|

市場調査レポート

商品コード

1773403

外科手術用縫合糸市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Surgical Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 外科手術用縫合糸市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月20日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

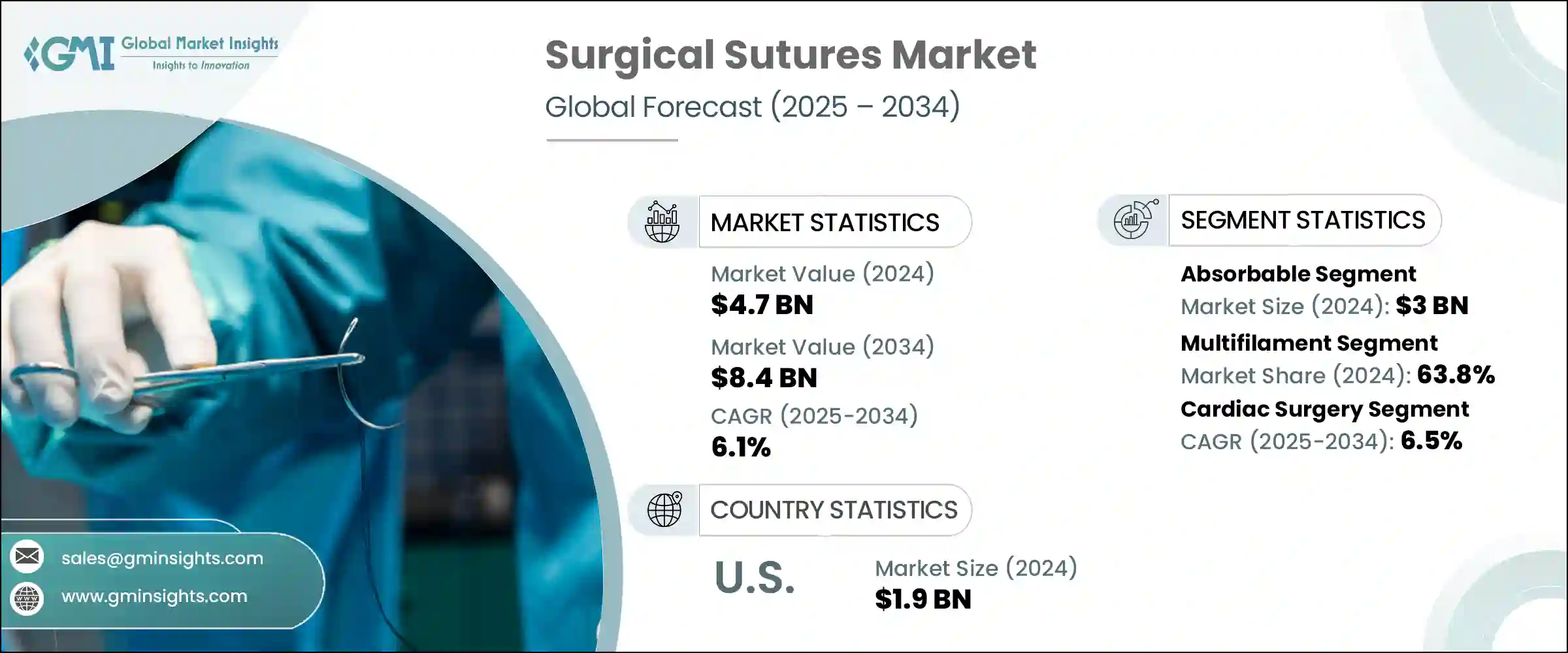

外科手術用縫合糸の世界市場規模は2024年に47億米ドルとなり、CAGR 6.1%で成長し、2034年には84億米ドルに達すると推定されます。

市場成長の原動力となっているのは、高齢者人口の増加と、整形外科手術や腹部手術など高齢化に関連した手術件数の増加です。糖尿病、心血管障害、肥満などの慢性疾患が世界的に増加の一途をたどっているため、外科手術の需要も増加し、縫合糸の必要性を直接煽っています。次世代手術器具の入手可能性は、低侵襲手術への傾向の高まりと相まって、業界の技術革新を加速させています。

合成吸収性材料の進歩も創傷管理のあり方を変えています。病院や手術センターは、手術件数の増加に対応するためにインフラを拡張しており、調達量をさらに押し上げています。ヘルスケア関係者の間では、感染リスクを軽減するコーティング縫合糸の採用が増加しており、感染対策と治癒の迅速化を目指す幅広いシフトを反映しています。伝統的な縫合糸と最新の縫合糸の両タイプとも、外科手術の専門分野全体で需要が高まっており、市場は長期的に持続的な拡大が見込まれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 47億米ドル |

| 予測金額 | 84億米ドル |

| CAGR | 6.1% |

吸収性縫合糸セグメントは2024年に30億米ドルを生み出しました。その人気は、体組織内で自然に分解され、物理的な抜糸の必要性をなくす能力にあります。この機能は患者の快適性を高め、特に抜糸が現実的でない体内手術では術後のケアを短縮します。軟部組織手術や小児手術では、感染リスクの低減と生体適合性の高さから、外科医が吸収性縫合糸を好む傾向が強まっています。このセグメントの勢いは、低侵襲治療に対する意識の高まりや、外科的解決を必要とする慢性疾患の負担増にも支えられています。これらの要因は総体的に、吸収性、生分解性オプションへの病院調達戦略のシフトを支えています。

マルチフィラメント縫合糸セグメントは2024年に63.8%のシェアを占めました。これらの縫合糸は、編組または撚り糸で構成され、優れた引張強度、結び目の安全性、柔軟性を備えており、確実な閉鎖が求められる手術に理想的です。その構造により、複雑な手術の際にも、より正確なコントロールと容易な取り扱いが可能となり、筋肉や消化器組織、生殖器官を含む手術には不可欠です。マルチフィラメント縫合糸は、創傷を効果的に固定し、圧力下でも破損しにくいため、一般外科手術、整形外科手術、婦人科手術、消化器外科手術で広く使用されています。

米国外科手術用縫合糸2024年の市場規模は19億米ドル。この成長を支えているのは、高度なヘルスケア・インフラ、高齢化社会、手術件数の多さです。メドトロニック、エチコン(ジョンソン・エンド・ジョンソン)、テレフレックスなどの世界的大手企業が市場に進出しているため、病院や手術センターは革新的な縫合ソリューションに迅速にアクセスできます。これらの企業は確立された販売網を通じて事業を展開しているため、公的・私的医療システム全体で新技術の迅速な導入が可能です。米国では、術後の転帰、患者の安全性、感染率の低下が重視され、入院・外来を問わず高度なコーティング縫合糸や吸収性縫合糸の需要が高まっています。

外科手術用縫合糸市場の主要企業は、縫合糸材料の特性(強度、生分解性、抗菌性能の向上)を改善するための継続的な研究開発に注力しています。各社は、感染管理をサポートし治癒を促進するコーティング縫合糸、有刺縫合糸、薬剤埋め込み縫合糸など、積極的にポートフォリオを拡大しています。戦略的な買収やパートナーシップは、大手企業が新たな地域市場に参入し、流通を強化するのに役立っています。製造とサプライチェーンの現地化は、コスト削減と需要の高い地域での製品供給を確保するために採用されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 手術件数の増加

- 外傷の発生率の上昇

- 縫合糸の設計と材料における技術的進歩

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- 高度な縫合糸の種類に対する償還の不一致

- 代替創傷閉鎖方法の利用可能性

- 市場機会

- カスタマイズおよび手術に特化した縫合糸の需要の増加

- 低侵襲手術への嗜好の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 特許分析

- 価格分析

- 製品タイプ別

- 地域別

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 吸収性縫合糸

- 天然縫合糸

- 合成縫合糸

- 非吸収性縫合糸

- ナイロン

- プロリーン

第6章 市場推計・予測:フィラメント別、2021年~2034年

- 主要動向

- モノフィラメント

- マルチフィラメント

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 眼科手術

- 心臓手術

- 整形外科

- 神経外科

- 婦人科手術

- その他の手術

第8章 市場推計・予測:最終用途別、2021年~2034年

- 病院

- 外来手術センター

- 専門クリニック

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Medical Solutions

- B. Braun Melsungen

- Boston Scientific

- CONMED

- Corza Medical

- Dolphin Sutures

- Ethicon(Johnson &Johnson)

- GPC Medical

- Healthium Medtech

- Integra Lifesciences

- Kono Seisakusho

- Medtronic

- Peters Surgical

- Smith and Nephew

- Stryker

- Teleflex

- Zimmer Biomet

The Global Surgical Sutures Market was valued at USD 4.7 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 8.4 billion by 2034. Market growth is being driven by a rising elderly population and an increasing number of surgeries related to aging, such as orthopedic and abdominal procedures. As chronic conditions, including diabetes, cardiovascular disorders, and obesity, continue to climb globally, so does the demand for surgical interventions, directly fueling the need for sutures. The availability of next-generation surgical tools, combined with the growing trend toward minimally invasive operations, is accelerating innovation in the industry.

Advancements in synthetic absorbable materials are also transforming wound management practices. Hospitals and surgical centers are expanding their infrastructure to support rising procedure volumes, further boosting procurement. Healthcare professionals are increasingly adopting coated sutures that reduce infection risks, reflecting a broader shift toward infection control and faster healing. Both traditional and modern suture types are experiencing elevated demand across surgical specialties, positioning the market for sustained long-term expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 6.1% |

The absorbable sutures segment generated USD 3 billion in 2024. Their popularity lies in their ability to naturally degrade within body tissues, removing the need for physical extraction. This feature enhances patient comfort and shortens post-operative care, especially in internal procedures where suture removal is impractical. Surgeons increasingly prefer absorbable sutures in soft tissue operations and pediatric surgeries due to reduced infection risks and better biocompatibility. The segment's momentum is also supported by growing awareness around minimally invasive treatments and the rising burden of chronic diseases that require surgical resolution. These factors collectively support a shift in hospital procurement strategies toward absorbable, biodegradable options.

The multifilament sutures segment held a 63.8% share in 2024. These sutures are composed of braided or twisted strands, delivering superior tensile strength, knot security, and flexibility-key attributes that make them ideal for surgeries that demand reliable closure. Their structure allows for more precise control and easy handling during intricate operations, which is essential for procedures involving muscle, gastrointestinal tissue, or reproductive organs. Multifilament sutures are used extensively in general, orthopedic, gynecological, and gastrointestinal surgeries due to their ability to secure wounds effectively and resist breakage under pressure.

U.S. Surgical Sutures Market generated USD 1.9 billion in 2024. This growth is supported by the country's advanced healthcare infrastructure, an aging population, and high surgical volumes. The market presence of global leaders such as Medtronic, Ethicon (Johnson & Johnson), and Teleflex ensures that hospitals and surgical centers have prompt access to innovative suturing solutions. These players operate through well-established distribution networks, enabling rapid adoption of new technologies across public and private health systems. In the U.S., emphasis on post-operative outcomes, patient safety, and reduced infection rates is pushing demand for advanced coated and absorbable sutures across both inpatient and outpatient surgical settings.

Notable companies influencing the Surgical Sutures Market include Dolphin Sutures, Boston Scientific, Corza Medical, Smith and Nephew, B. Braun Melsungen, Kono Seisakusho, Integra Lifesciences, Advanced Medical Solutions, Teleflex, Zimmer Biomet, Healthium Medtech, Peters Surgical, Ethicon (Johnson & Johnson), CONMED, Medtronic, Stryker, and GPC Medical. These manufacturers are deeply embedded in the value chain and continue to expand their reach through innovation and global partnerships.

Major players in the surgical sutures market are focusing on continuous R&D to improve suture material properties-enhancing strength, biodegradability, and antimicrobial performance. Companies are actively expanding their portfolios to include coated, barbed, and drug-embedded sutures that support infection control and accelerate healing. Strategic acquisitions and partnerships help leading firms enter new regional markets and strengthen distribution. Localization of manufacturing and supply chains is being adopted to reduce costs and ensure product availability in high-demand areas.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Filament

- 2.2.4 Application

- 2.2.5 End use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing growth in surgeries

- 3.2.1.2 Rising incidence of trauma

- 3.2.1.3 Technological advances in suture design and material

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Inconsistency in reimbursement for advanced suture types

- 3.2.2.2 Availability of alternative wound closure methods

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for customized and procedure specific sutures

- 3.2.3.2 Increasing preference toward minimally invasive surgical procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Absorbable sutures

- 5.2.1 Natural sutures

- 5.2.2 Synthetic sutures

- 5.3 Non-absorbable sutures

- 5.3.1 Nylon

- 5.3.2 Prolene

Chapter 6 Market Estimates and Forecast, By Filament, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Monofilament

- 6.3 Multifilament

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Ophthalmic surgery

- 7.3 Cardiac surgery

- 7.4 Orthopaedic surgery

- 7.5 Neurological surgery

- 7.6 Gynaecology surgery

- 7.7 Other surgeries

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Hospitals

- 8.2 Ambulatory surgical centers

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profile

- 10.1 Advanced Medical Solutions

- 10.2 B. Braun Melsungen

- 10.3 Boston Scientific

- 10.4 CONMED

- 10.5 Corza Medical

- 10.6 Dolphin Sutures

- 10.7 Ethicon (Johnson & Johnson)

- 10.8 GPC Medical

- 10.9 Healthium Medtech

- 10.10 Integra Lifesciences

- 10.11 Kono Seisakusho

- 10.12 Medtronic

- 10.13 Peters Surgical

- 10.14 Smith and Nephew

- 10.15 Stryker

- 10.16 Teleflex

- 10.17 Zimmer Biomet