|

市場調査レポート

商品コード

1773436

防音乾式壁材市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Soundproof Drywall Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 防音乾式壁材市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

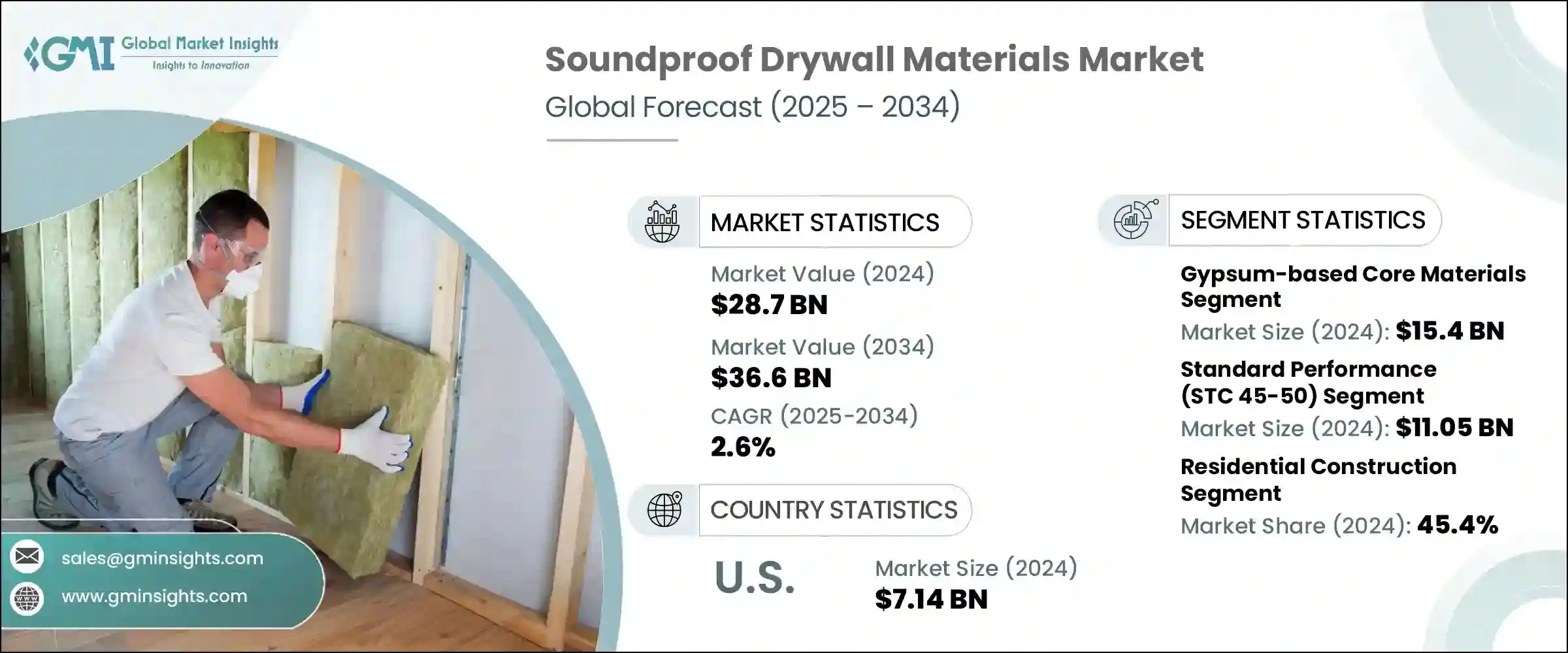

防音乾式壁材の世界市場規模は、2024年に287億米ドルとなり、CAGR 2.6%で成長し、2034年には366億米ドルに達すると予測されています。

この成長は、都市騒音レベルの上昇と音響快適性に関する意識の高まりが大きな要因となっています。都市が拡大し都市化が進むにつれて、交通量や産業活動、住宅密集地による騒音公害が大幅に増加しています。このため、建築物にはより良い音響ソリューションが求められるようになり、防音乾式壁材は住宅所有者や建築業者の間で好まれる選択肢となっています。今日の消費者は、生活環境や職場環境に対してより高い意識を持つようになり、より静かなインテリアを求めるようになっています。この動向は、騒音が日常的に懸念される大都市圏で特に強く、不動産開発業者が建設プロジェクトで防音対策を優先するよう促しています。

商業施設も防音乾式壁の需要拡大に貢献しており、ビル所有者は騒音対策が従業員の生産性や顧客満足度に与える影響を認識しています。オフィス、ヘルスケアセンター、ホスピタリティ施設、教育機関などでは、室内の音環境を改善するために先進的な乾式壁材への投資が増えています。建設業界各社は、このような進化する音響要件に対応するため、提供する製品を変化させています。開発者は、防音乾式壁を新規プロジェクトに組み込むだけでなく、変化する建築基準や消費者の期待に沿うよう、既存の構造物を改良された材料で改修しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 287億米ドル |

| 予測金額 | 366億米ドル |

| CAGR | 2.6% |

材料別では、石膏系コア乾式壁が引き続き市場を独占しています。この分野は2024年に154億米ドルと評価され、予測期間中にCAGR 1.8%で成長すると予想されます。その人気は、費用対効果と施工の容易さに起因しています。しかし、競争力を維持し、高まる期待に応えるため、メーカー各社は吸音性や耐火性に優れた機能を取り入れることで、これらの材料を強化しています。これらの技術革新は、住宅と商業建築の両方で主流ソリューションとして石膏系コアの需要を維持するのに役立っています。

性能面では、標準的な音響透過率クラス(STC)45~50のセグメントが、特にコスト効率が重要な要素となるプロジェクトで、依然として広く使用されています。このカテゴリーは2024年に110億5,000万米ドルと評価され、2025年から2034年にかけてCAGR 1.3%で成長すると予測されています。この標準レベルの防音壁に対する需要は安定しているもの、多くの用途でより高性能な乾式壁へのシフトが目に見えています。STC等級が51~55に改善された乾式壁が、特に集合住宅、オフィススペース、改築プロジェクトで支持を集めています。コストと性能のバランスが最適であるため、コストを大幅に上げることなく音響性能を高めたい開発者にとって有利な選択肢となっています。

住宅建設部門は世界市場で最大のシェアを占め、2024年には130億米ドルに達しました。この分野は2034年までCAGR 2.9%で拡大し、市場の45.4%のシェアを確保すると予想されています。都市部の住宅、特に高層アパートや集合住宅における騒音対策需要の高まりが、この動向を後押しする大きな要因となっています。住宅所有者が快適さと幸福感をより重視する中、住宅プロジェクトでは壁、天井、間仕切りに防音乾式壁を取り入れるケースが増えています。

米国では、防音乾式壁材市場は2024年に71億4,000万米ドルとなり、2025年から2034年までのCAGRは2.3%になると予測されています。この成長の原動力は、家庭と職場の両方における音響的快適性の重要性の高まりです。都市人口の増加、騒音による健康への影響に対する意識の高まり、主要州における厳格な建築基準法が、建設業者にSTCの高い乾式壁製品の採用を促しています。さらに、リモートワークの継続的な採用により、より静かなホームオフィス環境へのニーズが高まり、遮音ドライウォールソリューションへの需要がさらに高まっています。

防音乾式壁材市場のトップメーカーは、継続的な技術革新、大規模生産、整った流通システムに注力することでリーダーシップを維持しています。これらの企業は一貫して研究開発に投資し、防音性、耐湿性、耐火性を強化した乾式壁ソリューションを開発しています。包括的な壁システムを提供する能力により、住宅と商業建築の両分野で競争優位に立っています。早期の製品仕様を確保するため、これらの企業は建築家、建設業者、請負業者と積極的に協力しています。また、グリーン建築基準に沿って、環境に優しく認証された建築資材の採用を支援しています。技術サポート、施工者トレーニングプログラム、的を絞ったマーケティング戦略を提供することで、彼らは市場の嗜好を形成し、世界の防音乾式壁材業界における優位性を維持し続けています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 石膏ベースのコア材

- 標準密度石膏

- 高密度石膏

- 軽量石膏配合

- 粘弾性減衰材料

- ポリマーベースの制振材

- ビチューメン制振材

- ハイブリッドダンピングシステム

- 音響膜と遮音壁

- マスローデッドビニール(MLV)

- ポリマー音響膜

- 複合バリア材

- 補強材および外装材

- 紙張り材

- グラスファイバーマット表面

- 不織布合成表面材

- 添加剤およびパフォーマンス向上剤

- 難燃剤添加剤

- 耐湿性添加剤

- 音響性能向上装置

第6章 市場推計・予測:性能クラス別、2021年~2034年

- 主要動向

- 標準性能(STC 45-50)

- 強化性能(STC 51-55)

- 高性能(STC 56-60)

- プレミアム性能(STC 60+)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 住宅建設

- 内部間仕切り壁

- 床天井アセンブリ

- 外壁システム

- 商業建設

- オフィスビルおよび企業施設

- ホテルとホスピタリティ

- 小売店と娯楽施設

- 制度構築

- ヘルスケア施設

- 教育施設

- 政府機関および市町村の建物

- 産業および特殊用途

- 製造施設

- データセンターと技術ビル

- レコーディングスタジオと劇場

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第9章 企業プロファイル

- 3A Composites Holding AG

- 3M Company

- Acoustical Surfaces, Inc.

- American Gypsum

- Continental Building Products

- Dow Inc.

- Georgia-Pacific LLC

- Guardian Building Products

- Henkel AG &Co. KGaA

- Johns Manville(Berkshire Hathaway)

- Kinetics Noise Control, Inc.

- Knauf Group

- National Gypsum Company

- Owens Corning

- PABCO Gypsum

- Rockwool International A/S

- RPG Acoustical Systems

- Saint-Gobain(Gyproc/CertainTeed)

- Sika AG

- Trademark Soundproofing

- USG Corporation(Berkshire Hathaway)

The Global Soundproof Drywall Materials Market was valued at USD 28.7 billion in 2024 and is estimated to grow at a CAGR of 2.6% to reach USD 36.6 billion by 2034. This growth is largely driven by the rising levels of urban noise and the growing awareness around acoustic comfort. As cities expand and urbanization intensifies, noise pollution from heavy traffic, industrial activities, and densely packed residential zones has significantly increased. This has fueled the need for better acoustic solutions in buildings, making soundproof drywall materials a preferred choice among homeowners and builders alike. Consumers today are more conscious of their living and working environments, which has translated into a demand for quieter interiors. The trend is particularly strong in metropolitan areas where noise intrusion is a daily concern, prompting real estate developers to prioritize soundproofing in their construction projects.

Commercial properties are also contributing to the growing demand for soundproof drywall, as building owners recognize the impact of noise control on employee productivity and customer satisfaction. Offices, healthcare centers, hospitality facilities, and educational institutions are increasingly investing in advanced drywall materials to improve interior sound environments. Companies in the construction industry are adapting their offerings to meet these evolving acoustic requirements. Developers are not only integrating soundproof drywall into new projects but are also retrofitting existing structures with improved materials to stay aligned with changing building standards and consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.7 billion |

| Forecast Value | $36.6 billion |

| CAGR | 2.6% |

In terms of material, gypsum-based core drywall continues to dominate the market. This segment was valued at USD 15.4 billion in 2024 and is expected to grow at a CAGR of 1.8% during the forecast period. Its popularity stems from its cost-effectiveness and ease of installation. However, to stay competitive and cater to rising expectations, manufacturers are enhancing these materials by incorporating better sound absorption and fire-resistance features. These innovations are helping maintain the demand for gypsum-based cores as a mainstream solution in both residential and commercial construction.

From a performance standpoint, the standard sound transmission class (STC) 45-50 segment remains widely used, especially in projects where cost efficiency is a key factor. This category was valued at USD 11.05 billion in 2024 and is set to grow at a CAGR of 1.3% from 2025 to 2034. Although demand for this standard level of soundproofing remains steady, there is a visible shift toward higher-performance drywall in many applications. Drywall with an improved STC rating of 51-55 is gaining traction, particularly in apartment buildings, office spaces, and renovation projects. It offers an optimal balance between cost and performance, making it a favorable choice for developers looking to boost acoustic performance without significantly raising costs.

The residential construction sector accounted for the largest share of the global market, reaching a value of USD 13 billion in 2024. This segment is expected to expand at a CAGR of 2.9% through 2034, securing a 45.4% share of the market. Rising demand for noise control in urban housing, particularly in high-rise apartments and multi-family units, is a major factor driving this trend. With homeowners placing greater emphasis on comfort and well-being, residential projects are increasingly incorporating soundproof drywall into walls, ceilings, and partitions.

In the United States, the soundproof drywall materials market stood at USD 7.14 billion in 2024 and is anticipated to witness a CAGR of 2.3% from 2025 to 2034. This growth is fueled by the increasing importance of acoustic comfort in both homes and workplaces. Growing urban populations, higher awareness of the health effects of noise, and strict building codes in key states are prompting contractors to adopt drywall products with high STC ratings. Additionally, the continued adoption of remote work practices has increased the need for quieter home office environments, further boosting demand for acoustic drywall solutions.

Top manufacturers in the soundproof drywall materials market maintain their leadership by focusing on continuous innovation, large-scale production, and well-structured distribution systems. These companies are consistently investing in R&D to develop drywall solutions that offer enhanced acoustic, moisture, and fire-resistance properties. Their ability to deliver comprehensive wall systems gives them a competitive edge in both residential and commercial construction segments. To secure early product specifications, these players actively collaborate with architects, builders, and contractors. They also support the adoption of eco-friendly and certified building materials in line with green construction standards. By offering technical support, installer training programs, and targeted marketing strategies, they continue to shape market preferences and uphold their dominance in the global soundproof drywall materials industry.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Performance Class

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Gypsum-based core materials

- 5.2.1 Standard density gypsum

- 5.2.2 High-density gypsum

- 5.2.3 Lightweight gypsum formulations

- 5.3 Viscoelastic damping materials

- 5.3.1 Polymer-based damping compounds

- 5.3.2 Bituminous damping materials

- 5.3.3 Hybrid damping systems

- 5.4 Acoustic membranes and barriers

- 5.4.1 Mass-loaded vinyl (MLV)

- 5.4.2 Polymer acoustic membranes

- 5.4.3 Composite barrier materials

- 5.5 Reinforcement and facing materials

- 5.5.1 Paper facing materials

- 5.5.2 Fiberglass mat facing

- 5.5.3 Non-woven synthetic facings

- 5.6 Additives and performance enhancers

- 5.6.1 Fire retardant additives

- 5.6.2 Moisture resistance additives

- 5.6.3 Acoustic performance enhancers

Chapter 6 Market Estimates & Forecast, By Performance Class, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Standard performance (STC 45-50)

- 6.3 Enhanced performance (STC 51-55)

- 6.4 High performance (STC 56-60)

- 6.5 Premium performance (STC 60+)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential construction

- 7.2.1 Interior partition walls

- 7.2.2 Floor-ceiling assemblies

- 7.2.3 Exterior wall systems

- 7.3 Commercial construction

- 7.3.1 Office buildings and corporate facilities

- 7.3.2 Hotels and hospitality

- 7.3.3 Retail and entertainment venues

- 7.4 Institutional construction

- 7.4.1 Healthcare facilities

- 7.4.2 Educational buildings

- 7.4.3 Government and municipal buildings

- 7.5 Industrial and specialty applications

- 7.5.1 Manufacturing facilities

- 7.5.2 Data centers and technical buildings

- 7.5.3 Recording studios and theaters

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 3A Composites Holding AG

- 9.2 3M Company

- 9.3 Acoustical Surfaces, Inc.

- 9.4 American Gypsum

- 9.5 Continental Building Products

- 9.6 Dow Inc.

- 9.7 Georgia-Pacific LLC

- 9.8 Guardian Building Products

- 9.9 Henkel AG & Co. KGaA

- 9.10 Johns Manville (Berkshire Hathaway)

- 9.11 Kinetics Noise Control, Inc.

- 9.12 Knauf Group

- 9.13 National Gypsum Company

- 9.14 Owens Corning

- 9.15 PABCO Gypsum

- 9.16 Rockwool International A/S

- 9.17 RPG Acoustical Systems

- 9.18 Saint-Gobain (Gyproc/CertainTeed)

- 9.19 Sika AG

- 9.20 Trademark Soundproofing

- 9.21 USG Corporation (Berkshire Hathaway)