胸腰椎固定用インプラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Thoracolumbar Spinal Fusion Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773414

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

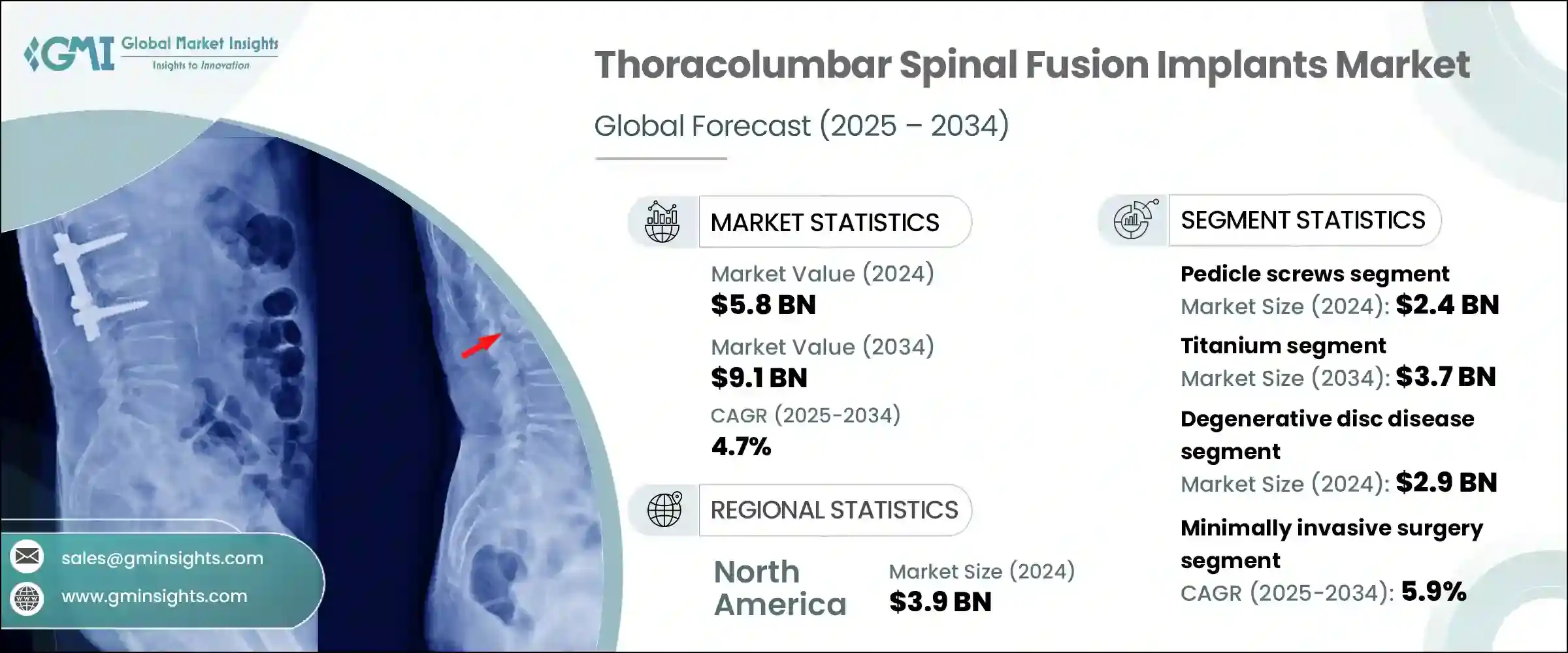

世界の胸腰椎固定用インプラント市場は、2024年に58億米ドルと評価され、CAGR 4.7%で成長し、2034年には91億米ドルに達すると推定されています。

市場拡大の原動力となっているのは、脊椎疾患の有病率の増加、交通事故による傷害の急増、低侵襲手術ソリューションへの関心の高まりです。外傷症例、変性疾患、先天性奇形における脊椎安定化に対する需要の高まりが、病院や外科センター全体における脊椎固定術の取り込みを大幅に後押ししています。世界の高齢者人口の増加に伴い、加齢に伴う脊椎合併症、特に胸腰椎領域の合併症の頻度は増加の一途をたどっており、固定インプラントの採用が拡大しています。

さらに、手術方法の改善や、侵襲性の低いアプローチを好む患者の嗜好が、特に新興ヘルスケアシステムにおいて、この動向を後押ししています。医療関係者は、回復時間の短縮と合併症の減少を求め、長期的な脊椎支持を提供しながら組織損傷を最小限に抑える手術用インプラントの技術革新に注目しています。全体として、臨床上の必要性、人口動態の高齢化、技術の進歩、外傷発生率の増加が相まって、市場は世界的に安定した成長に向かっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 58億米ドル |

| 予測金額 | 91億米ドル |

| CAGR | 4.7% |

2024年の胸腰椎固定用インプラント市場は、ペディクルスクリューが24億米ドルの評価額で圧倒的なシェアを占めています。その構造的強度と硬い3次元脊椎支持能力により、椎体骨折の安定化、アライメント問題の修正、椎間板圧の緩和のための有力な選択肢となっています。その有用性は、確実な固定が重要である胸腰椎手術においてさらに高まる。

外科医は、特に外傷や変形矯正症例など、高い精度と長時間の支持を必要とする手術に、これらのシステムを好んで使用しています。より低侵襲な手技が採用されるようになり、新しい世代のペディクル・スクリューには、多軸ヘッド、カニューレ型シャフト、拡張可能なバージョンなどの高度な構成が含まれるようになりました。これらの機能強化は、術中の効率、外科医のコントロール、様々な脊椎解剖への適応性を向上させており、これら全てが臨床結果を高め、手術の成功を後押ししています。

チタンセグメントは2034年までに37億米ドルに達すると思われます。チタンとその合金、特にTi-6Al-4Vは、高強度、生体適合性、耐食性という理想的な組み合わせにより、脊椎固定用インプラントの材料として好まれるようになっています。チタンは人体組織との適合性が高いため、長期的な癒合を達成するために不可欠な骨統合を迅速に行うことができます。その弾性率は人骨の弾性率に酷似しているため、応力の遮蔽が少なく、インプラントのゆるみや隣接セグメント疾患などの合併症を最小限に抑えることができます。さらに、MRIやCTスキャンなどの画像診断技術との適合性により、その臨床的有用性がさらに高まっています。

米国の胸腰椎固定用インプラント市場は、2024年に36億米ドルと評価されました。この成長は、手術件数の多さ、最先端の手術技術の利用可能性、有利な保険償還政策に起因しています。脊柱管狭窄症、脊椎すべり症、椎間板変性症を患う高齢者人口の増加が、引き続き手術需要を促進しています。加えて、ロボット工学とナビゲーション・システムが脊椎手術のワークフローに統合されたことで、固定術の精度が向上し、インプラントの需要が増加しています。低侵襲手技における拡張可能ケージや経皮的スクリューシステムの幅広い使用が、市場規模をさらに押し上げています。Globus Medical社やMedtronic社のような主要企業は、継続的な製品革新、外科医教育プログラム、広範な販売提携を通じて、米国市場で強い存在感を維持しています。

世界の胸腰椎固定用インプラント市場を形成している有力企業には、Highridge Medical(ZimVie)、B. Braun、Spineart、Orthofix Medical、DePuy Synthes(JnJ)、Ulrich、JAYON、Alphatec Spine、Medtronic、Stryker(VB Spine)、RTI Surgical、Globus Medical、WASTON MEDICAL、GS Medicalなどがあります。これらの企業は、手術ポートフォリオの拡大、インプラント技術の向上、多様な患者ニーズへの対応において極めて重要な役割を果たしています。

胸腰椎固定用インプラント市場の各社は、市場でのポジショニングを強化するため、積極的な技術革新、製品開発、世界展開を進めています。主要企業は、低侵襲手術をサポートし、患者の多様な解剖学的構造に対応する先進的なインプラントシステムの設計に投資しています。カスタマイズ性、モジュール性、適応性は、優先される製品の中核機能です。各社はまた、製品を改良し臨床的有効性を確保するために、外科医と協力して臨床試験や実臨床でのエビデンスを作成しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 脊椎疾患の有病率の上昇

- 低侵襲手術の需要増加

- 技術的進歩

- 有利な償還ポリシー

- 業界の潜在的リスク&課題

- 脊椎インプラントと手術の高額な費用

- 厳しい規制シナリオ

- 機会

- 脊椎手術におけるAIとロボットの統合

- 外来診療と通院診療への注目が高まる

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 製品別の価格動向

- 将来の市場動向

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 椎弓根スクリュー

- 椎間体固定装置(IBFD)

- ロッド

- プレート

- その他の製品タイプ

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- チタン

- ポリエーテルエーテルケトン(PEEK)

- コバルトクロム

- ステンレス鋼

- その他の材料

第7章 市場推計・予測:手術の種類別、2021年~2034年

- 主要動向

- 開腹手術

- 低侵襲手術

第8章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 変性椎間板疾患

- 脊椎外傷

- 脊椎変形

- 脊椎腫瘍

- その他の適応症

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 整形外科クリニック

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Alphatec Spine

- B. Braun

- DePuy Synthes(JnJ)

- Globus Medical

- GS Medical

- Highridge Medical(ZimVie)

- JAYON

- Medtronic

- Orthofix Medical

- RTI Surgical

- Spineart

- Stryker(VB Spine)

- Ulrich

- WASTON MEDICAL

目次

The Global Thoracolumbar Spinal Fusion Implants Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 9.1 billion by 2034. Market expansion is being driven by the increasing prevalence of spinal conditions, a surge in road-related injuries, and rising interest in minimally invasive surgical solutions. Growing demand for spinal stabilization in trauma cases, degenerative disorders, and congenital deformities has significantly boosted the uptake of spinal fusion procedures across hospitals and surgical centers. As the global elderly population rises, the frequency of age-associated spine complications-particularly in the thoracolumbar region-continues to grow, leading to greater adoption of fusion implants.

Furthermore, improvements in surgical methods and patient preference for less invasive approaches are supporting this trend, especially in emerging healthcare systems. As medical professionals seek faster recovery times and fewer complications, they're turning to innovations in surgical implants that minimize tissue damage while providing long-term spinal support. Overall, the combination of clinical necessity, aging demographics, technological advancement, and growing trauma incidence is pushing the market toward consistent growth globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 4.7% |

In 2024, pedicle screws dominated the thoracolumbar spinal fusion implants market with a total valuation of USD 2.4 billion. Their structural strength and ability to provide rigid three-dimensional spinal support make them the go-to option for stabilizing vertebral fractures, correcting alignment issues, or relieving disc pressure. Their utility is amplified in thoracolumbar surgeries, where secure fixation is critical.

Surgeons prefer these systems for procedures that demand high precision and long-lasting support, especially in trauma and deformity correction cases. With more minimally invasive techniques being adopted, newer generations of pedicle screws now include advanced configurations such as polyaxial heads, cannulated shafts, and expandable versions. These enhancements are improving intraoperative efficiency, surgeon control, and adaptability to varying spinal anatomies-all of which are enhancing clinical outcomes and boosting procedural success.

The titanium segment will reach USD 3.7 billion by 2034. Titanium and its alloys, especially Ti-6Al-4V, have become the preferred material choice for spinal fusion implants due to their ideal combination of high strength, biocompatibility, and corrosion resistance. Titanium's compatibility with human tissue enables quicker bone integration, which is vital for achieving long-term fusion. Its elastic modulus closely resembles that of human bone, reducing stress shielding and minimizing complications like implant loosening or adjacent segment disease. Moreover, its compatibility with diagnostic imaging technologies, including MRI and CT scans, further enhances its clinical desirability.

United States Thoracolumbar Spinal Fusion Implants Market was valued at USD 3.6 billion in 2024. This growth can be attributed to high surgical volumes, cutting-edge surgical technology availability, and favorable insurance reimbursement policies. A growing elderly population experiencing spinal stenosis, spondylolisthesis, and degenerative disc issues continues to fuel procedural demand. In addition, the integration of robotics and navigation systems into spinal surgery workflows has improved the precision of fusion procedures, thereby increasing the demand for implants. The broader use of expandable cages and percutaneous screw systems in minimally invasive techniques further boost market volume. Leading companies like Globus Medical and Medtronic maintain a strong market presence in the U.S. through continued product innovation, surgeon education programs, and wide-reaching distribution partnerships.

Prominent players shaping the Global Thoracolumbar Spinal Fusion Implants Market include Highridge Medical (ZimVie), B. Braun, Spineart, Orthofix Medical, DePuy Synthes (JnJ), Ulrich, JAYON, Alphatec Spine, Medtronic, Stryker (VB Spine), RTI Surgical, Globus Medical, WASTON MEDICAL, and GS Medical. These companies play pivotal roles in expanding surgical portfolios, improving implant technologies, and addressing diverse patient needs.

Companies in the thoracolumbar spinal fusion implants market are pursuing aggressive innovation, product development, and global expansion to strengthen their market positioning. Major players are investing in the design of advanced implant systems that support minimally invasive procedures and accommodate varying patient anatomies. Customization, modularity, and adaptability are core product features being prioritized. Firms are also collaborating with surgeons for clinical trials and real-world evidence generation to refine products and ensure clinical efficacy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates & calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Surgery type

- 2.2.5 Indication

- 2.2.6 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pedicle screws

- 5.3 Intervertebral body fusion device (IBFD)

- 5.4 Rods

- 5.5 Plates

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Cobalt chrome

- 6.5 Stainless steel

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal trauma

- 8.4 Spinal deformities

- 8.5 Spinal tumors

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 DePuy Synthes (JnJ)

- 11.4 Globus Medical

- 11.5 GS Medical

- 11.6 Highridge Medical (ZimVie)

- 11.7 JAYON

- 11.8 Medtronic

- 11.9 Orthofix Medical

- 11.10 RTI Surgical

- 11.11 Spineart

- 11.12 Stryker (VB Spine)

- 11.13 Ulrich

- 11.14 WASTON MEDICAL

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日