|

市場調査レポート

商品コード

1773345

子宮筋腫治療装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Uterine Fibroid Treatment Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 子宮筋腫治療装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

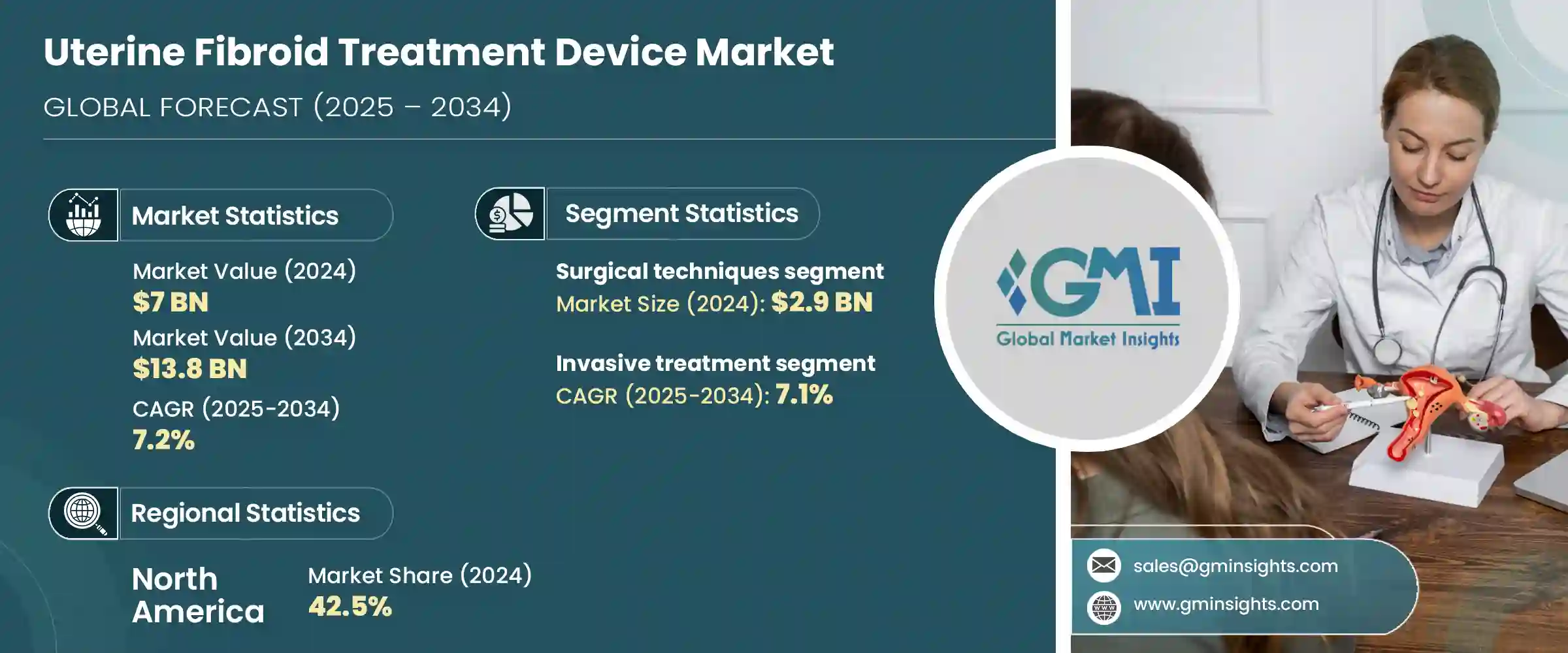

世界の子宮筋腫治療装置市場は、2024年には70億米ドルと評価され、CAGR 7.2%で成長し、2034年には138億米ドルに達すると推定されています。

出産適齢期の女性における子宮筋腫患者の一貫した増加が、信頼性と安全性を兼ね備えた高度な治療オプションに対する需要を大きく促進しています。技術的に洗練されたソリューションへの顕著なシフトとともに、低侵襲で子宮を温存する手技に対する意識の高まりが、ヘルスケアシステム全体での幅広い採用を促進しています。エネルギーベースの技術は、子宮の完全性を維持しながら子宮筋腫を効率的に管理する能力で人気を博しています。

非侵襲的で侵襲性の低い治療法における絶え間ない技術革新は、特に従来の手術に代わる治療法を求める患者にとって、患者の転帰を向上させています。熟練した医師が利用可能であり、先進国および新興国のヘルスケアインフラ全体で治療へのアクセスが拡大していることも、市場の成長を支える重要な役割を果たしています。月経痛やその他の婦人科疾患の有病率が高まるにつれ、子宮筋腫治療機器市場は拡大を続けています。Canyon Medical社、Minerva Surgical社、Medtronic社、Terumo Corporation社、Johnson &Johnson(Ethicon)社などの企業が、新しい治療器具で子宮筋腫管理を前進させている主要企業です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 70億米ドル |

| 予測金額 | 138億米ドル |

| CAGR | 7.2% |

外科的処置セグメントは、2024年に29億米ドルを生み出しました。これらの治療は、子宮筋腫を除去することに重点を置いており、状況によっては、症状の程度や複雑さに応じて子宮自体を摘出することもあります。子宮筋腫が大きかったり、数が多かったり、症状が強かったりする場合には、子宮筋腫核出術や子宮摘出術といった処置がしばしば好まれます。ヘルスケアプロバイダーと患者の両方から人気があるのは、成功率が高く、症状の緩和が長期間続くからです。このセグメントの継続的な優位性は、ヘルスケアインフラの拡大、保険オプションの改善、経験豊富な手術専門家へのアクセスの向上によって支えられています。過多月経出血や関連する婦人科疾患の増加といった要因も、外科的介入に対する強い需要に寄与しています。

2024年には、侵襲的処置分野が市場をリードし、2034年までCAGR 7.1%で成長すると予測されています。これらの治療は、複雑な筋腫や重度の筋腫に対して特に有効であり、包括的な症状緩和を提供します。薬物療法や非侵襲的治療で期待通りの結果が得られない場合、これらの方法が望ましい選択肢となります。開腹手術によるアプローチは、非侵襲的な手法に比べてより確実な結果をもたらすことで、骨盤の不快感、異常出血、不妊に関連する合併症などの持続的な問題に対処します。また、深く入り込んだ筋腫や多発性の筋腫を治療できることから、この分野は市場セグメンテーション市場において重要な位置を占めています。

米国の子宮筋腫治療装置市場は2024年に30億米ドルと評価されました。この成長の主な要因は、女性の健康と婦人科処置を専門とする医療専門家の利用可能性です。子宮筋腫を効果的に治療するために、毎年何千ものエネルギー療法や塞栓術が実施されています。治療機器の絶え間ない技術的進歩や、より低侵襲な選択肢に対する幅広い認識により、米国は引き続き市場全体の拡大に大きく貢献しています。新しい治療技術に関する教育やヘルスケア提供モデルの改善も、機器を用いた子宮筋腫ソリューションに対する患者の取り込みと信頼の向上に寄与しています。

業界大手としては、オリンパス、インサイテック、Shenzhen Mindray Bio-Medical Electronics、Conmed、Merit Medical Systems、CooperSurgical、Boston Scientific、Karl Storz、Hologic、Canyon Medical、Medtronic、Minerva Surgical、Terumo Corporation、Nesa Medtech、Johnson &Johnson(Ethicon)などが挙げられます。これらの企業は、継続的な製品開発とイノベーションを通じて、市場の方向性を形成する上で大きな役割を果たしています。主要企業は子宮筋腫治療装置市場での地位を強化するため、研究開発に積極的に投資し、安全性を向上させた低侵襲技術を導入しています。革新的な治療プラットフォームにアクセスするため、合併や戦略的提携、買収を通じて製品ポートフォリオを拡大することに注力している企業も多いです。いくつかの企業は、リアルタイム画像やAIベースのナビゲーションシステムを機器に統合することで、患者の転帰を向上させることに取り組んでいます。さらに、主要企業は未開拓市場への参入や地域のヘルスケアプロバイダーとの連携により、世界な足跡を増やしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 子宮筋腫の罹患率の増加

- 子宮および腹腔鏡デバイスの技術的進歩

- 低侵襲手術の需要の高まり

- 業界の潜在的リスク&課題

- 高度な治療機器の高コスト

- 農村部や発展途上地域では入手が限られる

- 市場機会

- 使い捨ておよび単回使用デバイスの採用の増加

- 生殖能力温存治療オプションの需要増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格分析

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:技術別、2021~2034年

- 主要動向

- 外科手術の技術

- 子宮摘出術

- 子宮筋腫摘出術

- 腹腔鏡手術

- 腹腔鏡下子宮筋腫摘出術

- 筋融解

- アブレーション技術

- マイクロ波アブレーション

- 水熱アブレーション

- 凍結療法

- 超音波アブレーション

- 高強度焦点式超音波(HIFU)

- MRI誘導集束超音波(MRGFUS)

- 塞栓術

第6章 市場推計・予測:治療別、2021~2034年

- 主要動向

- 侵襲的治療

- 低侵襲治療

- 非侵襲的治療

第7章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Boston Scientific

- Canyon Medical

- Conmed

- CooperSurgical

- Hologic

- Insightec

- Johnson &Johnson(Ethicon)

- Karl Storz

- Medtronic

- Merit Medical Systems

- Minerva Surgical

- Nesa Medtech

- Olympus

- Shenzhen Mindray Bio-Medical Electronics

- Terumo Corporation

The Global Uterine Fibroid Treatment Device Market was valued at USD 7 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 13.8 billion by 2034. The consistent rise in fibroid cases among women of childbearing age is significantly fueling the demand for advanced treatment options that are both reliable and safe. Greater awareness about minimally invasive and uterus-sparing procedures, along with a noticeable shift towards technologically sophisticated solutions, is driving broader adoption across healthcare systems. Energy-based technologies have gained popularity for their ability to manage fibroids efficiently while maintaining uterine integrity.

Continuous innovation in non-invasive and less aggressive treatment methods is enhancing patient outcomes, particularly for those seeking alternatives to traditional surgery. The availability of skilled practitioners and expanded access to treatment across developed and emerging healthcare infrastructures also play a critical role in supporting market growth. As the prevalence of conditions like menorrhagia and other gynecologic disorders increases, the market for uterine fibroid treatment devices continues to expand. Companies like Canyon Medical, Minerva Surgical, Medtronic, Terumo Corporation, Johnson & Johnson (Ethicon), and others are key players advancing the landscape of fibroid management with novel therapeutic devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 7.2% |

The surgical procedures segment generated USD 2.9 billion in 2024. These treatments focus on eliminating fibroids or, in certain situations, removing the uterus itself, depending on the extent and complexity of the condition. Procedures such as myomectomy and hysterectomy are often preferred when fibroids are large, numerous, or highly symptomatic. Their popularity among both healthcare providers and patients stems from high success rates and long-lasting relief from symptoms. The continued dominance of this segment is supported by an expanding healthcare infrastructure, improved insurance options, and better access to experienced surgical professionals. Factors like rising cases of excessive menstrual bleeding and related gynecological issues also contribute to the strong demand for surgical intervention.

In 2024, the invasive procedures segment led the market and is anticipated to grow at a CAGR of 7.1% through 2034. These treatments are especially effective for complicated or severe fibroid conditions, offering comprehensive symptom relief. When medications or non-invasive therapies fail to deliver the expected results, these methods become the preferred option. Open surgical approaches address persistent issues such as pelvic discomfort, abnormal bleeding, and fertility-related complications by providing more definitive outcomes compared to non-invasive techniques. The ability to treat deeply embedded or multiple fibroids also makes this segment a critical part of the uterine fibroid treatment device market.

U.S. Uterine Fibroid Treatment Device Market was valued at USD 3 billion in 2024. A key factor contributing to this growth is the availability of medical experts specializing in women's health and gynecologic procedures. Thousands of energy-based and embolization procedures are carried out annually to treat fibroids effectively. With continual technological advancements in treatment devices and broader awareness of less invasive alternatives, the U.S. continues to be a significant contributor to overall market expansion. Education around newer treatment techniques and improvements in healthcare delivery models are also helping to increase patient uptake and trust in device-based fibroid solutions.

Prominent industry players include Olympus, Insightec, Shenzhen Mindray Bio-Medical Electronics, Conmed, Merit Medical Systems, CooperSurgical, Boston Scientific, Karl Storz, Hologic, Canyon Medical, Medtronic, Minerva Surgical, Terumo Corporation, Nesa Medtech, and Johnson & Johnson (Ethicon). These companies are instrumental in shaping the market's direction through ongoing product development and innovation. To reinforce their position in the uterine fibroid treatment device market, leading companies are actively investing in research and development to introduce minimally invasive technologies with improved safety profiles. Many are focusing on expanding their product portfolios through mergers, strategic partnerships, and acquisitions to access innovative treatment platforms. Several firms are working to enhance patient outcomes by integrating real-time imaging and AI-based navigation systems into their devices. Additionally, key players are increasing their global footprint by entering untapped markets and aligning with regional healthcare providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Treatment

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of uterine fibroids

- 3.2.1.2 Technological advancements in uterine & laparoscopic devices

- 3.2.1.3 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment devices

- 3.2.2.2 Limited availability in rural and developing areas

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of disposable and single-use devices

- 3.2.3.2 Increased demand for fertility-preserving treatment options

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical techniques

- 5.2.1 Hysterectomy

- 5.2.2 Myomectomy

- 5.3 Laparoscopic techniques

- 5.3.1 Laparoscopic myomectomy

- 5.3.2 Myolysis

- 5.4 Ablation techniques

- 5.4.1 Microwave ablation

- 5.4.2 Hydrothermal ablation

- 5.4.3 Cryoablation

- 5.4.4 Ultrasound ablation

- 5.4.4.1 High intensity focused ultrasound (HIFU)

- 5.4.4.2 MRI-guided focused ultrasound (MRGFUS)

- 5.5 Embolization techniques

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Invasive treatment

- 6.3 Minimally invasive treatment

- 6.4 Non-invasive treatment

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Boston Scientific

- 8.2 Canyon Medical

- 8.3 Conmed

- 8.4 CooperSurgical

- 8.5 Hologic

- 8.6 Insightec

- 8.7 Johnson & Johnson (Ethicon)

- 8.8 Karl Storz

- 8.9 Medtronic

- 8.10 Merit Medical Systems

- 8.11 Minerva Surgical

- 8.12 Nesa Medtech

- 8.13 Olympus

- 8.14 Shenzhen Mindray Bio-Medical Electronics

- 8.15 Terumo Corporation