|

市場調査レポート

商品コード

1773406

タイル用接着剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Tile Adhesive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| タイル用接着剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

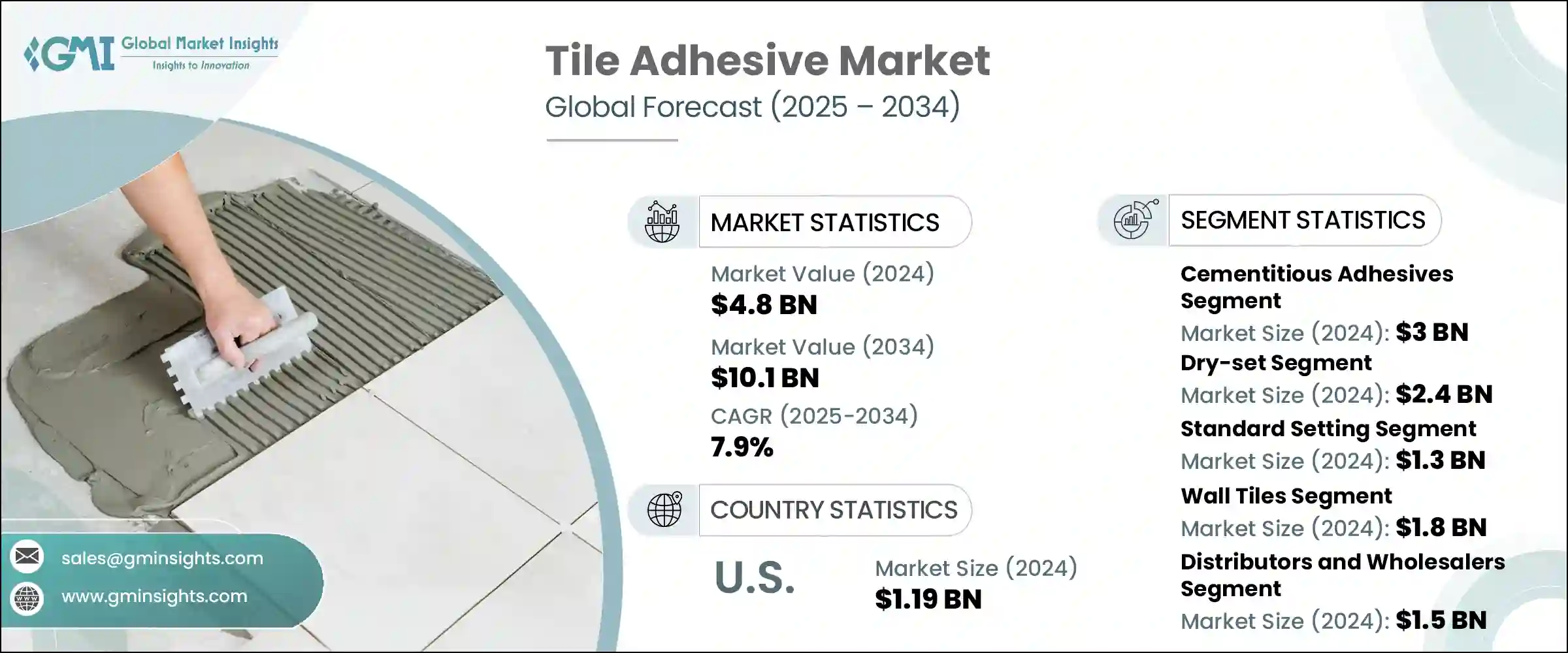

タイル用接着剤の世界市場規模は、2024年に48億米ドルとなり、CAGR 7.9%で成長し、2034年には101億米ドルに達すると予測されています。

この成長は、開発途上地域と先進地域の両方で建設活動が活発化していることに強く影響されています。都市インフラが拡大し、新しい商業・住宅プロジェクトが着工されるにつれて、高性能で時間を節約できる建材への需要が高まり続けています。タイル用接着剤は、その優れた接着強度、施工の容易さ、効率の良さから、従来のセメント系ソリューションに取って代わりつつあります。特に中東やアジア太平洋の急成長地域における大規模な都市化の取り組みにより、これらの製品は近代的な建築手法に不可欠なものとなっています。

米国と欧州では、特に老朽化した物件の住宅改修やリフォームの急増も需要に寄与しています。改築プロジェクトでは、湿気に対する耐性と様々な材料との適合性により、キッチン、バスルーム、および通行量の多い内装でタイル接着剤の使用が増加しています。さらに、接着剤の配合、特にポリマーの革新により、乾燥時間の短縮、柔軟性の向上、耐熱性の改善など、より軽量な製品が生み出されています。こうした進歩は、施工時間や材料の無駄を減らすだけでなく、施工時のエネルギー消費を抑えることで環境目標もサポートしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 101億米ドル |

| CAGR | 7.9% |

2024年、セメント系接着剤セグメントは30億米ドルを生み出し、2034年までの予測CAGRは7.1%で力強い成長を維持すると予想されます。これらの接着剤は、その費用対効果、耐久性、および商業と住宅の両方の建設のための適応性のために好ましい選択肢であり続けています。開発途上国で広く使用されているのは、その手頃な価格と実証済みの強度を反映しています。ポリマー変性変異体は、大判タイルや湿気が発生しやすい領域を含むインストール用に強化された性能を提供し、ますます一般的になってきました。柔軟性と耐水性が向上したことで、現代の建築用途に理想的なものとなっています。建設工法がより厳しい性能基準を満たすように進化するにつれて、これらのアップグレードされたセメント系接着剤は、複数のプロジェクトタイプや地域市場にわたって支配的な役割を確保しつつあります。

標準硬化性接着剤セグメントは、2024年に13億米ドルで評価され、2034年の間に5.9%のCAGRで成長すると予想されています。標準硬化性接着剤と速硬化性接着剤の選択は、プロジェクトの性質と必要なスケジュールに大きく依存します。スケジュールが許す一般的な建設では、強力な接着力と十分な作業時間を提供するため、標準硬化性接着剤が広く使用されています。しかし、商業施設の改修や公共施設のアップグレードなど、一刻を争う環境では、完成を早め、ダウンタイムを短縮できる速硬化性接着剤が好まれます。商業スペースや小売店では、操業の中断を最小限に抑えることが求められることが多いため、高性能の速硬化性接着剤の需要は今後も増え続けるでしょう。

米国のタイル用接着剤2024年の市場規模は11億9,000万米ドルで、2034年まで7.6%のCAGRで成長すると予想されています。この拡大には、持続可能な建築慣行を重視する国民性と相まって、住宅および商業施設の建設活動が増加していることが寄与しています。古い建物の更新や建て替えが進むにつれて、効率的で環境に配慮した接着剤製品に対する需要が高まっています。米国の消費者は、インテリアの見栄えを良くするだけでなく、長持ちする耐久性を備えた製品に高い価値を置くようになっています。このシフトは、メーカーがグリーン建設イニシアティブに合わせながら、現代の性能基準を満たす高度で環境に優しい接着剤にもっと焦点を当てることを後押ししています。

世界のタイル用接着剤市場における競合情勢は、Ardex Group、Sika AG、Laticrete International, Inc.、Saint-Gobain Weber、Mapei S.p.A.などの大手企業によって形成されています。これらの企業は、製品開発と市場開拓に一貫した投資を行っていることで知られています。

タイル用接着剤市場の主要企業は、技術革新、提携、地域拡大を織り交ぜながら、市場への足場固めに積極的に取り組んでいます。製品開発は最優先課題であり、多くの企業が耐久性、耐水性、柔軟性に優れた高度なポリマー変性接着剤に投資しています。このような新しい配合は、軽量タイルや湿気の多い場所での施工など、近代的な建築要件に合わせて調整されることが多いです。これと並行して、企業は請負業者や販売業者と戦略的パートナーシップを結ぶことで、世界の販売網を強化しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:化学タイプ別、2021年~2034年

- 主要動向

- セメント系接着剤

- 標準セメント質(C1)

- 改良セメント質(C2)

- 速硬化セメント質

- その他

- 分散接着剤

- 標準分散(D1)

- 分散の改善(D2)

- その他

- 反応樹脂接着剤

- エポキシベース

- ポリウレタンベース

- その他

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 乾式

- RTU(Ready-to-Use)

- 2成分

- その他

第7章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 標準

- 速乾

- 柔軟/変形可能

- 防滑性

- 耐水性

- 耐霜性

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 壁タイル

- 内壁

- 外壁

- その他

- 床タイル

- 内装床

- 外装床

- その他

- シーリング

- プールと湿地帯

- その他

第9章 市場推計・予測:タイルタイプ別、2021年~2034年

- 主要動向

- セラミックタイル

- 磁器タイル

- 天然石タイル

- 大理石

- 花崗岩

- スレート

- その他

- ガラスタイル

- モザイクタイル

- 大型タイル

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 新築

- 改修と改装

- その他

- 商業用

- オフィスビル

- 小売スペース

- ホスピタリティ

- ヘルスケア施設

- 教育機関

- その他

- 産業

- 製造施設

- 倉庫

- その他

- 機関

- 政府庁舎

- 宗教施設

- その他

- その他

第11章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 販売業者および卸売業者

- ホームセンター

- 専門店

- オンライン小売

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第13章 企業プロファイル

- Sika AG

- Mapei S.p.A.

- Ardex Group

- Laticrete International, Inc.

- Saint-Gobain Weber

- H.B. Fuller Company

- Bostik SA(Arkema Group)

- Henkel AG &Co. KGaA

- Pidilite Industries Ltd.

- Wacker Chemie AG

- Custom Building Products

- Parex Group(Sika AG)

- Fosroc International Ltd.

- Kerakoll S.p.A.

- 3M Company

The Global Tile Adhesive Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 10.1 billion by 2034. This growth is strongly influenced by rising construction activity across both developing and developed regions. As urban infrastructure expands and new commercial and residential projects break ground, demand for high-performance, time-saving building materials continues to rise. Tile adhesives are rapidly replacing conventional cement-based solutions due to their superior bond strength, easier application, and efficiency. Large urbanization efforts, especially in fast-growing areas across the Middle East and Asia-Pacific, have made these products essential for modern building practices.

In the U.S. and Europe, a surge in home improvement and remodeling efforts, particularly in aging properties, is also contributing to demand. Renovation projects are increasingly using tile adhesives in kitchens, bathrooms, and high-traffic interiors due to their resistance to moisture and their compatibility with a range of materials. Additionally, innovation in adhesive formulations-especially with polymers-has resulted in lighter products with faster drying times, enhanced flexibility, and improved thermal resistance. These advancements not only reduce installation time and material waste but also support environmental goals by lowering energy use during application.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 7.9% |

In 2024, the cementitious adhesives segment generated USD 3 billion and is expected to maintain strong growth with a projected CAGR of 7.1% through 2034. These adhesives remain a preferred choice due to their cost-effectiveness, durability, and adaptability for both commercial and residential construction. Their widespread use in developing nations reflects their affordability and proven strength. Polymer-modified variants have become increasingly common, offering enhanced performance for installations involving large-format tiles or moisture-prone areas. Their improved flexibility and water resistance make them ideal for modern building applications. As construction methods evolve to meet more demanding performance criteria, these upgraded cementitious adhesives are securing a dominant role across multiple project types and geographic markets.

The standard-setting adhesives segment was valued at USD 1.3 billion in 2024 and is expected to grow at a CAGR of 5.9% during 2034. The choice between standard and fast-setting adhesives depends heavily on the nature of the project and the required timelines. For typical construction where schedules allow, standard-setting adhesives are widely used because they provide strong adhesion and ample working time. However, in time-sensitive environments-such as commercial refurbishments or public facility upgrades-fast-setting adhesives are preferred for their ability to expedite completion and reduce downtime. As commercial spaces and retail outlets often demand minimal operational disruption, the demand for high-performance, quick-curing adhesives will continue to rise.

United States Tile Adhesive Market was valued at USD 1.19 billion in 2024 and is expected to grow at a CAGR of 7.6% through 2034. This expansion is fueled by increasing residential and commercial construction activity, coupled with a national emphasis on sustainable building practices. As older buildings are updated and replaced, there is a growing demand for efficient, environmentally conscious adhesive products. U.S. consumers are placing a higher value on products that not only enhance the appearance of interiors but also offer long-lasting durability. This shift is pushing manufacturers to focus more on advanced, eco-friendly adhesives that meet modern performance standards while aligning with green construction initiatives.

The competitive landscape in the Global Tile Adhesive Market is shaped by major players such as Ardex Group, Sika AG, Laticrete International, Inc., Saint-Gobain Weber, and Mapei S.p.A. These companies are known for their consistent investment in product development and market expansion.

Leading companies in the tile adhesive market are actively working to strengthen their market foothold through a mix of innovation, partnerships, and regional expansion. Product development is a top priority, with many firms investing in advanced polymer-modified adhesives that offer greater durability, water resistance, and flexibility. These new formulations are often tailored for modern building requirements, including lightweight tiles and wet-area installations. In parallel, companies are enhancing their global distribution networks by forming strategic partnerships with contractors and distributors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemical Type

- 2.2.3 Type

- 2.2.4 Feature

- 2.2.5 Application

- 2.2.6 Tile Type

- 2.2.7 End Use Sector

- 2.2.8 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Chemical Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cementitious Adhesives

- 5.2.1 Standard Cementitious (C1)

- 5.2.2 Improved Cementitious (C2)

- 5.2.3 Fast-Setting Cementitious

- 5.2.4 Others

- 5.3 Dispersion Adhesives

- 5.3.1 Standard Dispersion (D1)

- 5.3.2 Improved Dispersion (D2)

- 5.3.3 Others

- 5.4 Reaction Resin Adhesives

- 5.4.1 Epoxy-Based

- 5.4.2 Polyurethane-Based

- 5.4.3 Others

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry-Set

- 6.3 Ready-to-Use

- 6.4 Two-Component

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Feature, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Standard Setting

- 7.3 Fast Setting

- 7.4 Flexible/Deformable

- 7.5 Slip-Resistant

- 7.6 Water-Resistant

- 7.7 Frost-Resistant

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Wall Tiles

- 8.2.1 Interior Walls

- 8.2.2 Exterior Walls

- 8.2.3 Others

- 8.3 Floor Tiles

- 8.3.1 Interior Floors

- 8.3.2 Exterior Floors

- 8.3.3 Others

- 8.4 Ceiling

- 8.5 Swimming Pools and Wet Areas

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Tile Type, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Ceramic Tiles

- 9.3 Porcelain Tiles

- 9.4 Natural Stone Tiles

- 9.4.1 Marble

- 9.4.2 Granite

- 9.4.3 Slate

- 9.4.4 Others

- 9.5 Glass Tiles

- 9.6 Mosaic Tiles

- 9.7 Large Format Tiles

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By End Use Sector, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Residential

- 10.2.1 New Construction

- 10.2.2 Renovation and Remodeling

- 10.2.3 Others

- 10.3 Commercial

- 10.3.1 Office Buildings

- 10.3.2 Retail Spaces

- 10.3.3 Hospitality

- 10.3.4 Healthcare Facilities

- 10.3.5 Educational Institutions

- 10.3.6 Others

- 10.4 Industrial

- 10.4.1 Manufacturing Facilities

- 10.4.2 Warehouses

- 10.4.3 Others

- 10.5 Institutional

- 10.5.1 Government Buildings

- 10.5.2 Religious Buildings

- 10.5.3 Others

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 Direct Sales

- 11.3 Distributors and Wholesalers

- 11.4 Home Improvement Stores

- 11.5 Specialty Stores

- 11.6 Online Retail

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 Sika AG

- 13.2 Mapei S.p.A.

- 13.3 Ardex Group

- 13.4 Laticrete International, Inc.

- 13.5 Saint-Gobain Weber

- 13.6 H.B. Fuller Company

- 13.7 Bostik SA (Arkema Group)

- 13.8 Henkel AG & Co. KGaA

- 13.9 Pidilite Industries Ltd.

- 13.10 Wacker Chemie AG

- 13.11 Custom Building Products

- 13.12 Parex Group (Sika AG)

- 13.13 Fosroc International Ltd.

- 13.14 Kerakoll S.p.A.

- 13.15 3M Company