|

市場調査レポート

商品コード

1773386

NUT正中線がん治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測NUT Midline Carcinoma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| NUT正中線がん治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月25日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

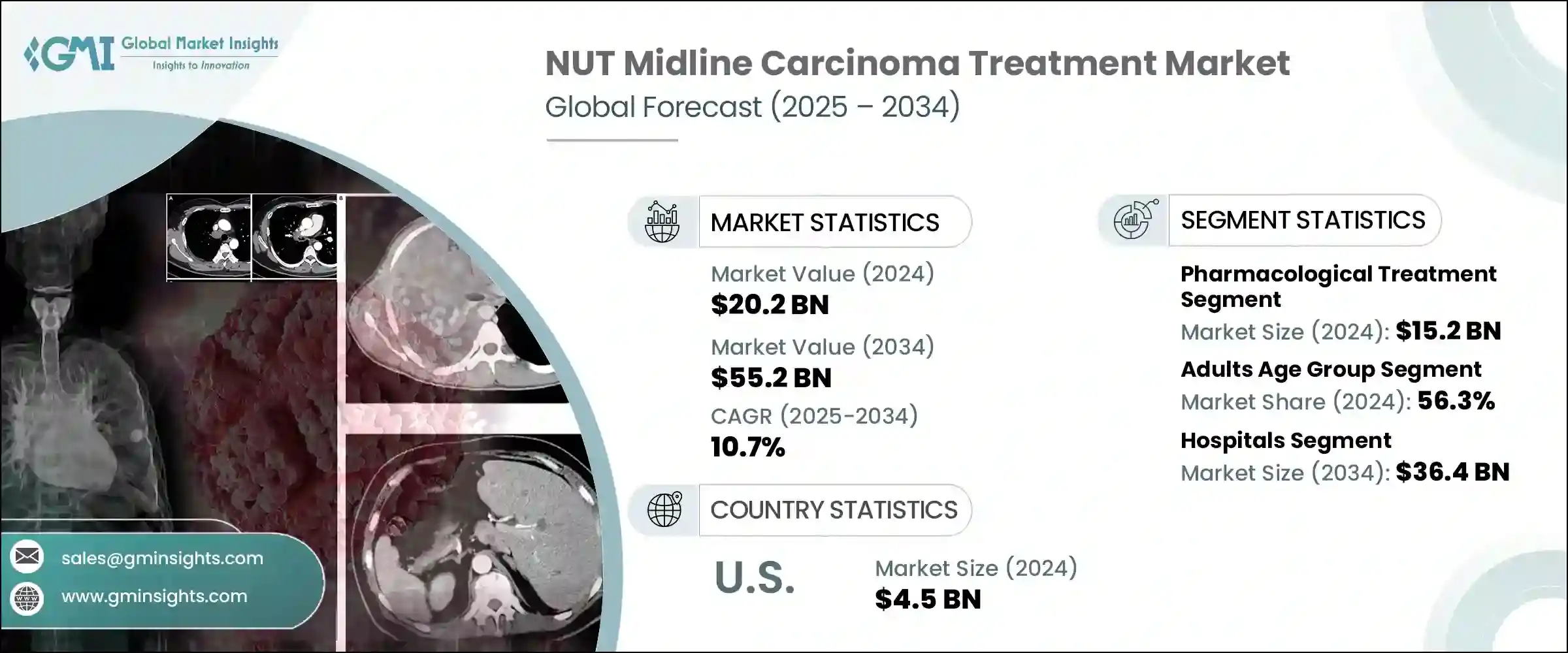

NUT正中線がん治療の世界市場規模は、2024年に202億米ドルとなり、CAGR 10.7%で成長し、2034年には552億米ドルに達すると予測されています。

NMCの世界の有病率の上昇と診断・治療技術の進歩により、市場は急速に拡大しています。政府の支援政策、臨床試験への資金提供、希少がん撲滅に向けた取り組みなどの主な要因が、この成長を後押ししています。

さらに、高度な診断ツールの利用可能性が高まったことで、医療従事者がより早期にNMCを発見できるようになり、治療の普及に寄与しています。さらに、新興市場における都市化、ヘルスケアへのアクセス改善、可処分所得の向上が診断率を高め、市場拡大をさらに後押ししています。政府および非政府の両方からの研究開発資金の増加、標的治療のような新規治療法の開発に継続的に注力していることも、市場拡大に大きな役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 202億米ドル |

| 予測金額 | 552億米ドル |

| CAGR | 10.7% |

腫瘍専門病院や高度診断センターの増加は、NUT正中線がんの早期発見と管理の改善に大きく寄与しており、市場全体の勢いを強めています。これらの施設は、分子イメージング、精密生検システム、遺伝子配列決定ツールなどの最先端技術を備えつつあり、臨床医が複雑な遺伝子異常をより高い精度で突き止めることを可能にしています。この診断精度の高さは、標的治療の開始を早めるだけでなく、予後を改善するものであり、NMCのような希少がんや攻撃性の高いがんでは重要な要素です。

薬理学的治療分野は2024年に152億米ドルを生み出しました。次世代シークエンシング(NGS)や蛍光in situハイブリダイゼーション(FISH)などの分子診断の技術的進歩により、NUTM1遺伝子再配列の正確な同定が可能になり、より的を絞った薬理学的治療が可能になりました。さらに、NMCの有病率の増加、診断能力の向上、治療法の改善に対する需要の高まりが、市場の成長を後押ししています。また、BET阻害剤やBRD-NUT融合タンパク質を標的とする薬剤など、初期段階の試験で有望な結果を示している新規治療薬の開発からも、このセグメントは恩恵を受けています。

2024年には、成人市場が56.3%と最大の市場シェアを占める。NMCは当初、主に小児や青年が罹患すると考えられていたが、最近の研究では成人、特に20~50歳での罹患率が高いことが示されています。このような人口動態の変化は、ヘルスケアや分子プロファイリング・ツールへのアクセスの向上と相まって、成人におけるより早期かつ正確な診断につながっています。その結果、特にBET阻害剤や免疫療法のような先進的な治療法の治療率が高まっています。

米国NUT正中線がん治療2024年の市場規模は45億米ドル。同国では、NMCを含む希少がんに焦点を当てた臨床試験が数多く実施されています。主要な開発機関が、BET阻害剤や免疫療法のような標的療法の開発を主導しています。さらに、米国FDAはいくつかの希少がん治療薬にオーファンドラッグ指定を与え、税額控除、市場独占権、早期承認パスウェイなどのインセンティブを提供しています。このような優遇措置は、製薬会社によるNMC研究開発への投資拡大を促し、市場の成長をさらに促進しています。

NUT正中線がん治療市場の主要企業には、Merck &Co、C4 Therapeutics、Constellation Pharmaceuticals、Pfizer、Syndax Pharmaceuticals、Bristol-Myers Squibb Company、GlaxoSmithKline、F. Hoffmann-La Roche、Ipsen Biopharmaceuticals、OncoFusion Therapeuticsなどがあります。NMC治療市場の各社は、NMCの分子的な複雑さに対処する標的療法を開発するため、研究開発に多額の投資を行い、その地位を強化することに注力しています。

学術・研究機関との提携により、これらの企業は臨床試験を加速させることができ、また先進的な診断技術の採用により、疾患に対する理解を深めることができます。さらに、企業は新しい治療法をより早く市場に投入するため、希少疾病用医薬品(オーファンドラッグ)認定や迅速承認といった薬事規制に注力しています。さらに、革新的な治療ソリューションを持つ中小バイオテクノロジー企業との提携や戦略的買収は、大手企業の製品ポートフォリオの拡大やNMCの治療選択肢の多様化に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- NMCを検出するための高度な診断技術の利用可能性

- 病院と専門腫瘍センターの拡大

- 治療法の進歩

- 業界の潜在的リスク&課題

- 治療費が高め

- 限られた治療選択肢

- 市場機会

- 標的療法への注目が高まる

- 臨床試験への投資の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 将来の市場動向

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推計・予測:治療タイプ別、2021年~2034年

- 主要動向

- 薬物治療

- 療法別

- 化学療法

- 免疫療法

- その他のタイプ

- 投与経路別

- 経口

- 非経口

- 療法別

- 非薬物治療

第6章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 小児

- 大人

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門腫瘍クリニック

- 在宅ケア環境

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Bristol-Myers Squibb Company

- C4 Therapeutics

- Constellation Pharmaceuticals

- F. Hoffmann-La Roche

- GlaxoSmithKline

- Ipsen Biopharmaceuticals

- Merck &Co

- OncoFusion Therapeutics

- Pfizer

- Syndax Pharmaceuticals

The Global NUT Midline Carcinoma Treatment Market was valued at USD 20.2 billion in 2024 and is estimated to grow at a CAGR of 10.7% to reach USD 55.2 billion by 2034. The market is expanding rapidly due to the rising global prevalence of NMC, coupled with advancements in diagnostic and therapeutic technologies. Key factors such as supportive government policies, funding for clinical trials, and initiatives aimed at combating rare cancers are driving this growth.

Moreover, the increased availability of advanced diagnostic tools is helping healthcare professionals detect NMC earlier, contributing to higher treatment uptake. Additionally, urbanization, improved healthcare access, and higher disposable incomes in emerging markets are enhancing diagnostic rates, further fueling market expansion. Increased research funding from both governmental and non-governmental sources, along with the continuous focus on developing novel treatments like targeted therapies, are also playing significant roles in market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.2 Billion |

| Forecast Value | $55.2 Billion |

| CAGR | 10.7% |

The growing number of specialized oncology hospitals and advanced diagnostic centers is significantly contributing to earlier detection and improved management of NUT midline carcinoma, reinforcing the market's overall momentum. These facilities are increasingly equipped with state-of-the-art technologies like molecular imaging, precision biopsy systems, and genetic sequencing tools that allow clinicians to pinpoint complex genetic abnormalities with higher accuracy. This diagnostic precision not only accelerates the initiation of targeted treatments but also enhances prognosis, which is a critical factor in rare and aggressive cancers like NMC.

The pharmacological treatment segment generated USD 15.2 billion in 2024. Technological advancements in molecular diagnostics, such as next-generation sequencing (NGS) and fluorescence in situ hybridization (FISH), have enabled precise identification of NUTM1 gene rearrangements, allowing for more targeted pharmacological treatments. Furthermore, the growing prevalence of NMC, increased diagnostic capabilities, and the rising demand for improved therapeutics options are boosting market growth. The segment is also benefitting from the development of novel therapies such as BET inhibitors and agents targeting BRD-NUT fusion proteins, which are showing promising results in early-stage trials.

In 2024, the adult segment accounted for the largest market share, with 56.3%. While NMC was initially thought to affect primarily children and adolescents, more recent studies have shown a higher incidence among adults, particularly those aged 20 to 50. This demographic shift, combined with better access to healthcare and molecular profiling tools, has led to earlier and more accurate diagnoses in adults. This, in turn, has resulted in higher treatment uptake, particularly for advanced therapies like BET inhibitors and immunotherapies.

U.S. NUT Midline Carcinoma Treatment Market was valued at USD 4.5 billion in 2024. The country is home to numerous clinical trials focused on rare cancers, including NMC. Leading institutions are spearheading the development of targeted therapies like BET inhibitors and immunotherapies. Furthermore, the U.S. FDA has granted orphan drug designations to several NMC treatments, offering incentives like tax credits, market exclusivity, and accelerated approval pathways. These incentives are encouraging pharmaceutical companies to increase their investment in NMC research and development, further propelling market growth.

Key players in the NUT Midline Carcinoma Treatment Market include Merck & Co, C4 Therapeutics, Constellation Pharmaceuticals, Pfizer, Syndax Pharmaceuticals, Bristol-Myers Squibb Company, GlaxoSmithKline, F. Hoffmann-La Roche, Ipsen Biopharmaceuticals, OncoFusion Therapeutics. Companies in the NMC treatment market focus on strengthening their position by investing heavily in research and development to create targeted therapies that address the molecular intricacies of NMC.

Collaborations with academic and research institutions allow these companies to accelerate clinical trials, while the adoption of advanced diagnostic technologies helps them gain a deeper understanding of the disease. Furthermore, companies are focusing on regulatory pathways like orphan drug status and fast-track approval to bring new treatments to market faster. Additionally, partnerships and strategic acquisitions of smaller biotech firms with innovative therapeutic solutions are helping larger players expand their product portfolios and diversify treatment options for NMC.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Disease type

- 2.2.3 Treatment type

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Availability of advanced diagnostic techniques to detect NMC

- 3.2.1.2 Increasing expansion of hospitals and specialty oncology centers

- 3.2.1.3 Growing advancement in treatment modalities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Limited treatment options

- 3.2.3 Market opportunities

- 3.2.3.1 Growing focus on targeted therapies

- 3.2.3.2 Increasing investment in clinical trials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmacological treatment

- 5.2.1 By therapy

- 5.2.1.1 Chemotherapy

- 5.2.1.2 Immunotherapy

- 5.2.1.3 Other types

- 5.2.2 By route of administration

- 5.2.2.1 Oral

- 5.2.2.2 Parenteral

- 5.2.1 By therapy

- 5.3 Non-pharmacological treatment

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adults

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty oncology clinics

- 7.4 Homecare settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bristol-Myers Squibb Company

- 9.2 C4 Therapeutics

- 9.3 Constellation Pharmaceuticals

- 9.4 F. Hoffmann-La Roche

- 9.5 GlaxoSmithKline

- 9.6 Ipsen Biopharmaceuticals

- 9.7 Merck & Co

- 9.8 OncoFusion Therapeutics

- 9.9 Pfizer

- 9.10 Syndax Pharmaceuticals