|

市場調査レポート

商品コード

1773438

建設用わらベールの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Straw Bale for Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 建設用わらベールの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

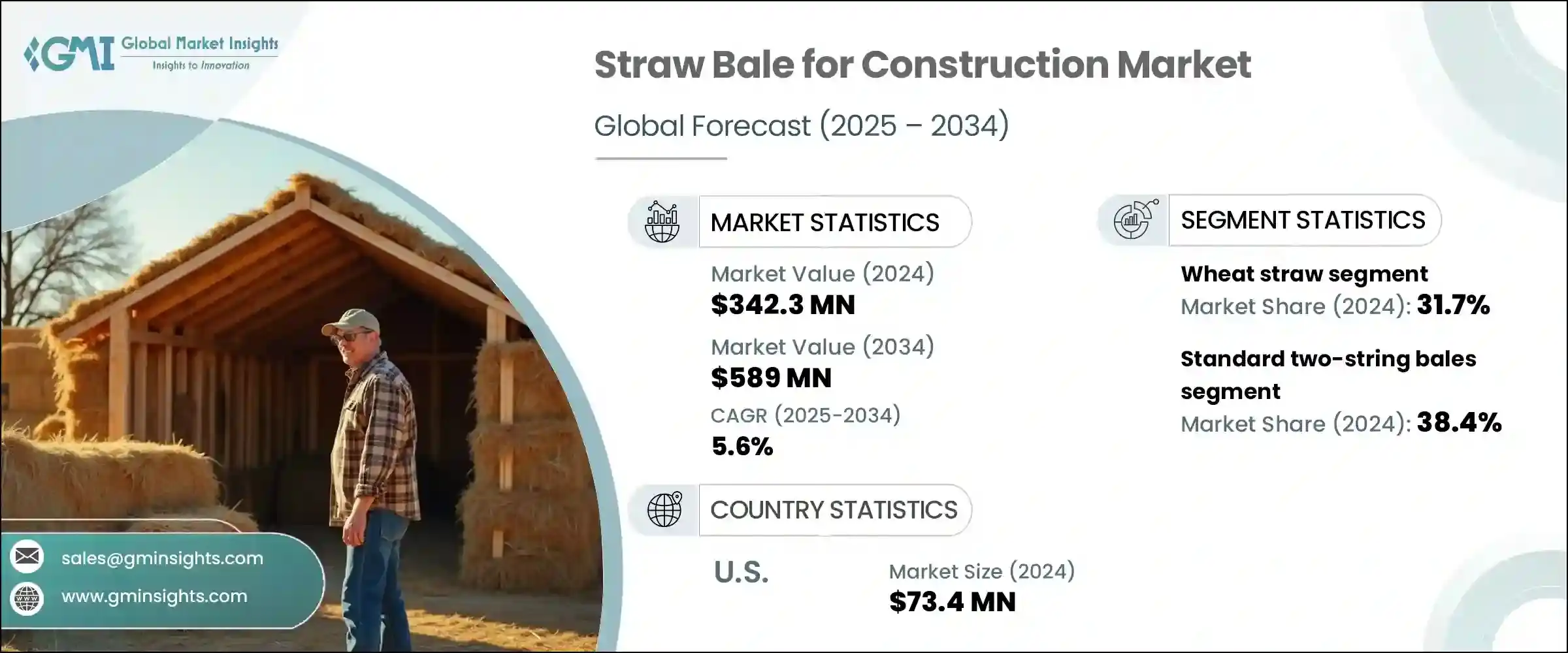

世界の建設用わらベール市場は、2024年に3億4,230万米ドルと評価され、CAGR 5.6%で成長し、2034年には5億8,900万米ドルに達すると推定されています。

この成長は、わらベール建築の環境に優しくエネルギー効率に優れた特性によるところが大きいです。密に圧縮されたわらベールを主要な壁材として利用し、自然素材のプラスターやコーティングで仕上げるこの技術は、環境への負荷が低いことで支持を集めています。農業製品別であるわらは豊富に入手でき、価格も手頃であるため、建築における持続可能な代替案となっています。わらベール構造が際立つのは、その優れた断熱性能で、ベールの密度と壁の厚さにもよりますが、R値は通常R-30からR-35の間です。

このような高い断熱性能は、特に冷暖房時のエネルギー消費を削減し、コスト削減と環境面でのメリットをもたらします。さらに、わらは自然の炭素吸収源として機能し、植物の成長サイクルの間に吸収された二酸化炭素を隔離します。この炭素貯蔵能力は、建物の二酸化炭素排出量を全体的に削減する上で、この材料の役割を高めます。低負荷建築ソリューションへの関心が高まる中、わらベール建築は、特にグリーンインフラ、持続可能な住宅、再生可能素材を重視する地域において、さまざまな地域でますます人気の選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 3億4,230万米ドル |

| 予測金額 | 5億8,900万米ドル |

| CAGR | 5.6% |

麦わらセグメントは、その入手可能性と構造上の優位性により、2024年には31.7%のシェアを占めました。その平行な繊維配向は、コンパクトな梱包、安定した断熱性、構造用途での耐久性を可能にします。さらに、生分解が容易で建設環境に適応しやすいことも、麦わらの利用拡大に寄与しています。麦わらは、その耐湿性とエコ建築工法への適合性が認められています。この素材は、伝統的な建築技法に長年組み込まれてきたことと、現代の持続可能な建築において実証された性能が、様々な地域での採用をさらに後押ししています。

標準的な2連ベールのセグメントは、2024年に38.4%のシェアを占めました。これらのベールは、耐荷重建築システムへの組み込みが容易なため、広く使用されています。バランスの取れたサイズと重量は取り扱い効率を向上させ、従来のベーリング機器との互換性により、非常に利用しやすくなっています。建設業者、請負業者、セルフビルダーは、費用対効果と輸送のしやすさから、これらのベールを好んで使用しています。さらに、持続可能な建築の促進を目的とした研修プログラムや教育イニシアティブでは、このベールが教材として取り上げられることが多く、環境に優しい建築手法に対する地域社会の理解を深めるのに役立っています。

米国建設用わらベール2024年の市場規模は7,340万米ドル。わらベール建築における同国のリーダーシップは、環境に配慮した住宅への関心の高まりと、低炭素建築工法を推進する地域イニシアティブに支えられています。農業の製品別として利用可能なわらは、持続可能なオフグリッド住宅や注文住宅への需要の高まりと相まって、引き続き普及を後押ししています。エコロジカルな住宅開発を奨励する政府のプログラムや、クリーンな素材に焦点を当てた州レベルのエネルギー政策による支援は、この動向を強化し、世界の郊外や半農村地域での拡大を促進しています。

世界の建設用わらベール業界は依然として適度に断片化されており、Endeavour Centre、Strawcture Eco、ModCell Straw Technology、Ecococon、Straw-Bale Building UKなどの主要企業がニッチ市場で積極的に事業を展開し、地域の需要を支えています。わらベール建築市場の企業は、市場での存在感を高め、環境と消費者の需要の変化に適応するため、的を絞った戦略を採用しています。

多くの企業は、物流コストと二酸化炭素排出量を削減するため、わらの現地生産と調達に注力しています。製品の標準化は、地域の建築基準法に準拠し、主要な建設部門からの信頼を得るために進められています。建築家や持続可能性に重点を置く開発業者との戦略的協力により、企業は最新のエコ住宅におけるわらベール構造の使用事例を紹介しています。教育主導のキャンペーンや地域に根ざしたワークショップが市場認知をさらに促進し、実地研修の取り組みが請負業者やセルフビルド業者の信頼を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- わらの種類別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:わらの種類別、2021~2034年

- 主要動向

- 麦わら

- 稲わら

- 大麦わら

- オート麦わら

- ライ麦の茎

- その他

第6章 市場推計・予測:ベール形式、2021~2034年

- 主要動向

- 標準的な2連ベール

- 3連ベール

- ジャンボベール

- カスタムサイズのベール

- プレハブわらパネル

第7章 市場推計・予測:工法別、2021~2034年

- 主要動向

- 耐荷重/ネブラスカスタイル

- 柱梁接合部

- ハイブリッド方式

- プレハブパネルシステム

- その他

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 外壁

- 内壁

- 屋根断熱材

- 床断熱材

- 遮音

- その他

第9章 推定・予測:用途別、2021~2034年

- 主要動向

- 住宅建設

- 一戸建て住宅

- 集合住宅

- 小さな家と小屋

- 増築と改修

- 商業建設

- 教育施設

- エコツーリズム施設

- 小売店とオフィススペース

- その他

- 農業用建物

- コミュニティと公共の建物

- その他

第10章 推定・予測:仕上げの種類別、2021~2034年

- 主要動向

- 石灰漆喰

- 粘土漆喰

- セメントスタッコ

- 土壁

- サイディングとクラッディング

- その他

第11章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第12章 企業プロファイル

- BRAR AGRO WORKS

- CalFibre

- Ecococon

- Endeavour Centre

- Grass Land Gold Pvt. Ltd

- Gruppo Carli

- ModCell Straw Technology

- Profodd Private Limited

- Straw-Bale Building UK

- Strawcture Eco

The Global Straw Bale for Construction Market was valued at USD 342.3 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 589 million by 2034. This growth is largely attributed to the eco-friendly and energy-efficient characteristics of straw bale construction. Utilizing tightly compacted straw bales as primary wall material, the technique is finished with natural plasters or coatings and has gained traction for its low environmental impact. As an agricultural by-product, straw is abundantly available and affordable, making it a sustainable alternative in construction. What makes straw bale structures stand out is their impressive insulation capability, with R-values typically ranging between R-30 and R-35, depending on bale density and wall thickness.

These high insulation values reduce energy consumption, especially in heating and cooling, resulting in cost savings and environmental benefits. Additionally, straw serves as a natural carbon sink, sequestering carbon dioxide absorbed during the plant's growth cycle. This carbon-storing ability enhances the material's role in reducing the overall carbon footprint of buildings. With rising interest in low-impact building solutions, straw bale construction is becoming an increasingly popular choice across different geographies, particularly in areas emphasizing green infrastructure, sustainable housing, and renewable materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $342.3 Million |

| Forecast Value | $589 Million |

| CAGR | 5.6% |

The wheat straw segment held a 31.7% share in 2024 due to its availability and structural advantages. Its parallel fiber orientation enables compact packing, consistent insulation, and durability in structural applications. Furthermore, its ease of biodegradation and adaptability to construction environments contribute to its growing use. Wheat straw is recognized for its moisture-resistant properties and compatibility with eco-construction methods. The material's long-standing integration into traditional building techniques and its proven performance in contemporary sustainable construction further boost its adoption across various regions.

The standard two-string bales segment held a 38.4% share in 2024. These bales are widely used because of their ease of integration into load-bearing construction systems. Their balanced size and weight improve handling efficiency, and their compatibility with conventional baling equipment makes them highly accessible. Builders, contractors, and self-builders favor these bales for their cost-effectiveness and ease of transport. Additionally, training programs and educational initiatives aimed at promoting sustainable building often feature these bales as teaching tools, helping to enhance community understanding of eco-friendly construction practices.

United States Straw Bale for Construction Market generated USD 73.4 million in 2024. The country's leadership in straw bale construction is supported by a growing emphasis on environmentally conscious housing and regional initiatives promoting low-carbon building methods. The availability of straw as a farming by-product, combined with evolving demand for sustainable off-grid and custom-built homes, continues to push adoption forward. Support from governmental programs encouraging ecological housing development, alongside state-level energy policies focused on clean materials, reinforces this trend and fosters expansion in suburban and semi-rural areas globally.

The Global Straw Bale for Construction Industry remains moderately fragmented, with key players such as Endeavour Centre, Strawcture Eco, ModCell Straw Technology, Ecococon, and Straw-Bale Building UK actively operating in niche markets and supporting localized demand. Companies in the straw bale construction market are employing targeted strategies to bolster their market presence and adapt to changing environmental and consumer demands.

Many firms are focusing on local production and sourcing of straw to reduce logistics costs and carbon emissions. Product standardization efforts are being pursued to comply with regional building codes and gain trust from mainstream construction sectors. Strategic collaborations with architects and sustainability-focused developers help companies showcase use cases of straw bale construction in modern eco-homes. Education-driven campaigns and community-based workshops further promote market awareness, while hands-on training initiatives increase confidence among contractors and self-builders.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Straw type

- 2.2.2 Bale format

- 2.2.3 Construction method

- 2.2.4 Application

- 2.2.5 End use sector

- 2.2.6 Finishing type

- 2.2.7 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By straw type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Straw Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Wheat straw

- 5.3 Rice straw

- 5.4 Barley straw

- 5.5 Oat straw

- 5.6 Rye straw

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Bale Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Standard two-string bales

- 6.3 Three-string bales

- 6.4 Jumbo bales

- 6.5 Custom-sized bales

- 6.6 Prefabricated straw panels

Chapter 7 Market Estimates and Forecast, By Construction Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Load-bearing/nebraska style

- 7.3 Post-and-beam infill

- 7.4 Hybrid methods

- 7.5 Prefabricated panel systems

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Exterior walls

- 8.3 Interior walls

- 8.4 Roof insulation

- 8.5 Floor insulation

- 8.6 Sound insulation

- 8.7 Others

Chapter 9 Estimates and Forecast, By End Use Sector, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Residential construction

- 9.2.1 Single-family homes

- 9.2.2 Multi-family buildings

- 9.2.3 Tiny homes and cabins

- 9.2.4 Additions and renovations

- 9.3 Commercial construction

- 9.3.1 Educational facilities

- 9.3.2 Eco-tourism facilities

- 9.3.3 Retail and office spaces

- 9.3.4 Others

- 9.4 Agricultural buildings

- 9.5 Community and public buildings

- 9.6 Others

Chapter 10 Estimates and Forecast, By Finishing Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Lime plaster

- 10.3 Clay plaster

- 10.4 Cement stucco

- 10.5 Earthen plasters

- 10.6 Siding and cladding

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 BRAR AGRO WORKS

- 12.2 CalFibre

- 12.3 Ecococon

- 12.4 Endeavour Centre

- 12.5 Grass Land Gold Pvt. Ltd

- 12.6 Gruppo Carli

- 12.7 ModCell Straw Technology

- 12.8 Profodd Private Limited

- 12.9 Straw-Bale Building UK

- 12.10 Strawcture Eco