カートニングマシンの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Cartoning Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773448

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

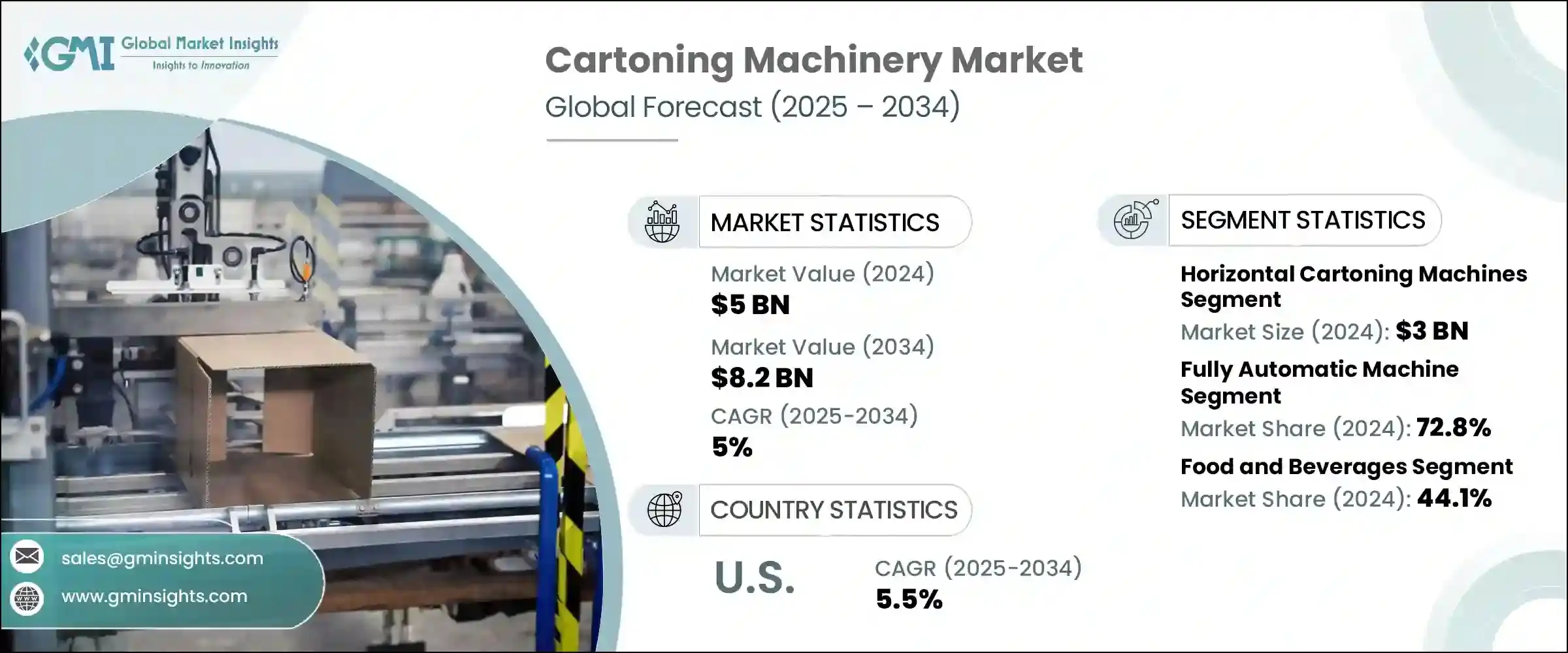

カートニングマシンの世界市場規模は、2024年に50億米ドルとなり、CAGR 5%で成長し、2034年には82億米ドルに達すると予測されています。

製造部門全体で自動化が優先されるようになり、飲食品、医薬品、パーソナルケアなどの業界で高度な漫画製作機に対する需要が高まっています。これらの分野では、大量かつ高速のパッケージングに依存しているため、自動カートンシステムは生産性の向上と手作業への依存を減らすための論理的な選択肢となっています。これと並行して、都市化や消費者のライフスタイルの変化に伴い、包装商品の需要が高まっており、業界の成長をさらに後押ししています。

特に医薬品や食品業界では、政府による包装規制が強化され、安全でトレーサブルな包装技術の採用が加速しています。カートニングマシンは、IoTセンサーやAIベースのモニタリングシステムなど、インダストリー4.0機能で強化されています。これらの機能により、予知保全やリアルタイムのデータ追跡が可能になり、業務効率が向上しています。現在、パッケージング企業の約40%がスマートオートメーションを使用して生産サイクルを合理化しています。さらに、市場では環境配慮型業務へのシフトが進んでいます。消費者の75%以上が持続可能な選択肢を好むようになり、メーカー各社はリサイクル可能な板紙やエネルギー効率の高いソリューションをカートニングラインに取り入れるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 50億米ドル |

| 予測金額 | 82億米ドル |

| CAGR | 5% |

横型カートニングマシン分野は2024年に30億米ドルを生み出し、2034年までCAGR 5.2%で成長すると予測されています。横型カートニングマシンの人気は、汎用性とスピードにあり、さまざまな製品形態の処理に理想的です。これらの機械は、パーソナルケアや食品包装に広く使用されており、精度とスループットを向上させるサーボ駆動システムのような強化された機能のおかげで、自動と手動の両方のローディングを扱うことができます。

全自動カートニングマシンセグメントは、2024年に72.8%と圧倒的なシェアを占め、2034年には61億米ドルに達すると予測されています。これらのシステムは、人手への依存を最小限に抑え、医薬品や食品生産などの大量生産分野で安定した生産量を確保できることから好まれています。AIを活用した追跡や無溶剤接着などの技術革新も、特に環境負荷の低減に重点を置く地域での利用拡大に寄与しています。

米国のカートニングマシン2024年の市場規模は9億8,000万米ドルで、2034年までCAGR 5.5%で成長する見込みです。同国は、ヘルスケア、食品、オンライン小売などの業界において、スマートカートニングマシンに対する幅広い需要でリードしています。強力な技術インフラと経験豊富な労働力により、自動化に有利な環境が整っています。また、米国のパッケージング企業は持続可能性に関する規制の影響を受けており、より環境に優しい事業へと市場を後押しし続けています。

カートニングマシン市場の主要企業は、Omori Machinery、Marchesini Group、Mpac Group、ShineBen Machinery、IMA Group、Jacob White Packaging、SaintyCo、Econocorp、BW Integrated Systems、Serpa Packaging Solution、Infinity Automated Solutions、Nichrome、ADCO Packaging Solutions、Mespack、Elite Packaging Machineryなどです。カートニングマシン市場の主要企業は、技術革新、製品のカスタマイズ、持続可能性に注力し、市場拡大を図っています。多くの企業はAIとIoTをシステムに統合し、リアルタイムの診断と予知保全を提供するスマートなコネクテッド・ソリューションを提供しています。パッケージング企業とのパートナーシップは、特に食品、製薬、パーソナルケア部門において、特定の業務ニーズに合わせて機器をカスタマイズするのに役立っています。エネルギー効率の高いシステムや環境に優しい機能を備えた製品ラインを拡大することも、世界の持続可能性の目標に沿った優先事項です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 横型カートニングマシン

- 縦型カートニングマシン

第6章 市場推計・予測:自動化別、2021年~2034年

- 主要動向

- 手動機械

- 半自動機

- 全自動機械

第7章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 100カートン未満/分

- 100~200カートン/分

- 200~400カートン/分

- 400カートン以上/分

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 医薬品

- 飲食品

- 消費財

- 化粧品とパーソナルケア

- その他(栄養補助食品など)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第11章 企業プロファイル

- ADCO Packaging Solutions

- BW Integrated Systems

- Econocorp

- Elite Packaging Machinery

- IMA Group

- Infinity Automated Solutions

- Jacob White Packaging

- Marchesini Group

- Mespack

- Mpac Group

- Nichrome

- Omori Machinery

- SaintyCo

- Serpa Packaging Solution

- ShineBen Machinery

目次

The Global Cartoning Machinery Market was valued at USD 5 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 8.2 billion by 2034. As automation becomes a priority across manufacturing sectors, demand for advanced cartooning machines is rising in industries such as food and beverages, pharmaceuticals, and personal care. These sectors rely on high-volume, high-speed packaging, making automated carton systems a logical choice for improved productivity and reduced reliance on manual labor. In parallel, the demand for packaged goods is rising with urbanization and shifting consumer lifestyles, further fueling industry growth.

Government-enforced packaging regulations, particularly in the pharmaceutical and food industries, are accelerating the adoption of secure and traceable packaging technologies. Cartoning machines are being enhanced with Industry 4.0 capabilities, including IoT sensors and AI-based monitoring systems. These features enable predictive maintenance and real-time data tracking, improving operational efficiency. About 40% of packaging firms now use smart automation to streamline their production cycles. Additionally, the market is seeing a growing shift toward eco-conscious operations. More than 75% of consumers now prefer sustainable options, prompting manufacturers to incorporate recyclable paperboard and energy-efficient solutions into cartoning lines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5 Billion |

| Forecast Value | $8.2 Billion |

| CAGR | 5% |

Horizontal cartoning machines segment generated USD 3 billion in 2024 and is forecasted to grow at a CAGR of 5.2% through 2034. Their popularity lies in their versatility and speed, making them ideal for processing different product forms. These machines are widely used in personal care and food packaging and can handle both automatic and manual loading, thanks to enhanced features like servo-driven systems that increase precision and throughput.

The fully automatic cartoning machines segment held a dominant share of 72.8% in 2024 and is projected to hit USD 6.1 billion by 2034. These systems are preferred for their minimal dependency on human labor and their ability to ensure consistent output in high-volume sectors such as pharmaceuticals and food production. Innovations such as AI-enabled tracking and solvent-free gluing have also contributed to their growing usage, particularly in regions focused on reducing environmental impact.

U.S. Cartoning Machinery Market generated USD 980 million in 2024 and is on track to grow at a 5.5% CAGR through 2034. The country leads with widespread demand for smart cartoning machinery across industries including healthcare, food, and online retail. Strong technological infrastructure and an experienced workforce make it a favorable environment for automation. U.S. packaging firms are also influenced by sustainability regulations, which continue to push the market toward greener operations.

Key players in the Cartoning Machinery Market include Omori Machinery, Marchesini Group, Mpac Group, ShineBen Machinery, IMA Group, Jacob White Packaging, SaintyCo, Econocorp, BW Integrated Systems, Serpa Packaging Solution, Infinity Automated Solutions, Nichrome, ADCO Packaging Solutions, Mespack, and Elite Packaging Machinery. Leading companies in the cartoning machinery market are focusing on technological innovation, product customization, and sustainability to expand their market reach. Many are integrating AI and IoT into their systems to offer smart, connected solutions that provide real-time diagnostics and predictive maintenance. Partnerships with packaging companies help them tailor equipment for specific operational needs, especially in the food, pharma, and personal care sectors. Expanding product lines with energy-efficient systems and eco-friendly features is another priority, aligning with global sustainability goals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Automation

- 2.2.4 Capacity

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 CXO Perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behaviour analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behaviour

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Billion)(Thousand Units)

- 5.1 Key trends

- 5.2 Horizontal cartoning machines

- 5.3 Vertical cartoning machines

Chapter 6 Market Estimates & Forecast, By Automation, 2021 - 2034, (USD Billion)(Thousand Units)

- 6.1 Key trends

- 6.2 Manual machine

- 6.3 Semi-automatic machine

- 6.4 Fully automatic machine

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034, (USD Billion)(Thousand Units)

- 7.1 Key trends

- 7.2 Up to 100 cartons/ min

- 7.3 100 to 200 cartons/ min

- 7.4 200 to 400 cartons/ min

- 7.5 Above 400 cartons/ min

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Billion)(Thousand Units)

- 8.1 Key trends

- 8.2 Pharmaceuticals

- 8.3 Food and beverages

- 8.4 Consumer goods

- 8.5 Cosmetics and personal care

- 8.6 Others (nutraceuticals etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion)(Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion)(Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 ADCO Packaging Solutions

- 11.2 BW Integrated Systems

- 11.3 Econocorp

- 11.4 Elite Packaging Machinery

- 11.5 IMA Group

- 11.6 Infinity Automated Solutions

- 11.7 Jacob White Packaging

- 11.8 Marchesini Group

- 11.9 Mespack

- 11.10 Mpac Group

- 11.11 Nichrome

- 11.12 Omori Machinery

- 11.13 SaintyCo

- 11.14 Serpa Packaging Solution

- 11.15 ShineBen Machinery

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日