|

市場調査レポート

商品コード

1773319

軍用非ステアラブルアンテナの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Military Non-steerable Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 軍用非ステアラブルアンテナの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

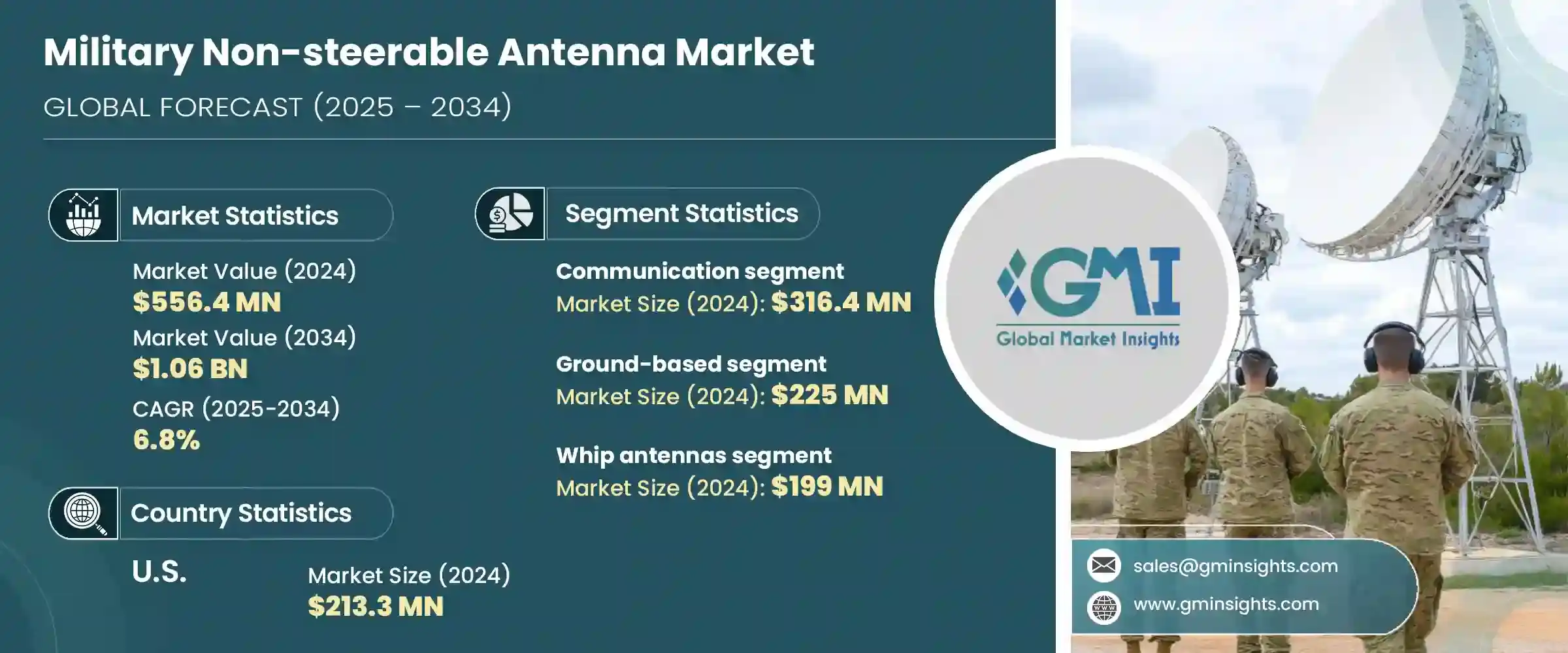

軍用非ステアラブルアンテナの世界市場は、2024年には5億5,640万米ドルとなり、CAGR6.8%で成長し、2034年までには10億6,000万米ドルに達すると予測されています。

市場の拡大は、無人システムの台頭と遠隔監視業務への注目の高まりによって推進されています。各国が国防予算を拡大し、戦術作戦がより複雑になるにつれ、頑丈でメンテナンスフリーの通信システムへの需要が高まっています。全方向への到達性、迅速な展開、高い耐久性で知られる軍用非ステアラブルアンテナは、防衛通信において不可欠な資産となっています。これらのシステムは、積極的な妨害や信号干渉が存在する場合でも、ダイナミックで電子的に争いの多い環境下で音声、データ、コマンド信号を伝送するために不可欠です。

現代の戦争では、統合部隊の連携やリアルタイムの領域横断通信が重視されるため、これらのアンテナは戦闘車両、海軍艦隊、前方作戦基地、監視インフラに搭載されています。インド、米国、中国、NATO加盟国などの世界大国は、堅牢でインフラが軽いシステムの設置を優先しています。戦場での通信を強化する動きが強まる中、各国はロジスティクスの複雑さを軽減しながら高い可用性を提供するシステムに積極的に投資しており、非ステアラブルアンテナを今日のデジタル防衛アーキテクチャにおける好ましいソリューションとして位置付けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 5億5,640万米ドル |

| 予測金額 | 10億6,000万米ドル |

| CAGR | 6.8% |

電子戦セグメントは、非ステアラブルアンテナがジャミング、信号傍受、パッシブ偵察などの作戦をサポートする役割を果たすことにより、2034年までCAGR8.6%で成長する見込みです。軽量固定アンテナは、状況認識を提供し、スペクトラム制御を強化するために、電子戦システムへの統合が進んでいます。これらのシステムはさらに小型化され、無人航空機プラットフォーム用に適応され、セットアップ時間の短縮と生存性の向上で柔軟な戦術的配備を可能にしています。

空中プラットフォーム分野は、2025年から2034年にかけてCAGR8.2%で成長すると予想されています。この急成長は、ISR(情報・監視・偵察)任務の必要性が高まり、有人機と無人機の両方への依存度が高まっていることが主な要因です。このような新たな需要に対応するため、高周波通信や電子戦能力をサポートする耐振動性でコンパクトな非ステアラブルアンテナが配備されています。最新の防衛構想では、これらのアンテナを空中通信スイートに組み込み、戦闘区域や戦略的作戦区域を横断する安全なリンクを確保しています。

ドイツの軍用非ステアラブルアンテナ市場は2024年に2,000万米ドルと評価されました。NATOとの協力や国内近代化プログラムを通じて通信インフラの強化に注力していることが需要を押し上げています。ドイツは、ミッションの弾力性と戦略的自律性のために、安全な多周波システムに投資しています。HENSOLDTやRohde &Schwarzといった著名な防衛関連企業は、生産やシステム開発で大きな役割を果たしています。軍事環境における5Gの採用やサイバーセキュア通信の強化に向けた国家規模のプログラムが、この市場を押し上げる大きな要因となっています。

軍用非ステアラブルアンテナ市場をリードする主要企業には、MTI Wireless Edge、Abracon、HR Smith Group of Companies、L3Harris Technologies, Inc、Hascall-Denke、Rohde & Schwarzなどがあります。軍用非ステアラブルアンテナ分野の主要企業は、戦略的イノベーション、グローバルフパートナーシップ、素材の進化に注力し、存在感を高めています。その多くは、空、陸、海の各システムにまたがるマルチプラットフォーム統合に最適化された、小型、軽量、堅牢なアンテナ設計を開発しています。これらの企業は、進化する周波数需要、電磁波耐性、相互運用性規格を満たすための研究開発に投資しています。防衛省やOEMとの協力により、ミッションクリティカルなプログラムへのオーダーメイドのシステム展開が可能になっています。また、防衛調達政策を遵守し、納期を向上させるために、現地生産を行う企業も増えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 世界の国防予算の増加

- 堅牢な戦場通信の需要増加

- 戦術的および機動的な軍事部隊の拡大

- 無人システムと遠隔監視の成長

- メンテナンスの手間が少なく、費用対効果の高いアンテナソリューションの必要性

- 業界の潜在的リスク・課題

- 方向制御の制限により信号精度に影響が出る

- 電子戦と信号干渉に対する脆弱性

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:アンテナタイプ別、2021年~2034年

- 主要動向

- ブレードアンテナ

- ホイップアンテナ

- パッチアンテナ

- コンフォーマルアンテナ

- ラバーダッキーアンテナ

- ループアンテナ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コミュニケーション

- ナビゲーション

- 電子戦

第7章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- 地上配備型

- 海軍型

- 空挺型

- 携帯型

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Abeillon

- Abracon

- Antcom

- CBG Systems

- Chelton Limited

- Comrod Communication AS

- Fei Teng Wireless Technology

- Hascall-Denke

- HR Smith Group of Companies

- KNL

- L3Harris Technologies, Inc.

- MTI Wireless Edge

- RAMI

- Rohde &Schwarz

- Rojone Pty Ltd

- Thales

The Global Military Non-steerable Antenna Market was valued at USD 556.4 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 1.06 billion by 2034. The market expansion is being propelled by the rise of unmanned systems and increased focus on remote surveillance operations. With countries expanding their defense budgets and tactical operations becoming more intricate, the demand for rugged and maintenance-free communication systems has intensified. Military non-steerable antennas, known for their all-directional reach, rapid deployment, and high durability, have become essential assets in the defense communication landscape. These systems are vital for transmitting voice, data, and command signals across dynamic and electronically contested environments, even where active jamming or signal interference exists.

As modern warfare emphasizes joint-force coordination and real-time cross-domain communication, these antennas are being mounted on combat vehicles, naval fleets, forward operating bases, and surveillance infrastructure. Global powers such as India, the United States, China, and members of NATO are prioritizing the installation of robust, infrastructure-light systems. With a growing push for hardened battlefield communications, countries are actively investing in systems that provide high availability with reduced logistical complexity, positioning non-steerable antennas as a preferred solution in today's digital defense architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $556.4 Million |

| Forecast Value | $1.06 Billion |

| CAGR | 6.8% |

The electronic warfare segment is expected to grow at a CAGR of 8.6% through 2034, driven by the role non-steerable antennas play in supporting operations such as jamming, signal interception, and passive surveillance. Lightweight fixed antennas are being increasingly integrated into electronic warfare systems to provide situational awareness and enhance spectrum control. These systems are being further miniaturized and adapted for unmanned aerial platforms, enabling flexible tactical deployments with reduced setup time and improved survivability.

The airborne platforms segment is expected to grow at a CAGR of 8.2% between 2025 and 2034. This surge is largely due to the intensifying need for ISR (intelligence, surveillance, and reconnaissance) missions and growing reliance on both manned and unmanned aircraft. Vibration-resistant, compact non-steerable antennas that support high-frequency communication and electronic warfare capabilities are being deployed to meet these new demands. Modern defense initiatives are embedding these antennas in airborne communication suites to ensure secure links across combat zones and strategic areas of operation.

Germany Military Non-steerable Antenna Market accounted for USD 20 million in 2024. The country's focus on strengthening its communication infrastructure through NATO collaboration and internal modernization programs is boosting demand. Germany is investing in secure, multi-frequency systems for mission resilience and strategic autonomy. Prominent defense companies such as HENSOLDT and Rohde & Schwarz are playing a major role in production and system development. Nationwide programs geared toward adopting 5G in military environments and enhancing cyber secure communications are major factors driving this market upward.

Key companies leading the Military Non-steerable Antenna Market include MTI Wireless Edge, Abracon, HR Smith Group of Companies, L3Harris Technologies, Inc., Hascall-Denke, and Rohde & Schwarz. Leading firms in the military non-steerable antenna space are focusing on strategic innovation, global partnerships, and material advancements to strengthen their presence. Many are developing compact, lightweight, and ruggedized antenna designs optimized for multi-platform integration across air, land, and sea systems. These companies invest in R&D to meet evolving frequency demands, electromagnetic resilience, and interoperability standards. Collaborations with defense ministries and OEMs allow tailored system deployment in mission-critical programs. Businesses are also localizing production to comply with defense procurement policies and enhance delivery timelines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising defense budgets globally

- 3.3.1.2 Increased demand for robust battlefield communication

- 3.3.1.3 Expansion of tactical and mobile military units

- 3.3.1.4 Growth in unmanned systems and remote surveillance

- 3.3.1.5 Need for low-maintenance and cost-effective antenna solutions

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Limited directional control affecting signal precision

- 3.3.2.2 Vulnerability to electronic warfare and signal interference

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Antenna Type, 2021 – 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Blade antennas

- 5.3 Whip antennas

- 5.4 Patch antennas

- 5.5 Conformal antennas

- 5.6 Rubbery ducky antennas

- 5.7 Loop antennas

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Communication

- 6.3 Navigation

- 6.4 Electronic warfare

Chapter 7 Market Estimates and Forecast, By Platform, 2021 – 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Ground-based

- 7.3 Naval

- 7.4 Airborne

- 7.5 Man-portable

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abeillon

- 9.2 Abracon

- 9.3 Antcom

- 9.4 CBG Systems

- 9.5 Chelton Limited

- 9.6 Comrod Communication AS

- 9.7 Fei Teng Wireless Technology

- 9.8 Hascall-Denke

- 9.9 HR Smith Group of Companies

- 9.10 KNL

- 9.11 L3Harris Technologies, Inc.

- 9.12 MTI Wireless Edge

- 9.13 RAMI

- 9.14 Rohde & Schwarz

- 9.15 Rojone Pty Ltd

- 9.16 Thales