褥瘡治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pressure Ulcers Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773363

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

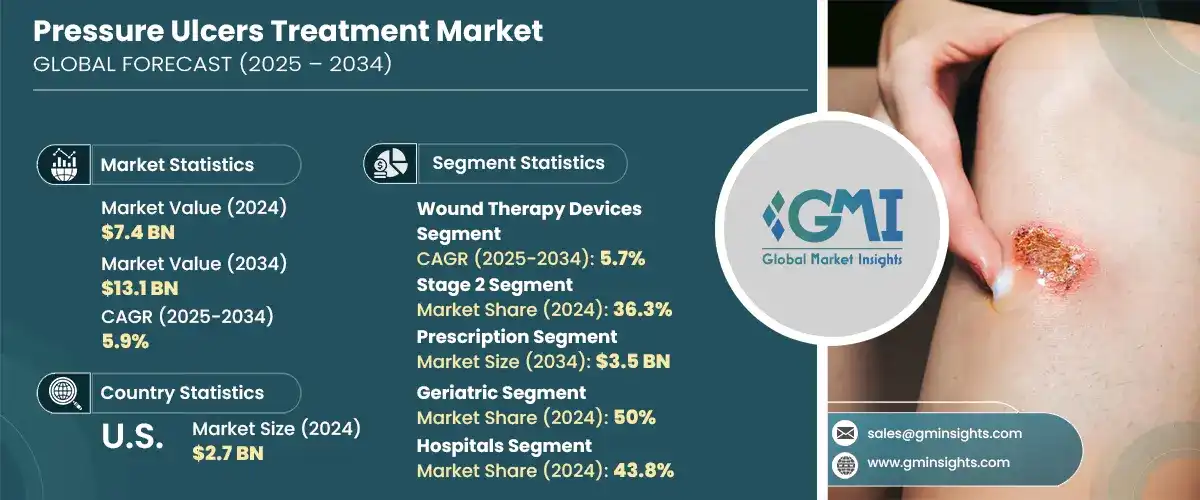

褥瘡治療の世界市場規模は、2024年に74億米ドルとなり、CAGR 5.9%で成長し、2034年には131億米ドルに達すると予測されています。

この成長の主な要因は、特に先進国における人口の高齢化であり、高齢化によって移動が制限され、長時間動けない状態が続くと、褥瘡のリスクが高まる。高齢になると、動きを妨げる症状が現れやすくなり、褥瘡の開発につながります。さらに、創傷治癒を遅らせることが知られている肥満や糖尿病などの生活習慣病が蔓延していることも、効果的な創傷治療に対する需要をさらに高めています。慢性疾患の増加は、治癒しない創傷の臨床例の増加につながり、患者の転帰を改善する高度な治療アプローチの需要に拍車をかけています。

市場はまた、創傷ケアソリューションの継続的な技術開発からも恩恵を受けています。スマート創傷被覆材、生物学的に活性な製品、最新の治療システムなどの技術革新は、治癒時間を短縮し患者の快適性を向上させることで、褥瘡管理に革命をもたらしています。これらのソリューションは複雑な創傷を管理するのに有効であるため、病院環境と在宅介護環境の両方で採用が増加しています。早期介入や予防戦略の利点に対する認識が高まり、より多くの患者や医療提供者が先進的な製品を選ぶようになっています。特に北米と欧州では、政府のヘルスケアプログラムによる支援も採用を後押ししています。保険償還制度や臨床ガイドラインにより、エビデンスに基づいた創傷治療法が好まれる傾向が強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 74億米ドル |

| 予測金額 | 131億米ドル |

| CAGR | 5.9% |

褥瘡治療には、体圧による皮膚損傷の予防と治癒を目的とした様々な医療ソリューションが含まれます。これらの潰瘍は褥瘡(床ずれ)または褥瘡(じょくそう)とも呼ばれ、一般に移動が制限された患者に発生します。治療の目的は、圧迫を和らげ、組織の回復を促し、感染を予防し、患者の健康状態を全般的に改善することです。治療の選択肢としては、創傷ケア用にデザインされた特殊なドレッシング材、生物学的製剤、治療機器、薬剤などがあります。臨床の関心が治療成績の改善にシフトするにつれ、複数の治療を組み合わせた統合的な治療アプローチが市場に浸透しつつあります。

主要製品カテゴリーの中で、創傷治療器具は2024年に33億米ドルの評価額でトップとなり、2034年にはCAGR 5.7%を記録して57億米ドルに成長すると予測されています。これらの機器には、治癒を早め、感染リスクを低減し、患者の不快感を最小限に抑える技術が含まれています。病院や外来での使用が増加していることは、複雑な創傷をより効率的に管理するための先端技術への依存が高まっていることを浮き彫りにしています。最近の体圧管理システムや自動創傷モニタリングの改良により、このセグメントの機能がさらに向上し、臨床での採用が広がっています。

タイプ別では、2024年には処方箋分野がリードし、2034年には35億米ドルに達すると推定されています。この優位性は、処方療法の有効性が高いことと、重篤な症例の治療において規制された介入が医学的に必要であることに起因しています。このカテゴリーの製品には、より複雑で慢性的な創傷に処方される高度な局所製剤や全身療法が含まれます。ヘルスケアプロバイダーは患者のニーズに基づいた個別化治療計画をますます好むようになっているため、処方薬カテゴリーは今後数年間リードを維持すると予想されます。

エンドユース別では、病院が2024年に43.8%と最大のシェアを占め、2034年には55億米ドルの売上になると予測されています。病院は包括的なインフラ、熟練した医療スタッフ、創傷ケアのための専門部門を備えているため、特に進行した褥瘡の治療の主要な拠点であり続けています。移動が困難な患者や健康上の問題を抱える患者は、集学的アプローチを効果的に展開できる病院での治療を求める傾向が強いです。さらに、外科的介入や集中治療が必要な患者が最初に接触するのは病院であることが多いです。

地域別では、北米が2024年に29億米ドルの収益を上げて世界市場をリードし、2034年にはCAGR 5.5%の成長率で50億米ドルに達すると予想されています。このリーダーシップは、ヘルスケアの枠組みが確立されていること、最先端の創傷ケア技術が早期から導入されていること、臨床研究開発に多額の投資が行われていることなどに支えられています。同地域では高齢者の数が増加し、肥満や糖尿病などの合併症の有病率が高いため、高度な治療ソリューションが必要となっています。さらに、有利な償還シナリオと強力な規制監督により、革新的な治療法の計画的な展開が可能となっています。

主要企業は広範な製品ポートフォリオ、戦略的な研究開発投資、世界な事業展開を通じて、その地位を強化し続けています。大手企業は先進的な創傷管理ソリューションを積極的に開発し、新興経済諸国でのプレゼンス拡大を図っています。合併、ライセンシング契約、製品発売などの競合情勢は、競合情勢の形成に重要な役割を果たしています。新興企業や小規模企業も、特殊な生物製剤やカスタマイズ可能なケアオプションに注力することでニッチを開拓し、業界内のイノベーションのペースを高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の上昇

- 創傷ケア技術の進歩

- 意識向上と予防ケア対策

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- 高額な治療費

- 市場機会

- 在宅ケアに基づく創傷管理の拡大

- 研究開発投資と活動の増加

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- 規制情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 創傷ケア用ドレッシング

- アルギン酸塩ドレッシング

- フォームドレッシング

- ハイドロコロイドドレッシング

- ハイドロゲルドレッシング

- フィルムドレッシング

- その他の創傷ケアドレッシング

- バイオロジック

- 皮膚代替品

- 成長因子

- その他のバイオロジック

- 創傷治療デバイス

- 陰圧創傷療法

- 高圧酸素療法

- その他の創傷治療デバイス

- 医薬品

- その他の製品

第6章 市場推計・予測:潰瘍ステージ別、2021年~2034年

- 主要動向

- ステージ1

- ステージ2

- ステージ3

- ステージ4

第7章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- OTC

- 処方

第8章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 小児

- 成人

- 高齢者

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター(ASC)

- 専門クリニック

- その他の最終用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 3M Healthcare

- AHA Hyperbarics

- Integra LifeSciences

- Ascend Laboratories

- B. Braun

- Baxter

- BioTissue

- Cardinal Health

- Coloplast

- Convatec

- Ethicon(Johnson and Johnson)

- GlaxoSmithKline(GSK)

- Ipca Laboratories

- LifeNet Health

- Medline

- MIMEDX

- Molnlycke Health Care

- Organogenesis

- Pfizer

- Smith &Nephew

- StimLabs

- Zimmer Biomet

目次

The Global Pressure Ulcers Treatment Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 13.1 billion by 2034. A major contributor to this growth is the aging population, particularly in developed nations, where limited mobility and prolonged immobility increase the risk of pressure ulcers. As individuals age, they are more likely to develop conditions that hinder movement, leading to the development of pressure sores. Additionally, the rising prevalence of lifestyle-related diseases such as obesity and diabetes-both of which are known to slow wound healing-further drives demand for effective wound care therapies. The growing incidence of chronic illnesses is translating into increased clinical cases of non-healing wounds, spurring the demand for sophisticated treatment approaches that improve patient outcomes.

The market is also benefiting from ongoing technological developments in wound care solutions. Innovations such as smart wound dressings, biologically active products, and modern therapy systems are revolutionizing pressure ulcer management by reducing healing time and improving comfort for patients. These solutions are increasingly adopted across both hospital settings and homecare environments due to their effectiveness in managing complex wounds. Greater awareness about early intervention and the benefits of preventive strategies is encouraging more patients and healthcare providers to opt for advanced products. Support from government healthcare programs, particularly in North America and Europe, is also bolstering adoption. Reimbursement schemes and clinical guidelines are reinforcing the preference for evidence-based wound care methods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 5.9% |

Pressure ulcer treatment encompasses a range of medical solutions aimed at preventing and healing pressure-induced skin injuries. These ulcers, also referred to as bedsores or decubitus ulcers, generally occur in patients with limited mobility. The goal of treatment is to relieve pressure, promote tissue recovery, prevent infection, and enhance overall patient health. Therapeutic options include specialized dressings, biologics, therapy devices, and pharmaceutical agents designed for wound care. As clinical attention shifts toward improving healing outcomes, integrated treatment approaches that combine multiple therapies are gaining ground in the market.

Among the key product categories, wound therapy devices emerged as the top-performing segment in 2024 with a valuation of USD 3.3 billion and are projected to grow to USD 5.7 billion by 2034, registering a CAGR of 5.7%. These devices include technologies that support faster healing, reduce infection risk, and minimize patient discomfort. Their increasing use in hospitals and outpatient settings highlights the growing reliance on advanced technology to manage complex wounds more efficiently. Recent improvements in pressure management systems and automated wound monitoring are further enhancing the capabilities of this segment, leading to broader clinical adoption.

In terms of type, the prescription segment led in 2024 and is estimated to reach USD 3.5 billion by 2034. This dominance can be attributed to the higher efficacy of prescription therapies and the medical necessity for regulated interventions in treating severe cases. Products in this category include advanced topical formulations and systemic therapies that are prescribed for more complex or chronic wounds. As healthcare providers increasingly favor personalized treatment plans based on patient needs, the prescription category is expected to maintain its lead over the coming years.

By end use, hospitals represented the largest share of the market in 2024, accounting for 43.8%, and are projected to generate USD 5.5 billion in revenue by 2034. Hospitals remain the primary centers for treating pressure ulcers, particularly in advanced stages, owing to their comprehensive infrastructure, availability of skilled medical staff, and specialized departments for wound care. Patients with limited mobility or underlying health issues are more likely to seek hospital-based care where multidisciplinary approaches can be deployed effectively. Additionally, hospitals are often the first point of contact for patients requiring surgical intervention or intensive care.

Regionally, North America led the global market with a revenue of USD 2.9 billion in 2024 and is expected to reach USD 5 billion by 2034, growing at a CAGR of 5.5%. This leadership is supported by a well-established healthcare framework, early adoption of cutting-edge wound care technologies, and substantial investment in clinical research and development. The rising number of elderly individuals and the high prevalence of comorbid conditions such as obesity and diabetes in the region make advanced treatment solutions a necessity. Furthermore, favorable reimbursement scenarios and strong regulatory oversight have enabled a structured rollout of innovative therapies.

Leading companies continue to strengthen their positions through extensive product portfolios, strategic R&D investment, and global reach. Major participants are actively developing advanced wound management solutions and expanding their presence in emerging economies. Competitive strategies such as mergers, licensing agreements, and product launches are playing a vital role in shaping the landscape. Startups and smaller firms are also carving out a niche by focusing on specialized biologics and customizable care options, intensifying the pace of innovation within the industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Ulcer stage

- 2.2.4 Type

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease

- 3.2.1.2 Growing advancement in wound care technologies

- 3.2.1.3 Increasing awareness and preventive care measures

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding homecare-based wound management

- 3.2.3.2 Growing R&D investment and activities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wound care dressings

- 5.2.1 Alginate dressings

- 5.2.2 Foam dressings

- 5.2.3 Hydrocolloid dressings

- 5.2.4 Hydrogel dressings

- 5.2.5 Film dressings

- 5.2.6 Other wound care dressings

- 5.3 Biologics

- 5.3.1 Skin substitutes

- 5.3.2 Growth factors

- 5.3.3 Other biologics

- 5.4 Wound therapy devices

- 5.4.1 Negative pressure wound therapy

- 5.4.2 Hyperbaric oxygen therapy

- 5.4.3 Other wound therapy devices

- 5.5 Medications

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Ulcer Stage, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Stage 1

- 6.3 Stage 2

- 6.4 Stage 3

- 6.5 Stage 4

Chapter 7 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Over-the-counter (OTC)

- 7.3 Prescription

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pediatric

- 8.3 Adult

- 8.4 Geriatric

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers (ASCs)

- 9.4 Specialty clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M Healthcare

- 11.2 AHA Hyperbarics

- 11.3 Integra LifeSciences

- 11.4 Ascend Laboratories

- 11.5 B. Braun

- 11.6 Baxter

- 11.7 BioTissue

- 11.8 Cardinal Health

- 11.9 Coloplast

- 11.10 Convatec

- 11.11 Ethicon (Johnson and Johnson)

- 11.12 GlaxoSmithKline (GSK)

- 11.13 Ipca Laboratories

- 11.14 LifeNet Health

- 11.15 Medline

- 11.16 MIMEDX

- 11.17 Molnlycke Health Care

- 11.18 Organogenesis

- 11.19 Pfizer

- 11.20 Smith & Nephew

- 11.21 StimLabs

- 11.22 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日