医療専門家賠償責任保険市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Medical Professional Liability Insurance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773416

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

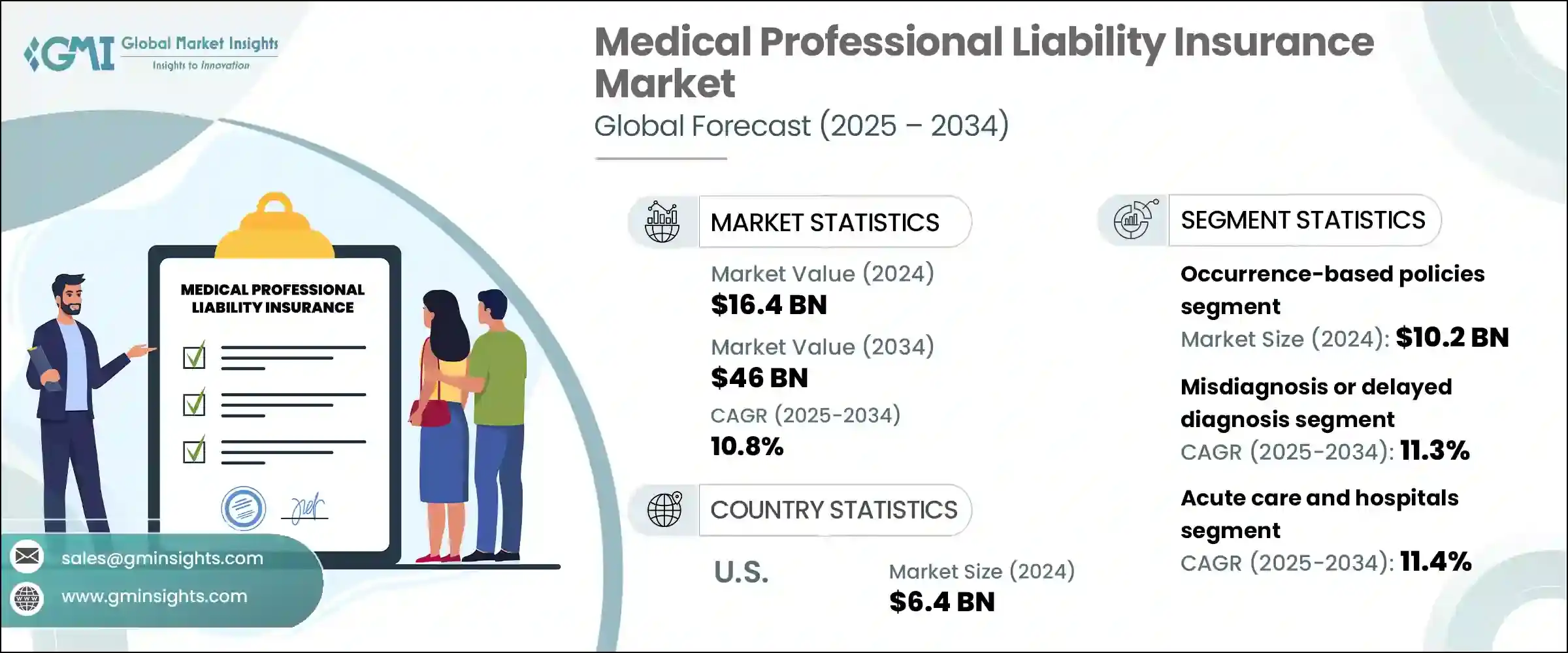

医療専門家賠償責任保険の世界市場規模は、2024年に164億米ドルとなり、CAGR 10.8%で成長し、2034年には460億米ドルに達すると予測されています。

この成長の主な要因は、医療過誤によるクレームの頻度が増加し、ヘルスケア提供者がより強力な保険を求めるようになったことです。加えて、医療従事者が直面するリスクに対する認識が高まり、より良いリスク管理方法を採用するよう促しています。保険会社は、潜在的な問題を予測し、クレームの可能性を減らすのに役立つ高度なデジタル・ツールや分析を提供することで、このシフトに貢献しており、これらの保険は医療提供者にとってさらに魅力的なものとなっています。病院やクリニックがリスク管理により積極的に取り組む中、ヘルスケア業界における安全性と保護への全体的な注目が原動力となり、市場は拡大を続けています。

医療専門家賠償責任保険は、医師や看護師などのヘルスケア・プロバイダーを、標準以下のケアによって損害を受けたと考える患者からの法的請求から保護します。ヘルスケアはますます複雑化し、医療過誤による損害賠償請求は増加の一途をたどっているため、こうした保険商品はキャリアと財政を守るために不可欠なものとなっています。市場はまた、リスクをより効果的に管理し、クレームの発生を未然に防ぐテクノロジーの採用からも恩恵を受けており、業界の成長をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 164億米ドル |

| 予測金額 | 460億米ドル |

| CAGR | 10.8% |

発生ベースの保険が市場で最大のシェアを占め、2024年の市場規模は102億米ドルでした。この分野は、保険金請求がいつ行われたかにかかわらず、保険期間中に発生した事故による保険金請求から医療従事者を保護する包括的な補償が支持されています。この長期的な保障は、安心感を求める医療従事者にとって特に価値があります。これらの保険は、保険金請求型の保険に比べ、より信頼性が高く、補償範囲が広いため、特にリスクの高い医療専門分野で高い人気を誇っています。

誤診または診断の遅れを扱う分野は2024年に最大のシェアを占め、2034年までCAGR 11.3%で成長すると予想されます。誤診や診断の遅れは、最も一般的で費用のかかる過誤の一つであり、患者に深刻な結果をもたらすケースも多いです。このような請求は多額の和解金や訴訟手続きの長期化につながる可能性が高く、保険会社の中心的な焦点となっています。この動向は、タイムリーで正確な診断が不可欠な腫瘍学、心臓病学、救急医療などの専門分野で特に顕著です。

米国医療専門家賠償責任保険2024年の市場規模は64億米ドル。米国は、その複雑な法的環境、広大なヘルスケア・インフラ、医療サービスの利用頻度の高さから、依然としてこの市場の支配的プレイヤーです。特に手術や産科のようなリスクの高い分野での訴訟の増加が、賠償責任保険の需要を押し上げています。米国のヘルスケアプロバイダーは、医療過誤訴訟による経済的リスクの増大から自らを守るための保険を求めるようになっています。

市場ポジションを強化するため、医療専門家賠償責任保険セクターの各社は、様々な専門分野の医療従事者の具体的なニーズを満たす、よりテーラーメイドで柔軟性の高い保険を導入することで、商品ラインナップの拡充に注力しています。参考資料の多くは、データ分析や機械学習を利用してリスクを予測・軽減し、保険契約をより効果的で魅力的なものにするデジタル・ツールに多額の投資を行っています。さらに、各社は顧客基盤を拡大し、顧客エンゲージメントを向上させるため、ヘルスケア機関と戦略的パートナーシップを結んでいます。リスク管理ソリューションと顧客体験の向上に注力することで、保険会社は競争が激化する市場でより強固な足場を確保しつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 医療過誤訴訟の増加

- 意識の高まりとリスク管理の取り組み

- ヘルスケア技術の導入拡大

- 専門業務の範囲の拡大

- 業界の潜在的リスク&課題

- 高額な保険料

- 新興経済諸国における認識の低さ

- 市場機会

- 保険金請求額の増加による再保険と超過補償の機会

- カスタマイズ可能なバンドルポリシーの需要の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 発生ベースのポリシー

- クレームベースのポリシー

第6章 市場推計・予測:請求タイプ別、2021年~2034年

- 主要動向

- 誤診または診断の遅れ

- 出産時の損傷

- 投薬ミス

- 外科手術のミス

- その他の請求タイプ

第7章 市場推計・予測:ヘルスケア分野別、2021年~2034年

- 主要動向

- 急性期ケアと病院

- 長期ケア

- 外来診療

- メンタルヘルスと行動ヘルス

- その他のヘルスケア分野

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- エージェントとブローカー

- 直接的回答

- 銀行

- その他の流通チャネル

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AXA

- Allianz

- Beazley Group

- Berkshire Hathaway Specialty Insurance

- Chubb

- CNA Financial

- CoverWallet

- Coverys

- Hiscox

- Ignyte Insurance

- Liberty Mutual Group

- MagMutual LLC

- ProAssurance Group

- The Doctors Company

- Tokio Marine HCC

目次

The Global Medical Professional Liability Insurance Market was valued at USD 16.4 billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 46 billion by 2034. This growth is primarily driven by the increasing frequency of medical malpractice claims, which has led healthcare providers to seek stronger insurance coverage. Additionally, there is a rise in awareness about the risks healthcare professionals face, which is pushing them to adopt better risk management practices. Insurance companies are contributing to this shift by offering advanced digital tools and analytics that help predict potential issues and reduce the chances of claims, making these policies even more attractive to healthcare providers. With hospitals and clinics taking more proactive steps to manage risks, the market continues to expand, driven by an overall focus on safety and protection in the healthcare industry.

Medical professional liability insurance protects healthcare providers, such as doctors and nurses, against legal claims made by patients who believe they were harmed due to substandard care. As healthcare becomes increasingly complex and malpractice claims continue to rise, these insurance products have become crucial for safeguarding careers and finances. The market is also benefiting from the adoption of technology to manage risks more effectively and prevent claims from occurring in the first place, thus further driving growth in the industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.4 Billion |

| Forecast Value | $46 Billion |

| CAGR | 10.8% |

Occurrence-based policies accounted for the largest share of the market, valued at USD 10.2 billion in 2024. This segment is favored for its comprehensive coverage, which protects healthcare providers against claims resulting from incidents that happened during the policy period, regardless of when the claim is made. This long-term protection is especially valuable for medical professionals who seek peace of mind. These policies are highly popular, especially in high-risk medical specialties, because they offer more reliable and extended coverage compared to claims-made policies.

The segment dealing with misdiagnosis or delayed diagnosis represented the largest share in 2024 and is expected to grow at a CAGR of 11.3% through 2034. Misdiagnosis or delayed diagnosis is one of the most common and costly forms of malpractice, with cases often involving serious consequences for patients. These claims are more likely to result in significant settlements and prolonged legal proceedings, making them a central focus for insurers. This trend is particularly notable in specialties such as oncology, cardiology, and emergency medicine, where timely and accurate diagnosis is essential.

United States Medical Professional Liability Insurance Market was valued at USD 6.4 billion in 2024. The U.S. remains the dominant player in this market due to its complex legal environment, vast healthcare infrastructure, and high frequency of medical services utilization. Increased litigation, particularly in high-risk areas like surgery and obstetrics, is driving the demand for liability insurance. Healthcare providers in the U.S. are increasingly seeking policies to protect themselves from growing financial risks posed by malpractice suits.

Key players in the Medical Professional Liability Insurance Market include Berkshire Hathaway Specialty Insurance, AXA, Allianz, ProAssurance Group, Coverys, Beazley Group, The Doctors Company, CNA Financial, Tokio Marine HCC, Liberty Mutual Group, Chubb, MagMutual LLC, Ignyte Insurance, CoverWallet, Hiscox. To strengthen their market position, companies in the medical professional liability insurance sector are focusing on expanding their product offerings by introducing more tailored and flexible policies that meet the specific needs of healthcare professionals in various specialties. Many are investing heavily in digital tools that use data analytics and machine learning to predict and mitigate risks, making insurance policies more effective and attractive. Furthermore, companies are forming strategic partnerships with healthcare organizations to expand their client base and improve customer engagement. By focusing on risk management solutions and improving the customer experience, insurers are securing a stronger foothold in an increasingly competitive market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Claim type

- 2.2.4 Healthcare sector

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of medical malpractice claims

- 3.2.1.2 Growing awareness and risk management initiatives

- 3.2.1.3 Increasing healthcare technology adoption

- 3.2.1.4 Expanding scope of professional practice

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High premium cost

- 3.2.2.2 Limited awareness in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Opportunities in reinsurance and excess coverage due to rising claim severity

- 3.2.3.2 Growing demand for customizable and bundled policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Occurrence-based policies

- 5.3 Claims-based policies

Chapter 6 Market Estimates and Forecast, By Claim Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Misdiagnosis or delayed diagnosis

- 6.3 Childbirth injuries

- 6.4 Medication errors

- 6.5 Surgical errors

- 6.6 Other claim types

Chapter 7 Market Estimates and Forecast, By Healthcare Sector, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Acute care and hospitals

- 7.3 Long-term care

- 7.4 Ambulatory and outpatient care

- 7.5 Mental health and behavioral health

- 7.6 Other healthcare sectors

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Agents and brokers

- 8.3 Direct response

- 8.4 Banks

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AXA

- 10.2 Allianz

- 10.3 Beazley Group

- 10.4 Berkshire Hathaway Specialty Insurance

- 10.5 Chubb

- 10.6 CNA Financial

- 10.7 CoverWallet

- 10.8 Coverys

- 10.9 Hiscox

- 10.10 Ignyte Insurance

- 10.11 Liberty Mutual Group

- 10.12 MagMutual LLC

- 10.13 ProAssurance Group

- 10.14 The Doctors Company

- 10.15 Tokio Marine HCC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日