|

市場調査レポート

商品コード

1773426

肩撃ち兵器の市場機会、成長促進要因、産業動向分析、2025~2034年予測Shoulder Fired Weapons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 肩撃ち兵器の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

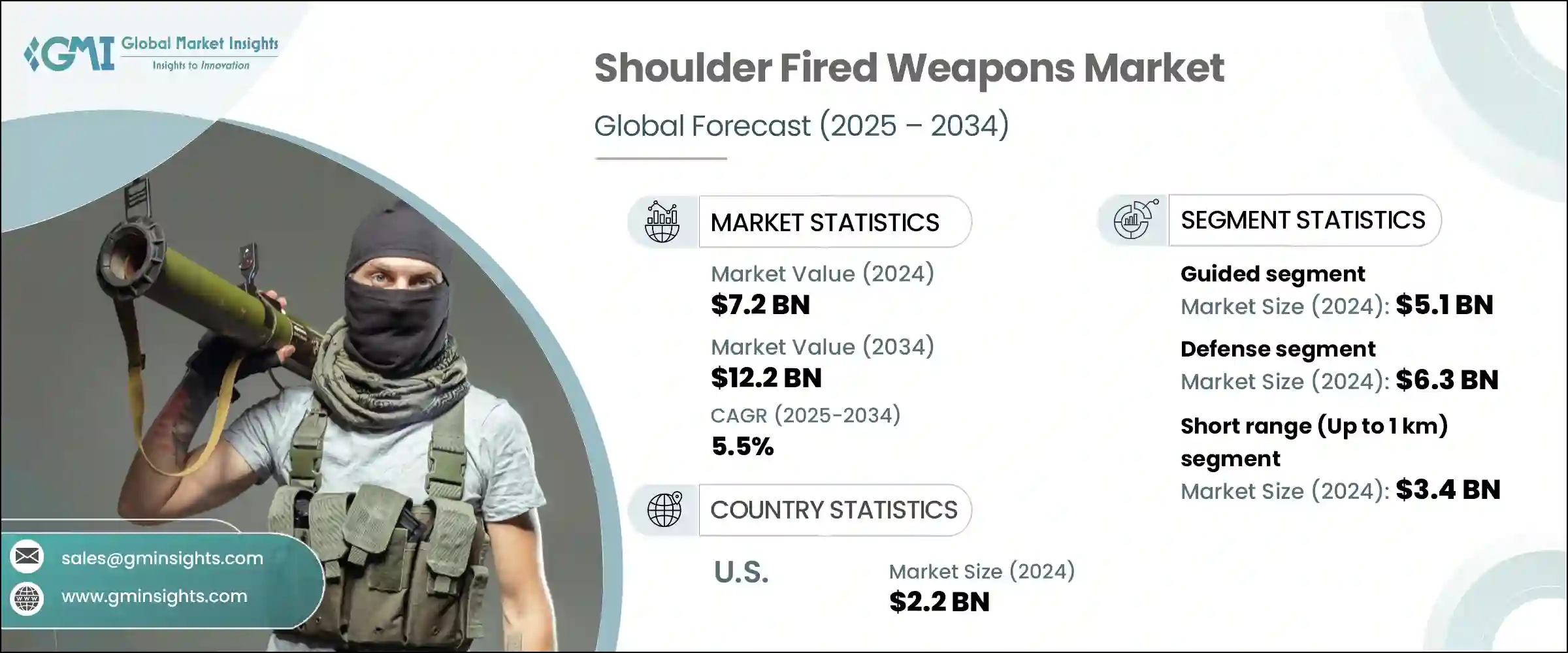

肩撃ち兵器の世界市場規模は、2024年に72億米ドルとなり、CAGR 5.5%で成長し、2034年には122億米ドルに達すると予測されています。

この成長は、主に世界の軍事近代化計画の強化によってもたらされます。地政学的緊張の高まりと国境紛争の進行は、軍隊が手頃な価格で配備可能な戦力増強兵器を求めているため、肩撃ち兵器の需要を大きく促進しています。さまざまな地域での紛争やにらみ合いは、携帯可能で精密な対装甲・対空システムの必要性を高めています。さらに、軍の近代化努力は、市街地や非対称戦シナリオにおける機動性と有効性を高める次世代軽量兵器の開発に重点を置いています。これらのプログラムは、改良された照準や発射重量の軽減といったアップグレードを優先しており、これが先進的な肩部発射ミサイルの需要を促進しています。

世界の戦略的防衛イニシアティブは、人型携帯兵器システムの研究開発に多大な資源を投入し、技術革新を加速させ、能力を拡大しています。この投資は、現代の戦闘シナリオの要求を満たす、より先進的で軽量かつ多用途な肩撃ち兵器の創造に重点を置いています。精度の向上、照準技術の改善、携帯性の向上は、これらの取り組みを推進する重要な優先事項です。軍が多様な作戦環境に適応可能な最先端システムで兵器をアップグレードしようとする中、研究開発への資金は増加の一途をたどっており、市場の拡大に拍車をかけ、兵士の有効性と戦場の敏捷性において新たな基準を設定する画期的な技術を育成しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 72億米ドル |

| 予測金額 | 122億米ドル |

| CAGR | 5.5% |

2024年の市場規模は51億米ドルで、誘導兵器分野が市場を牽引しました。先進的な指揮統制システムなどの包括的な防衛ネットワークに誘導肩火器が統合されたことで、その戦略的重要性が高まっています。これらの兵器は精度、柔軟性、リアルタイムの目標調整能力を提供し、現代の戦場では不可欠なものとなっています。この統合は作戦の有効性を高め、高度な誘導システムに対する需要を刺激し、市場の成長を促進しています。

防衛分野は2024年に63億米ドルを生み出しました。兵士の敏捷性と戦闘効果を高めるため、軽量で展開が容易な兵器へのニーズが高まっており、肩撃ち兵器が最前線に押し上げられています。これらのシステムは、対装甲および対空の役割においてますます重要性を増しており、多用途で正確なソリューションで時代遅れの兵器を置き換えることを目的とした防衛近代化プログラムの中心となっています。通常戦と非正規戦にまたがるその適応性は、さまざまな軍事部門における確固たる地位を確実なものにしています。

米国肩撃ち兵器2024年の市場規模は22億米ドルでした。この市場の成長を後押ししているのは、国防総省による高度な携帯型システムの継続的な調達です。市街地戦闘における兵士の致死性、機動性、能力の強化に重点を置いたプログラムが、肩部発射型対装甲および対構造物兵器の継続的なアップグレードを推進しています。市街戦の準備態勢と配備に対する注目の高まりが需要をさらに支えています。

肩撃ち兵器市場の主要プレーヤーには、Lockheed Martin Corporation、RTX、Saab AB、MBDAが含まれます。肩撃ち兵器市場の企業は、市場での存在感を確固たるものにするために複数の戦略を採用しています。各社は研究開発に多額の投資を行い、進化する戦場のニーズを満たす、より軽量で、より正確な、多機能な兵器を革新しています。

軍事機関との戦略的パートナーシップや協力関係は、主要な契約を確保し、特定の防衛要件に合わせて製品を調整するのに役立ちます。各社はまた、ターゲットを絞ったマーケティングや地域拠点を通じて世界な足跡を拡大し、顧客サポートやアフターサービスを強化することにも注力しています。さらに、多くの企業は、精密誘導や接続機能などの最先端技術を統合して作戦効果を高めることを優先し、自らを現代戦ソリューションのリーダーとして位置づけています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 地政学的緊張と国境紛争の高まり

- 軍事近代化プログラムの強化

- 携帯型軽量兵器の需要増加

- 非対称戦と市街戦シナリオの急増

- 誘導・照準システムにおける技術的進歩

- 業界の潜在的リスク&課題

- 高度なシステムのライフサイクルとメンテナンスコストが高め

- 厳格な輸出管理と規制障壁

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 高度なターゲティングシステムの統合

- 優れた携帯性と軽量素材

- 改良された弾頭と推進能力

- 新興技術

- AI対応の射撃管制システム

- ネットワーク中心の戦争統合

- 指向性エネルギーおよび電磁発射システム

- 現在の技術動向

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- 分野別防衛予算配分

- 人事

- 運用と保守

- 調達

- 調査、開発、試験、評価

- インフラと建設

- テクノロジーとイノベーション

- 持続可能性への取り組み

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021-2024)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:技術別、2021 –2034

- 主要動向

- ガイド付き

- ガイドなし

第6章 市場推計・予測:範囲別、2021 –2034

- 主要動向

- 短距離(1 km未満)

- 中距離(1~2.5 km)

- 長距離(2.5 km以上)

第7章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 防衛

- 対空砲

- 対戦車砲

- その他

- 国土安全保障省

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Daycraft Systems

- Dynamit Nobel Defence GmbH

- Lockheed Martin Corporation

- MBDA

- Nammo AS

- RAFAEL Advanced Defense Systems Ltd.

- Rheinmetall AG

- RTX

- Saab AB

The Global Shoulder Fired Weapons Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 12.2 billion by 2034. This growth is primarily driven by intensified military modernization programs worldwide. Rising geopolitical tensions and ongoing border disputes are significantly fueling demand for shoulder-fired weapons, as armed forces seek affordable, deployable force multipliers. Conflicts and standoffs in various regions have heightened the need for portable, precise anti-armor and anti-air systems. Additionally, military modernization efforts focus on developing next-generation lightweight weapons that enhance mobility and effectiveness in urban and asymmetric warfare scenarios. These programs prioritize upgrades like improved targeting and reduced launch weight, which propel demand for advanced shoulder-fired missiles.

Strategic defense initiatives worldwide are channeling significant resources into the research and development of man-portable weapon systems, accelerating innovation, and expanding capabilities. This investment focuses on creating more advanced, lightweight, and versatile shoulder-fired weapons that meet the demands of modern combat scenarios. Enhanced precision, improved targeting technologies, and greater portability are key priorities driving these efforts. As militaries seek to upgrade their arsenals with cutting-edge systems capable of adapting to diverse operational environments, funding for R&D continues to rise, fueling market expansion and fostering breakthroughs that set new standards in soldier effectiveness and battlefield agility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.5% |

The guided weapons segment led the market in 2024, valued at USD 5.1 billion. The integration of guided shoulder-fired weapons into comprehensive defense networks, such as advanced command and control systems, has elevated their strategic importance. These weapons deliver precision, flexibility, and real-time target adjustment capabilities, making them indispensable on modern battlefields. This integration enhances operational effectiveness and stimulates demand for sophisticated guided systems, driving market growth.

The defense segment generated USD 6.3 billion in 2024. The increasing need for lightweight, easily deployable weaponry to enhance soldier agility and combat effectiveness is pushing shoulder-fired weapons to the forefront. These systems are increasingly vital in anti-armor and anti-air roles and are central to defense modernization programs aiming to replace outdated weaponry with versatile, accurate solutions. Their adaptability across conventional and irregular warfare ensures a solid position within various military branches.

United States Shoulder Fired Weapons Market was valued at USD 2.2 billion in 2024. Growth here is fueled largely by ongoing procurements of advanced portable systems by the Department of Defense. Programs focused on enhancing soldier lethality, mobility, and capabilities in urban combat are driving continuous upgrades in shoulder-fired anti-armor and anti-structure weaponry. Heightened attention to urban warfare readiness and deployment further sustains demand.

Key players in the Shoulder Fired Weapons Market include Lockheed Martin Corporation, RTX, Saab AB, and MBDA. Companies in the shoulder-fired weapons market are adopting multiple strategies to solidify their market presence. They invest heavily in research and development to innovate lighter, more accurate, and multifunctional weapons that meet evolving battlefield needs.

Strategic partnerships and collaborations with military agencies help them secure key contracts and tailor products to specific defense requirements. Firms also focus on expanding their global footprint through targeted marketing and regional offices, enhancing customer support and after-sales services. Moreover, many players prioritize integrating cutting-edge technologies such as precision guidance and connectivity features to improve operational effectiveness, positioning themselves as leaders in modern warfare solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology

- 2.2.2 Range

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising geopolitical tensions and border conflicts

- 3.3.1.2 Increased military modernization programs

- 3.3.1.3 Growing demand for portable and lightweight weaponry

- 3.3.1.4 Surge in asymmetric and urban warfare scenarios

- 3.3.1.5 Technological advancements in guidance and targeting systems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High lifecycle and maintenance costs of advanced systems

- 3.3.2.2 Stringent export controls and regulatory barriers

- 3.3.3 Market opportunities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Integration of advanced targeting systems

- 3.8.1.2 Enhanced portability and lightweight materials

- 3.8.1.3 Improved warhead and propulsion capabilities

- 3.8.2 Emerging technologies

- 3.8.2.1 AI-enabled fire control systems

- 3.8.2.2 Network-centric warfare integration

- 3.8.2.3 Directed energy and electromagnetic launch systems

- 3.8.1 Current technological trends

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Defense budget analysis

- 3.12 Global defense spending trends

- 3.13 Regional defense budget allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key defense modernization programs

- 3.15 Budget forecast (2025-2034)

- 3.15.1 Impact on industry growth

- 3.15.2 Defense budgets by country

- 3.15.3 Defense budget allocation by segment

- 3.15.3.1 Personnel

- 3.15.3.2 Operations and maintenance

- 3.15.3.3 Procurement

- 3.15.3.4 Research, development, test and evaluation

- 3.15.3.5 Infrastructure and construction

- 3.15.3.6 Technology and innovation

- 3.16 Sustainability initiatives

- 3.17 Supply chain resilience

- 3.18 Geopolitical analysis

- 3.19 Workforce analysis

- 3.20 Digital transformation

- 3.21 Mergers, acquisitions, and strategic partnerships landscape

- 3.22 Risk assessment and management

- 3.23 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Guided

- 5.3 Unguided

Chapter 6 Market Estimates and Forecast, By Range, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Short range (up to 1 km)

- 6.3 Medium range (1–2.5 km)

- 6.4 Long range (above 2.5 km)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Defense

- 7.2.1 Anti-aircraft

- 7.2.2 Anti-tank

- 7.2.3 Others

- 7.3 Homeland Security

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Daycraft Systems

- 9.2 Dynamit Nobel Defence GmbH

- 9.3 Lockheed Martin Corporation

- 9.4 MBDA

- 9.5 Nammo AS

- 9.6 RAFAEL Advanced Defense Systems Ltd.

- 9.7 Rheinmetall AG

- 9.8 RTX

- 9.9 Saab AB