|

市場調査レポート

商品コード

1773367

乗用車用ディーゼルエンジン排気バルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Passenger Vehicle Diesel Engine Exhaust Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 乗用車用ディーゼルエンジン排気バルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

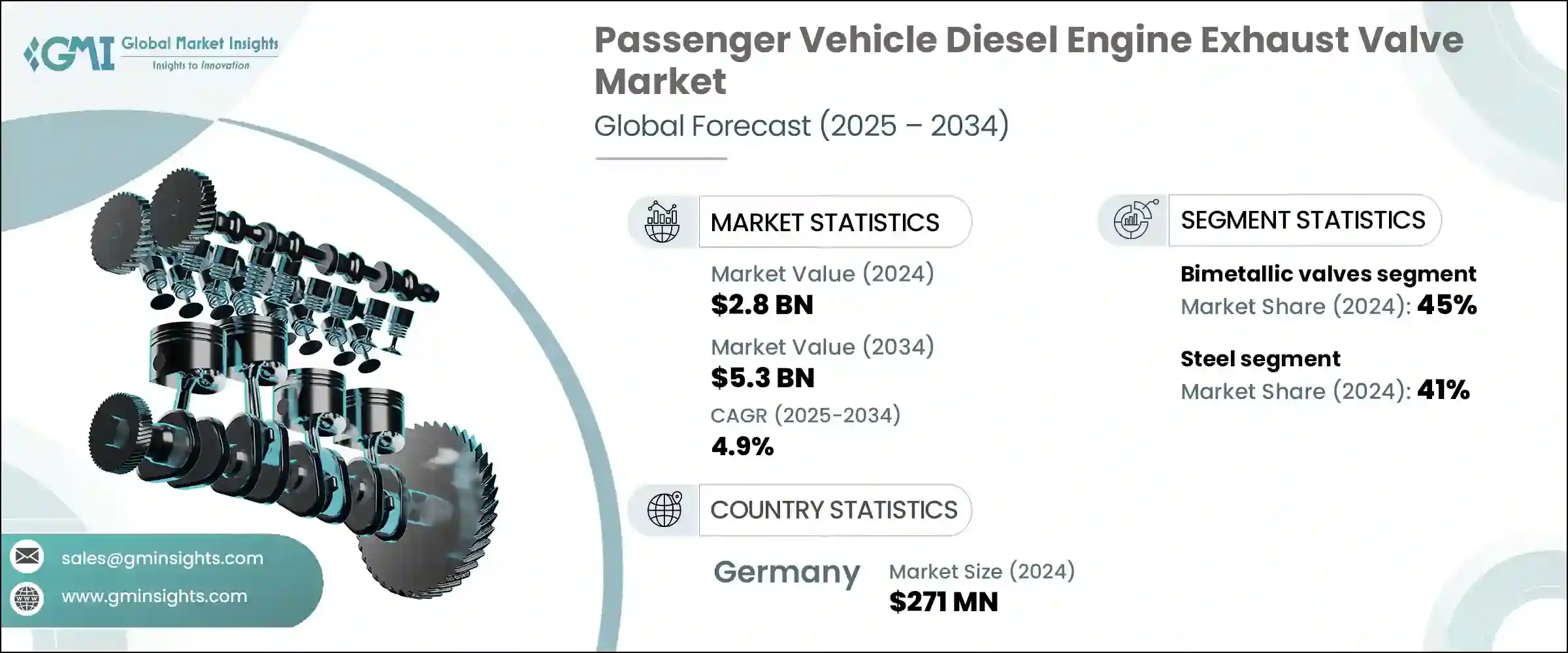

乗用車用ディーゼルエンジン排気バルブの世界市場規模は2024年に28億米ドルとなり、CAGR 4.9%で成長し、2034年には53億米ドルに達すると予測されています。

この着実な成長は、特にディーゼル乗用車が長年使用されてきた地域における自動車アフターマーケット・サービスの拡大が大きな要因となっています。自動車の所有者は、新車を購入する代わりに、排気バルブのような主要部品のメンテナンスや交換を好むようになっており、アフターマーケット分野の継続的な需要を確保しています。オンライン流通チャネルの台頭と地域の修理工場の普及により、交換部品へのアクセスがさらに向上し、バルブメーカーにとっては、相手先商標製品メーカー(OEM)契約から独立した信頼性の高い収益源が形成されています。この動向は、新車販売は停滞しているもの、アフターマーケットでのメンテナンス活動が増加している市場において特に顕著です。

研究開発の進歩は、排気バルブの性能向上に重要な役割を果たしています。特殊な表面コーティング、バイメタルバルブ設計、耐熱鋼合金の使用などの技術革新により、バルブの耐久性が向上し、排ガス規制への適合が改善され、エンジン全体の効率が最適化されました。CNC加工とデジタル検査技術によってもたらされる精密さによって、メーカーは、燃焼圧力の上昇と排出ガス規制の強化の下で運転される現代のディーゼルエンジンの厳しい条件を満たすために、バルブの形状を微調整することができるようになりました。このような技術改善により、OEMは規制要件を満たしながら、ディーゼルエンジンをパワー密度の高い乗用車に搭載し続けることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 28億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 4.9% |

2024年には、バイメタルバルブのシェアが45%で市場を独占し、2034年までCAGR 5%で成長すると予測されます。バイメタルバルブの人気は、強度と耐熱性が非常に優れていることに起因しており、極端な熱と圧力の下で作動するディーゼルエンジンに最適です。これらのバルブは通常、耐熱オーステナイト鋼のヘッドとマルテンサイト鋼またはクロム鋼のステムを組み合わせており、厳しいエンジン環境において優れた性能と長寿命を提供します。

スチールバルブ分野は2024年に41%のシェアを占め、2025年から2034年にかけてCAGR 4%で成長すると予測されています。スチールバルブは、チタンやニッケル合金のような高価な代替品よりも伝統的な鍛造や機械加工プロセスを好む既存の製造インフラにより、最も費用対効果の高い選択肢であり続けています。高級鋼バルブは、過酷な使用条件、腐食、摩耗に対して顕著な耐性を示します。クロム、モリブデン、バナジウム合金の配合により、耐久性、耐クリープ性、疲労寿命が向上し、特にリーンバーンディーゼルエンジンやターボチャージャー付きディーゼルエンジンに、高価な材料を使用することなくメリットをもたらします。

ドイツ乗用車用ディーゼルエンジン排気バルブ2024年の市場シェアは25%、売上高は2億7,100万米ドル。ドイツの自動車セクターは、確立された生産エコシステムの恩恵を受けており、ディーゼル技術への継続的な取り組みが排気バルブの安定した需要を支えています。ドイツのメーカーは、東欧、ラテンアメリカ、アフリカなどの輸出市場向けのプレミアムディーゼルSUV、多目的車、セダンの生産量を増やす構えです。欧州の多くが電動モビリティにシフトする中、ドイツはクリーンディーゼル規制に強く重点を置き、Euro 6d基準に適合させ、ディーゼルエンジン分野での地位を強化しています。

世界の乗用車用ディーゼルエンジン排気バルブ市場で競争している主要企業は、Mahle、Aisan、Fuji Oozx、Eaton、Rane、Nittan、Dengyun Auto Parts、SSV、Yangzhou Guanghui、Tennecoなどです。これらの企業は、継続的な製品革新と戦略的提携を通じて、市場力学を形成しています。乗用車用ディーゼルエンジン排気バルブ市場における足場を固めるため、各社はバルブの耐久性と排出ガス規制への適合性を向上させるため、材料と製造プロセスの革新を優先しています。各社は研究開発に多額の投資を行い、ますます厳しくなる規制基準を満たす高度な表面コーティングやバイメタル設計を開発しています。企業はまた、現地のサービスプロバイダと提携し、eコマースプラットフォームを強化することで、アフターマーケットの流通網を拡大し、世界中の交換部品へのアクセスを容易にすることにも注力しています。OEMとの戦略的提携は、これらのメーカーが長期供給契約を確保することを可能にすると同時に、ディーゼル車の保有台数が老朽化している地域におけるアフターマーケットの成長を狙っています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- ディーゼルエンジン搭載SUVとセダンの需要増加

- 高トルクと燃費効率の要件

- エンジンの耐久性への重点化

- プレミアムおよび多目的セグメントの増加

- 業界の潜在的リスク&課題

- ディーゼル乗用車の世界の需要減少

- 厳しい排出規制によりコンプライアンスコストが増加

- 市場機会

- 大型ディーゼルSUVとMPVの需要増加

- 厳しい排出ガス規制がバルブの革新を促進

- バルブ交換によるアフターマーケットの成長

- バルブ材料と設計の進歩

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- ケーススタディ

- ユースケース

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:バルブタイプ別、2021年~2034年

- 主要動向

- モノメタルバルブ

- バイメタルバルブ

- 中空バルブ

- ナトリウム充填バルブ

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- ハッチバック

- セダン

- SUV

- MPV(多目的車)

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 鋼鉄

- チタン

- ニッケル基合金

- その他

第8章 市場推計・予測:エンジンタイプ別、2021年~2034年

- 主要動向

- ターボチャージャー付きディーゼルエンジン

- 自然吸気ディーゼルエンジン

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM(オリジナル機器メーカー)

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aisan

- AnFu

- Burg

- Dengyun Auto-parts

- Eaton

- Ferrea

- Fuji Oozx

- JinQingLong

- Mahle

- Nittan

- Rane

- ShengChi

- SSV

- Tenneco(including Federal-Mogul)

- Tongcheng

- Tyen Machinery

- Wode Valve

- Worldwide Auto

- Xin Yue

- Yangzhou Guanghui

The Global Passenger Vehicle Diesel Engine Exhaust Valve Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 5.3 billion by 2034. This steady growth is largely fueled by the expansion of automotive aftermarket services, especially in regions where diesel passenger vehicles have been in use for many years. Instead of purchasing new cars, vehicle owners increasingly prefer maintaining and replacing key components like exhaust valves, ensuring ongoing demand in the aftermarket sector. The rise of online distribution channels and the widespread availability of local repair shops has further enhanced access to replacement parts, creating reliable revenue streams for valve manufacturers independent of original equipment manufacturer (OEM) contracts. This trend is particularly significant in markets with stagnant new vehicle sales but rising aftermarket maintenance activities.

Advancements in research and development are playing a critical role in enhancing exhaust valve performance. Innovations such as specialized surface coatings, bimetallic valve designs, and the use of heat-resistant steel alloys have extended valve durability, improved emissions compliance, and optimized overall engine efficiency. The precision afforded by CNC machining and digital inspection technologies has allowed manufacturers to fine-tune valve geometries to meet the demanding conditions of modern diesel engines, which operate under increased combustion pressures and tighter emissions standards. These technological improvements enable OEMs to continue integrating diesel engines into power-dense passenger vehicles while meeting regulatory requirements.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.9% |

In 2024, bimetallic valves dominated the market by 45% share and are forecasted to grow at a CAGR of 5% through 2034. Their popularity stems from their exceptional blend of strength and thermal resistance, making them ideal for diesel engines operating under extreme heat and pressure. These valves typically feature a heat-resistant austenitic steel head combined with a martensitic or chrome steel stem, offering superior performance and longevity in demanding engine environments.

The steel valve segment accounted for 41% share in 2024 and is projected to grow at a CAGR of 4% between 2025 and 2034. Steel valves remain the most cost-effective option due to existing manufacturing infrastructure that favors traditional forging and machining processes over more expensive alternatives like titanium or nickel alloys. High-grade steel valves demonstrate remarkable resistance to harsh operating conditions, corrosion, and wear. The inclusion of chromium, molybdenum, and vanadium alloys enhances their durability, creep resistance, and fatigue life, particularly benefiting lean burn and turbocharged diesel engines without the need for costly materials.

Germany Passenger Vehicle Diesel Engine Exhaust Valve Market held a 25% share and generated USD 271 million in 2024. Germany's automotive sector benefits from a well-established production ecosystem and its continued commitment to diesel technology supports steady demand for exhaust valves. German manufacturers are poised to increase the output of premium diesel SUVs, multi-purpose vehicles, and sedans destined for export markets including Eastern Europe, Latin America, and Africa. While much of Europe shifts toward electric mobility, Germany maintains a strong focus on clean diesel compliance, aligning with Euro 6d standards and reinforcing its position in the diesel engine segment.

Key players competing in the Global Passenger Vehicle Diesel Engine Exhaust Valve Market include Mahle, Aisan, Fuji Oozx, Eaton, Rane, Nittan, Dengyun Auto Parts, SSV, Yangzhou Guanghui, and Tenneco. These companies collectively shape market dynamics through continuous product innovation and strategic collaborations. To strengthen their foothold in the passenger vehicle diesel engine exhaust valve market, companies prioritize innovation in materials and manufacturing processes to improve valve durability and emissions compliance. They invest heavily in R&D to develop advanced surface coatings and bimetallic designs that meet increasingly strict regulatory standards. Firms also focus on expanding aftermarket distribution networks by partnering with local service providers and enhancing e-commerce platforms, ensuring easier access to replacement parts worldwide. Strategic alliances with OEMs enable these manufacturers to secure long-term supply contracts while simultaneously targeting aftermarket growth in regions with aging diesel vehicle fleets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Valve type

- 2.2.3 Vehicle

- 2.2.4 Material

- 2.2.5 Engine type

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for diesel-powered SUVs & sedans

- 3.2.1.2 High torque & fuel efficiency requirements

- 3.2.1.3 Increasing focus on engine durability

- 3.2.1.4 Rise in premium & multipurpose segments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Declining global demand for diesel passenger vehicles

- 3.2.2.2 Stringent emission regulations increasing compliance costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for heavy-duty diesel SUVs and MPVs

- 3.2.3.2 Stricter emission norms driving valve innovation

- 3.2.3.3 Aftermarket growth from valve replacements

- 3.2.3.4 Advancements in valve material and design

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Valve Type, 2021 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Monometallic valves

- 5.3 Bimetallic valves

- 5.4 Hollow valves

- 5.5 Sodium-filled valves

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUVs

- 6.5 MPV (multi-purpose vehicle)

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Steel

- 7.3 Titanium

- 7.4 Nickel-based alloys

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Engine type, 2021 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 Turbocharged diesel engine

- 8.3 Naturally aspirated diesel engine

Chapter 9 Market Estimates & Forecast, By Sales channel, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 OEMs (Original equipment manufacturers)

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisan

- 11.2 AnFu

- 11.3 Burg

- 11.4 Dengyun Auto-parts

- 11.5 Eaton

- 11.6 Ferrea

- 11.7 Fuji Oozx

- 11.8 JinQingLong

- 11.9 Mahle

- 11.10 Nittan

- 11.11 Rane

- 11.12 ShengChi

- 11.13 SSV

- 11.14 Tenneco (including Federal-Mogul)

- 11.15 Tongcheng

- 11.16 Tyen Machinery

- 11.17 Wode Valve

- 11.18 Worldwide Auto

- 11.19 Xin Yue

- 11.20 Yangzhou Guanghui