蒸気回収装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vapor Recovery Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773343

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

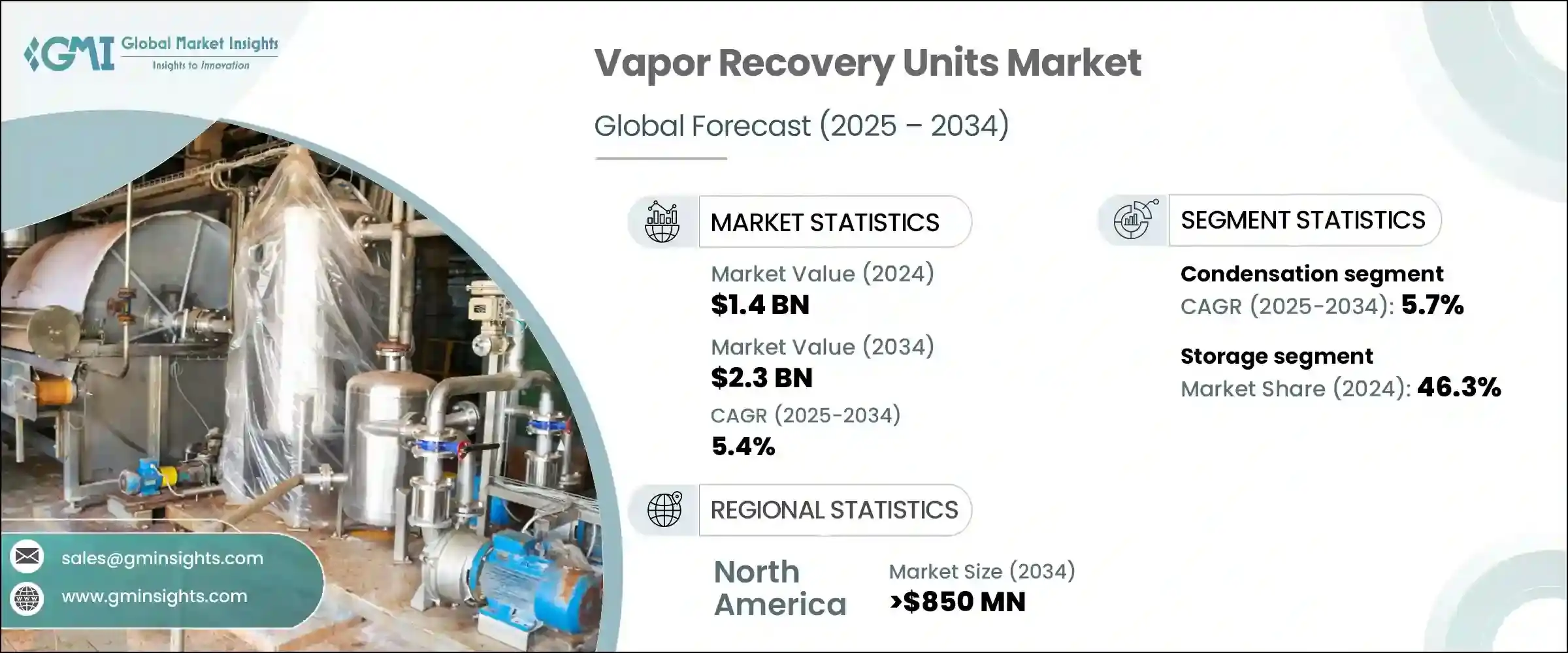

蒸気回収装置の世界市場規模は、2024年に14億米ドルとなり、CAGR5.4%で成長し、2034年までには23億米ドルに達すると予測されています。

揮発性有機化合物(VOC)の排出を制御することの環境および規制上の重要性に関する意識の高まりが、市場の勢いを加速する上で重要な役割を果たしています。いくつかの発展途上国では政府がより厳しい排出規制を導入しており、産業界はコンプライアンス戦略の一環として蒸気回収技術の導入を余儀なくされています。これらの装置は、そうしなければ大気中に放出されてしまう炭化水素蒸気を回収し、再利用するための持続可能なソリューションを提供します。産業界が従来の排出制御システムに代わる、環境に優しく効率的な選択肢を求める中、VRUは実行可能で好ましい選択肢として急速に台頭しています。

環境への影響を最小限に抑えるだけでなく、運用コスト面でも有利な、よりクリーンな技術への選好が高まっていることが、さまざまな分野でのVRU採用に拍車をかけています。市場拡大の主な要因の1つは、特に急速に工業化が進む地域で燃料貯蔵施設や原油ターミナルが増加していることです。これらの地域の事業者は、公害規制の強化に対応し、プロセス全体の効率を向上させるため、蒸気回収システムに投資しています。貴重な燃料蒸気を回収するVRUの能力は、さらなるコスト削減につながるため、事業者にとって戦略的な投資となっています。さらに同市場では、スペースに制約のあるセットアップや移動用途向けに設計された、コンパクトなスキッド搭載型ベーパーリカバリーシステムの需要が高まっています。これらの最新システムは、改良されたろ過、耐腐食性材料、一体型コンデンサー、セルフクリーニング機構などの高度な機能を備えており、メンテナンス間隔を最小化し、運用信頼性を高めるのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 14億米ドル |

| 予測金額 | 23億米ドル |

| CAGR | 5.4% |

さらに、回収燃料の再販価値と、コンプライアンスや検査に必要な労力の削減が相まって、VRUシステムの普及をさらに後押ししています。市場が性能主導型になるにつれて、運転の中断を減らしながら安定した出力を提供する高効率システムに重点が移りつつあります。エネルギーインフラが拡大し、世界の貯蔵ネットワークで燃料処理量が増加するのに伴い、このようなユニットに対する需要も増え続けています。

技術的には、市場セグメンテーション市場は凝縮システム、吸着システム、吸収システム、圧縮システムに区分されます。このうち、凝縮分野は2034年までCAGR5.7%で拡大すると予想されています。この成長を大きく支えているのは、クローズドループ冷却システムへの関心の高まりであり、これによって事業者は水の消費を抑え、事業の持続可能性プロファイルを高めることができます。回収率を犠牲にすることなく資源使用量を削減するエココンシャスな設計へのシフトが、凝縮型VRUセグメントを大きく後押ししています。これらのシステムは、環境目標に沿いながら幅広い炭化水素を効率的に回収する能力で人気を集めています。

用途別では、市場は処理、貯蔵、輸送に分類されます。2024年時点では、貯蔵用途セグメントが46.3%と最大のシェアを占めており、予測期間を通じて優位性を維持すると予想されます。これは、貯蔵タンクからの排出物、特にタンクブリージングや作業損失から生じる排出物を最小限に抑えることが規制上重視されていることが主な原因です。排出基準が厳しくなるにつれ、施設運営者はコンプライアンスを維持し罰則を回避するため、VRUをターミナルインフラに統合する必要性が高まっています。貯蔵部門は依然としてこれらのシステムの主要な応用分野であり、需要は大規模・中規模施設の両方で強い勢いを見せています。

地域別分析では、米国の蒸気回収装置市場は2022年に3億7,360万米ドルでしたが、2023年には3億8,980万米ドルに増加し、2024年には4億720万米ドルに達しました。同国では、特に石油上流事業とシェール盆地において、VRUの強力な導入が続いています。シェール層の探査活動が拡大するにつれて、タンクバッテリーの放出を管理し、大気浄化法に準拠することができる排出制御技術に対する需要が高まっています。さらに、製油所や燃料配給ターミナルは、厳格な大気質規制を満たし、環境フットプリントを削減するため、VRUへの投資を増やしています。こうした取り組みがサプライヤーに新たなビジネス機会を生み出し、この地域の安定した市場成長を後押ししています。

競合情勢は中程度に細分化されており、大規模な産業用メーカーと専門的なシステムインテグレーターが混在しています。Ingersoll Rand、PSG、Cimarron Energy、Kilburn、Zeecoを含む主要5社は、合計で市場シェアの約40%を占めています。これらの企業は、戦略的な製品革新、技術サービスの拡大、システム統合能力の強化に注力し、その地位を強化しています。競争が激化するなか、各社は多様な分野で進化するエンドユーザーニーズに対応するため、現地生産、自動化、モジュラーシステム開発にも投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 結露

- 吸着

- 吸収

- 圧縮

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 処理

- 貯蔵

- 交通機関

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 石油・ガス

- 化学・石油化学

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- ノルウェー

- ポーランド

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- オマーン

- 南アフリカ

- ナイジェリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

第9章 企業プロファイル

- ALMA Group

- BORSIG

- Cimarron Energy

- Cool Sorption

- Flogistix

- Ingersoll Rand

- KAPPA GI

- Kilburn

- Koch Engineered Solutions

- PSG

- Reynold India

- S&S Technical

- SCS Technologies

- SYMEX Technologies

- Tecam

- VOCZero

- Zeeco

目次

The Global Vapor Recovery Units Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 2.3 billion by 2034. Growing awareness regarding the environmental and regulatory importance of controlling volatile organic compound (VOC) emissions is playing a significant role in accelerating market momentum. Governments in several developing nations are rolling out stricter emissions norms, compelling industries to deploy vapor recovery technologies as part of their compliance strategy. These units offer a sustainable solution for capturing and recycling hydrocarbon vapors that would otherwise be released into the atmosphere. As industries seek eco-friendly and efficient alternatives to traditional emission control systems, VRUs are rapidly emerging as a viable and preferred choice.

The increasing preference for cleaner technologies that not only minimize environmental impact but also offer operational cost benefits is fueling VRU adoption across multiple sectors. One of the primary drivers for market expansion is the growing number of fuel storage facilities and crude oil terminals, especially in rapidly industrializing regions. Operators in these areas are investing in vapor recovery systems to align with tightening pollution norms and to improve overall process efficiency. The ability of VRUs to recover valuable fuel vapors translates into added cost savings, making them a strategic investment for operators. Moreover, the market is witnessing rising demand for compact, skid-mounted vapor recovery systems designed for space-constrained setups or mobile applications. These modern systems are being equipped with advanced features such as improved filtration, corrosion-resistant materials, integrated condensers, and self-cleaning mechanisms, which help minimize maintenance intervals and enhance operational reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.4% |

Additionally, the resale value of recovered fuel, combined with reduced labor requirements for compliance and inspection, is further encouraging the uptake of VRU systems. As the market becomes more performance-driven, the emphasis is shifting toward high-efficiency systems that deliver consistent output while reducing operational disruptions. The demand for such units continues to rise in line with expanding energy infrastructure and increasing fuel throughput across global storage networks.

Technologically, the vapor recovery units market is segmented into condensation, adsorption, absorption, and compression systems. Among these, the condensation segment is expected to expand at a CAGR of 5.7% through 2034. This growth is largely supported by growing interest in closed-loop cooling systems, which allow operators to limit water consumption and enhance the sustainability profile of their operations. The shift toward eco-conscious designs that reduce resource use without compromising recovery rates is giving a considerable push to the condensation VRU segment. These systems are gaining traction for their ability to recover a wide range of hydrocarbons efficiently while aligning with environmental goals.

By application, the market is classified into processing, storage, and transportation. In 2024, the storage application segment held the largest share at 46.3%, and it is expected to maintain dominance throughout the forecast period. This is largely due to the regulatory emphasis on minimizing emissions from storage tanks, particularly emissions stemming from tank breathing and working losses. As emissions standards tighten, facility operators are increasingly compelled to integrate VRUs into their terminal infrastructure to stay in compliance and avoid penalties. The storage sector remains the primary area of application for these systems, with demand showing strong momentum across both large and mid-sized facilities.

In terms of regional analysis, the vapor recovery units market in the United States stood at USD 373.6 million in 2022, rose to USD 389.8 million in 2023, and reached USD 407.2 million in 2024. The country continues to witness strong adoption of VRUs, particularly across upstream oil operations and shale basins. As shale exploration activities grow, there is heightened demand for emissions control technologies capable of managing tank battery releases and complying with the Clean Air Act. Additionally, refineries and fuel distribution terminals are increasing their investment in VRUs to meet strict air quality mandates and reduce their environmental footprint. These efforts are creating new business opportunities for suppliers and driving consistent market growth in the region.

The competitive landscape of the vapor recovery units market is moderately fragmented, with a mix of large-scale industrial manufacturers and specialized system integrators. The top five players, which include Ingersoll Rand, PSG, Cimarron Energy, Kilburn, and Zeeco, collectively account for around 40% of the market share. These companies are focusing on strategic product innovation, technical service expansion, and enhanced system integration capabilities to strengthen their position. As competition intensifies, players are also investing in localized manufacturing, automation, and modular system development to cater to evolving end-user needs across diverse sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Condensation

- 5.3 Adsorption

- 5.4 Absorption

- 5.5 Compression

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Processing

- 6.3 Storage

- 6.4 Transportation

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Chemical & petrochemical

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Norway

- 8.3.8 Poland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.4.6 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 Oman

- 8.5.6 South Africa

- 8.5.7 Nigeria

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ALMA Group

- 9.2 BORSIG

- 9.3 Cimarron Energy

- 9.4 Cool Sorption

- 9.5 Flogistix

- 9.6 Ingersoll Rand

- 9.7 KAPPA GI

- 9.8 Kilburn

- 9.9 Koch Engineered Solutions

- 9.10 PSG

- 9.11 Reynold India

- 9.12 S&S Technical

- 9.13 SCS Technologies

- 9.14 SYMEX Technologies

- 9.15 Tecam

- 9.16 VOCZero

- 9.17 Zeeco

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日