|

市場調査レポート

商品コード

1773431

カテーテル安定化装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Catheter Stabilization Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カテーテル安定化装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

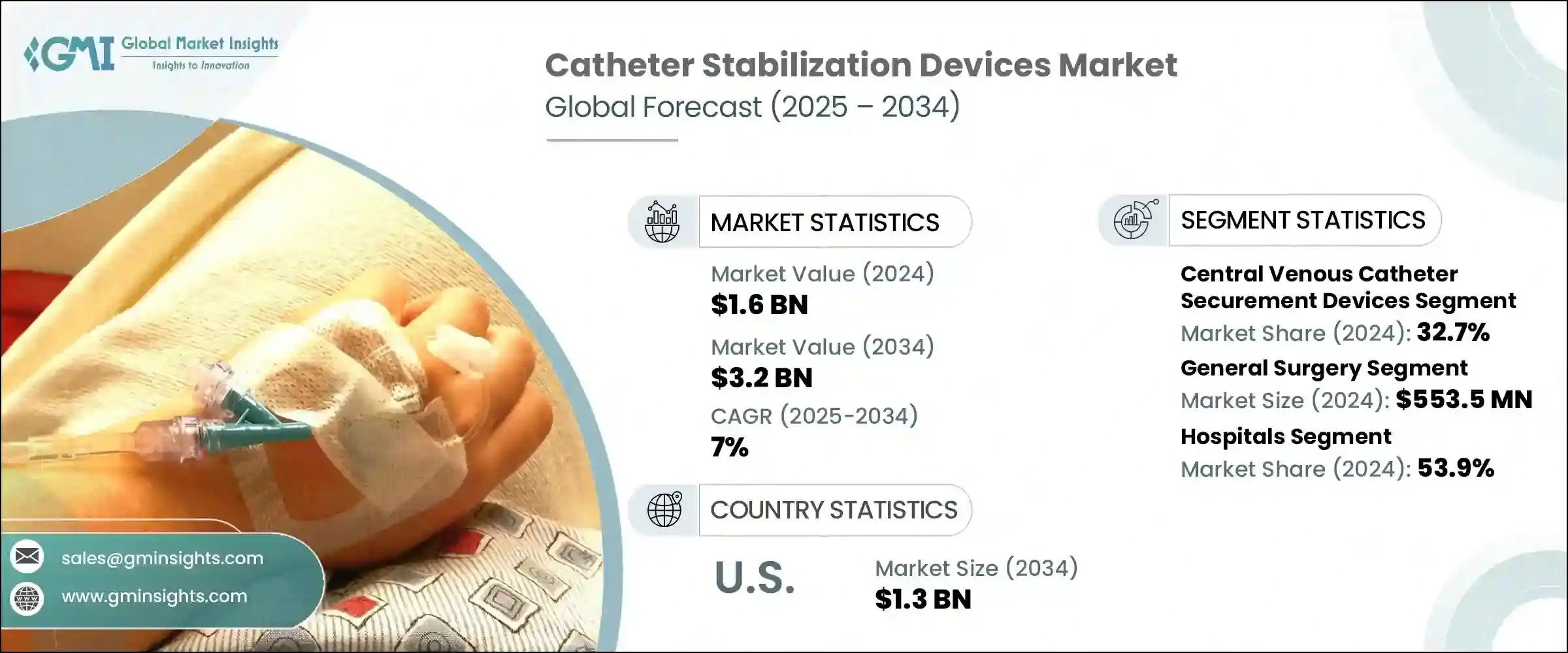

カテーテル安定化装置の世界市場規模は2024年に16億米ドルで、CAGR 7%で成長し、2034年には32億米ドルに達すると予測されています。

カテーテル安定化装置は臨床治療に不可欠なツールであり、さまざまなタイプのカテーテルを身体にしっかりと固定し、動きを抑えて脱落を防ぎ、移動のリスクを低減するように設計されています。この安定性は患者を保護するだけでなく、正確で中断のない治療を可能にします。がん、腎不全、糖尿病、心血管疾患などの慢性疾患の世界の蔓延が進むにつれ、臨床現場におけるカテーテルの長期使用の必要性が高まっています。

さらに、病院では感染対策がますます優先されるようになっており、固定方法の改善を通じてカテーテル関連感染を予防することにますます焦点が当てられています。カテーテルを使用した処置や在宅介護支援を頻繁に必要とする高齢化も、この市場の拡大にさらに寄与しています。高齢者では皮膚が脆弱で感染症にかかりやすいため、安全で快適なカテーテル固定の必要性が高まっています。そのため、高品質で装着が簡単な安定化装置に対する需要は、特に長期および在宅ヘルスケアサービスを提供する施設全体で急速に高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 7% |

2024年には、デバイス部門が32.7%のシェアを占める。これらのカテーテルは、集中治療、腫瘍学、救急医療において、薬剤投与や栄養補給などの重要な治療に広く応用されています。これらの臨床領域における高度な治療に対する需要の高まりに伴い、カテーテルの移動や汚染に起因する血流感染、心内膜炎、敗血症などの合併症を最小限に抑えるために、固定器具が不可欠となっています。こうしたリスクを軽減するため、ヘルスケア機関や管理団体はより厳格な感染管理プロトコルを施行し、その多くがカテーテル固定用具の使用を義務付けています。このような規制の変化は、複数の医療現場における固定器具の採用を後押ししています。

一般外科セグメントは、2024年に5億5,350万米ドルを生み出しました。カテーテルは、麻酔の投与、体液のモニタリング、バイタルサインの追跡など、外科手術で幅広く使用されています。安定化装置は、手術中や術後ケア、特に手術室から回復エリアへの移動中にカテーテルの留置を確実に維持するために不可欠です。病院は、外科手術中にしばしば発生する中心静脈ライン関連血流感染や手術部位感染の発生率を低下させる必要に迫られています。このため、病院の安全対策に合致し、手技の転帰を改善する安定化ソリューションへの需要が高まっています。

米国カテーテル安定化装置2024年の市場規模は6億6,750万米ドルで、2034年には13億米ドルに達すると予測されています。全米で慢性疾患患者が増加していることが、カテーテルを用いた治療の必要性を高めており、ひいては安定化装置の採用を増加させています。米国の病院は、さまざまなヘルスケア団体が定めた厳しい安全規制に従っており、施設は標準化された感染制御方法を使用することが義務付けられています。このような安全基準を遵守しないと、診療報酬の減額や金銭的な罰則につながる可能性があるため、医療機関は固定器具への投資を促しています。こうした動向は、米国を世界のカテーテル安定化領域における主要な成長地域と位置づけています。

現在、BD、3M、Cardinal Health、ConvaTec、B. Braunなどの企業が業界を支配しており、合計で市場全体の約65%のシェアを占めています。カテーテル安定化装置市場の大手企業は、複数の戦略を駆使して存在感を高め、長期的な成長を確保しています。主な焦点は、感染リスクを低減し、適用を容易にする、患者に優しい先進的な製品の開発です。

各社は、特定の医療ニーズに対応し、高齢者のような脆弱な患者集団に対応する革新的なデザインを提供するため、研究開発努力を強化しています。パートナーシップ、現地製造、戦略的流通契約による地理的拡大は、製品ラインへのアクセス拡大に役立っています。法規制の遵守もまた主要な焦点であり、企業は進化する臨床基準に沿うことで、医療機関の信頼を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 慢性疾患の発生率の増加

- 世界の人口高齢化

- カテーテル安定化技術の継続的な革新

- 固定装置の費用対効果

- 業界の潜在的リスク&課題

- 代替製品の入手可能性

- 厳格な規制要件

- 市場機会

- 外科手術件数の増加

- 院内感染予防の需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 特許分析

- ポーター分析

- PESTEL分析

- 消費者行動分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 動脈固定デバイス

- 中心静脈カテーテル固定器具

- 周辺固定装置

- 尿道カテーテル固定装置

- 胸部ドレナージチューブ固定装置

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 心臓血管手術

- 一般外科

- 泌尿器手技

- オンコロジー手技

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 在宅ケア環境

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- B. Braun

- Baxter International

- Becton, Dickinson and Company

- Cardinal Health

- Centurion Medical Products

- ConvaTec

- Dale Medical Products

- DeRoyal Industries

- Merit Medical Systems

- Pepper Medical

- Smiths Medical

- TIDI Products

- VYGON

- Zibo Qichuang Medical Products

- 3M

The Global Catheter Stabilization Devices Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 3.2 billion by 2034. Catheter stabilization devices are essential tools in clinical care, designed to securely anchor various types of catheters to the body, reducing movement, preventing dislodgement, and lowering the risk of migration. This stability not only safeguards the patient but also ensures accurate and uninterrupted delivery of medical treatments. The increasing global prevalence of chronic illnesses such as cancer, kidney failure, diabetes, and cardiovascular conditions is driving the need for long-term catheter use in clinical settings.

In addition, as infection control becomes a growing priority in hospitals, there is an increasing focus on preventing catheter-related infections through improved securement methods. An aging population that frequently requires catheter-based procedures and home care support further contributes to this market's expansion. Fragile skin and susceptibility to infections in older adults heighten the need for secure and comfortable catheter fixation. The demand for high-quality, easy-to-apply stabilization devices is therefore rising rapidly, especially across facilities providing long-term and in-home healthcare services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 7% |

In 2024, the devices segment held a 32.7% share. These catheters are widely applied in intensive care, oncology, and emergency care for critical treatments such as drug administration and nutritional support. With the rise in demand for advanced therapies in these clinical areas, securement devices have become essential in minimizing complications like bloodstream infections, endocarditis, and septic conditions that stem from catheter movement or contamination. To reduce these risks, healthcare institutions and governing bodies have enforced stricter infection control protocols, many of which mandate the use of catheter securement tools. These regulatory shifts are boosting the adoption of securement devices across multiple care settings.

The general surgery segment generated USD 553.5 million in 2024. Catheters are used extensively in surgical procedures for delivering anesthesia, monitoring fluids, and tracking vital signs. Stabilization devices are indispensable in ensuring catheter placement remains intact during surgeries and post-operative care, especially during transitions from operating theaters to recovery areas. Hospitals are under pressure to lower rates of central line-associated bloodstream infections and surgical site infections, which often occur during surgical interventions. This is intensifying the demand for stabilization solutions that align with hospital safety initiatives and improve procedural outcomes.

U.S. Catheter Stabilization Devices Market was valued at USD 667.5 million in 2024 and is expected to reach USD 1.3 billion by 2034. Rising chronic disease cases across the country are driving the need for catheter-based treatments, and in turn, increasing the adoption of stabilization devices. U.S. hospitals follow stringent safety regulations set by various healthcare bodies, which require institutions to use standardized infection control practices. Failure to comply with these safety benchmarks could lead to reduced reimbursement and financial penalties, prompting providers to invest in securement devices. These trends are firmly positioning the U.S. as a key growth region in the global catheter stabilization space.

Companies such as BD, 3M, Cardinal Health, ConvaTec, and B. Braun currently dominate the industry and collectively hold around 65% of the total market share. Leading players in the catheter stabilization devices market are leveraging multiple strategies to boost their presence and secure long-term growth. A primary focus lies in the development of advanced, patient-friendly products that reduce infection risk and enhance application ease.

Companies are strengthening their R&D efforts to deliver innovative designs that cater to specific medical needs and accommodate fragile patient populations, such as the elderly. Geographic expansion through partnerships, local manufacturing, and strategic distribution agreements helps widen access to their product lines. Regulatory compliance is also a major focus, as firms align with evolving clinical standards to increase institutional trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of chronic diseases

- 3.2.1.2 Global aging population

- 3.2.1.3 Continuous innovations in catheter stabilization technology

- 3.2.1.4 Cost-benefits of securement devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative products

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in surgical procedure volume

- 3.2.3.2 Growing demand for preventing hospital acquired infections

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Price trends

- 3.5.1 By region

- 3.5.2 By product

- 3.6 Future market trends

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Arterial securement devices

- 5.3 Central venous catheter securement devices

- 5.4 Peripheral securement devices

- 5.5 Urinary catheters securement devices

- 5.6 Chest drainage tubes securement devices

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular procedures

- 6.3 General surgery

- 6.4 Urological procedures

- 6.5 Oncology procedures

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Home care settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. Braun

- 9.2 Baxter International

- 9.3 Becton, Dickinson and Company

- 9.4 Cardinal Health

- 9.5 Centurion Medical Products

- 9.6 ConvaTec

- 9.7 Dale Medical Products

- 9.8 DeRoyal Industries

- 9.9 Merit Medical Systems

- 9.10 Pepper Medical

- 9.11 Smiths Medical

- 9.12 TIDI Products

- 9.13 VYGON

- 9.14 Zibo Qichuang Medical Products

- 9.15 3M