targeted toward improving formulation efficiency and performance under varied environmental conditions. Many players are also expanding production capacities in high-growth regions like Asia-Pacific to meet rising urban construction demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Chemical Composites

- 2.2.4 Application

- 2.2.5 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for high-performance concrete

- 3.2.1.2 Increasing infrastructure development projects

- 3.2.1.3 Rising focus on durability and crack prevention

- 3.2.1.4 Technological advancements in admixture formulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price fluctuations

- 3.2.2.2 Stringent regulatory requirements

- 3.2.2.3 Technical expertise requirements

- 3.2.2.4 Competition from alternative shrinkage control methods

- 3.2.3 Market opportunities

- 3.2.3.1 Development of eco-friendly shrinkage-reducing agents

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Integration with smart concrete technologies

- 3.2.3.4 Application in specialized construction segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid shrinkage-reducing agents

- 5.3 Powder shrinkage-reducing agents

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Chemical Composites, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyethers

- 6.3 Polyalcohols

- 6.4 Glycols and glycol ethers

- 6.5 Surfactants

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ready-mix concrete

- 7.3 Precast concrete

- 7.4 Self-consolidating concrete

- 7.5 High-performance concrete

- 7.6 Shotcrete

- 7.7 Mortars and grouts

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Commercial construction

- 8.4 Infrastructure development

- 8.5 Industrial construction

- 8.6 Water containment structures

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Cementaid International Group

- 10.3 Cemex S.A.B. de C.V.

- 10.4 Euclid Chemical Company

- 10.5 Fosroc International Ltd.

- 10.6 GCP Applied Technologies (now part of Saint-Gobain)

- 10.7 Imerys S.A.

- 10.8 Mapei S.p.A.

- 10.9 Nippon Shokubai Co., Ltd.

- 10.10 RPM International Inc.

- 10.11 Sika AG

- 10.12 Sobute New Material Co., Ltd.

- 10.13 W. R. Grace & Co. (now part of Standard Industries)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日