|

市場調査レポート

商品コード

1773361

米でん粉の市場機会、成長促進要因、産業動向分析と2025年~2034年予測Rice Starch Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 米でん粉の市場機会、成長促進要因、産業動向分析と2025年~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

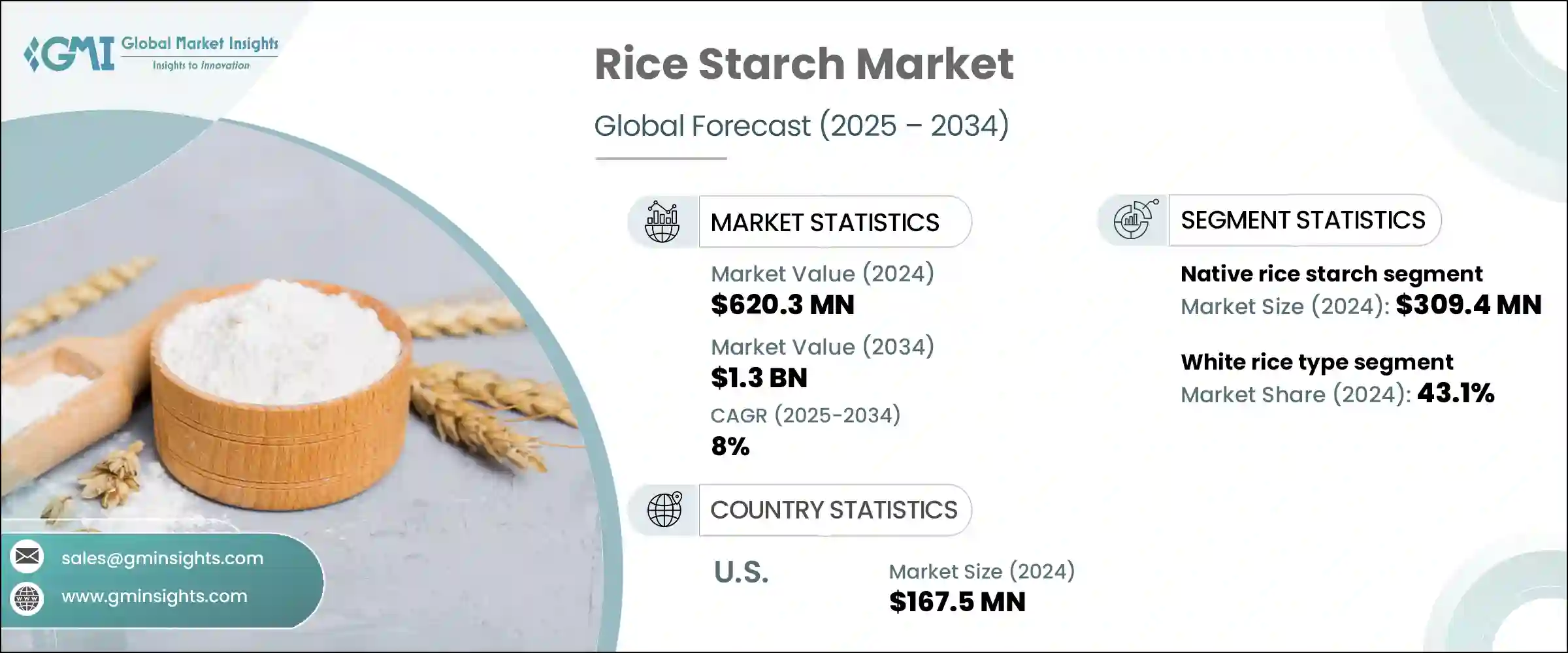

米でん粉の世界市場は、2024年には6億2,030万米ドルとなり、CAGR 8%で成長し、2034年には13億米ドルに達すると予測されています。

この市場拡大の原動力となっているのは、複数の業界で米でん粉の採用が増加していることです。本分析では、過去の実績と将来の予測をバランスよく提供し、市場全体の軌跡に関する貴重な洞察を提供します。潜在的な投資家を惹きつけるために、市場の価値と数量の両方を分析しています。一貫した成長は、クリーンラベル原料への需要の高まりと、天然食品成分への幅広い消費者シフトに支えられてきました。飲食品セクターは依然として主要な牽引役であり、米でん粉の増粘、食感改良、安定化などの多機能特性により、製品配合に広く採用されています。グルテンフリーやアレルゲンフリーの製品に対する需要の急増が、この動向にさらに拍車をかけています。

さらに、従来は成長が鈍化していた分野で新たな革新的用途が登場しており、市場セグメンテーション市場全体の拡大に大きく貢献するものと思われます。こうした開発用途は、急成長産業で見られる勢いを補完し強化する新たな需要の流れを生み出します。特殊な医薬品製剤、高度な化粧品、ニッチな食品用途など、最終用途事例を多様化することで、これらの新興セクターは成長を安定させ、業界横断的な統合の機会を開きます。このような広範な採用は、販売量の増加を促進するだけでなく、研究開発への投資を促し、製品イノベーションを促進し、メーカーがこれまで未開拓だった市場に参入することを可能にします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 6億2,030万米ドル |

| 予測金額 | 13億米ドル |

| CAGR | 8% |

2024年の天然米でん粉分野の評価額は3億940万米ドルで、2034年までのCAGRは7.9%と予測されます。天然米でん粉は、さまざまな業界で幅広く使用されているため、引き続き市場を独占しています。特に、粉砕由来の形態、汎用性、クリーンラベル要件との整合性から支持されています。乳製品、ソース、乳幼児用栄養剤などの製品において、増粘、ゲル化、安定化機能を活用し、飲食品産業が天然米でん粉の最大の消費者基盤を占めています。天然由来で機能的な利点があるため、多くの製剤に欠かせない成分となっています。

白米タイプのセグメントは2024年に2億6,740万米ドルを占め、2034年までCAGR 8.1%で成長し、43.1%のシェアを占めると予想されています。白米は加工のしやすさ、豊富な入手可能性、ニュートラルな風味プロファイルにより、依然として米でん粉の主要供給源です。消費者も製造業者も白米由来の米でん粉を好むのは、安定した高品質の収量が得られるためであり、優れたデンプン品質が求められる食品、医薬品、化粧品への使用に理想的です。大規模な生産者も、標準化された特性と効率的な抽出方法から白米を好んでいます。さらに、有機食品や最小限の加工食品への関心の高まりが、高級食材として認識されつつある白米の米でん粉需要を押し上げています。

米国の米でん粉市場は2024年に1億6,750万米ドルとなり、2025年から2034年にかけてCAGR 7.8%で成長すると予測されています。米国の成長の背景には、クリーンラベル、グルテンフリー、植物由来の食材に対する嗜好の高まりがあります。飲食品業界は、特にベーカリー、乳製品、コンビニエンス・フードの用途において、引き続き主要な消費者です。米でん粉の低刺激性や生分解性の特性により、医薬品や化粧品分野でも需要が増加しています。加工技術の進歩により製品の品質が向上し、用途の幅が広がったため、市場の成長がさらに強まっています。米国は北米で最も活発な市場国であり、同地域全体の成長を牽引しています。

世界規模では、米でん粉市場は適度に統合されており、Roquette Freres、Cargill Incorporation、BENEO GmbH、AGRANA Beteiligungs-AG、Ingredient Incorporatedといった大手企業が競争をリードしています。これらの企業は大きな市場シェアを持ち、業界動向の形成に貢献しています。米でん粉市場の主要企業は、市場での地位を強化するために様々な戦略的イニシアティブを採用しています。これらの企業は技術革新に重点を置き、製品の機能性を高め、クリーンラベルの需要に応える新しい配合や加工技術を開発しています。飲食品メーカーとの戦略的提携や協力関係は、流通網や最終用途の拡大に役立ちます。持続可能な調達と生産慣行への投資は、環境責任へのコミットメントを強化し、環境意識の高い消費者にアピールしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- クリーンラベル原料の需要増加

- グルテン不耐症の有病率の上昇

- 食品・飲料業界での応用が増加

- 医薬品・化粧品への使用拡大

- 業界の潜在的リスク&課題

- 代替デンプンとの競合

- 原材料価格の変動

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- 天然米でん粉

- 加工米でん粉

- 物理的加工

- ゼラチン化済み米でん粉

- 熱処理済み米でん粉

- その他の物理的加工米でん粉

- 化学的加工

- 相互リンクされた米でん粉

- 酸化された米でん粉

- アセチル化米でん粉

- その他の化学的加工米でん粉

- 酵素修飾

- 物理的加工

- 耐性のある米でん粉

第6章 市場推計・予測:原料別、2021~2034年

- 主要動向

- 白米

- 玄米

- 砕米と製品別

- その他

第7章 市場推計・予測:形態別、2021~2034年

- 主要動向

- 粉

- 液体とジェル

- その他

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 食品・飲料

- ベーカリー&菓子類

- 乳製品

- スープ、ソース、ドレッシング

- 肉・鶏肉製品

- スナックとコンビニ食品

- 飲み物

- ベビーフード・幼児向け製品タイプ

- グルテンフリー製品

- その他の食品用途

- 医薬品

- 錠剤の結合と崩壊

- カプセル製品ソリューション

- ドラッグデリバリーシステム

- その他の医薬品用途

- 化粧品・パーソナルケア

- スキンケア製品

- ヘアケア製品

- カラー化粧品

- その他の化粧品用途

- 紙・繊維

- 紙のサイズ加工とコーティング

- 繊維のサイジングと仕上げ

- その他の紙および繊維用途

- その他の用途

- 接着剤

- 生分解性包装

- その他の産業用途

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- A&B Ingredients

- AGRANA Beteiligungs-AG

- Agrana Group

- Anhui Lianhe

- Archer Daniels Midland Company

- Bangkok Starch Industrial Co., Ltd.

- Beneo(Sudzucker Group)

- Cargill, Incorporated

- Golden Agriculture Co., Ltd.

- Herba Ingredients

- Hunan ER-KANG

- Ingredion Incorporated

- Jiangxi Golden Agriculture Co., Ltd.

- Roquette Freres

- Shaanxi Tianyu Pharmaceutical Co., Ltd.

- Sonish Starch Technology Co., Ltd.

- Tate &Lyle PLC

- THAI WAH PUBLIC COMPANY LIMITED

- Thai Flour Industry Co., Ltd.

- Wuxi Chuangda Food Co., Ltd.

The Global Rice Starch Market was valued at USD 620.3 million in 2024 and is estimated to grow at a CAGR of 8% to reach USD 1.3 billion by 2034. This market expansion is driven by the increasing adoption of rice starch across multiple industries. The analysis provides a balanced view of past performance alongside future projections, offering valuable insights into the market's overall trajectory. Both market value and volume are analyzed to attract potential investors. Consistent growth has been supported by rising demand for clean-label ingredients and a broader consumer shift towards natural food components. The food and beverage sector remains the primary driver, with rice starch's multifunctional properties, like thickening, texturizing, and stabilizing, leading to its widespread inclusion in product formulations. The surge in demand for gluten-free and allergen-free products has further fueled this trend.

Additionally, new and innovative uses emerging within traditionally slower-growing segments are poised to contribute significantly to the rice starch market's overall expansion. These developing applications create fresh demand streams that complement and strengthen the momentum seen in faster-growing industries. By diversifying the range of end-use cases, such as specialized pharmaceutical formulations, advanced cosmetic products, and niche food applications, these emerging sectors help stabilize growth and open opportunities for cross-industry integration. This broader adoption not only drives incremental volume but also encourages investment in research and development, fueling product innovation and enabling manufacturers to tap into previously untapped markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $620.3 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 8% |

In 2024, the native rice starch segment held a valuation of USD 309.4 million and is anticipated to grow at a CAGR of 7.9% through 2034. Native rice starch continues to dominate the market due to its extensive use across various industries. It is especially favored because of its milled-derived form, versatility, and alignment with clean-label requirements. The food and beverage industry represents the largest consumer base for native rice starch, leveraging its thickening, gelling, and stabilizing functions in products such as dairy, sauces, and infant nutrition. Its natural origin and functional benefits make it an essential ingredient in many formulations.

The white rice type segment accounted for USD 267.4 million in 2024 and is expected to grow at an 8.1% CAGR through 2034, holding a 43.1% share. White rice remains the leading source of rice starch, thanks to its ease of processing, abundant availability, and neutral flavor profile. Both consumers and manufacturers prefer rice starch derived from white rice due to its consistent, high-quality yield, making it ideal for use in food, pharmaceutical, and cosmetic products that demand superior starch quality. Large-scale producers also favor white rice because of its standardized properties and efficient extraction methods. Additionally, rising interest in organic and minimally processed foods is boosting the demand for rice starch from white rice, which is increasingly perceived as a premium ingredient.

U.S. Rice Starch Market was valued at USD 167.5 million in 2024 and is expected to grow at a 7.8% CAGR from 2025 to 2034. Growth in the U.S. is attributed to the rising preference for clean-label, gluten-free, and plant-based ingredients. The food and beverage industry continues to be the dominant consumer, particularly within bakery, dairy, and convenience food applications. Demand is also increasing in the pharmaceutical and cosmetics sectors due to rice starch's hypoallergenic and biodegradable properties. Advances in processing technologies have enhanced product quality and expanded the range of applications, further strengthening market growth. The U.S. stands as the most active market player in North America, driving growth across the region.

On a global scale, the Rice Starch Market is moderately consolidated, with major players such as Roquette Freres, Cargill Incorporation, BENEO GmbH, AGRANA Beteiligungs-AG, and Ingredient Incorporated leading the competition. These companies hold significant market shares and are instrumental in shaping industry trends. Leading companies in the rice starch market adopt various strategic initiatives to strengthen their market position. They focus heavily on innovation, developing new formulations and processing techniques that enhance product functionality and meet clean-label demands. Strategic partnerships and collaborations with food and beverage manufacturers help expand their distribution networks and end-use applications. Investment in sustainable sourcing and production practices reinforces their commitment to environmental responsibility, which appeals to eco-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360 synopsis

- 2.2 Key market trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for clean label ingredients

- 3.2.1.2 Rising prevalence of gluten intolerance

- 3.2.1.3 Increasing applications in food & beverage industry

- 3.2.1.4 Expanding use in pharmaceutical & cosmetic products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternative starches

- 3.2.2.2 Price volatility of raw materials

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Price trends

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Native rice starch

- 5.3 Modified rice starch

- 5.3.1 Physically modified

- 5.3.1.1 Pre-gelatinized rice starch

- 5.3.1.2 Heat-moisture treated rice starch

- 5.3.1.3 Other physically modified rice starch

- 5.3.2 Chemically modified

- 5.3.2.1 Cross-linked rice starch

- 5.3.2.2 Oxidized rice starch

- 5.3.2.3 Acetylated rice starch

- 5.3.2.4 Other chemically modified rice starch

- 5.3.3 Enzymatically modified

- 5.3.1 Physically modified

- 5.4 Resistant Rice Starch

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 White rice

- 6.3 Brown rice

- 6.4 Broken rice & by-products

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Liquid & gel

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Bakery & confectionery

- 8.2.2 Dairy products

- 8.2.3 Soups, sauces & dressings

- 8.2.4 Meat & Poultry Products

- 8.2.5 Snacks & convenience foods

- 8.2.6 Beverages

- 8.2.7 Baby food & infant product type

- 8.2.8 Gluten-free products

- 8.2.9 Other food applications

- 8.3 Pharmaceuticals

- 8.3.1 Tablet binding & disintegration

- 8.3.2 Capsule product solutions

- 8.3.3 Drug delivery systems

- 8.3.4 Other pharmaceutical applications

- 8.3.5 Cosmetics & personal care

- 8.3.6 Skin care products

- 8.3.7 Hair care products

- 8.3.8 Color cosmetics

- 8.3.9 Other cosmetic applications

- 8.4 Paper & textile

- 8.4.1 Paper sizing & coating

- 8.4.2 Textile sizing & finishing

- 8.4.3 Other paper & textile applications

- 8.5 Other applications

- 8.5.1 Adhesives & glues

- 8.5.2 Biodegradable packaging

- 8.5.3 Other industrial applications

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 A&B Ingredients

- 10.2 AGRANA Beteiligungs-AG

- 10.3 Agrana Group

- 10.4 Anhui Lianhe

- 10.5 Archer Daniels Midland Company

- 10.6 Bangkok Starch Industrial Co., Ltd.

- 10.7 Beneo (Sudzucker Group)

- 10.8 Cargill, Incorporated

- 10.9 Golden Agriculture Co., Ltd.

- 10.10 Herba Ingredients

- 10.11 Hunan ER-KANG

- 10.12 Ingredion Incorporated

- 10.13 Jiangxi Golden Agriculture Co., Ltd.

- 10.14 Roquette Freres

- 10.15 Shaanxi Tianyu Pharmaceutical Co., Ltd.

- 10.16 Sonish Starch Technology Co., Ltd.

- 10.17 Tate & Lyle PLC

- 10.18 THAI WAH PUBLIC COMPANY LIMITED

- 10.19 Thai Flour Industry Co., Ltd.

- 10.20 Wuxi Chuangda Food Co., Ltd.