ヒツジおよびヤギ用機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Sheep and Goat Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 260 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773366

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

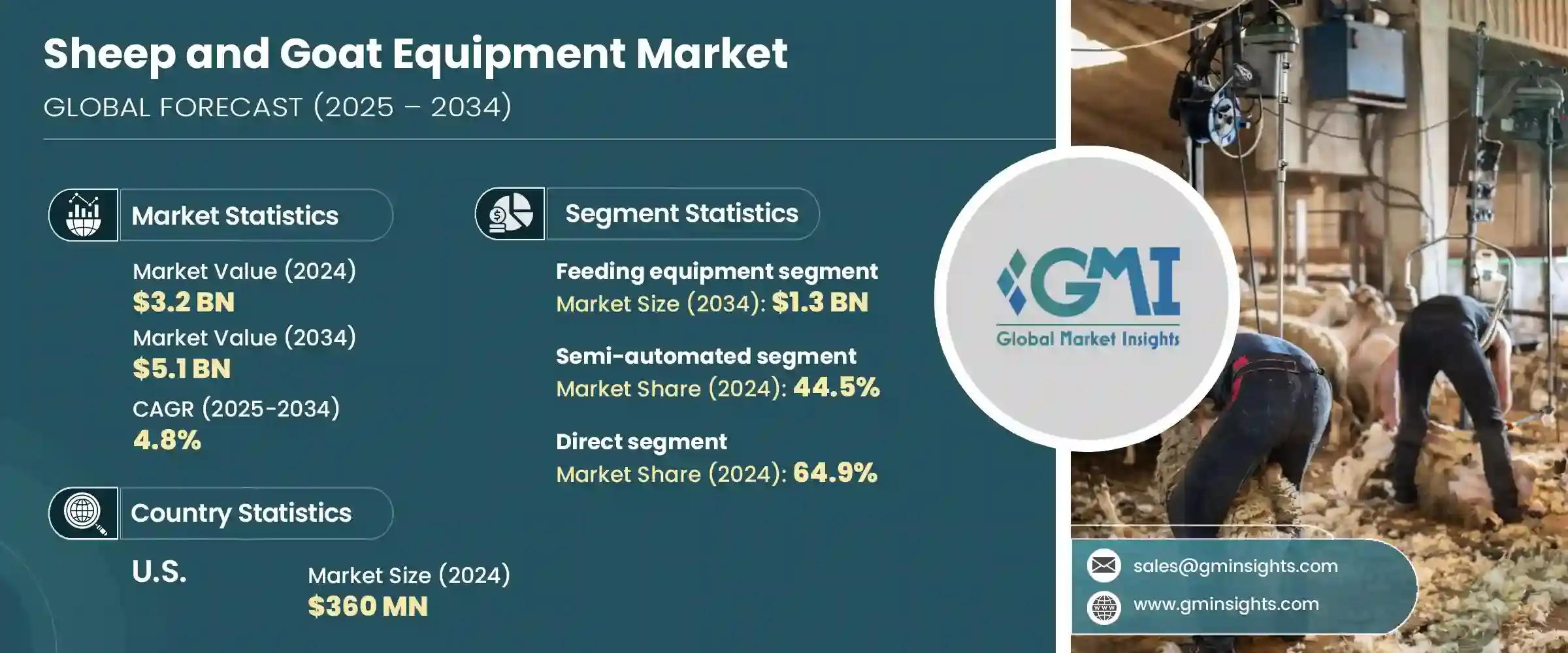

世界のヒツジおよびヤギ用機器市場は、2024年には32億米ドルとなり、CAGR 4.8%で成長し、2034年には51億米ドルに達すると推定されています。

農法が近代化し、家畜を管理するためのより効率的な方法が採用され続けているため、この業界は大きな変革期を迎えています。農家は、生産性を向上させ、手作業への依存を減らす革新的な機器ソリューションにますます注目するようになっています。日々の作業を合理化する必要性が高まる中、機械化された給餌ツール、高度なせん断システム、精密モニタリング装置などの機器は、畜産農場にとって不可欠な要素になりつつあります。

自動化システムの採用は、生産者が給餌ルーチンの一貫性、労働集約的作業の時間節約、動物福祉の向上といった利点を認識するにつれて増加しています。特に家畜飼料は経営経費の大部分を占めるため、酪農家は資源の最適化に注力しています。機器の技術的統合は、飼料の無駄や人件費の削減に役立つだけでなく、病気の早期発見や行動追跡を通じて、家畜の健康管理の向上にも役立っています。このような技術革新は、畜産経営の管理方法を再構築し、今後10年間の市場の安定成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 32億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 4.8% |

機器タイプ別では、給餌機器が圧倒的な地位を占めており、2024年のセグメント評価額は8億米ドルでした。このカテゴリーは着実に成長し、2034年には13億米ドルに達すると予測されます。飼料管理用に設計された機器は、生産者が飼料ロスを減らし、流通効率を向上させるのに役立つため、引き続き強い需要があります。自動ディスペンサー、精密フィーダー、その他の給餌ツールは、動物の健康的な成長をサポートし、畜産における最も高い運用コストの1つである飼料の無駄を最小限に抑えることができるため、好まれています。

操作モード別市場を見ると、2024年の世界収益シェアの約44.5%を半自動機器が占めています。この分野は予測期間中、CAGR 4.4%で拡大すると予想されます。これらのシステムは、自動化と手動制御のバランスを取ろうとする中規模および大規模農家にとってますます魅力的になってきています。作業速度の向上、安定した性能、手作業への依存度の低減を提供できることから、特に農業労働力不足に直面している地域では、効率的な選択肢となっています。

流通チャネルは、製品の入手しやすさとサービスの質を決定する上で重要な役割を果たします。2024年には、直接流通分野が約64.9%のシェアで市場を独占します。このモデルは、メーカーがエンドユーザーと直接関わることを可能にし、機器のより良いカスタマイズを可能にし、特定の農業ニーズに対応する機会を提供します。また、リアルタイムのフィードバック収集もサポートするため、メーカーは市場力学の変化に応じて自社の製品を適応させることができます。ダイレクト・チャネルはロジスティクスにもメリットをもたらし、特に季節的な需要急増時には、迅速な納品とスムーズな在庫の流れを確保します。

地域別では、米国が世界的に強い存在感を示しており、2024年の市場規模は3億6,000万米ドルでした。同国は2025年から2034年にかけてCAGR 5.1%の成長が見込まれています。米国の畜産部門は、近代的な農業インフラと肉、牛乳、羊毛の需要増に支えられて拡大を続けています。米国の農法に合わせた高性能機器が入手可能なことも、業界の上昇軌道に大きく寄与しています。

北米全体も、持続可能な農業と家畜管理の革新を奨励する政策に支えられ、着実な進歩を遂げています。責任ある資源利用と農機具のデジタル統合が重視され、世界市場におけるこの地域の地位が強化されています。

この進化する市場において、メーカーはエネルギー効率の高いシステム、耐久性の強化、ヒツジおよびヤギ農家の多様な要求に応えるオーダーメイド機能の提供に注力しています。また、アフターセールス・サービスや地域のサポート・インフラも重視されるようになっています。新興市場では、フィーダー、フェンシングユニット、電子識別(EID)スケール、移動式ハンドリングシステムなど、費用対効果が高く、かつ信頼性の高い機器への需要が高まっています。このような優先課題は、世界の畜産業界のニーズに対応し、ポートフォリオを拡大する中で、主要な業界参加者の戦略的方向性を形成し続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 機器タイプ別

- 規制の枠組み

- 規格と認証

- 環境規制

- 輸出入規制

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーターのファイブフォース分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:機器タイプ別、2021年~2034年

- 主要動向

- 給餌器具

- 飼料ミキサー

- 飼料ディスペンサー

- 干し草フィーダー

- ミネラルフィーダー

- ハンドリング機器

- ゲートとパネル

- シュート

- 選別システム

- 積載ランプ

- せん断装置

- 電動ハサミ

- 手動ハサミ

- せん断プラットフォーム

- その他

- 計量機器

- デジタル家畜用体重計

- プラットフォームスケール

- 移動式計量システム

- ポータブルウェイトクレート

- ウォークスルー計量システム

- その他

- トリミング機器

- 蹄切り

- 羊毛鋏

- 電動バリカン

- その他

- 散水設備

- 自動給水器

- 水槽

- 水ろ過システム

- その他

- 飼育設備

- 人工授精ツール

- 超音波装置

- 子羊の飼育小屋

- 熱検知装置

- その他

- 健康管理機器

- ワクチン銃

- 散水装置

- 医療用品保管

- その他

第6章 市場推計・予測:動作モード別、2021年~2034年

- 主要動向

- 手動機器

- 半自動装置

- 全自動機器

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 個人農家

- 協同組合

- 商業農業

- と畜場

- 研究施設

- その他

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第9章 市場推計・予測:地域別、2021年~2034年

- 主な傾向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

第10章 企業プロファイル

- Allflex Livestock Intelligence

- Arrowquip

- Gallagher

- Heiniger

- IAE

- Kerbl

- Lister Shearing

- Premier 1 Supplies

- Priefert

- Ritchie Agricultural

- Stockpro

- Sydell Inc.

- Te Pari Products

- Tru-Test(Datamars)

- WOPA

目次

The Global Sheep and Goat Equipment Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 5.1 billion by 2034. The industry is undergoing a major transformation as farming practices continue to modernize and adopt more efficient methods for managing livestock. Farmers are increasingly turning to innovative equipment solutions that improve productivity and reduce the reliance on manual labor. With the growing need to streamline daily operations, equipment like mechanized feeding tools, advanced shearing systems, and precision monitoring devices is becoming an essential component of livestock farms.

The adoption of automated systems is rising as producers recognize the benefits of consistency in feeding routines, time savings in labor-intensive tasks, and enhanced animal welfare. Farmers are focusing on optimizing their resources, especially as livestock feed accounts for a large portion of operational expenses. Technological integration in equipment is not only helping reduce feed waste and labor costs but also supports better health management of animals through early disease detection and behavioral tracking. These innovations are reshaping how livestock operations are managed, pushing the market toward consistent growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 4.8% |

In terms of equipment type, feeding equipment held a dominant position, with the segment valued at USD 800 million in 2024. This category is projected to grow steadily and reach USD 1.3 billion by 2034. Equipment designed for feed management continues to see strong demand as it helps producers reduce feed loss and improve distribution efficiency. Automatic dispensers, precision feeders, and other feeding tools are being preferred due to their ability to support healthier animal growth and minimize feed waste, which remains one of the highest operational costs in livestock farming.

The market based on operation mode shows that semi-automated equipment accounted for approximately 44.5% of the global revenue share in 2024. This segment is expected to expand at a CAGR of 4.4% during the forecast period. These systems are becoming increasingly attractive to mid-scale and large-scale farmers who seek to strike a balance between automation and manual control. Their ability to offer improved operational speed, consistent performance, and reduced dependence on manual labor makes them an efficient alternative, especially in regions facing agricultural workforce shortages.

Distribution channels play a key role in determining product accessibility and service quality. In 2024, the direct distribution segment dominated the market with a share of around 64.9%. This model allows manufacturers to engage directly with end users, enabling better customization of equipment and providing the opportunity to address specific farming needs. It also supports real-time feedback collection, allowing manufacturers to adapt their offerings based on changing market dynamics. The direct channel also benefits logistics, ensuring quicker deliveries and smoother inventory flow, particularly during seasonal demand spikes.

Regionally, the United States held a strong presence in the global landscape, with the market valued at USD 360 million in 2024. The country is expected to see growth at a CAGR of 5.1% between 2025 and 2034. The U.S. livestock sector continues to expand, bolstered by modern farming infrastructure and rising demand for meat, milk, and wool. The availability of high-performance equipment tailored to U.S. farming practices contributes significantly to the industry's upward trajectory.

North America as a whole is also witnessing steady progress, supported by policies that encourage sustainable agriculture and innovations in livestock management. The emphasis on responsible resource use and digital integration in farm equipment is strengthening the region's position in the global market.

In this evolving market, manufacturers are concentrating on offering energy-efficient systems, enhanced durability, and tailored features that cater to the diverse requirements of sheep and goat farmers. There is also an increasing emphasis on after-sales services and regional support infrastructure. In emerging markets, demand is growing for cost-effective yet reliable equipment such as feeders, fencing units, electronic identification (EID) scales, and mobile handling systems. These priorities continue to shape the strategic direction of key industry participants as they expand their portfolios and cater to the needs of the global livestock community.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Operation mode

- 2.2.4 End use

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistic

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Feeding equipment

- 5.2.1 Feed mixers

- 5.2.2 Feed dispensers

- 5.2.3 Hay feeders

- 5.2.4 Mineral feeders

- 5.3 Handling equipment

- 5.3.1 Gates and panels

- 5.3.2 Chutes

- 5.3.3 Sorting systems

- 5.3.4 Loading ramps

- 5.4 Shearing equipment

- 5.4.1 Electric shears

- 5.4.2 Manual shears

- 5.4.3 Shearing platforms

- 5.4.4 Others

- 5.5 Weighing equipment

- 5.5.1 Digital livestock scales

- 5.5.2 Platform scales

- 5.5.3 Mobile weighing systems

- 5.5.4 Portable weight crates

- 5.5.5 Walk-through weighing systems

- 5.5.6 Others

- 5.6 Trimming equipment

- 5.6.1 Hoof trimmers

- 5.6.2 Wool shears

- 5.6.3 Electric clippers

- 5.6.4 Others

- 5.7 Watering equipment

- 5.7.1 Automatic waterers

- 5.7.2 Water troughs

- 5.7.3 Water filtration systems

- 5.7.4 Others

- 5.8 Breeding equipment

- 5.8.1 Artificial insemination tools

- 5.8.2 Ultrasound machines

- 5.8.3 Lambing pens

- 5.8.4 Heat detection devices

- 5.8.5 Others

- 5.9 Health management equipment

- 5.9.1 Vaccination guns

- 5.9.2 Drenching equipment

- 5.9.3 Medical supplies storage

- 5.9.4 Others

Chapter 6 Market Estimates & Forecast, By Operation Mode, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual equipment

- 6.3 Semi-automated equipment

- 6.4 Fully automated equipment

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Individual farmers

- 7.3 Cooperatives

- 7.4 Commercial farming operations

- 7.5 Slaughterhouses

- 7.6 Research facilities

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trend

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 UAE

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Allflex Livestock Intelligence

- 10.2 Arrowquip

- 10.3 Gallagher

- 10.4 Heiniger

- 10.5 IAE

- 10.6 Kerbl

- 10.7 Lister Shearing

- 10.8 Premier 1 Supplies

- 10.9 Priefert

- 10.10 Ritchie Agricultural

- 10.11 Stockpro

- 10.12 Sydell Inc.

- 10.13 Te Pari Products

- 10.14 Tru-Test (Datamars)

- 10.15 WOPA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 260 Pages

- 納期

- 2~3営業日