|

市場調査レポート

商品コード

1773439

ロボットパレタイザー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Robotic Palletizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ロボットパレタイザー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

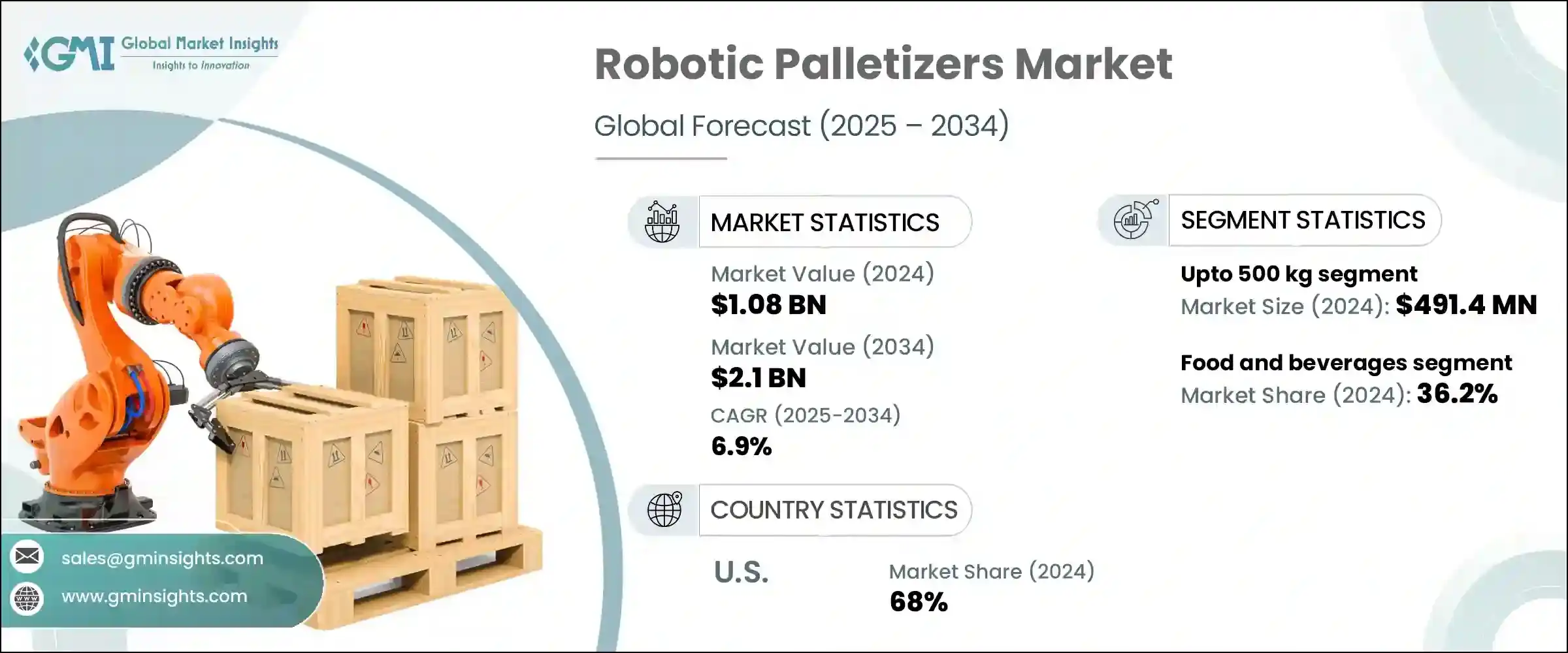

ロボットパレタイザーの世界市場規模は2024年に10億8,000万米ドルとなり、CAGR 6.9%で成長し、2034年には21億米ドルに達すると予測されています。

様々な分野での自動化需要の急増が、この市場を推進している主な要因です。ロボットパレタイザーは、パレタイジングとデパレタイジング作業を自動化するように設計されており、サイクルタイムの短縮、スループットの向上、フットプリントのコンパクト化、コスト効率の向上を可能にしています。労働力不足の深刻化、賃金の高騰、より安全で効率的なマテリアルハンドリングの推進が成長の主な要因です。パレットに商品を積み上げるという労働集約的なプロセスを自動化することで、これらのロボット・システムは手作業への依存を減らし、ミスを制限し、事故リスクを最小限に抑えることで職場の安全性を高める。

世界・ロジスティクスの複雑化とeコマースの拡大が成長をさらに後押ししています。両者とも、迅速な注文処理のために倉庫や配送センターで多様な製品を高度に効率的に取り扱うことを必要としています。先進的なロボットアームや協働ロボットの導入といったイントロダクションは、ロボットパレタイザーをより汎用性の高いものとし、中小企業にとっても身近なものとしました。このような利点がある一方で、初期コストの高さ、既存システムとの統合の複雑さ、メンテナンスやプログラミングの継続的な費用、熟練した人材の必要性などの課題に直面しています。とはいえ、技術革新と経済的メリットがロボットパレタイザーの自動製造およびサプライチェーン環境への導入を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億8,000万米ドル |

| 予測金額 | 21億米ドル |

| CAGR | 6.9% |

500kgまでの製品を扱うセグメントは、2024年に4億9,140万米ドルを生み出しました。このカテゴリのロボットは、軽量から中重量のパッケージ用に設計されており、特にeコマースや消費者製品のハンドリングにおける自動化の増加により、急速な成長を遂げています。これらのロボットパレタイザーは、医薬品、飲食品、消費財、その他の製造業などの業界で支持されています。様々なサイズの箱、袋、ケースを管理する能力により、多様なパレタイジング用途に多用途で高い需要があります。

2024年の市場シェアは、飲食品が36.2%を占め、最大でした。ロボットパレタイザーは、効率性、衛生性、一貫性が重要なこの業界で不可欠なものとなっています。大量生産と迅速な流通の需要に加え、パレタイジングのような反復作業にかかる持続的な労働力不足とコスト上昇が、企業にプロセスの自動化を促しています。ロボットシステムは作業効率を向上させるだけでなく、食品に人が触れる機会を減らし、汚染リスクを最小限に抑えます。さらに、厳格な衛生基準に適合する食品用ロボットも開発されており、この分野での採用をさらに後押ししています。

米国のロボットパレタイザー2024年の市場シェアは68%。この成長を後押ししている要因には、サプライチェーンの複雑化や人件費の高騰などがあり、ロボットパレタイザーはオペレーションの継続性を維持するための実用的な投資となっています。米国はまた、製造技術の進歩とインダストリー4.0イニシアチブの恩恵を受けており、ロボットパレタイジングソリューションの需要を押し上げています。ロボット導入のリーダー的存在である同国は、複数の製造工程でロボット密度を高めており、市場の勢いを高めています。

世界のロボットパレタイザー産業で競合する主要企業には、ファナック株式会社、KUKA AG、ABB、Honeywell International Inc、Schneider Packaging Equipment Company、Bastian Solutions、Fuji Robotics、Okura LLC、Pasco Systems、Premier Tech、Robotiq、川崎重工業株式会社、KION Group AG、Sidel、安川電機株式会社が含まれます。市場での存在感を高めるため、ロボットパレタイザー分野の企業は、幅広いサイズと重量の製品を正確に扱える、適応性の高いロボットシステムを開発し、イノベーションに注力しています。自動化の効率、統合の容易さ、ユーザーフレンドリーなインターフェースを改善するために研究開発に投資しています。包装・物流ソリューション・プロバイダーとの戦略的提携により、既存のサプライチェーンにシームレスに適合するエンド・ツー・エンドの自動化ソリューションを提供することができます。また、現地生産、顧客サービス網の強化、および顧客との強固な関係を確保するためのアフターセールス・サポートを通じて、世界なフットプリントを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 自動化の需要の高まり

- ロボット技術とAIの進歩

- eコマースと物流の成長

- 業界の潜在的リスク&課題

- 初期投資と設置コストが高め

- 技術的な複雑さと熟練労働者の必要性

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:積載量別、2021年~2034年

- 主要動向

- 500kg未満

- 501~1000 kg

- 1000kg以上

第6章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品

- 化粧品とパーソナルケア

- eコマースと物流

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- ABB

- Bastian Solutions

- FANUC Corporation

- Fuji Robotics

- Honeywell International Inc

- Kawasaki Heavy Industries Ltd

- KION Group AG

- KUKA AG

- Okura LLC

- Pasco Systems

- Premier Tech

- Robotiq

- Schneider Packaging Equipment Company

- Sidel

- Yaskawa Electric Corporation

The Global Robotic Palletizers Market was valued at USD 1.08 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 2.1 billion by 2034. The surge in automation demand across various sectors is a major factor propelling this market. Robotic palletizers are engineered to automate palletizing and depalletizing tasks, enabling faster cycle times, increased throughput, compact footprints, and cost-efficiency. Rising labor shortages, escalating wages, and the drive for safer, more efficient material handling are primary growth drivers. By automating the labor-intensive process of stacking goods onto pallets, these robotic systems reduce the dependency on manual labor, limit errors, and enhance workplace safety by minimizing accident risks.

Growth is further supported by the complexity of global logistics and the expansion of e-commerce, both of which require highly efficient handling of diverse products in warehouses and distribution centers for rapid order processing. Innovations such as advanced robotic arms and the introduction of collaborative robots have made robotic palletizers more versatile and accessible to small and medium-sized businesses alike. Despite their advantages, the market faces challenges due to high upfront costs, integration complexities with existing systems, ongoing maintenance and programming expenses, and the need for skilled personnel. Nevertheless, ongoing technological innovations and economic benefits are driving the adoption of robotic palletizers within automated manufacturing and supply chain environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.08 billion |

| Forecast Value | $2.1 billion |

| CAGR | 6.9% |

The handling products up to 500 kg segment generated USD 491.4 million in 2024. Robots in this category are designed for light to medium-weight packages and are experiencing rapid growth, particularly due to increasing automation in e-commerce and consumer product handling. These robotic palletizers are favored across industries such as pharmaceuticals, food and beverages, consumer goods, and other manufacturing sectors. Their ability to manage varying box sizes, bags, and cases makes them versatile and highly demanded for diverse palletizing applications.

The food & beverages segment held the largest market share in 2024, accounting for 36.2%. Robotic palletizers have become indispensable in this industry where efficiency, hygiene, and consistency are critical. High-volume production and swift distribution demands, combined with persistent labor shortages and rising costs for repetitive tasks like palletizing, push companies to automate processes. Robotic systems not only improve operational efficiency but also reduce human contact with food products, minimizing contamination risks. Additionally, specialized food-grade robots are developed to comply with strict hygiene standards, further driving adoption in this sector.

United States Robotic Palletizers Market held a 68% share in 2024. Factors fueling this growth include increasing supply chain complexity and high labor costs, which make robotic palletizers a practical investment to maintain operational continuity. The U.S. also benefits from advancements in manufacturing technology and Industry 4.0 initiatives, boosting the demand for robotic palletizing solutions. As one of the leaders in robotics adoption, the country exhibits growing robot density across multiple manufacturing processes, enhancing market momentum.

Leading companies competing in the Global Robotic Palletizers Industry include FANUC Corporation, KUKA AG, ABB, Honeywell International Inc, Schneider Packaging Equipment Company, Bastian Solutions, Fuji Robotics, Okura LLC, Pasco Systems, Premier Tech, Robotiq, Kawasaki Heavy Industries Ltd, KION Group AG, Sidel, and Yaskawa Electric Corporation. To strengthen their market presence, companies in the robotic palletizers sector focus on innovation by developing highly adaptable robotic systems capable of handling a wide range of product sizes and weights with precision. They invest in research and development to improve automation efficiency, ease of integration, and user-friendly interfaces. Strategic collaborations with packaging and logistics solution providers allow them to deliver end-to-end automation solutions that fit seamlessly into existing supply chains. Firms also expand their global footprint through localized production, enhanced customer service networks, and tailored after-sales support, ensuring robust client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Payload Capacity

- 2.2.3 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for automation

- 3.2.1.2 Advancements in robotic technology and AI

- 3.2.1.3 Growth of e-commerce and logistics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and installation costs

- 3.2.2.2 Technical complexity and need for skilled labor

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Payload Capacity, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Upto 500 kg

- 5.3 501-1000 kg

- 5.4 Above 1000 kg

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Food and beverages

- 6.3 Pharmaceuticals

- 6.4 Cosmetics and personal care

- 6.5 E-commerce and logistics

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Bastian Solutions

- 8.3 FANUC Corporation

- 8.4 Fuji Robotics

- 8.5 Honeywell International Inc

- 8.6 Kawasaki Heavy Industries Ltd

- 8.7 KION Group AG

- 8.8 KUKA AG

- 8.9 Okura LLC

- 8.10 Pasco Systems

- 8.11 Premier Tech

- 8.12 Robotiq

- 8.13 Schneider Packaging Equipment Company

- 8.14 Sidel

- 8.15 Yaskawa Electric Corporation