オーガニックベビーフードの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Organic Baby Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773337

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

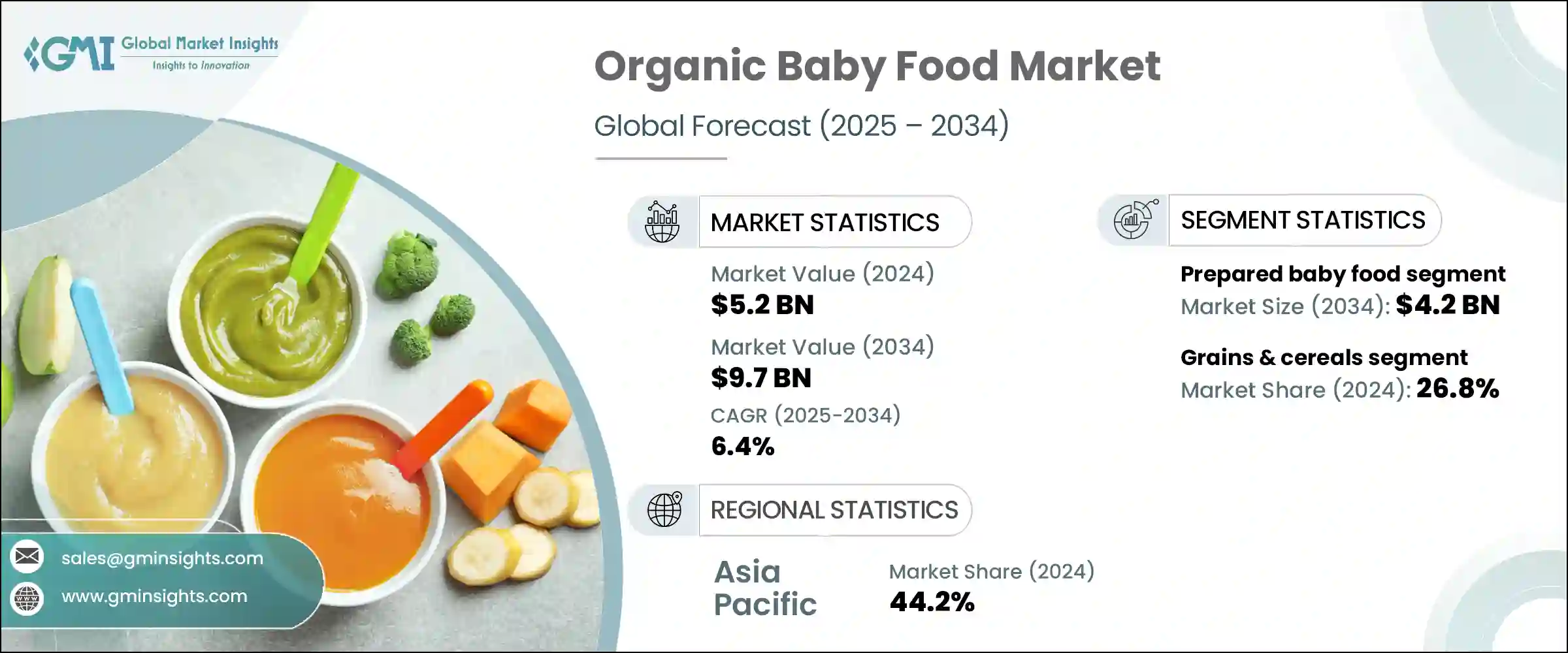

世界のオーガニックベビーフード市場は、2024年には52億米ドルとなり、CAGR 6.4%で成長し、2034年には97億米ドルに達すると推定されています。

同市場は着実な成長を続けており、その主な要因は消費者の習慣の変化、子どもの栄養に対する意識の高まり、ライフスタイルの力学の進化にあります。現代の親、特にミレニアル世代とZ世代は、透明性、クリーンラベルの原材料、化学物質を含まない製品を優先しています。乳幼児に与える食品についてより多くの養育者が意識するようになるにつれて、有機代替食品への需要が急増しています。遺伝子組み換え作物、防腐剤、人工成分、合成殺虫剤を含まない製品は、家族がより健康的な人生のスタートを切ることを重視する中で、大きな人気を集めています。

加工食品や長期的な健康への影響に対する懸念が、オーガニックベビーフードをより望ましいものにしています。消費者は、安全で環境に配慮した選択肢を積極的に選ぶようになっています。アレルギーや過敏症を経験する乳幼児が増加していることも、この市場動向に一役買っており、よりシンプルな成分プロファイルに対する需要を押し上げています。ペースの速い都市生活や家族構成の変化と相まって、栄養価が高く、かつ手間がかからず、品質に妥協することなく利便性を追求した離乳食へのニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 52億米ドル |

| 予測金額 | 97億米ドル |

| CAGR | 6.4% |

調理済み食品(Preparedオーガニックベビーフード)は最も急成長しているカテゴリーとして浮上しており、2034年には42億米ドルとなり、CAGR 6.6%で成長すると予測されています。このセグメントは、パウチ、ジャー、ピューレなどの便利なフォーマットですぐに食べられる食事を好む、今日の多忙な介護者とよく共鳴しています。これらの製品は、栄養と手軽さの完璧なバランスを提供し、特に時間の節約を求める共働きの親に適しています。再就職する母親が増えるにつれ、このカテゴリーの需要は高まっています。リシーラブル容器や環境に配慮した素材など、パッケージングにおける革新は、持ち運びやすさを提供し、鮮度を保ち、持続可能性の価値観に沿うことで、その魅力をさらに高めています。

穀物・シリアルセグメントは2024年に26.8%と圧倒的なシェアを占め、2034年までCAGR 6.1%で成長すると予想されています。このセグメントは、その栄養プロファイルと、おかゆ、乳児用シリアル、バー、歯が生えるまでの間食などの食事形態における汎用性により、引き続きリードしています。オーツ麦、雑穀、キヌア、米を使った食品は高エネルギーで消化がよく、早期開発に適しています。オーツ麦は柔軟性に富み、離乳食の基本的な役割を果たすため、健康的で自然な食材で子どもに栄養を与えたいと願う養育者に常に愛用されています。

アジア太平洋オーガニックベビーフード市場は2024年に44.2%のシェアを占めました。インドネシア、中国、インドなどの国々では、中産階級の人口拡大とともに出生率が上昇しています。赤ちゃん用栄養剤に含まれる化学添加物のリスクに対する意識の高まりが、都市部や半都市部の購買パターンに影響を与えています。この地域全体の政府も食品安全基準を引き上げ、より厳格な有機認証基準を実施しており、これが消費者の信頼を高めています。さらに、インターネットへのアクセスやeコマースの普及により、高級オーガニックベビーフード製品が遠隔地でも入手できるようになり、顧客基盤の拡大に寄与しています。

世界のオーガニックベビーフード市場は、Hero Group、Danone S.A.、The Hain Celestial Group、Abbott Laboratories、Nestle S.A.などの主要企業により、引き続き統合されています。市場ポジションを強化するため、オーガニックベビーフード分野の主要企業は、植物由来の処方、アレルゲンフリーのバリエーション、特定の発育ニーズに対応した強化ブレンドなど、製品ポートフォリオの拡大に注力しています。多くの企業は、クリーンラベルへの期待に応え、ブランドの信頼を高めるために、持続可能な農業パートナーシップやトレーサビリティ技術に投資しています。eコマース・ブームも追い風となり、特に新興市場では、流通の裾野が広がっています。小児科医や栄養士とのコラボレーションは製品の信頼性を高めるのに役立ち、革新的で環境に優しいパッケージング・ソリューションは長期的な持続可能性の目標をサポートします。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 親の健康意識の高まり

- 従来の食品に含まれる化学物質の残留に対する懸念の高まり

- アレルギーや食物過敏症の発生率の増加

- 働く女性の増加

- 業界の潜在的リスク&課題

- オーガニック製品のプレミアム価格設定

- 防腐剤が含まれていないため、保存期間が限られている

- オーガニック原料のサプライチェーンの課題

- 市場機会

- 新興市場への拡大

- eコマースの成長と消費者直販モデル

- 製品の革新と多様化

- 促進要因

- 成長可能性分析

- 規制情勢

- 世界のオーガニック認証基準

- 地域による規制の違い

- 北米(USDAオーガニック)

- 欧州(EU有機規制)

- アジア太平洋地域の規制枠組み

- ラベル要件と主張

- 安全基準と試験プロトコル

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- 消費者行動分析

- 購入パターンと好み

- オーガニック製品にプレミアムを支払う意欲

- 購買決定に対する人口統計学的影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- 調理済みベビーフード

- 乾燥ベビーフード

- 乳児用調合乳

- その他

第6章 市場推計・予測:食材別、2021~2034年

- 主要動向

- 穀物

- 果物

- 野菜

- 乳製品

- 肉類と鶏肉

- その他

第7章 市場推計・予測:年齢別、2021~2034年

- 主要動向

- 乳児(0~6か月)

- 乳児(6~12ヶ月)

- 幼児(12~24か月)

- 児童(24ヶ月以上)

第8章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- 薬局・ドラッグストア

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Abbott Laboratories

- Nestle S.A.

- Danone S.A.

- Hero Group

- The Hain Celestial Group, Inc.

- Kraft Heinz Company

- Plum Organics(Campbell Soup Company)

- Once Upon a Farm

- HiPP GmbH &Co. Vertrieb KG

- Amara Organic Foods

- Babylife Organics

- Little Spoon

- Serenity Kids

- Sprout Organic Foods, Inc.

- Tiny Organics

目次

The Global Organic Baby Food Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 9.7 billion by 2034. The market continues to witness steady growth, largely due to shifting consumer habits, greater awareness about child nutrition, and evolving lifestyle dynamics. Modern-day parents, especially those from millennial and Gen Z demographics, are prioritizing transparency, clean-label ingredients, and chemical-free products. As more caregivers become conscious about the foods they give to their infants, the demand for organic alternatives has surged. Products free from GMOs, preservatives, artificial ingredients, and synthetic pesticides are gaining significant popularity as families focus on providing a healthier start in life.

Concerns over processed food and potential long-term health impacts have made organic baby food more desirable. Consumers are actively choosing options that are both safe and environmentally responsible. The increasing number of infants experiencing allergies and sensitivities has also played a role in this market trend, pushing demand for simpler ingredient profiles. Coupled with fast-paced urban living and changing family dynamics, there's a greater need for nutritious yet hassle-free feeding choices that cater to convenience without compromising quality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 6.4% |

Prepared organic baby food is emerging as the fastest-growing category and is forecasted to be valued at USD 4.2 billion by 2034, growing at 6.6% CAGR. This segment resonates well with today's busy caregivers who prefer ready-to-serve meals in convenient formats like pouches, jars, and purees. These products offer the perfect balance of nutrition and ease, especially for working parents looking to save time. With more mothers rejoining the workforce, demand for this category has climbed. Innovations in packaging, such as resealable containers and eco-conscious materials, have further boosted its appeal by offering portability, preserving freshness, and aligning with sustainability values.

The grains and cereals segment held the dominant share in 2024 at 26.8% and is expected to grow at a CAGR of 6.1% through 2034. This segment continues to lead due to its nutritional profile and versatility in meal formats like porridge, infant cereals, bars, and teething snacks. Foods made with oats, millet, quinoa, and rice are high in energy, easily digestible, and suitable for early development. Their flexibility and foundational role in baby diets make them a consistent favorite for caregivers looking to nourish their children with wholesome, natural ingredients.

Asia Pacific Organic Baby Food Market held a 44.2% share in 2024. Countries such as Indonesia, China, and India are seeing a rise in birth rates alongside expanding middle-class populations. Heightened awareness about the risks of chemical additives in baby nutrition is influencing buying patterns across urban and semi-urban areas. Governments across the region are also raising food safety standards and enforcing stricter organic certification norms, which boost consumer trust. Moreover, increased internet access and e-commerce adoption are making premium organic baby food products available in more remote regions, helping grow the customer base.

The Global Organic Baby Food Market remains consolidated, with major players including Hero Group, Danone S.A., The Hain Celestial Group, Abbott Laboratories, and Nestle S.A. To enhance their market position, leading companies in the organic baby food sector are focusing on expanding product portfolios through plant-based formulations, allergen-free variants, and fortified blends for specific developmental needs. Many are investing in sustainable farming partnerships and traceability technologies to meet clean-label expectations and enhance brand trust. Businesses are also capitalizing on the e-commerce boom to widen their distribution footprint, especially in emerging markets. Collaborations with pediatricians and nutritionists help drive product credibility, while innovative, eco-friendly packaging solutions support long-term sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Ingredients type trends

- 2.2.3 Age group

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health consciousness among parents

- 3.2.1.2 Growing concerns over chemical residues in conventional food

- 3.2.1.3 Increasing incidence of allergies and food sensitivities

- 3.2.1.4 Rising number of working women

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Premium pricing of organic products

- 3.2.2.2 Limited shelf life due to absence of preservatives

- 3.2.2.3 Supply chain challenges for organic ingredients

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 E-commerce growth and direct-to-consumer models

- 3.2.3.3 Product innovation and diversification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global organic certification standards

- 3.4.2 Regional Regulatory Variations

- 3.4.2.1 North America (USDA organic)

- 3.4.2.2 Europe (EU organic regulations)

- 3.4.2.3 Asia pacific regulatory framework

- 3.4.3 Labeling requirements and claims

- 3.4.4 Safety standards and testing protocols

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Consumer behavior analysis

- 3.13.1 Purchasing patterns and preferences

- 3.13.2 Willingness to pay premium for organic products

- 3.13.3 Demographic influences on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Prepared baby food

- 5.3 Dried baby food

- 5.4 Infant milk formula

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Ingredients Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Grains & cereals

- 6.3 Fruits

- 6.4 Vegetables

- 6.5 Dairy products

- 6.6 Meat & poultry

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Age Group, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Infants (0–6 months)

- 7.3 Babies (6–12 months)

- 7.4 Toddlers (12–24 months)

- 7.5 Children (24+ months)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets & hypermarkets

- 8.3 Specialty stores

- 8.4 Convenience stores

- 8.5 Online retail

- 8.6 Pharmacies & drug stores

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Nestle S.A.

- 10.3 Danone S.A.

- 10.4 Hero Group

- 10.5 The Hain Celestial Group, Inc.

- 10.6 Kraft Heinz Company

- 10.7 Plum Organics (Campbell Soup Company)

- 10.8 Once Upon a Farm

- 10.9 HiPP GmbH & Co. Vertrieb KG

- 10.10 Amara Organic Foods

- 10.11 Babylife Organics

- 10.12 Little Spoon

- 10.13 Serenity Kids

- 10.14 Sprout Organic Foods, Inc.

- 10.15 Tiny Organics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日