プラズマ照明市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Plasma Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773387

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

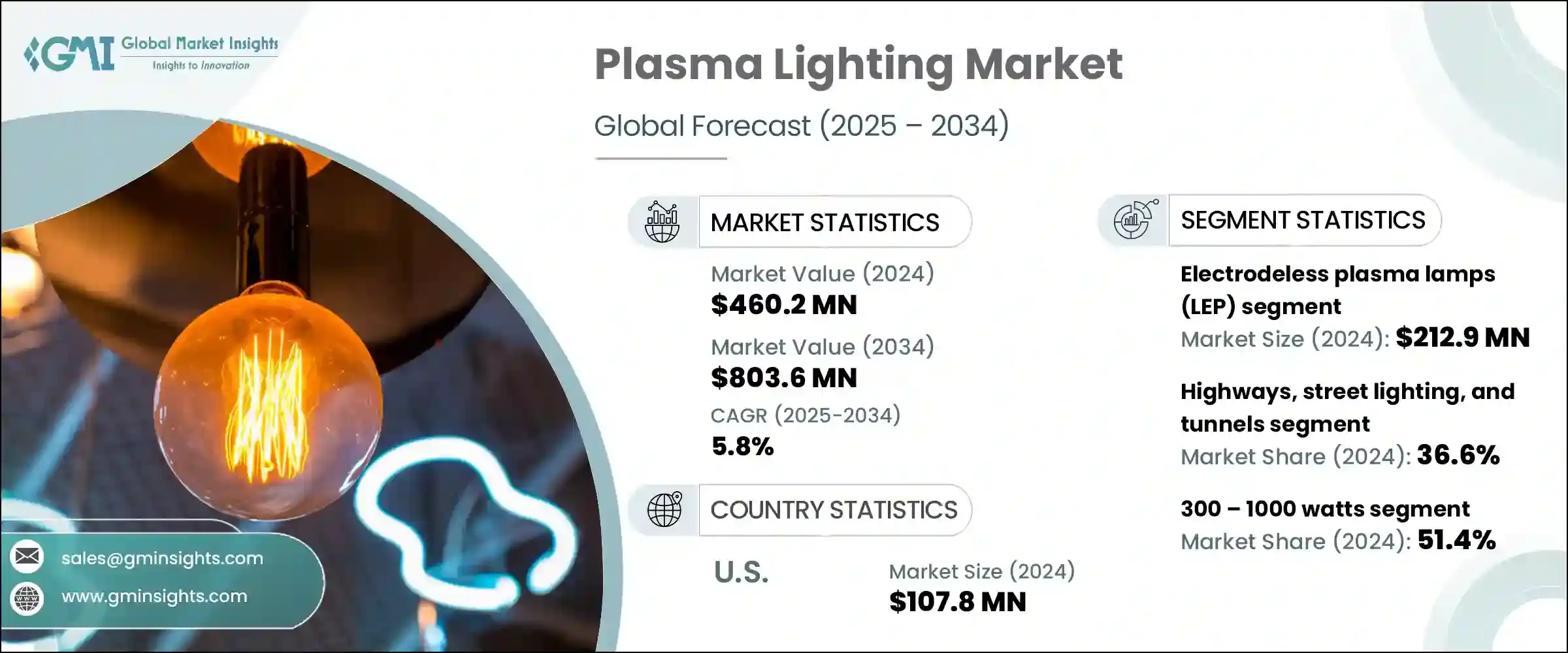

プラズマ照明の世界市場は、2024年には4億6,020万米ドルとなり、CAGR 5.8%で成長し、2034年には8億360万米ドルに達すると予測されています。

この成長の原動力となっているのは、園芸用照明と産業用・屋外用照明の両分野における需要の高まりです。制御環境農業(CEA)、垂直農法、温室栽培システムの拡大は、園芸における業界別プラズマライトの必要性を高める重要な要因です。

プラズマライトは、自然の太陽光に近い幅広いスペクトルの光を発生し、植物の健全な成長と収穫量の増加を促進します。寿命が長く、エネルギー効率に優れ、耐久性に優れているため、一貫した継続的な照明が必要な環境に適しています。一方、産業用途や屋外用途では、厳しい条件下で高光束出力と長寿命を実現する照明ソリューションが求められます。プラズマ照明は、高い演色評価数(CRI)、耐衝撃性、温度変化への耐性により、これらの要件に完璧に適合します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 4億6,020万米ドル |

| 予測金額 | 8億360万米ドル |

| CAGR | 5.8% |

政府主導によるインフラの近代化とエネルギー効率の高い取り組みにより、さまざまな分野で従来のメタルハライドやHID照明システムから先進的なプラズマ照明技術への移行が大幅に加速しています。このような政策主導の取り組みは、照明の品質と耐久性を向上させながら、エネルギー消費量を削減し、二酸化炭素排出量を削減することに重点を置いています。その結果、エネルギー効率に優れ、寿命が長く、光質が良いプラズマ照明が、公共インフラプロジェクトに選ばれるようになってきています。

無電極プラズマランプ(LEP)セグメントは2024年に2億1,290万米ドルの市場価値を持ち、信頼性の高い技術で自治体や産業用照明用途に広く採用されていることからプラズマ照明市場を独占しています。LEPランプは安定した光出力と長寿命を提供するため、安定した高輝度照明を必要とする場所に最適です。しかし、LEPランプの成長は、運用コストの増加や新興照明技術との競合激化といった課題に直面しています。

高速道路、街灯、トンネル分野は、2024年に36.6%という大きなシェアを占め、市場を独占しました。これは主に、信頼性が高く、高輝度、低メンテナンスの照明ソリューションを求めるインフラ開発プロジェクトの急増によるものです。公共機関や自治体がプラズマ照明を好むのは、トンネルや橋、交通量の多い道路など、安全性と運用コストの削減が最優先される厳しい屋外条件下で、卓越した長寿命と堅牢な性能を発揮するからです。また、プラズマ照明は、最小限のメンテナンスで安定した照明を提供できるため、重要なインフラ環境におけるダウンタイムと交換コストを削減することができます。

米国のプラズマ照明市場規模は2024年に1億780万米ドルとなり、産業および園芸分野での広範な応用とともに、インフラ近代化のための積極的な政府投資が後押ししています。最先端の照明技術をいち早く取り入れた同国では、プラズマ照明をスマートシティプロジェクトや制御環境農業システムに組み込む動きが加速しています。これらの取り組みでは、エネルギー効率、正確な光スペクトル制御、長寿命のソリューションが重視され、さまざまな用途でプラズマ照明の需要がさらに高まっています。旺盛なインフラ投資、技術革新、分野別需要の組み合わせにより、米国のプラズマ照明市場は今後数年間、力強い成長の勢いを維持するものと思われます。

プラズマ照明業界の主要企業には、LG Electronics、Gavita International B.V.、Ushio Inc.などがあり、継続的な技術革新と戦略的な市場開拓により、市場で重要な地位を占めています。市場での存在感を強め、競争力を構築するために、プラズマ照明分野の企業は複数の戦略的イニシアチブに注力しています。技術革新が中心的な役割を果たし、企業は、園芸や産業用途の進化するニーズに対応した、よりエネルギー効率が高く、より長持ちするプラズマ照明ソリューションの開発に多額の投資を行っています。農業技術プロバイダー、インフラ開発業者、自治体との提携や共同開発により、企業は事業範囲を拡大し、特定の顧客の需要に合わせて製品を調整することができます。スマートで制御可能な照明システムを含む製品ポートフォリオを拡大することで、精密農業やスマートシティインフラのような新たな動向を取り込むことができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 園芸照明の需要増加

- 優れたエネルギー効率と寿命

- 環境コンプライアンス圧力

- 産業および屋外用途からの需要の増加

- 持続可能な照明への投資の増加

- 業界の潜在的リスク&課題

- LED技術との競合

- 限られたベンダーエコシステム

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- デジタル変革イニシアチブ

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 無電極プラズマランプ(LEP)

- 電子レンジプラズマ照明

- 無線周波数(RF)プラズマ照明

第6章 市場推計・予測:パワー別、2021年~2034年

- 主要動向

- 300ワット未満

- 300~1000ワット

- 1000ワット以上

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 高速道路、街路照明、トンネル

- 産業

- スポーツ、エンターテイメント

- 園芸

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alphalite Inc.

- Gavita International B.V.

- Green De Corp

- Hive Lighting

- LG Electronics

- Lumartix SA.

- pinkRF

- Plasma International GmbH

- PlasmaBright

- Ushio Inc.

- WAVEPIA CO., LTD.

- Solaronix SA

目次

The Global Plasma Lighting Market was valued at USD 460.2 million in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 803.6 million by 2034. This growth is fueled by rising demand from both horticultural lighting and industrial and outdoor sectors. The expansion of controlled environment agriculture (CEA), vertical farming, and greenhouse farming systems is a significant factor driving the need for plasma lighting in horticulture.

Plasma lights produce a broad spectrum of light closely resembling natural sunlight, which promotes healthier plant growth and higher yields. Their long lifespan, energy efficiency, and robust durability make them highly suitable for environments that require consistent, continuous lighting. Meanwhile, industrial and outdoor applications demand lighting solutions that deliver high-lumen output and long operational life under tough conditions. Plasma lighting fits these requirements perfectly due to its high color rendering index (CRI), resistance to shocks, and ability to withstand temperature fluctuations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $460.2 Million |

| Forecast Value | $803.6 Million |

| CAGR | 5.8% |

Infrastructure modernization and energy-efficient initiatives led by governments are significantly accelerating the transition from traditional metal halide and HID lighting systems to advanced plasma lighting technologies across various sectors. These policy-driven efforts focus on reducing energy consumption and lowering carbon footprints while enhancing lighting quality and durability. As a result, plasma lighting, with its superior energy efficiency, longer lifespan, and better light quality, is becoming the preferred choice for public infrastructure projects.

The electrodeless plasma lamps (LEP) segment held a market value of USD 212.9 million in 2024, dominating the plasma lighting market because of its dependable technology and widespread adoption in municipal and industrial lighting applications. LEP lamps offer a consistent light output and long service life, making them ideal for locations demanding steady, high-intensity illumination. However, their growth faces challenges from increasing operational costs and rising competition from emerging lighting technologies.

The highways, street lighting, and tunnels segment dominated the market in 2024, holding a significant 36.6% share, driven primarily by the surge in infrastructure development projects demanding dependable, high-intensity, and low-maintenance lighting solutions. Public authorities and municipalities favor plasma lighting because of its exceptional longevity and robust performance under tough outdoor conditions, such as in tunnels, bridges, and busy roadways, where both safety and operational cost savings are paramount. This preference is reinforced by plasma lighting's ability to deliver consistent illumination with minimal maintenance, reducing downtime and replacement costs in critical infrastructure settings.

United States Plasma Lighting Market was valued at USD 107.8 million in 2024, fueled by proactive government investments in modernizing infrastructure alongside widespread applications in industrial and horticultural sectors. The country's early embrace of cutting-edge lighting technologies has accelerated the integration of plasma lighting into smart city projects and controlled environment agriculture systems. These initiatives emphasize energy efficiency, precise light spectrum control, and long-lasting solutions, further increasing the demand for plasma lighting across diverse applications. The combination of robust infrastructure spending, technological innovation, and sector-specific demand is set to sustain strong growth momentum in the U.S. plasma lighting market over the coming years.

Leading companies in the Plasma Lighting Industry include LG Electronics, Gavita International B.V., and Ushio Inc., which hold significant market positions through continuous innovation and strategic market outreach. To strengthen their market presence and build a competitive edge, companies in the plasma lighting sector focus on multiple strategic initiatives. Innovation plays a central role, with firms investing heavily in developing more energy-efficient, longer-lasting plasma lighting solutions that meet the evolving needs of horticultural and industrial applications. Partnerships and collaborations with agricultural technology providers, infrastructure developers, and municipal authorities allow companies to expand their reach and tailor products to specific client demands. Expanding product portfolios to include smart, controllable lighting systems helps tap into emerging trends like precision agriculture and smart city infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Power trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for horticultural lighting

- 3.2.1.2 Superior energy efficiency and lifespan

- 3.2.1.3 Environmental compliance pressure

- 3.2.1.4 Increasing demand from industrial & outdoor applications

- 3.2.1.5 Growing investments in sustainable lighting

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from LED technology

- 3.2.2.2 Limited vendor ecosystem

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.13 Consumer sentiment analysis

- 3.14 Patent and ip analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Electrodeless plasma lamps (LEP)

- 5.3 Microwave plasma lighting

- 5.4 Radio frequency (RF) plasma lighting

Chapter 6 Market Estimates & Forecast, By Power, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Less than 300 watts

- 6.3 300 – 1000 watts

- 6.4 Above 1000 watts

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Highways, street lighting, and tunnels

- 7.3 Industrial

- 7.4 Sports & entertainment

- 7.5 Horticulture

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alphalite Inc.

- 9.2 Gavita International B.V.

- 9.3 Green De Corp

- 9.4 Hive Lighting

- 9.5 LG Electronics

- 9.6 Lumartix SA.

- 9.7 pinkRF

- 9.8 Plasma International GmbH

- 9.9 PlasmaBright

- 9.10 Ushio Inc.

- 9.11 WAVEPIA CO., LTD.

- 9.12 Solaronix SA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日