|

市場調査レポート

商品コード

1773389

自動車用フェンダーホイールハウスパネル部品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Fender Wheel House Panel Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用フェンダーホイールハウスパネル部品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月19日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

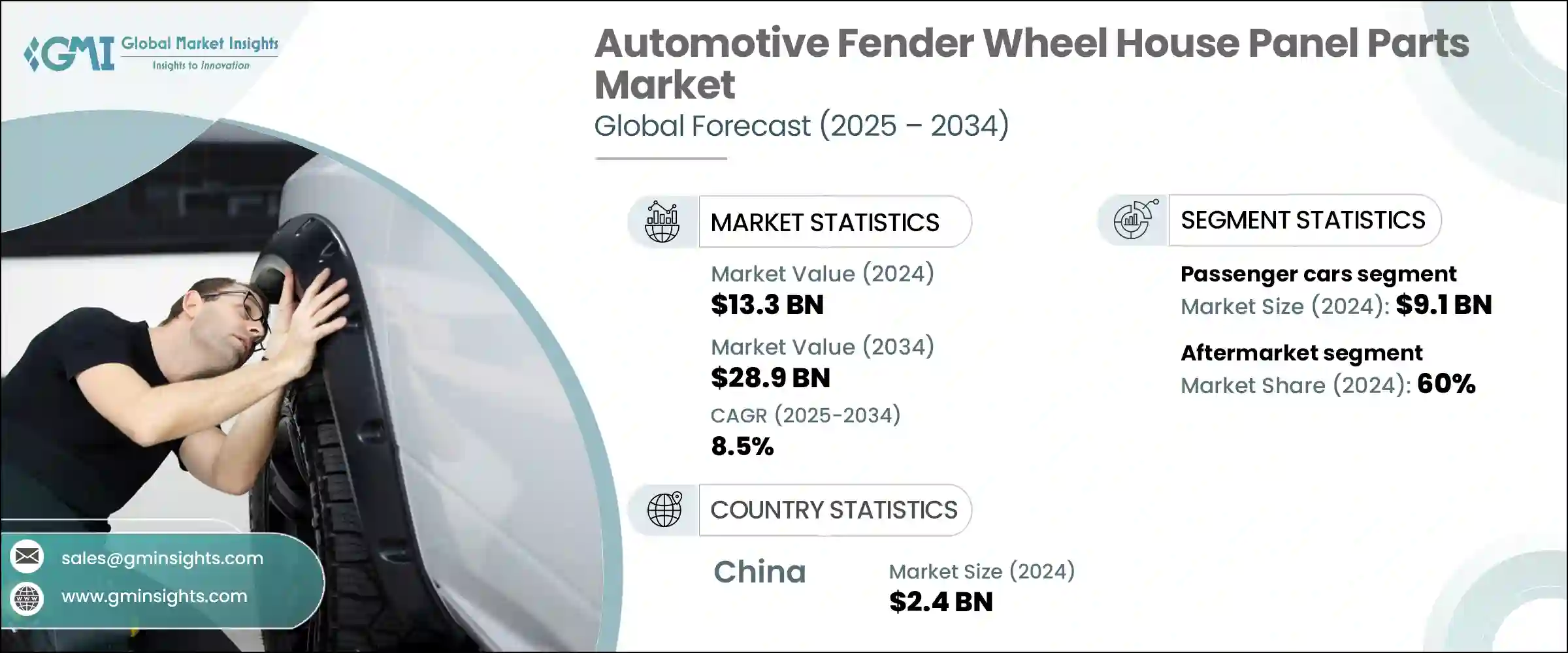

自動車用フェンダーホイールハウスパネル部品の世界市場規模は、2024年に133億米ドルとなり、CAGR 8.5%で成長し、2034年には289億米ドルに達すると予測されています。

自動車メーカーが自動車の効率性、安全性、デザインの革新にますます注力するようになり、市場は着実に拡大しています。ライナー、フロント・フェンダー、リア・フェンダー、ホイール・ハウス・パネルなどのフェンダー部品は、見た目の美しさと機能的性能の両立に不可欠です。これらの部品は、風の抵抗を減らして空気力学を向上させるだけでなく、道路の要素や破片から車両の下半身を保護します。衝突安全規制や設計要求の厳格化により、特に自動車メーカーがより強靭で空力特性に優れた車両を目指しているため、新しい車両プラットフォームではこれらの部品がより重要となっています。

自動車メーカーは、車両全体の重量を減らすために、鋼鉄から複合材料、熱可塑性プラスチック、アルミニウムなどの軽量な代替材料へと移行しつつあります。このシフトは、燃費効率を支える上で重要な役割を担っており、軽量構造によって航続距離を伸ばすことができる電気自動車分野では特に重要です。滑らかなフェンダーの輪郭や一体化したホイールアーチが空気の流れを改善し、エネルギー消費を削減するためです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 133億米ドル |

| 予測金額 | 289億米ドル |

| CAGR | 8.5% |

こうした機能強化は、騒音低減と効率がセールスポイントである電気自動車や高性能モデルにとって特に有益です。メーカーが国際的なエネルギー基準への適応を続ける中、モジュール式組立技術も台頭しており、複数の部品を1つのユニットに統合することで、迅速な製造と容易な取り付けを可能にしています。

乗用車セグメントは、2024年に91億米ドルを生み出しました。このセグメントは、特に個人移動が増加しているラテンアメリカやアジア太平洋のような地域で繁栄を続けています。セダン、SUV、ハッチバックなどの乗用車タイプは、洗練されたデザイン、空力スタイリング、軽量素材への依存度を高めており、強化フェンダーシステムの需要を押し上げています。また、電気自動車やハイブリッド車の台頭により、フェンダーの設計要件も変化しています。さらに、厳しい騒音基準を満たし、路上の破片からより優れた保護を提供する必要性から、機能性と安全性の両方の役割を果たす多層フェンダーパネルの開発がメーカーに促されています。

2024年には、アフターマーケット分野が60%のシェアを占める。この分野は、軽微な事故や車両の老朽化、消耗に伴う交換部品の安定した需要により成長を続けています。ホイールハウス・パネルやフェンダーなどの外装部品は、特に厳しい天候や交通量の多い地域で最も交換されています。消費者は、オンライン・チャネル、独立系ショップ、地元のサプライヤーを通じて提供される、費用対効果の高いアフターマーケット・オプションの幅広い選択肢に惹かれています。アフターマーケットによって、消費者は自分の車を手頃な価格でカスタマイズしたり修理したりすることができます。

中国の自動車用フェンダーホイールハウスパネル部品2024年の市場規模は24億米ドル。同国は、消費者需要の高まりと自動車生産への継続的な投資に後押しされ、特に乗用車とEVカテゴリーにおいて自動車製造大国であり続けています。政府の強力な支援と国家エネルギー目標に支えられた中国の電動モビリティへの推進は、自動車部品における先端材料と空力設計の使用を促しています。同国の強固なサプライチェーンとコスト効率の高い生産能力は重要な強みであり、金属製と複合材の両方のフェンダー部品の主要輸出国となっています。

自動車用フェンダーホイールハウスパネル部品世界市場の注目すべき市場参入企業には、Kostal Group、Valeo S.A.、矢崎総業、Flex-N-Gate Corporation、Lear Corporation、Magna International Inc.、アイシン精機株式会社などがあります。自動車用フェンダーホイールハウスパネル部品市場の主要企業は、競争力を維持するために革新的な材料開拓と高度な製造技術に注力しています。その多くは、組立時間と車両の空力特性を改善する軽量複合材技術やモジュラーパネルシステムに投資しています。EVメーカーとの提携により、サプライヤーはパーツを電動ドライブトレインや構造レイアウトに合わせることができます。企業はまた、拡大する地域需要に対応し、コストを削減するために、新興市場での生産を拡大しています。アフターマーケットに対応するため、企業はカスタマイズ可能で耐久性があり、手頃な価格の部品を導入することで、提供する製品を多様化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 影響要因

- 促進要因

- 車両の複雑化と電子制御ユニットの統合の増大

- ADASとセンサーベースの安全システムの進歩

- 遠隔診断を可能にするコネクテッドカー技術の成長

- 専門的なメンテナンスを必要とする電気自動車やハイブリッド車の普及が増加

- 業界の潜在的リスク&課題

- 高度な診断ツールや機器への高額な初期投資

- EVやADAS技術の訓練を受けた熟練技術者の不足

- 市場機会

- AIベースの予知保全システムの開発

- スマート診断によるモバイルプラットフォームの拡張

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- フロントフェンダーパネル

- フェンダーライナー

- リアフェンダーパネル

- ホイールハウスパネル

- インナーフェンダーパネル

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 鋼鉄

- プラスチック

- アルミニウム

- 複合

- カーボンファイバー

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車部品販売・卸売業者

- フリートオペレーター

- 政府および地方自治体

- 特殊車両メーカー

- DIY愛好家や趣味人

- その他

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- アフターマーケット

- OEM

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Aisin Seiki

- Dongfeng Liuzhou

- Dongfeng Motor

- Ficosa International

- Flex-N-Gate

- Gestamp Automocion

- Hyundai Mobis

- Inteva Products

- Kostal

- Lear Corporation

- Magna International

- Martinrea International

- Plastic Omnium

- Sanden

- Siemens

- Schaeffler

- Toyoda Gosei

- Toyota Boshoku

- Valeo

- Yazaki

The Global Automotive Fender Wheel House Panel Parts Market was valued at USD 13.3 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 28.9 billion by 2034. The market is experiencing steady expansion as automakers increasingly focus on vehicle efficiency, safety features, and design innovation. Fender components, including liners, front and rear fenders, and wheel house panels, are essential for both visual appeal and functional performance. These parts not only help reduce wind resistance and increase aerodynamics but also protect vehicles' underbodies from road elements and debris. Stricter crash safety regulations and design demands have made them more critical in new vehicle platforms, especially as carmakers aim for stronger, more aerodynamic vehicle builds.

Automotive manufacturers are transitioning from steel to lighter alternatives like composites, thermoplastics, and aluminum to reduce overall vehicle weight. This shift plays a critical role in supporting fuel efficiency, which is especially vital in the electric vehicle space, where lighter structures can boost driving range. The trend toward aerodynamic paneling is also shaping product development, as smooth fender contours and integrated wheel arches improve airflow and reduce energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $28.9 Billion |

| CAGR | 8.5% |

These enhancements are particularly beneficial for electric and high-performance models, where noise reduction and efficiency are selling points. As manufacturers continue adapting to international energy standards, modular assembly techniques are also gaining ground, allowing multiple components to be integrated into single units for quicker manufacturing and easier installation.

The passenger vehicles segment generated USD 9.1 billion in 2024. This segment continues to thrive, particularly in regions like Latin America and the Asia Pacific, where personal mobility is on the rise. Passenger vehicle types such as sedans, SUVs, and hatchbacks increasingly rely on sleek designs, aerodynamic styling, and lighter materials, driving up demand for enhanced fender systems. The rise of electric and hybrid passenger models is also reshaping Fender design requirements, as newer vehicles require lighter and structurally unique panel configurations. Additionally, the need to meet strict noise standards and provide better protection from road debris is encouraging manufacturers to develop multilayered fender panels that serve both functional and safety roles.

In 2024, the aftermarket segment held a 60% share. This sector continues to grow due to the consistent demand for replacement parts following minor accidents, aging vehicles, or wear and tear. Exterior body parts like wheel house panels and fenders are among the most replaced, especially in areas prone to harsh weather or heavy traffic. Consumers are drawn to the wide selection of cost-effective aftermarket options offered through online channels, independent shops, and local suppliers. The aftermarket also enables consumers to customize or repair their vehicles affordably, particularly in areas with high car ownership but limited warranties.

China Automotive Fender Wheel House Panel Parts Market generated USD 2.4 billion in 2024. The country remains a powerhouse in vehicle manufacturing, particularly in the passenger and EV categories, fueled by growing consumer demand and continued investment in automotive production. China's push toward electric mobility, backed by strong government support and national energy goals, is encouraging the use of advanced materials and aerodynamic designs in vehicle parts. The country's robust supply chain and cost-effective production capabilities are key advantages, making it a leading exporter of both metal and composite fender parts.

Notable market participants in the Global Automotive Fender Wheel House Panel Parts Market include Kostal Group, Valeo S.A., Yazaki Corporation, Flex-N-Gate Corporation, Lear Corporation, Magna International Inc., Aisin Seiki Co., Ltd., among others. Leading companies in the automotive fender wheel house panel parts market are focusing on innovative material development and advanced manufacturing techniques to stay competitive. Many are investing in lightweight composite technologies and modular panel systems that improve assembly time and vehicle aerodynamics. Partnerships with EV manufacturers allow suppliers to tailor parts to electric drivetrains and structural layouts. Firms are also expanding production in emerging markets to meet growing regional demand and reduce costs. To cater to the aftermarket, businesses are diversifying their offerings by introducing customizable, durable, and affordable components.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing vehicle complexity and integration of electronic control units

- 3.2.1.2 Advancements in ADAS and sensor-based safety systems

- 3.2.1.3 Growth in connected car technologies enabling remote diagnostics

- 3.2.1.4 Rising adoption of electric and hybrid vehicles requiring specialized maintenance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment in advanced diagnostic tools and equipment

- 3.2.2.2 Shortage of skilled technicians trained in EVs and ADAS technologies

- 3.2.3 Market Opportunities

- 3.2.3.1 Development of AI-based predictive maintenance systems

- 3.2.3.2 Expansion of mobile platforms with smart diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front fender panels

- 5.3 Fender liners

- 5.4 Rear fender panels

- 5.5 Wheel house panels

- 5.6 Inner fender panels

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Plastic

- 6.4 Aluminum

- 6.5 Composite

- 6.6 Carbon Fiber

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUV

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles

- 7.3.2 Medium Commercial Vehicles

- 7.3.3 Heavy Commercial Vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automotive part distributor and wholesaler

- 8.3 Fleet operators

- 8.4 Government and municipal bodies

- 8.5 Specialty vehicle manufacturers

- 8.6 DIY enthusiasts and hobbyists

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Aftermarket

- 9.3 OEM

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Dongfeng Liuzhou

- 11.3 Dongfeng Motor

- 11.4 Ficosa International

- 11.5 Flex-N-Gate

- 11.6 Gestamp Automocion

- 11.7 Hyundai Mobis

- 11.8 Inteva Products

- 11.9 Kostal

- 11.10 Lear Corporation

- 11.11 Magna International

- 11.12 Martinrea International

- 11.13 Plastic Omnium

- 11.14 Sanden

- 11.15 Siemens

- 11.16 Schaeffler

- 11.17 Toyoda Gosei

- 11.18 Toyota Boshoku

- 11.19 Valeo

- 11.20 Yazaki