ストレージラック市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Storage Rack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773372

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

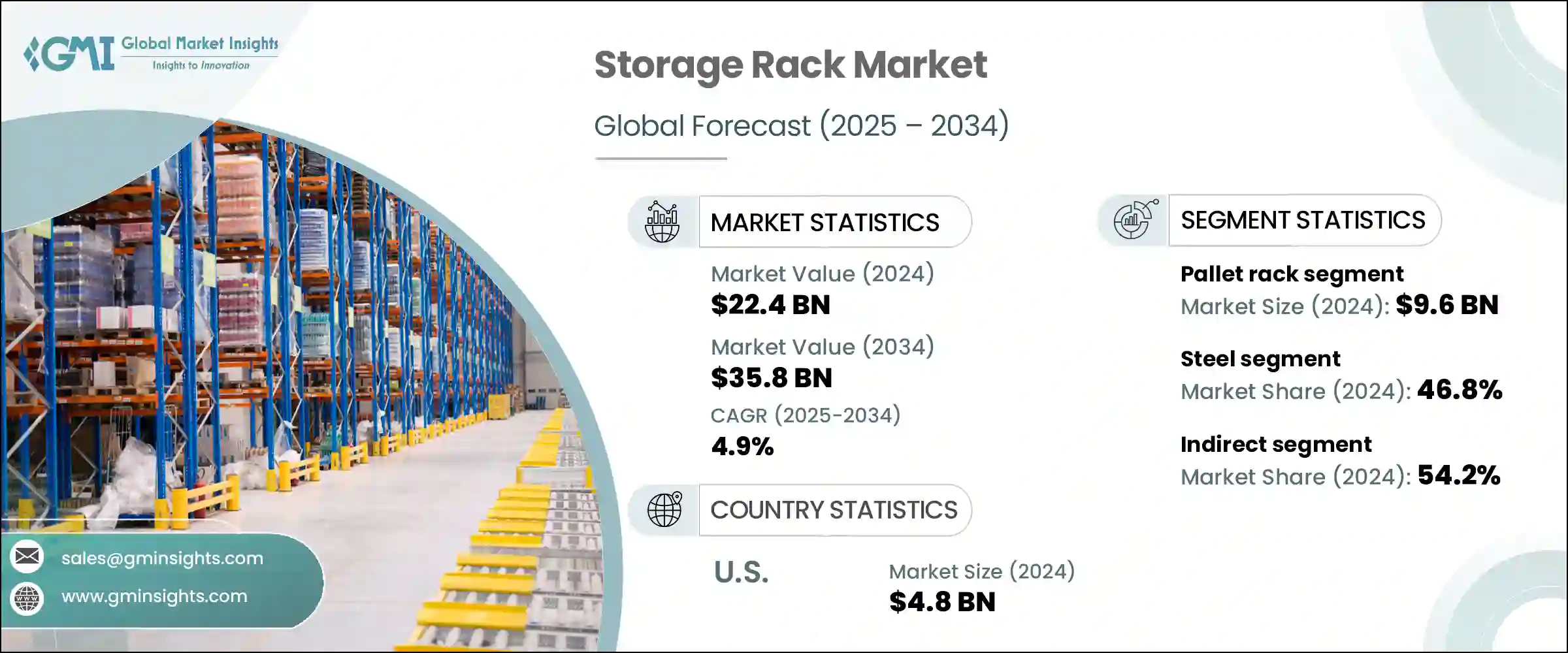

ストレージラックの世界市場規模は、2024年に224億米ドルとなり、CAGR 4.9%で成長し、2034年には358億米ドルに達すると予測されています。

都市部のフルフィルメント拠点における効率的で省スペースなソリューションに対する需要の高まりが、この成長に拍車をかけています。都市部では運用コストの上昇やスペースの制限に直面しているため、企業は保管を最適化するために高密度ラッキング、モジュラーシェルビング、メザニンベースの構造に目を向けています。eコマース、特にクイック・コマースの拡大により、迅速なオーダーピッキングと在庫回転の必要性が加速しています。これをサポートするため、倉庫はロボットピッキングや自動保管・検索システムなどの自動化システムとシームレスに連動するラックを採用しています。

ストレージインフラは、ロジスティクスのワークフローや配送スケジュールの変化とともに急速に進化しており、企業は業務スピードと柔軟性を高めるラッキングシステムを優先しています。都市部の配送センターでは、狭い通路のラック、移動棚、垂直レイアウトが採用されています。モジュール化の傾向も強く、企業は在庫需要の変化に合わせて進化できる、調整・拡張可能なストレージ・ソリューションを好んでいます。市場の変革は、自動化の採用、スマート倉庫の動向、速いペースの物流環境に適したコスト効率の高い設計ソリューションの組み合わせによって推進されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 224億米ドル |

| 予測金額 | 358億米ドル |

| CAGR | 4.9% |

2024年、パレットラックの市場規模は96億米ドルに達し、2034年までのCAGRは5.3%と予測されます。これらのラックは、その適応性、経済的価値、さまざまな分野での互換性により、市場で最も広く使用されています。パレットラックは、パレット化された在庫を水平に保管し、垂直方向に複数段積み上げるように設計されており、倉庫の効率を高め、在庫の重量や量の変動に対応します。パレットラックの関連性は、物流、飲食品、小売、製薬、自動車など、主要な業界に及んでおり、伝統的な倉庫形式でも近代的な倉庫形式でも定番となっています。

スチール部門は2024年に46.8%のシェアを占め、保管ラックの主要材料としてトップの座を維持しており、2025年から2034年にかけてCAGR 5.4%で成長すると予想されています。その高い強度対重量比、長寿命、コスト効率は、大規模倉庫や産業用途に理想的です。スチールラックは、大規模で高密度の在庫を支える頑丈な保管環境に広く導入されています。製造業、小売業、eコマースなどの分野では、大量のマテリアルを扱い、オペレーションを合理化し、構造的な妥協なしに重機の使用に耐える能力を持つスチールベースのラックが頼りにされています。

米国のストレージラック市場は、2024年に48億米ドルと評価され、2034年までCAGR 5.5%で成長すると予測されています。この成長は、同国におけるeコマースの急速な拡大、倉庫ロボットの採用の増加、自動化システムの広範な導入に起因しています。需要は、産業部門、物流業者、大規模小売業者が牽引しています。また、医薬品や食品のサプライチェーンにおけるコールドチェーンインフラの開発が市場拡大に寄与しています。同地域では人件費が高いため、生産性向上と手作業の削減を目的とした高密度ストレージへの投資がさらに活発化しています。同地域では米国が依然として市場を独占しており、メキシコ、カナダがこれに続いています。

ストレージラック業界の主要企業には、Interlake Mecalux、Dematic、Kardex Group、Toyota Industries、Constructor Group、Gonvarri Material Handling、AK Material Handling Systems、SSI Schaefer、Ridg-U-Rak、Mecalux、Daifuku、Arpac、North American Steel Equipment、AR Racking、Jungheinrichなどがあります。ストレージラック市場のトップ企業は、競争力を強化するため、デジタル統合、製品イノベーション、業務効率化に注力しています。

その多くは、ロボット工学、AS/RS、先進的な倉庫ソフトウェアプラットフォームをサポートする自動化対応ラッキングシステムの開発に投資しています。メーカー各社は、さまざまなスペースの制約や保管要件に合わせたモジュラー設計を提供しており、カスタマイズもカギとなっています。ロジスティクス企業やサプライチェーン・オペレーターとの戦略的パートナーシップは、顧客ネットワークの拡大や流通の合理化に役立っています。さらに、納期を短縮し、移り変わる市場の需要に迅速に対応するため、企業はより強力な地域サプライチェーンや地域製造ハブを構築しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 都市型倉庫とマイクロフルフィルメントセンター

- 物流・サプライチェーンネットワークの拡大

- 自動化倉庫の増加

- 冷蔵・食品物流の成長

- 業界の潜在的リスク&課題

- 既存施設のスペースと構造上の制約

- 市場間の標準化の欠如

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計(HSコード73269099)

- 主要輸入国

- 主要輸出国

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- パレットラック

- ドライブイン/ドライブスルーラック

- カンチレバーラック

- その他

第6章 市場推計・予測:収容能力別、2021年~2034年

- 主要動向

- ライトデューティ

- ミディアムデューティ

- ヘビーデューティー

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 鋼鉄

- アルミニウム

- プラスチック

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 小売・eコマース

- 自動車・製造業

- 食品・飲料

- 倉庫・物流

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第11章 企業プロファイル

- AK Material Handling Systems

- AR Racking

- Arpac

- Constructor Group

- Daifuku

- Dematic

- Gonvarri Material Handling

- Interlake Mecalux

- Jungheinrich

- Kardex Group

- Mecalux

- North American Steel Equipment

- Ridg-U-Rak

- SSI Schaefer

- Toyota Industries

目次

The Global Storage Rack Market was valued at USD 22.4 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 35.8 billion by 2034. Increasing demand for efficient, space-saving solutions in urban fulfillment hubs is fueling this growth. As urban centers face rising operational costs and space limitations, businesses are turning to high-density racking, modular shelving, and mezzanine-based structures to optimize storage. The expansion of e-commerce, especially in the quick commerce segment, has accelerated the need for rapid order picking and inventory turnover. To support this, warehouses are adopting racks that work seamlessly with automation systems like robotic picking and automated storage and retrieval systems.

Storage infrastructure is evolving rapidly alongside changes in logistics workflows and delivery timelines, with businesses prioritizing racking systems that boost operational speed and flexibility. Urban distribution centers are adopting narrow aisle racks, mobile shelving, and vertical layouts. The trend toward modularity is also strong, with businesses favoring adjustable and expandable storage solutions that can evolve with changing inventory demands. The market's transformation is being powered by a mix of adoption of automation, smart warehousing trends, and cost-efficient design solutions suited for fast-paced distribution environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.4 Billion |

| Forecast Value | $35.8 Billion |

| CAGR | 4.9% |

In 2024, the pallet racks segment contributed USD 9.6 billion and is projected to grow at a CAGR of 5.3% through 2034. These racks remain the most widely used in the market due to their adaptability, economic value, and compatibility across a range of sectors. Designed to store palletized inventory horizontally with multiple vertical tiers, pallet racks enhance warehouse efficiency and accommodate variable inventory weights and volumes. Their relevance spans key industries, including logistics, food and beverage, retail, pharma, and automotive, making them a staple in both traditional and modern warehouse formats.

The steel segment accounted for 46.8% share in 2024, maintaining its lead as the primary material of choice for storage racks, and is expected to grow at a CAGR of 5.4% from 2025 to 2034. Its high strength-to-weight ratio, longevity, and cost-efficiency make it ideal for large-scale warehousing and industrial applications. Steel racks are widely implemented in heavy-duty storage environments where they support large and dense inventory loads. Sectors like manufacturing, retail, and e-commerce rely on steel-based racks for their ability to handle bulk materials, streamline operations, and endure heavy equipment use without structural compromise.

U.S. Storage Rack Market was valued at USD 4.8 billion in 2024 and is anticipated to grow at a CAGR of 5.5% through 2034. This growth stems from the country's rapid e-commerce expansion, rising adoption of warehouse robotics, and widespread implementation of automation systems. Demand is driven by industrial sectors, logistics providers, and large-scale retailers. In addition, the development of cold chain infrastructure in pharma and food supply chains is contributing to market expansion. High labor costs in the region further incentivize investment in high-density storage to enhance productivity and reduce manual handling. The U.S. remains the dominant market in the region, followed by Mexico and Canada.

Leading players in the Storage Rack Industry include Interlake Mecalux, Dematic, Kardex Group, Toyota Industries, Constructor Group, Gonvarri Material Handling, AK Material Handling Systems, SSI Schaefer, Ridg-U-Rak, Mecalux, Daifuku, Arpac, North American Steel Equipment, AR Racking, and Jungheinrich. Top companies in the storage rack market are focusing on digital integration, product innovation, and operational efficiency to strengthen their competitive edge.

Many are investing in the development of automation-compatible racking systems to support robotics, AS/RS, and advanced warehouse software platforms. Customization is also key, with manufacturers offering modular designs tailored to different space constraints and storage requirements. Strategic partnerships with logistics firms and supply chain operators help expand client networks and streamline distribution. In addition, companies are building stronger local supply chains and regional manufacturing hubs to reduce delivery times and adapt quickly to shifting market demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Carrying capacity

- 2.2.4 Material

- 2.2.5 End use

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urban warehousing & micro fulfillment centers

- 3.2.1.2 Expansion of logistics & supply chain networks

- 3.2.1.3 Rise in automated warehousing

- 3.2.1.4 Growth of cold storage & food logistics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Space & structural constraints in existing facilities

- 3.2.2.2 Lack of standardization across markets

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code 73269099)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Pallet rack

- 5.3 Drive-in / drive-thru rack

- 5.4 Cantilever rack

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Carrying Capacity, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Light duty

- 6.3 Medium duty

- 6.4 Heavy duty

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Steel

- 7.3 Aluminum

- 7.4 Plastic

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Retail & e-commerce

- 8.3 Automotive & manufacturing

- 8.4 Food & beverage

- 8.5 Warehouse & logistics

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 AK Material Handling Systems

- 11.2 AR Racking

- 11.3 Arpac

- 11.4 Constructor Group

- 11.5 Daifuku

- 11.6 Dematic

- 11.7 Gonvarri Material Handling

- 11.8 Interlake Mecalux

- 11.9 Jungheinrich

- 11.10 Kardex Group

- 11.11 Mecalux

- 11.12 North American Steel Equipment

- 11.13 Ridg-U-Rak

- 11.14 SSI Schaefer

- 11.15 Toyota Industries

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日