プロセスプラントガスタービン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Process Plants Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773377

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

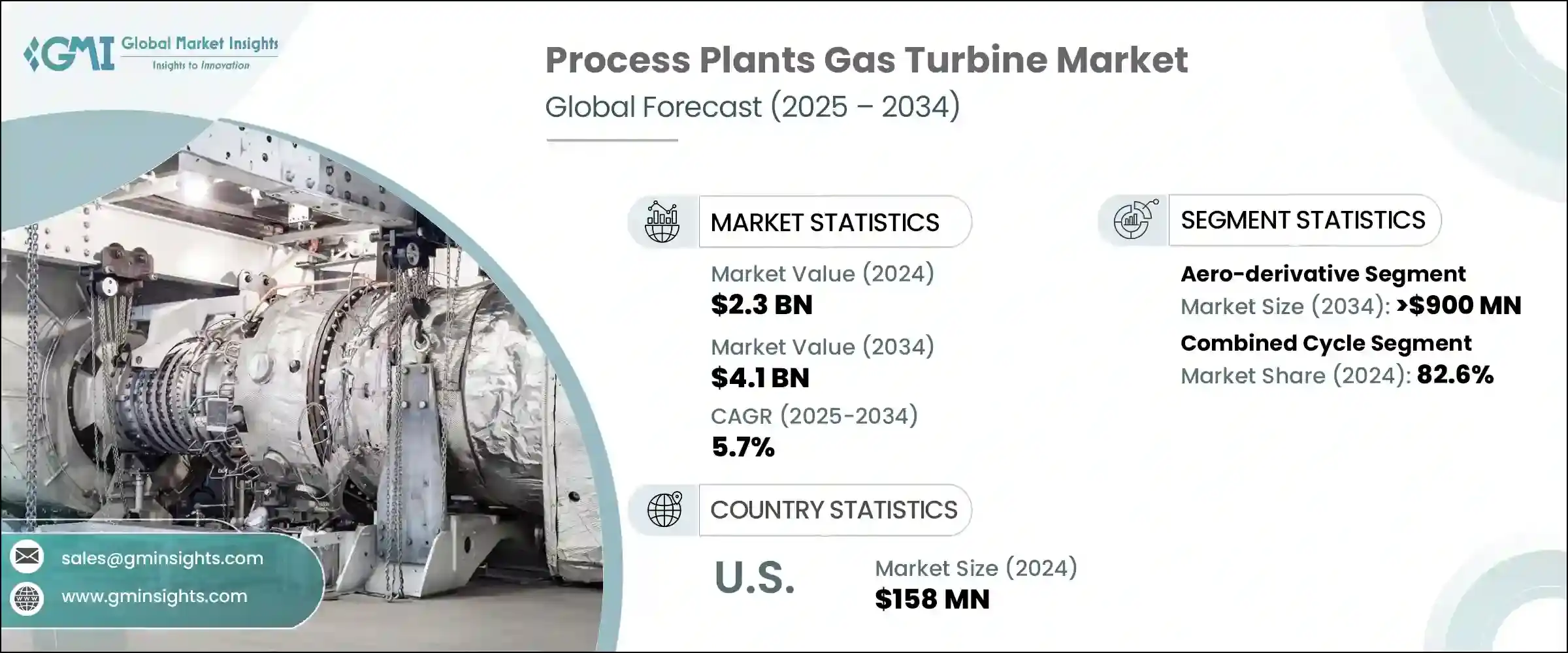

プロセスプラントガスタービンの世界市場規模は、2024年に23億米ドルとなり、CAGR 5.7%で成長し、2034年には41億米ドルに達すると予測されています。

プロセス産業では、特に電力障害が頻繁に発生する地域において、信頼性の低い送電網インフラへの依存を軽減するため、自家発電用にガスタービンを選択するケースが増えています。自家発電用途でガスタービンの使用が増加していることは、中断のない操業をサポートし、生産ロスを防止するためであり、市場拡大に直接貢献しています。これらのシステムは、熱電併給(CHP)セットアップで一般的に使用され、発電と蒸気を同時に発生させ、プラント全体の効率を高める。この二重機能は、産業施設全体でガスタービンの設置を促進する重要な要因です。

中小規模のプロセス施設では、迅速な配備を可能にし、大規模な土木工事の必要性を抑えるコンパクトなモジュール式タービンパッケージへの需要が高まっています。タービンはまた、従来のインフラが実行不可能な、移動式化学製品やパイプライン事業などの一時的な現場や遠隔地にも配備されています。これらのタービンは、セメント、ガラス、石油化学などの分野で、機械システムに電力を供給したり、特殊な機能のために熱エネルギーを供給したりするために、製造工程に直接組み込まれています。排ガスからの熱は、乾燥、脱炭酸、蒸気分解に利用されることが増えており、プロセス産業にさらなる効率化のメリットを提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 5.7% |

大型ガスタービン分野は、2034年までCAGR 5.5%で成長すると予測されます。これらのタービンは、ベースロードの電力需要が継続する製鉄所、セメント施設、石油化学コンビナートなどの重工業環境に広く設置されています。コージェネレーション・ソリューションとの統合は、電力と熱エネルギーの同時供給をサポートし、大規模な産業拠点に効率的なエネルギー・ループを提供し、このセグメントの長期的成長を強化します。

オープン・サイクル・セグメントは、2034年までCAGR 5.5%で成長すると予想されます。これらの構成は、急速始動が可能なため、ピーク負荷やバックアップ用途に適しています。不安定な電力供給に直面している産業界は、操業を確保し停電を防ぐためにオープンサイクルのガスタービンに注目しており、これが引き続き市場力学を強化しています。

米国プロセスプラントガスタービン2024年の市場規模は1億5,800万米ドル。米国は産業電化に力を入れており、老朽化した複合火力発電設備を近代化する必要があるため、ガスタービンと再生可能エネルギーとの統合が進んでいます。環境機関による規制措置は、肥料や化学製造などの分野で旧式のタービンシステムの交換をさらに加速させ、米国の採用を後押ししています。

プロセスプラントガスタービン世界市場の主要企業には、MAN Energy Solutions、三菱重工業、シーメンス・エナジー、ベーカー・ヒューズ、ロールス・ロイス、GE Vernovaなどがあります。プロセスプラントガスタービン市場の主要企業は、製品の最適化、現地生産の拡大、用途別カスタマイズの深化に注力しています。研究開発への投資は、低排出ガス、燃料の柔軟性向上、モジュール化されたタービンの開発を目指しています。多くの企業は、EPC請負業者やプロセスプラント事業者と積極的にパートナーシップを結び、ターンキータービンパッケージや長期サービス契約を提供しています。進化する産業界の需要に対応するため、メーカーはデジタル診断と予知保全機能をタービンプラットフォームに統合しています。アジア太平洋や中東などの地域での生産拠点の拡大も、引き続き戦略的優先事項となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 50kW未満

- 50kW~500kW以上

- 500kW~1MW

- 1MW~30MW以上

- 30MW~70MW以上

- 70MW~200MW以上

- 200MW以上

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 航空転用

- ヘビーデューティー

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- オープンサイクル

- 複合サイクル

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- オランダ

- フィンランド

- ギリシャ

- デンマーク

- ルーマニア

- ポーランド

- スウェーデン

- アジア太平洋地域

- 中国

- オーストラリア

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- バングラデシュ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- エジプト

- トルコ

- バーレーン

- イラク

- ヨルダン

- レバノン

- 南アフリカ

- ナイジェリア

- アルジェリア

- ケニア

- ガーナ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

- チリ

第9章 企業プロファイル

- Ansaldo Energia

- Baker Hughes

- Bharat Heavy Electricals

- Capstone Green Energy

- Destinus Energy

- Doosan

- Flex Energy Solutions

- GE Vernova

- Harbin Electric

- IHI Corporation

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Nanjing Turbine &Electric Machinery

- Rolls Royce

- Shanghai Electric Gas Turbine

- Siemens Energy

- Solar Turbines

- Vericor

- Wartsila

目次

The Global Process Plants Gas Turbine Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 4.1 billion by 2034. Process industries are increasingly choosing gas turbines for on-site power generation to reduce dependence on unreliable grid infrastructure, particularly in areas with frequent power disturbances. The growing use of these turbines in captive power applications supports uninterrupted operations and safeguards against production losses, contributing directly to market expansion. These systems are commonly used in combined heat and power (CHP) setups, where they simultaneously generate electricity and steam, enhancing overall plant efficiency. This dual functionality is a critical factor driving gas turbine installations across industrial facilities.

Small and mid-sized process facilities are fueling demand for compact and modular turbine packages that offer rapid deployment and limit the need for extensive civil works. Turbines are also being deployed in temporary or remote sites, including mobile chemical or pipeline operations, where conventional infrastructure is not viable. These turbines are directly integrated into manufacturing processes to power mechanical systems or deliver heat energy for specialized functions in sectors such as cement, glass, and petrochemicals. The heat from exhaust gases is increasingly being utilized for drying, calcining, or steam cracking, offering added efficiency benefits to process industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.7% |

Heavy-duty gas turbines segment is forecasted to grow at a CAGR of 5.5% through 2034. These turbines are widely installed in heavy industrial environments such as steelworks, cement facilities, and petrochemical complexes, where base-load power demand is continuous. Their integration with cogeneration solutions supports the simultaneous delivery of electricity and thermal energy, providing an efficient energy loop at large industrial hubs and reinforcing long-term growth in this segment.

The open cycle segment is expected to grow at a CAGR of 5.5% through 2034. These configurations are favored for their ability to start rapidly, making them suitable for peak load and backup applications. Industries facing unstable power supply are turning to open-cycle gas turbines to secure operations and prevent power interruptions, which continues to strengthen market dynamics.

U.S. Process Plants Gas Turbine Market was valued at USD 158 million in 2024. The nation's focus on industrial electrification and the need to modernize aging combined cycle assets are encouraging the integration of gas turbines with renewable sources. Regulatory measures from environmental agencies are further accelerating the replacement of outdated turbine systems in segments such as fertilizers and chemical manufacturing, pushing U.S. adoption forward.

Key players in the Global Process Plants Gas Turbine Market include MAN Energy Solutions, Mitsubishi Heavy Industries, Siemens Energy, Baker Hughes, Rolls Royce, GE Vernova, and several others. Leading companies in the process plants gas turbine market are focused on product optimization, expanding localized manufacturing, and deepening application-specific customization. Investments in R&D are aimed at developing turbines with lower emissions, enhanced fuel flexibility, and greater modularity. Many players are actively forming partnerships with EPC contractors and process plant operators to offer turnkey turbine packages and long-term service agreements. To cater to evolving industrial demands, manufacturers are integrating digital diagnostics and predictive maintenance capabilities into turbine platforms. Expanding production footprints in regions such as Asia-Pacific and the Middle East also remains a strategic priority.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Product, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Aero-derivative

- 6.3 Heavy duty

Chapter 7 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Open cycle

- 7.3 Combined cycle

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Finland

- 8.3.8 Greece

- 8.3.9 Denmark

- 8.3.10 Romania

- 8.3.11 Poland

- 8.3.12 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.4.6 Thailand

- 8.4.7 Malaysia

- 8.4.8 Bangladesh

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 Bahrain

- 8.5.9 Iraq

- 8.5.10 Jordan

- 8.5.11 Lebanon

- 8.5.12 South Africa

- 8.5.13 Nigeria

- 8.5.14 Algeria

- 8.5.15 Kenya

- 8.5.16 Ghana

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Peru

- 8.6.4 Chile

Chapter 9 Company Profiles

- 9.1 Ansaldo Energia

- 9.2 Baker Hughes

- 9.3 Bharat Heavy Electricals

- 9.4 Capstone Green Energy

- 9.5 Destinus Energy

- 9.6 Doosan

- 9.7 Flex Energy Solutions

- 9.8 GE Vernova

- 9.9 Harbin Electric

- 9.10 IHI Corporation

- 9.11 Kawasaki Heavy Industries

- 9.12 MAN Energy Solutions

- 9.13 Mitsubishi Heavy Industries

- 9.14 Nanjing Turbine & Electric Machinery

- 9.15 Rolls Royce

- 9.16 Shanghai Electric Gas Turbine

- 9.17 Siemens Energy

- 9.18 Solar Turbines

- 9.19 Vericor

- 9.20 Wartsilä

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日