|

市場調査レポート

商品コード

1773323

タイヤバランスウェイトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Tire Balance Weight Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| タイヤバランスウェイトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

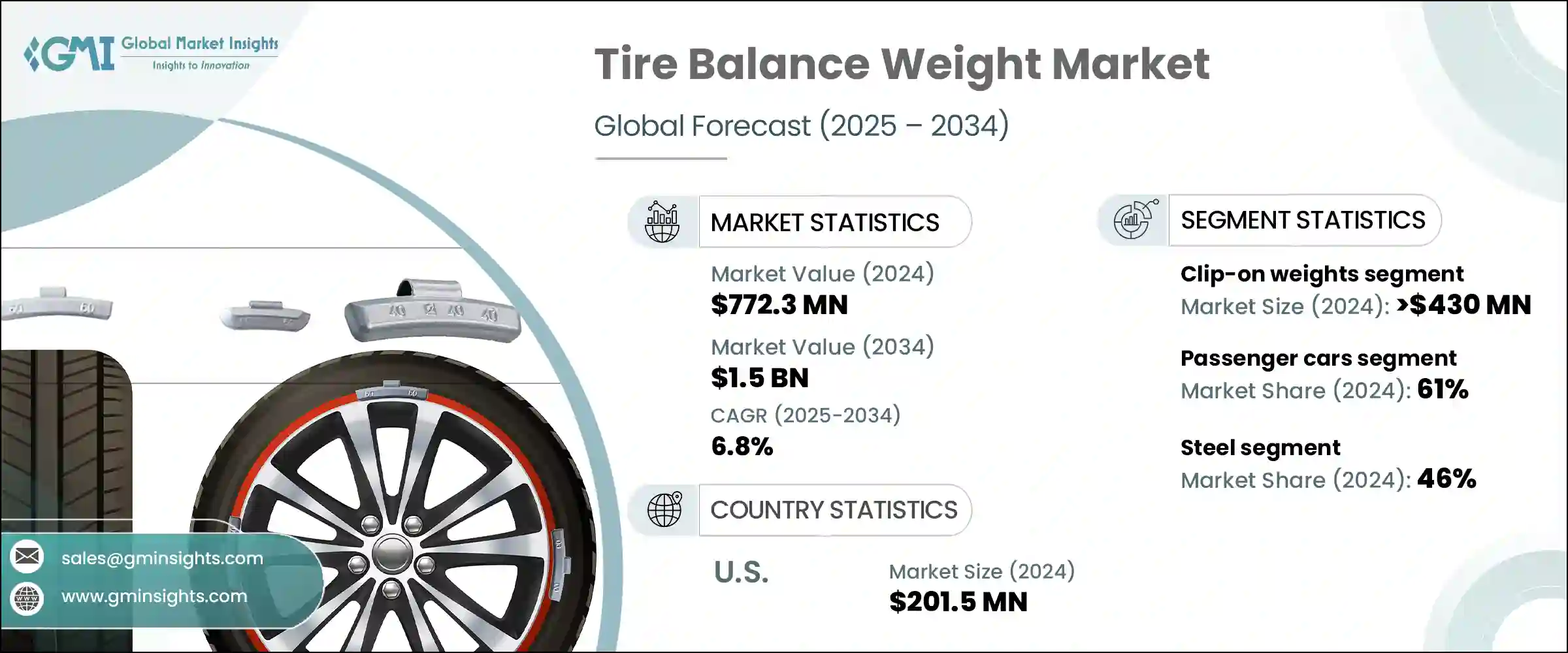

タイヤバランスウェイトの世界市場は、2024年には7億7,230万米ドルとなり、CAGR6.8%で成長し、2034年までには15億米ドルに達すると予測されています。

この成長の主な要因は、新興市場を中心とした世界の自動車生産の急増です。自動車の所有率が上昇し、商用車の保有台数が拡大するにつれて、ホイールバランシングを含む定期的なタイヤメンテナンスの需要は、特に移動ニーズの高い活気ある都市部で急増しています。さらに、公共部門によるインフラ投資の増加や、ロジスティクス、旅客輸送、eコマース部門による輸送需要の高まりが、車両整備活動を活発化させ、タイヤバランスウェイトに対する旺盛なニーズを生み出しています。これらの部品は自動車の安全性と乗り心地を確保する上で重要な役割を果たしているため、その需要は当然ながら世界の自動車台数とともに拡大しています。

各地域の政府や規制機関は、安全基準や道路遵守基準を強化しており、これも市場を牽引しています。タイヤバランスウェイトによって可能になる適切なホイールバランスは、不要な振動を排除し、タイヤの寿命を延ばし、高速走行時の安全性を向上させ、全体的なメンテナンスコストを削減します。特に北米、欧州、アジアでは、こうした規制の遵守が強化されているため、自動車事業者は定期的なタイヤメンテナンスを採用せざるを得ず、需要が高まっています。さらに、規制遵守と消費者および車両運行者の車両性能と安全性に関する意識の高まりが組み合わさって、市場の着実な拡大を支える基本的な要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 7億7,230万米ドル |

| 予測金額 | 15億米ドル |

| CAGR | 6.8% |

2024年、クリップオン分銅セグメントは4億3,000万米ドルを生み出し、市場における支配的地位を維持しました。従来は鉛から製造されていましたが、規制上の制約から多くの地域で亜鉛やスチールの代替品にシフトしており、製造工程の再設計や新素材の調達に関連する製造コストが上昇しています。商用車や格安車に大きく依存している新興経済諸国では、特に南米、東欧、アジアの一部のように合金ホイールが一般的でない地域では、依然としてクリップオンウェイトが主に使用されています。こうした需要に対応するため、メーカーは先進合金、ポリマーコーティング鋼、亜鉛コーティング鋼を含む新素材の開発に注力しています。

乗用車セグメントは2024年に61%のシェアを占め、予測期間中にかなりの成長が見込まれます。乗用車における合金ホイールの人気の高まりは、ホイール表面の損傷を防ぎ、車両の外観を向上させるスティックオンウェイトのような革新的なバランシング技術に対する需要の増加につながっています。この動向は、消費者が性能と美観の両方を優先する都市部や高級車セグメントで強いです。乗用車が古くなるにつれて、その再販価値とメンテナンス価値は、バランシングサービスに対するアフターマーケット需要の持続を促しています。

北米のタイヤバランスウェイト市場は2024年に30%のシェアを占め、米国が2億150万米ドルを拠出しています。この地域は、レーザー測定、2点最適化、デジタル診断を組み込んだ自動バランシング機械の進歩から利益を得ています。これらの技術革新は、サービスの精度と効率を向上させるだけでなく、タイヤ空気圧モニタリングシステムとの統合を可能にし、車両全体の安全性と性能を高めます。Hunter EngineeringやCEMBのような業界リーダーは、市場のデジタル変革の最前線におり、北米をよりスマートで精密なバランシング技術へと押し上げています。さらに、厳しい環境規制により、同地域では鉛ベースのウェイトが全廃され、より安全で環境に優しい代替品の採用が加速しています。

世界のタイヤバランスウェイト市場を独占している主要企業には、Baolong Automotive Corp.、3M Company、Hunter Engineering Company、Hennessy Industries(現Coats Company)、TOHO KOGYO Co.、Plombco、WEGMANN Automotiveなどがあります。

タイヤバランスウェイト分野の主要企業は、市場での存在感を強め、足場を広げるために、いくつかの戦略的アプローチを採用しています。素材と製造工程における革新は主要な焦点であり、企業は従来の鉛製ウェイトに代わる、環境に優しく軽量で耐久性のある代替品の開発に多額の投資を行っています。これにより、進化する環境規制への準拠が可能になると同時に、より高い性能を求める顧客の需要にも応えることができます。さらに、企業は生産設備とサービス設備に自動化とデジタル技術の統合を採用し、精度を高め、ターンアラウンド時間を短縮することで、OEMとフリートオペレーターにアピールしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- アフターサービスとタイヤ交換の増加

- 車両の安全に関する規制の強化

- 鉛から無毒物質への環境転換

- タイヤとホイールの設計における技術的進歩

- 業界の潜在的リスク・課題

- 発展途上地域における意識の欠如

- 先進国の市場飽和

- 市場機会

- 鉛フリーおよび環境に優しい材料の需要の高まり

- EVとハイブリッド車の普及率増加

- 自動車アフターマーケットサービスの急速な拡大の新たな動向

- スマートワークショップ技術の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- クリップオンウェイト

- 粘着式ウェイト

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 鋼鉄

- 亜鉛

- 鉛

- その他

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV(スポーツ用多目的車)

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

- 二輪車

- オフロード車

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車工場

- タイヤショップ

- 自動車メーカー

- フリートオペレーター

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- 3M Company

- Alpha Autoparts

- Baolong Automotive Corp.

- Bharat Balancing Weights Pvt.

- Cangzhou Yaqiya Auto Parts(Yaqiya)

- Hatco/HARTEC s.a.l.

- HEBEI FANYA

- HEBEI XST

- Hennessy Industries(now Coats Company)

- Holman

- Hunter Engineering Company

- John Bean Technologies Corp.

- Micro-Poise Measurement Systems(AMETEK)

- Plombco Inc.

- Shengshi Weiye(Cangzhou Shengshiweiye)

- Snap-on Incorporated

- TOHO KOGYO Co.

- Trax JH

- WEGMANN Automotive

- Wurth USA

The Global Tire Balance Weight Market was valued at USD 772.3 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 1.5 billion by 2034. This growth is largely fueled by the rapid increase in automobile production worldwide, particularly in emerging markets. As car ownership rises and commercial vehicle fleets expand, the demand for regular tire maintenance, including wheel balancing, has surged, especially in bustling urban centers with high mobility needs. Furthermore, growing investments by public sectors in infrastructure and the rising transportation demands driven by logistics, passenger transit, and e-commerce sectors have intensified fleet servicing activities, creating a robust need for tire balance weights. Since these components play a critical role in ensuring vehicle safety and ride comfort, their demand naturally scales alongside the global vehicle population.

Governments and regulatory bodies across various regions are tightening safety and road compliance standards, which also drives the market. Proper wheel balancing-made possible through tire balance weights-eliminates unwanted vibrations, extends tire lifespan, improves driving safety at high speeds, and reduces overall maintenance costs. Enhanced adherence to these regulations, especially in North America, Europe, and Asia, is compelling vehicle operators to adopt routine tire maintenance, thereby bolstering demand. Moreover, the combination of regulatory compliance and rising consumer and fleet operator awareness about vehicle performance and safety continues to be a fundamental driver behind the market's steady expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 6.8% |

In 2024, the clip-on weights segment generated USD 430 million in 2024, maintaining a dominant position in the market. Traditionally manufactured from lead, many regions have shifted toward zinc or steel alternatives due to regulatory restrictions, which have increased production costs related to redesigning manufacturing processes and sourcing new materials. Developing economies, which rely heavily on commercial fleets and budget vehicles, still predominantly use clip-on weights, especially where alloy wheels are less common, such as in South America, Eastern Europe, and parts of Asia. To meet these demands, manufacturers are focusing on developing new materials including advanced alloys, polymer-coated steel, and zinc-coated steel.

The passenger car segment held a 61% share in 2024 and is expected to experience considerable growth over the forecast period. The rising popularity of alloy wheels in passenger vehicles has led to increased demand for innovative balancing techniques such as stick-on weights, which prevent damage to the wheel surface and enhance vehicle appearance. This trend is strong in urban areas and higher-end vehicle segments, where consumers prioritize both performance and aesthetics. As passenger cars age, their resale and maintenance values encourage sustained aftermarket demand for balancing services.

North America Tire Balance Weight Market held a 30% share in 2024, with the United States contributing USD 201.5 million. The region benefits from advancements in automated balancing machinery that incorporate laser measurement, two-point optimization, and digital diagnostics. These innovations not only improve service accuracy and efficiency but also enable integration with tire pressure monitoring systems, enhancing overall vehicle safety and performance. Industry leaders like Hunter Engineering and CEMB are at the forefront of digital transformation in the market, pushing North America toward smarter, more precise balancing technologies. Additionally, strict environmental regulations have led to a complete phase-out of lead-based weights in the region, accelerating the adoption of safer, eco-friendly alternatives.

Key players dominating the Global Tire Balance Weight Market include Baolong Automotive Corp., 3M Company, Hunter Engineering Company, Hennessy Industries (now Coats Company), TOHO KOGYO Co., Plombco, and WEGMANN Automotive.

Leading companies in the tire balance weight sector employ several strategic approaches to strengthen their market presence and expand their foothold. Innovation in materials and manufacturing processes is a primary focus, with firms investing heavily in developing eco-friendly, lightweight, and durable alternatives to traditional lead weights. This enables compliance with evolving environmental regulations while meeting customer demand for higher performance. Additionally, companies are embracing automation and digital technology integration in production and service equipment, which enhances precision and reduces turnaround times, appealing to OEMs and fleet operators alike.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 End use

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in aftermarket services & tire replacement

- 3.2.1.2 Stricter regulations for vehicle safety

- 3.2.1.3 Environmental shift from lead to non-toxic materials

- 3.2.1.4 Technological advancements in tire & wheel design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of awareness in developing regions

- 3.2.2.2 Market saturation in developed economies

- 3.2.3 Market opportunities

- 3.2.3.1 Surging demand for lead-free and eco-friendly materials

- 3.2.3.2 Rising EV and hybrid vehicle adoption

- 3.2.3.3 Emerging trends of rapid expansion in automotive aftermarket services

- 3.2.3.4 Integration of smart workshop technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Clip-on weights

- 5.3 Adhesive/Stick-on weights

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Zinc

- 6.4 Lead

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUVs (Sport utility vehicles)

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

- 7.4 Two-wheelers

- 7.5 Off-road vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 Automotive workshops

- 8.3 Tire shops

- 8.4 Vehicle manufacturers

- 8.5 Fleet operators

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M Company

- 11.2 Alpha Autoparts

- 11.3 Baolong Automotive Corp.

- 11.4 Bharat Balancing Weights Pvt.

- 11.5 Cangzhou Yaqiya Auto Parts (Yaqiya)

- 11.6 Hatco / HARTEC s.a.l.

- 11.7 HEBEI FANYA

- 11.8 HEBEI XST

- 11.9 Hennessy Industries (now Coats Company)

- 11.10 Holman

- 11.11 Hunter Engineering Company

- 11.12 John Bean Technologies Corp.

- 11.13 Micro-Poise Measurement Systems (AMETEK)

- 11.14 Plombco Inc.

- 11.15 Shengshi Weiye (Cangzhou Shengshiweiye)

- 11.16 Snap-on Incorporated

- 11.17 TOHO KOGYO Co.

- 11.18 Trax JH

- 11.19 WEGMANN Automotive

- 11.20 Wurth USA