工業炉の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Industrial Furnaces Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773331

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

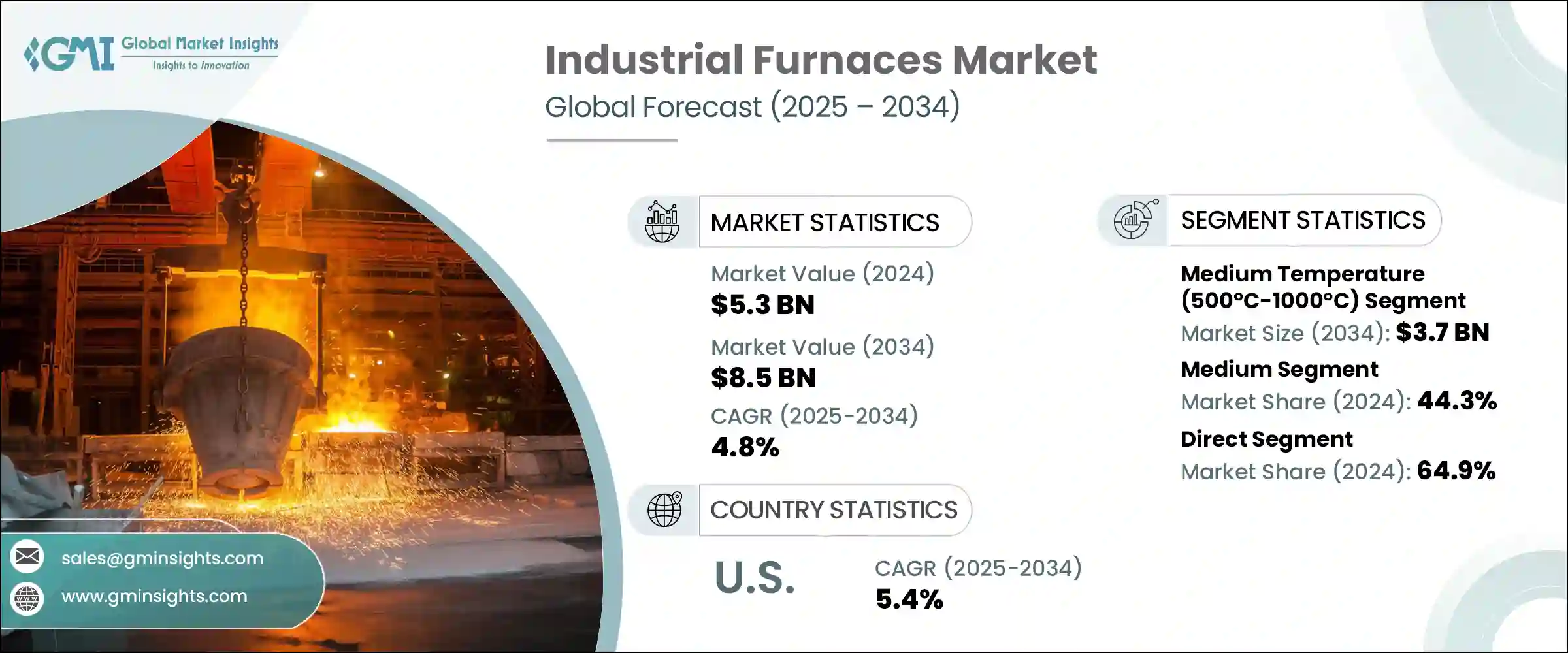

工業炉の世界市場規模は、2024年に53億米ドルとなり、CAGR4.8%で成長し、2034年までには85億米ドルに達すると予測されています。

工業炉は、金属の成形や処理に必要な溶融、焼きなまし、焼き戻しなどの高温プロセスに不可欠であるため、金属および鉄鋼産業がこの成長に大きく貢献しています。特に中国、インド、米国などの地域では、インフラ、自動車生産、産業開発に対する需要が増加しており、より効率的で耐久性のある炉の必要性が高まっています。従来の高炉に比べて排出量が少なくエネルギー効率が高い電気アーク炉(EAF)の採用が増加していることも重要な動向です。EAFは現在、世界の鉄鋼生産の約30%を占めており、先進的な炉技術に対する世界の需要がさらに高まっています。

脱炭素化への注目の高まりに加え、産業界は二酸化炭素排出量を削減するため、水素炎や電気アークなどの代替加熱技術への関心を高めています。これらの代替技術は、より持続可能な製造プロセスへの移行における重要なソリューションとみなされています。例えば水素炎は、水蒸気しか排出しないクリーンな燃焼方法であり、高温プロセスでの排出量削減に魅力的な選択肢となります。鉄鋼生産ですでに普及している電気アーク炉(EAF)も、従来の炉技術に比べ炭素排出を削減できることから検討されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 53億米ドル |

| 予測金額 | 85億米ドル |

| CAGR | 4.8% |

工業炉市場の中温セグメントは、2024年に22億米ドルを生み出し、2034年までには37億米ドルに達すると予測されています。500°Cから1000°Cの間で作動する中温炉は、その多用途性と様々な熱処理プロセスへの対応能力により、世界市場で支配的なセグメントであり続けています。これらの炉は、金属や合金の処理能力により、自動車や航空宇宙から電子機器製造に至るまで、あらゆる産業で広く使用されています。

中容量炉セグメントは2024年に44.3%のシェアを占め、2034年までCAGR4.4%で成長すると予想されています。これらの炉は、頻繁な温度サイクルと中程度の処理能力を必要とする中規模産業用途に特に好まれています。機械製造、自動車部品製造、鋳造などの業界は、一貫した品質管理と生産要件を満たすために中温炉に依存しています。

米国の工業炉市場は2024年に7億米ドルと評価され、2034年までのCAGRは5.4%と力強い成長が予測されています。米国は、その高度な製造能力とエネルギー効率の高い炉技術の採用増加により、北米工業炉市場をリードし続けています。金属加工工場、航空宇宙工場、自動車産業は、排出ガスの削減と生産性の向上に取り組んでおり、新しい高効率工業炉の需要を牽引しています。北米、特に米国、カナダ、メキシコは、同地域の成熟した製造基盤と持続可能な生産方式への注力により、世界市場で大きなシェアを占めています。

工業炉市場の主要企業には、Harper International、SECO/WARWICK S.A.、Tenova S.p.A.、Despatch Industries、Carbolite Gero、Lindberg/MPH、Gasbarre Thermal Processing Systems、Nabertherm GmbH、Inductotherm Group、Surface Combustion, Inc.、ABB、Ipsen International GmbH、Wisconsin Oven Corporation、Nutec Bickley、ANDRITZ AGなどがあります。工業炉市場の企業は、その地位を強化するためにいくつかの重要な戦略を採用しています。そのひとつが、よりエネルギー効率の高い持続可能な炉の開発など、技術革新への注力です。

各社は、電気アーク炉(EAF)の性能を向上させ、脱炭素目標を達成するために水素火炎のような代替手段を模索する研究開発に多額の投資を行っています。さらに、これらの企業は、自動車、航空宇宙、金属加工などの主要産業のメーカーとの戦略的提携や協力を通じて、グローバルフットプリントの拡大に取り組んでいます。もう一つの戦略は、様々な業界の特定のニーズを満たすためにカスタマイズされたソリューションを提供することで、市場での魅力を高め、長期的な顧客関係を確保することです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制の枠組み

- 規格と認証

- 環境規制

- 輸出入規制

- 貿易統計(HSコード8417)

- 主要輸入国

- 主要輸出国

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:炉タイプ別、2021年~2034年

- 主要動向

- 電気炉

- ガス炉

- 石油炉

- 石炭炉

- 誘導炉

- アーク炉

- その他

第6章 市場推計・予測:温度別、2021年~2034年

- 主要動向

- 低温(500℃以下)

- 中温(500℃~1000℃)

- 高温(1000℃以上)

第7章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 小

- 中

- 大

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙

- 非鉄金属

- 化学・石油化学

- 石油・ガス

- 食品・飲料

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

第11章 企業プロファイル

- ABB

- ANDRITZ AG

- Carbolite Gero

- Despatch Industries

- Gasbarre Thermal Processing Systems

- Harper International

- Inductotherm Group

- Ipsen International GmbH

- Lindberg/MPH

- Nabertherm GmbH

- Nutec Bickley

- SECO/WARWICK S.A.

- Surface Combustion, Inc.

- Tenova S.p.A.

- Wisconsin Oven Corporation

目次

The Global Industrial Furnaces Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 8.5 billion by 2034. The metal and steel industries are key contributors to this growth, as industrial furnaces are essential for high-temperature processes such as melting, annealing, and tempering, which are required for shaping and treating metals. Rising demand for infrastructure, automotive production, and industrial development, particularly in regions like China, India, and the U.S., is driving the need for more efficient and durable furnaces. The increasing adoption of electric arc furnaces (EAFs), which offer lower emissions and higher energy efficiency compared to traditional blast furnaces, is another important trend. EAFs now account for approximately 30% of global steel production, further increasing the demand for advanced furnace technologies worldwide.

In addition to the rising focus on decarbonization, industries are increasingly turning to alternative heating technologies like hydrogen flames and electric arcs to reduce their carbon footprint. These alternatives are seen as key solutions in the transition to more sustainable manufacturing processes. Hydrogen flames, for example, offer a clean burning option that emits only water vapor, making them an attractive choice for reducing emissions in high-temperature processes. Electric arc furnaces (EAFs), already popular in steel production, are also being explored for their ability to reduce carbon emissions compared to traditional furnace technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 4.8% |

The medium-temperature segment of the industrial furnaces market generated USD 2.2 billion in 2024 and is expected to reach USD 3.7 billion by 2034. Medium-temperature furnaces, which operate between 500°C and 1000°C, remain a dominant segment in the global market due to their versatility and ability to handle various heat-treatment processes. These furnaces are widely used across industries, from automotive and aerospace to electronics manufacturing, due to their ability to process metals and alloys.

The medium-capacity segment accounted for a 44.3% share in 2024 and is expected to grow at a CAGR of 4.4% through 2034. These furnaces are particularly favored for mid-sized industrial applications that require frequent temperature cycling and moderate throughput. Industries such as machinery manufacturing, auto parts production, and foundries rely on medium-temperature furnaces for consistent quality control and fulfilling production requirements.

United States Industrial Furnaces Market was valued at USD 700 million in 2024, with projections showing strong growth at a CAGR of 5.4% through 2034. The U.S. continues to lead the North American industrial furnaces market due to its advanced manufacturing capabilities and the increasing adoption of energy-efficient furnace technologies. Metal processing plants, aerospace workshops, and the automotive industry are driving demand for new, high-efficiency industrial furnaces, as these sectors work to reduce emissions and improve productivity. North America, particularly the U.S., Canada, and Mexico, holds a significant share of the global market due to the region's mature manufacturing base and focus on sustainable production practices.

Key players in the Industrial Furnaces Market include Harper International, SECO/WARWICK S.A., Tenova S.p.A., Despatch Industries, Carbolite Gero, Lindberg/MPH, Gasbarre Thermal Processing Systems, Nabertherm GmbH, Inductotherm Group, Surface Combustion, Inc., ABB, Ipsen International GmbH, Wisconsin Oven Corporation, Nutec Bickley, and ANDRITZ AG. Companies in the industrial furnaces market are adopting several key strategies to strengthen their position. One of the main approaches is focusing on technological innovation, such as the development of more energy-efficient and sustainable furnaces.

Companies are investing heavily in research and development to improve the performance of electric arc furnaces (EAFs) and explore alternatives like hydrogen flames to meet decarbonization targets. Additionally, these companies are working on expanding their global footprint through strategic partnerships and collaborations with manufacturers in key industries, such as automotive, aerospace, and metal processing. Another strategy is offering customized solutions to meet the specific needs of various industries, enhancing their market appeal and ensuring long-term customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Furnace type

- 2.2.3 Temperature

- 2.2.4 Capacity

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code- 8417)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Furnace Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Electric furnaces

- 5.3 Gas furnaces

- 5.4 Oil furnaces

- 5.5 Coal furnaces

- 5.6 Induction furnaces

- 5.7 Arc furnaces

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Temperature, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low temperature (Below 500°C)

- 6.3 Medium temperature (500°C - 1000°C)

- 6.4 High temperature (Above 1000°C)

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small

- 7.3 Medium

- 7.4 Large

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace

- 8.4 Non-Ferrous metals

- 8.5 Chemical and petrochemical

- 8.6 Oil and gas

- 8.7 Food and beverage

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 UAE

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 ANDRITZ AG

- 11.3 Carbolite Gero

- 11.4 Despatch Industries

- 11.5 Gasbarre Thermal Processing Systems

- 11.6 Harper International

- 11.7 Inductotherm Group

- 11.8 Ipsen International GmbH

- 11.9 Lindberg/MPH

- 11.10 Nabertherm GmbH

- 11.11 Nutec Bickley

- 11.12 SECO/WARWICK S.A.

- 11.13 Surface Combustion, Inc.

- 11.14 Tenova S.p.A.

- 11.15 Wisconsin Oven Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日