プレス・吹きガラスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Pressed and Blown Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773312

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

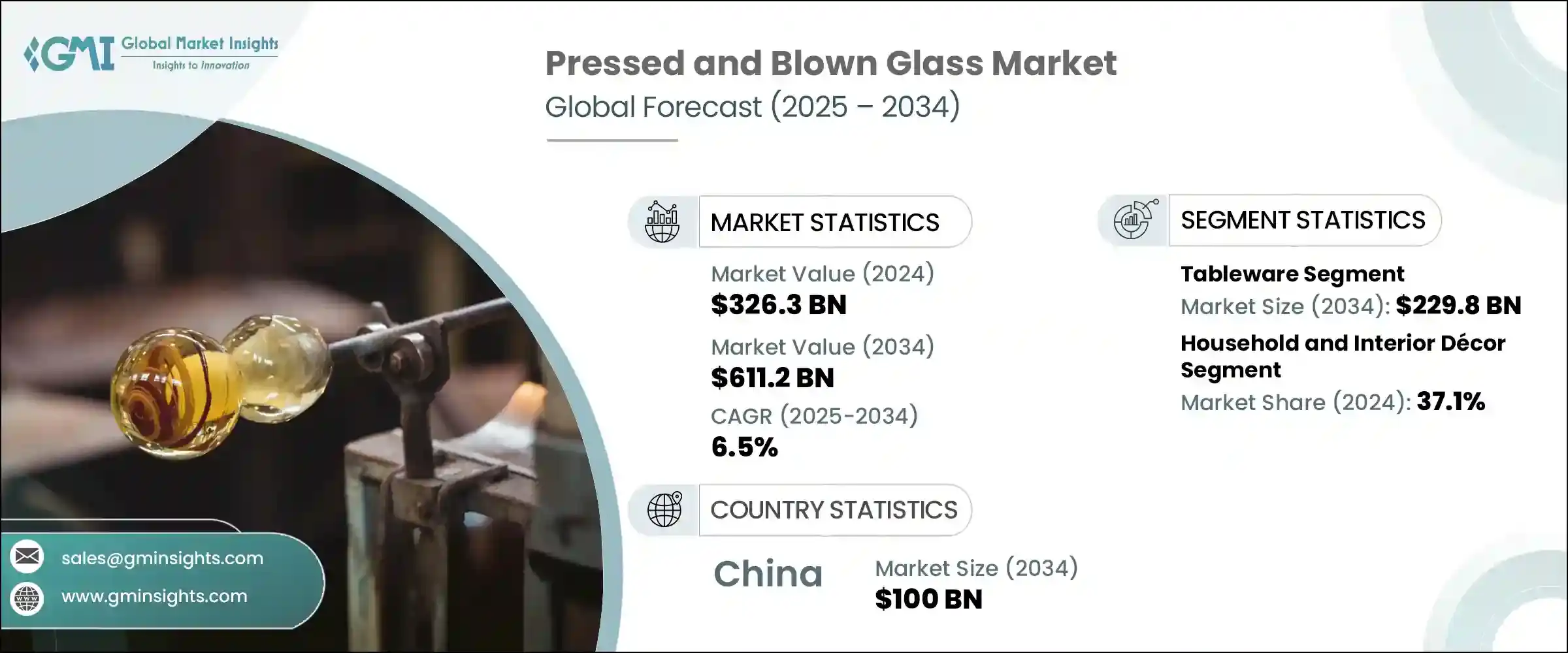

プレス・吹きガラスの世界市場規模は、2024年に3,263億米ドルとなり、CAGR6.5%で成長し、2034年までには6,112億米ドルに達すると予測されています。

同市場は、成形技術の進化、建築用途の拡大、装飾用途や包装用途の需要の高まりによって推進されています。アジア太平洋市場では、産業の拡大と消費者の豊かさの増大が、様々な分野でのガラス製品の採用を後押ししており、大きな勢いを見せています。

消費者の選好が性能と美観の双方を重視するように変化する中、ガラスはその機能的な汎用性と現代的なデザインにおける視覚的な魅力から、ますます好まれるようになっています。包装やインテリアなどの分野では、耐久性がありリサイクル可能なガラス素材が、持続可能性の低い代替素材に取って代わりつつあります。さらに、自動化されたブロー工程やプレス工程における技術的なアップグレードにより、メーカーはカスタムメイドの要件を満たしながら大規模な生産を行うことができます。AIを統合したモニタリングやロボット成形のような先進的なツールが普及し、生産成果と品質管理を向上させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3,263億米ドル |

| 予測金額 | 6,112億米ドル |

| CAGR | 6.5% |

欧州と北米の事業は自動化を導入し、スピードと効率を向上させ、企業が消費者の期待の高まりに応えるのに役立っています。この市場は、世界の持続可能性の目標に沿った、環境に配慮した生産方法への継続的な投資によってさらに支えられています。吹きガラスは、パーソナライズされたハイエンドの装飾製品への需要の高まりにより、牽引力を増しています。一方、プレスガラスは依然として容器製造の主要素材であり、医薬品、美容、飲料などの業界で重要な役割を果たしています。

テーブルウェア分野は、2024年に1,212億米ドルを生み出し最大の市場シェアを占め、2034年には2,298億米ドルに達し、CAGR6.7%で成長すると予測されています。ドリンクウェア、プレート、サービングアイテムを含むガラス製テーブルウェアは、その衛生性、耐熱性、長期的な使用性から引き続き高い需要があります。環境に配慮した食習慣を求める動きは、消費者のプラスチックや陶器離れを促しています。職人の手仕事やミニマルで透明な食器を好むデザイン動向は、北米や欧州などの主要市場でガラス食器の売上を加速させています。

家庭用・室内装飾品カテゴリーは2024年に37.1%のシェアを獲得します。この成長を後押ししているのは、都市開発、モダンな生活美学への関心の高まり、多機能装飾品の特注注文です。ガラスの花瓶、照明器具、アートピース、アクセントパネルなどのアイテムは、特に手作りや持続可能な方法で生産されたものに人気が集まっています。長持ちし、環境に優しいインテリアアイテムに対する消費者の選好は、アジア太平洋、欧州、北米を含むいくつかの地域で、プレス加工と手吹きの両方のデザインの使用を促進しています。

中国のプレス・吹きガラス市場は2024年に527億米ドルとなり、CAGR6.7%で成長し、2034年には1,000億米ドルに達すると予想されます。この拡大は、消費の増加、機械化された製造業の改善、よりインテリジェントな生産システムへの移行に結びついています。中国の生産者は持続可能性を重視し、コスト削減と環境への影響を最小限に抑えるため、より多くの再生カレットを生産に組み込んでいます。若い世代がカスタムメイドやデジタルガラス製品の動向を形成し、ユニークな美的感覚や機能的なエレガンスへの需要を促進しています。

同市場の主要企業には、Krosno Glass S.A.、Libbey Inc.、Arc Holdings、Bormioli Rocco、Sisecam Group傘下のPasabahceなどがあります。プレス・吹きガラス市場の主要企業は、生産性向上とエラー削減のために技術統合を優先しています。ロボット成形システムやAIを活用した品質検査ツールは、一貫性の向上と生産時間の短縮のために広く導入されています。持続可能なソリューションに対する需要の高まりに対応するため、多くの企業がリサイクル原材料の使用やエネルギー効率の高いプロセスの採用にシフトしています。デジタルデザインプラットフォームへの投資により、これらのブランドは製品の迅速な試作とカスタマイズが可能になり、産業界の顧客とデザインに敏感な消費者の両方に対応しています。さらに、デザイナーや小売業者との戦略的パートナーシップにより、企業はスタイルと機能において常に最先端を行くことができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 食器

- グラス

- タンブラー

- 脚付きグラス

- マグカップ・カップ

- ショットグラス

- その他

- 食器

- プレート

- ボウル

- サービングディッシュ

- その他

- サーブウェア

- ピッチャー・デカンタ

- トレイ・大皿

- その他

- グラス

- コンテナ

- ボトル

- 飲料ボトル

- 医薬品ボトル

- 化粧品・香水のボトル

- その他

- 瓶

- 食品瓶

- 化粧品の瓶

- その他

- バイアル・アンプル

- その他

- ボトル

- 装飾ガラス

- 人形と彫刻

- 花瓶とボウル

- 装飾品

- その他

- 照明製品

- ランプシェード

- シャンデリアとペンダント

- その他

- 技術および工業用ガラス

- 実験用ガラス器具

- 技術コンポーネント

- その他

- その他

第6章 市場推計・予測:ガラスタイプ別、2021年~2034年

- 主要動向

- ソーダ石灰ガラス

- ホウケイ酸ガラス

- クリスタルガラス

- 鉛クリスタル

- 鉛フリークリスタル

- 耐熱ガラス

- 色ガラス

- その他

第7章 市場推計・予測:製造工程別、2021年~2034年

- 主要動向

- プレス工程

- シングルゴブ

- ダブルゴブ

- トリプルゴブ

- ブロープロセス

- 吹いて吹いて

- 押して吹く

- ナローネックプレスアンドブロー(NNPB)

- 複合プロセス

- 手作りのプロセス

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品と飲料

- アルコール飲料

- ノンアルコール飲料

- 食品包装

- その他

- 医薬品

- パッケージ

- 実験装置

- その他

- 化粧品とパーソナルケア

- 香水とフレグランス

- スキンケア製品

- その他

- 家庭用品と室内装飾

- 食器

- 装飾品

- 点灯

- その他

- ホスピタリティとフードサービス

- ホテルとレストラン

- バーやパブ

- ケータリングサービス

- その他

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- B2B/直接販売

- メーカーから小売業者へ

- メーカーから卸売業者へ

- メーカーが最終用途に

- 小売り

- ハイパーマーケット/スーパーマーケット

- 専門店

- デパート

- その他

- オンライン小売

- 企業のウェブサイト

- eコマースプラットフォーム

- その他

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Anchor Hocking LLC

- Arc International

- Ardagh Group S.A.

- Beatson Clark Ltd.

- Bormioli Rocco S.p.A.

- Borosil Limited

- Garbo Glassware Co., Ltd.

- Gerresheimer AG

- Glass Dynamics LLC

- Kopp Glass, Inc.

- Libbey Inc.

- O-I Glass, Inc.(Owens-Illinois)

- Piramal Glass Limited

- Rayotek Scientific Inc.

- Saverglass SAS

- SCHOTT AG

- Sisecam Group

- Steelite International

- Stoelzle Glass Group

- Verallia

- Vetropack Holding Ltd.

- Vidrala S.A.

- Vitro, S.A.B. de C.V.

- Wiegand-Glas GmbH

- Zwiesel Kristallglas AG

目次

The Global Pressed and Blown Glass Market was valued at USD 326.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 611.2 billion by 2034. The market is being propelled by the evolution of molding technologies, expanding architectural applications, and heightened demand for decorative and packaging uses. Significant momentum is being generated in Asia-Pacific markets, where industrial expansion and growing consumer affluence are supporting glass product adoption across multiple verticals.

Glass is increasingly favored for its functional versatility and visual appeal in modern design, with shifting consumer preferences emphasizing both performance and aesthetics. In sectors like packaging and interiors, durable and recyclable glass materials are replacing less sustainable alternatives. Additionally, technological upgrades in automated blowing and pressing processes allow manufacturers to produce at scale while meeting custom requirements. Advanced tools like AI-integrated monitoring and robotic forming are gaining traction, improving production outcomes and quality control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $326.3 Billion |

| Forecast Value | $611.2 Billion |

| CAGR | 6.5% |

European and North American operations have embraced automation, enhanced speed and efficiency, and helping companies meet rising consumer expectations. The market is further supported by ongoing investments in eco-conscious production methods, as the industry aligns itself with global sustainability goals. Blown glass is gaining traction due to rising demand for personalized and high-end decorative products. Meanwhile, pressed glass remains a dominant material in container manufacturing, playing a crucial role in industries such as pharmaceuticals, beauty, and beverages.

The tableware segment held the largest market share in 2024, generating USD 121.2 billion, and is projected to hit USD 229.8 billion by 2034, growing at a CAGR of 6.7%. Glass tableware-including drinkware, plates, and serving items-continues to be in high demand for its hygiene, thermal resistance, and long-term usability. The movement toward environmentally friendly dining habits is steering consumers away from plastics and ceramics. Design trends favoring artisan craftsmanship and minimal, transparent serveware have helped accelerate glass tableware sales in key markets such as North America and Europe.

The household and interior decor category captured a 37.1% share in 2024. This growth is being fueled by urban development, increased interest in modern living aesthetics, and custom orders for multifunctional decorative pieces. Items like glass vases, lighting fixtures, art pieces, and accent panels are seeing a rise in popularity, especially those that are handcrafted or sustainably produced. Consumer preference for long-lasting, eco-friendly interior elements is promoting greater use of both pressed and hand-blown designs across several regions including parts of Asia-Pacific, Europe, and North America.

China Pressed and Blown Glass Market generated USD 52.7 billion in 2024 and is expected to grow at a CAGR of 6.7%, reaching USD 100 billion by 2034. This expansion is tied to rising consumption, improvements in mechanized manufacturing, and a transition to more intelligent production systems. Chinese producers are placing greater emphasis on sustainability, integrating more recycled cullet into production to cut costs and minimize environmental impact. Younger generations are shaping trends in custom and digital glassware, fostering demand for unique aesthetics and functional elegance.

Leading players in the market include Krosno Glass S.A., Libbey Inc., Arc Holdings, Bormioli Rocco, and Pasabahce under the Sisecam Group. Major companies in the pressed and blown glass market are prioritizing technological integration to enhance productivity and reduce errors. Robotic forming systems and AI-powered quality inspection tools are being widely deployed to improve consistency and cut production time. To meet the growing demand for sustainable solutions, many firms are shifting toward using recycled raw materials and adopting energy-efficient processes. Investments in digital design platforms allow these brands to quickly prototype and customize products, catering to both industrial clients and design-conscious consumers. Strategic partnerships with designers and retail distributors further enable companies to stay ahead in style and function.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Tableware

- 5.2.1 Drinking glasses

- 5.2.1.1 Tumblers

- 5.2.1.2 Stemware

- 5.2.1.3 Mugs and cups

- 5.2.1.4 Shot glasses

- 5.2.1.5 Others

- 5.2.2 Dinnerware

- 5.2.2.1 Plates

- 5.2.2.2 Bowls

- 5.2.2.3 Serving dishes

- 5.2.2.4 Others

- 5.2.3 Serveware

- 5.2.3.1 Pitchers and decanters

- 5.2.3.2 Trays and platters

- 5.2.3.3 Others

- 5.2.1 Drinking glasses

- 5.3 Containers

- 5.3.1 Bottles

- 5.3.1.1 Beverage bottles

- 5.3.1.2 Pharmaceutical bottles

- 5.3.1.3 Cosmetic and perfume bottles

- 5.3.1.4 Others

- 5.3.2 Jars

- 5.3.2.1 Food jars

- 5.3.2.2 Cosmetic jars

- 5.3.2.3 Others

- 5.3.3 Vials and ampoules

- 5.3.4 Others

- 5.3.1 Bottles

- 5.4 Decorative glass

- 5.4.1 Figurines and sculptures

- 5.4.2 Vases and bowls

- 5.4.3 Ornaments

- 5.4.4 Others

- 5.5 Lighting products

- 5.5.1 Lamp shades

- 5.5.2 Chandeliers and pendants

- 5.5.3 Others

- 5.6 Technical and industrial glass

- 5.6.1 Laboratory glassware

- 5.6.2 Technical components

- 5.6.3 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Glass Type, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Soda-lime glass

- 6.3 Borosilicate glass

- 6.4 Crystal glass

- 6.4.1 Lead crystal

- 6.4.2 Lead-free crystal

- 6.5 Heat-resistant glass

- 6.6 Colored glass

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Press process

- 7.2.1 Single gob

- 7.2.2 Double gob

- 7.2.3 Triple gob

- 7.3 Blow process

- 7.3.1 Blow and blow

- 7.3.2 Press and blow

- 7.3.3 Narrow neck press and blow (NNPB)

- 7.4 Combined processes

- 7.5 Hand-crafted processes

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.2.1 Alcoholic beverages

- 8.2.2 Non-alcoholic beverages

- 8.2.3 Food packaging

- 8.2.4 Others

- 8.3 Pharmaceutical

- 8.3.1 Packaging

- 8.3.2 Laboratory equipment

- 8.3.3 Others

- 8.4 Cosmetics and personal care

- 8.4.1 Perfumes and fragrances

- 8.4.2 Skincare products

- 8.4.3 Others

- 8.5 Household and interior decor

- 8.5.1 Tableware

- 8.5.2 Decorative items

- 8.5.3 Lighting

- 8.5.4 Others

- 8.6 Hospitality and foodservice

- 8.6.1 Hotels and restaurants

- 8.6.2 Bars and pubs

- 8.6.3 Catering services

- 8.6.4 Others

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 B2b/direct sales

- 9.2.1 Manufacturers to retailers

- 9.2.2 Manufacturers to wholesalers

- 9.2.3 Manufacturers to end use

- 9.3 Retail

- 9.3.1 Hypermarkets/supermarkets

- 9.3.2 Specialty stores

- 9.3.3 Department stores

- 9.3.4 Others

- 9.4 Online retail

- 9.4.1 Company websites

- 9.4.2 E-commerce platforms

- 9.4.3 Others

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anchor Hocking LLC

- 11.2 Arc International

- 11.3 Ardagh Group S.A.

- 11.4 Beatson Clark Ltd.

- 11.5 Bormioli Rocco S.p.A.

- 11.6 Borosil Limited

- 11.7 Garbo Glassware Co., Ltd.

- 11.8 Gerresheimer AG

- 11.9 Glass Dynamics LLC

- 11.10 Kopp Glass, Inc.

- 11.11 Libbey Inc.

- 11.12 O-I Glass, Inc. (Owens-Illinois)

- 11.13 Piramal Glass Limited

- 11.14 Rayotek Scientific Inc.

- 11.15 Saverglass SAS

- 11.16 SCHOTT AG

- 11.17 Sisecam Group

- 11.18 Steelite International

- 11.19 Stoelzle Glass Group

- 11.20 Verallia

- 11.21 Vetropack Holding Ltd.

- 11.22 Vidrala S.A.

- 11.23 Vitro, S.A.B. de C.V.

- 11.24 Wiegand-Glas GmbH

- 11.25 Zwiesel Kristallglas AG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日