|

市場調査レポート

商品コード

1773362

従来型パレタイザーの市場機会と促進要因、業界動向分析、2025年~2034年予測Conventional Palletizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 従来型パレタイザーの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年06月20日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

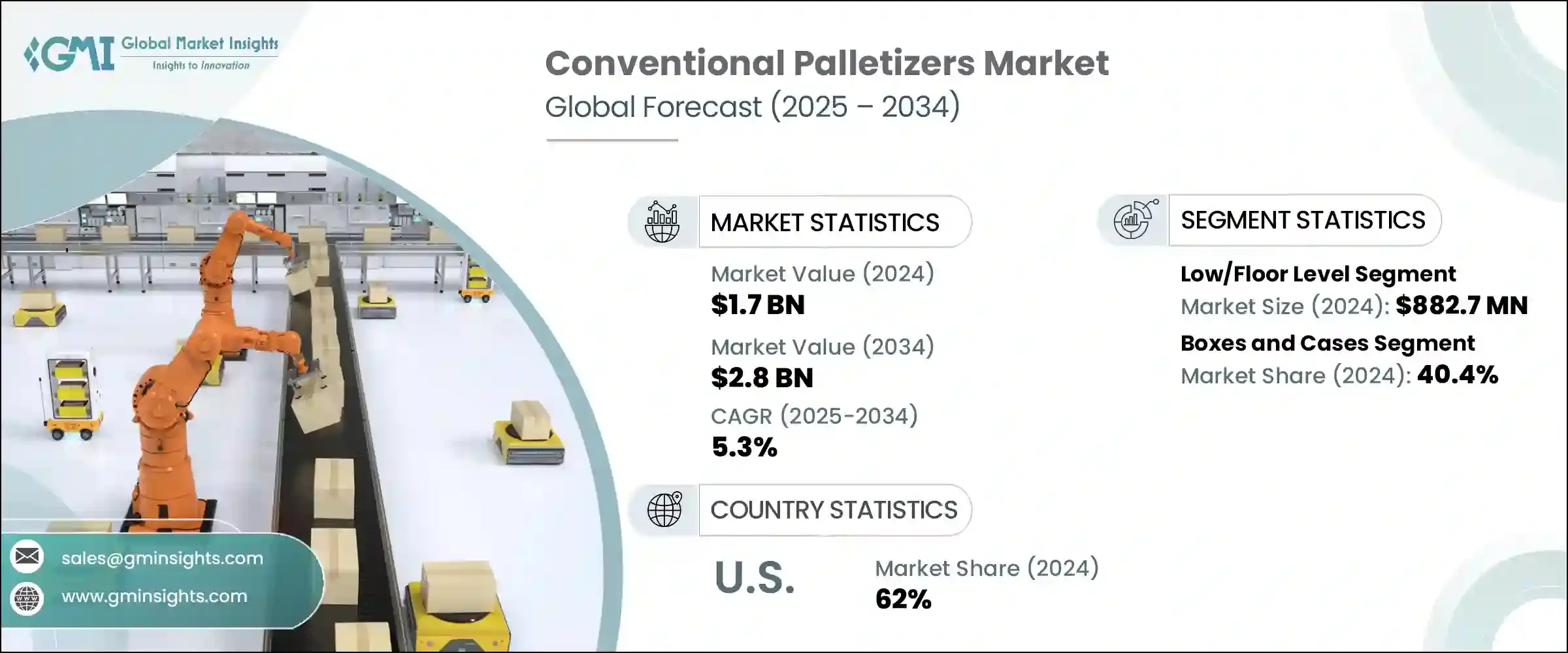

世界の従来型パレタイザー市場は、2024年には17億米ドルと評価され、CAGR 5.3%で成長し、2034年には28億米ドルに達すると推定されています。

様々な業界における合理化されたパッケージングとロジスティクス業務に対する需要の急増が、この市場の主な促進要因の一つです。eコマースが成長を続け、世界サプライチェーンがますます複雑化するにつれて、製造環境における自動パレタイジングシステムの必要性が顕著になっています。これらのシステムは、ケースや袋が流通拠点に運ばれる前に一貫したハンドリングが不可欠な場合に特に重要です。フルフィルメントセンターの多様な製品群には、ロボットによる代替が一般的に好まれていますが、従来型パレタイザーは、産業環境における高速での均一な製品積み重ねに非常に効果的です。

従来のパレタイジングシステムは、生産を中断することなく、充填パレットと空パレットのシームレスな移行を可能にすることで、パッケージングラインの効率を向上させます。この機能はワークフローを安定させ、アイドル時間を最小限に抑えます。代替ソリューションと比較して、これらのマシンはコンパクトで密閉されたスタッキング機構のおかげで、より少ないフロアスペースしか必要としません。また、設置面積が小さくなるため、広大な安全バリアも不要となり、スペースの最適化が優先される施設に最適です。大量連続生産で知られる飲食品セクターでは、乳製品、スナック菓子、缶詰などの製品を処理するために、これらの機械に大きく依存しています。従来型パレタイザーは、迅速な処理と配送を必要とする生鮮食品において、ペースの速い生産需要に対応する出力速度を維持することで信頼を得ています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 5.3% |

低床/フロアレベルパレタイザーセグメントは、2024年に8億8,270万米ドルを生み出しました。これらの機械は、パレット層に押し込む前に物品を整列させ、列に回転させるフロアレベルコンベアシステム上で動作します。上方から積み込む高所作業型とは異なり、床置き型は積み重ね時の垂直移動が不要です。この機能により、積み込み時間が短縮され、操作が簡素化されるため、より効率的で、さまざまな規模の生産フロアで利用しやすくなります。

2024年、箱・ケース部門のシェアは40.4%でした。これらのシステムは、カートンや長方形のパッケージのような均一な容器を扱うのに特に効果的です。剛性の高い形状であるため、正確な積み重ねに適しており、ミスを最小限に抑えた高速作業が可能です。食品、電子機器、医薬品、パーソナルケアアイテムなど、箱やケースは、その保護性、ブランディングのしやすさ、積み重ねの効率性から、業界を問わず、依然として支配的な包装形態です。大量生産を行うメーカーは、特に均一性と包装量が多い場合、スピードと精度を提供するパレタイジングシステムに注目します。

米国従来型パレタイザー2024年のシェアは62%。人件費の高騰と労働力不足を補う必要性から、同国のメーカーは従来型のパレタイジング・システムへの投資を増やしています。これらのシステムは、肉体的に激しく反復的な作業を自動化することで、従業員の離職率を低下させながら安全性と生産性を向上させる。自動化の推進は、製造業の成長やオンライン小売チャネルの拡大など、より広範な経済動向とも結びついており、これらすべてが高効率のエンド・オブ・ライン機器に対する需要を煽っています。

従来型パレタイザーの世界市場をリードする主要企業には、Columbia Machine Inc.、大倉洋行、ROBOPAC、MSK Covertech、Premier Tech、KUKA AG、SIPA SpA、Signode Industrial Group LLC、OCME Srl、Brenton Engineering、PAYPER SA、Concetti SpA、BW Flexible Systems、Baust &Co.GmbH、Wuxi Taiyang Packaging Technology Co.Ltd.です。従来型パレタイザー市場の各社は、食品、医薬品、物流など様々な業界の要求に応えるため、提供する機器を多様化することで市場での地位を強化しています。また、プログラマブル・ロジック・コントローラ(PLC)、ヒューマン・マシン・インターフェース(HMI)、モジュール設計など、よりスマートな技術を統合し、運用の柔軟性を高めています。アフターサービスを拡大し、保守サポートを提供することで、これらのプレーヤーは顧客維持とシステムの寿命を向上させています。システム・インテグレーターやパッケージング・オートメーション企業との戦略的提携により、メーカーは完全なターンキー・ソリューションを提供できるようになり、顧客の価値を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- eコマースと物流の成長

- 飲食品業界からの需要の高まり

- さまざまな業界における人件費の増加と自動化の導入

- 業界の潜在的リスク&課題

- 初期投資と維持費が高め

- 製品バリエーションの柔軟性が限られている

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 高レベル

- 低/フロアレベル

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 箱とケース

- バッグと袋

- トレイと木箱

- その他

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品

- 消費財

- eコマースと物流

- その他

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Baust &Co GmbH

- Brenton Engineering

- BW Flexible Systems

- Columbia Machine Inc

- Concetti SpA

- KUKA AG

- MSK Covertech

- OCME Srl

- Okura Yusoki

- PAYPER SA

- Premier Tech

- ROBOPAC

- Signode Industrial Group LLC

- SIPA SpA

- Wuxi Taiyang Packaging Technology Co Ltd

The Global Conventional Palletizers Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 2.8 billion by 2034. The surge in demand for streamlined packaging and logistics operations across various industries is one of the primary drivers for this market. As e-commerce continues to grow and global supply chains become increasingly complex, the need for automated palletizing systems in manufacturing environments has become more pronounced. These systems are particularly important where consistent handling of cases or bags is essential before they are transported to distribution hubs. While robotic alternatives are commonly favored for varied product assortments in fulfillment centers, conventional palletizers remain highly effective for uniform product stacking at high speeds in industrial settings.

Conventional palletizing systems improve packaging line efficiency by enabling seamless transitions between filled and empty pallets without disrupting production. This capability keeps the workflow steady and minimizes idle time. Compared to alternative solutions, these machines require less floor space thanks to their compact and enclosed stacking mechanisms. The reduced footprint also eliminates the need for expansive safety barriers, making them ideal for facilities where space optimization is a priority. The food and beverage sector, known for its high-volume continuous production, relies heavily on these machines to handle products like dairy, snacks, and canned goods. With perishable goods requiring quick processing and delivery, conventional palletizers are trusted to maintain output speeds that align with fast-paced production demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.3% |

The low/floor-level palletizer segment generated USD 882.7 million in 2024. These machines operate on a floor-level conveyor system that aligns and rotates items into rows before pushing them into pallet layers. Unlike their high-level counterparts, which load from above, floor-level units eliminate the need for vertical movement during stacking. This feature reduces load time and increases operational simplicity, making them more efficient and accessible across production floors of varying sizes.

In 2024, the boxes and cases segment held a 40.4% share. These systems are particularly effective at handling uniform containers such as cartons and rectangular packages. Their rigid form makes them suitable for precise stacking, allowing for high-speed operations with minimal error. Whether it's food, electronics, pharmaceuticals, or personal care items, boxes, and cases remain a dominant packaging format across industries due to their protective nature, ease of branding, and stacking efficiency. Manufacturers dealing in mass production turn to palletizing systems that offer speed and accuracy, especially where uniformity and packaging volume are high.

United States Conventional Palletizers Market held a 62% share in 2024. The need to offset rising labor costs and workforce shortages has prompted manufacturers in the country to increase investments in conventional palletizing systems. These systems automate physically intense and repetitive tasks, thereby improving safety and productivity while reducing employee turnover. The push for automation is also tied to broader economic trends, including manufacturing growth and the expansion of online retail channels, which are all fueling demand for high-efficiency end-of-line equipment.

Key companies leading the Global Conventional Palletizers Market include Columbia Machine Inc., Okura Yusoki, ROBOPAC, MSK Covertech, Premier Tech, KUKA AG, SIPA SpA, Signode Industrial Group LLC, OCME Srl, Brenton Engineering, PAYPER SA, Concetti SpA, BW Flexible Systems, Baust & Co. GmbH, and Wuxi Taiyang Packaging Technology Co. Ltd. Companies in the conventional palletizers market are strengthening their market position by diversifying their equipment offerings to cater to various industry requirements, including food, pharmaceuticals, and logistics. They are also integrating smarter technologies such as programmable logic controllers (PLCs), human-machine interfaces (HMIs), and modular designs to enhance operational flexibility. By expanding after-sales services and providing maintenance support, these players are improving customer retention and system longevity. Strategic collaborations with system integrators and packaging automation firms allow manufacturers to offer complete turnkey solutions, increasing value to clients.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of e-commerce and logistics

- 3.2.1.2 Rising demand from the food and beverages industry

- 3.2.1.3 Increased labor costs and adoption of automation in various industries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Limited flexibility for product variation

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 High level

- 5.3 Low/floor level

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Boxes and cases

- 6.3 Bags and sacks

- 6.4 Trays and crates

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.3 Pharmaceuticals

- 7.4 Consumer goods

- 7.5 E-commerce and logistics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution channel, 2021 – 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Baust & Co GmbH

- 10.2 Brenton Engineering

- 10.3 BW Flexible Systems

- 10.4 Columbia Machine Inc

- 10.5 Concetti SpA

- 10.6 KUKA AG

- 10.7 MSK Covertech

- 10.8 OCME Srl

- 10.9 Okura Yusoki

- 10.10 PAYPER SA

- 10.11 Premier Tech

- 10.12 ROBOPAC

- 10.13 Signode Industrial Group LLC

- 10.14 SIPA SpA

- 10.15 Wuxi Taiyang Packaging Technology Co Ltd