|

市場調査レポート

商品コード

1773273

動物用POC診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Veterinary Point of Care Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物用POC診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

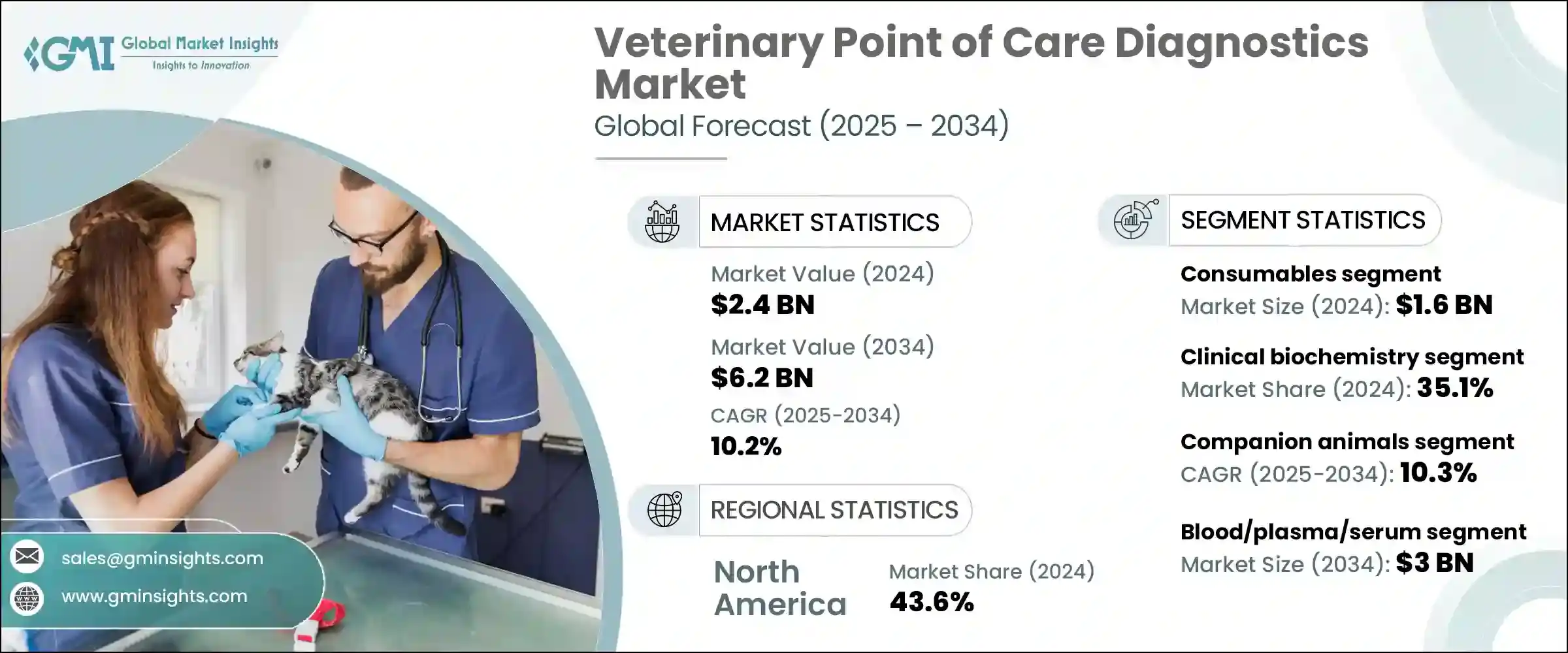

世界の動物用POC診断市場は、2024年には24億米ドルと評価され、CAGR 10.2%で成長し、2034年には62億米ドルに達すると推定されています。

この急成長は、動物における感染症発生率の増加や、種を越えて感染する人獣共通感染症に対する懸念の高まりを反映しています。ペットの飼育や家畜の個体数の増加に伴い、迅速な現場検査の必要性が高まっています。診療所や研究所は、精度を高め動物の健康管理を合理化するAIやIoT対応プラットフォームのおかげで、迅速な結果と携帯性を誇る高度な診断ツールを導入することで対応しています。

獣医療へのアクセスの向上やペット保険の普及率の上昇とともに、こうした動向はポイントオブケア検査への信頼感を高め、市場の成長を加速させています。予防医療と病気の早期発見を優先する飼い主が増えるにつれ、治療を迅速に決定するために、診療の時点で利用できる迅速診断に頼る傾向が強まっています。このような需要の高まりにより、動物病院やクリニックは、外部検査室での検査に遅れをとることなく、正確でリアルタイムの結果を提供する高度なポータブル診断ツールへの投資を促しています。さらに、これらのツールが提供する利便性と信頼性は、質の高いケアという認識を強め、ペットの飼い主に定期的な獣医検診と健康監視をより積極的に行わせることで、獣医学的診断分野全体の持続的成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 62億米ドル |

| CAGR | 10.2% |

動物用POC診断市場の消耗品セグメントは、2024年に16億米ドルを創出しました。消耗品には、カートリッジ、試薬、検査キット、アッセイなどが含まれ、ポイントオブケアの各手順に不可欠で、頻繁な補充が必要です。このような継続的な要件は、検査量が増加するにつれて、確実な経常収益を支えています。診療所や病院が拡大するにつれ、携帯可能で使いやすい消耗品への需要が高まり、ペットの飼い主や専門家が喜ぶ、即座の結果と待ち時間の短縮が可能になります。

臨床生化学分野は、代謝、臓器機能、感染症、炎症の評価における中心的役割によって、2024年には35.1%のシェアを占めました。この分野の検査には、肝臓、腎臓、電解質、グルコース、敗血症バイオマーカーのパネルが含まれます。動物病院や検査室で広く採用されていることから、タイムリーな診断と治療、特に緊急時や慢性的な症状における重要性が裏付けられています。

欧州の動物用POC診断2024年の市場規模は6億580万米ドルに達し、今後も力強い成長が見込まれます。人獣共通感染症や家畜伝染病をターゲットとした政府の取り組みに後押しされ、迅速な動物診断に対する意識が高まり、導入が加速しています。マイクロフルイディクス、イムノアッセイ、ポータブル分子検査などの技術革新と、診断企業と獣医療機関との提携により、欧州市場は急速に発展しています。

動物用POC診断市場の主要企業には、IDEXX Laboratories、GE Healthcare、Zoetis、Thermo Fisher Scientific、Mindray、BioMerieux、Antech、FUJIFILM SonoSite、Eurolyser Diagnostics、Randox Laboratories、Carestream Health、Esaote、NeuroLogica、Biotangents、Virbac、WoodleyEquipmentなどがある。診断プロバイダーは、製品革新、パートナーシップの拡大、戦略的価格設定により、市場での足場を固めています。各社は、検査感度、移植性、AIやクラウドプラットフォームとの統合を強化するための研究開発を優先しています。動物病院、動物医療ネットワーク、政府機関と提携し、流通を拡大し、標準的なケアプロトコルにソリューションを組み込みます。消耗品を機器にバンドルし、サブスクリプションや再補充プログラムを提供することで、臨床医のロイヤリティを維持しつつ、経常収益を確保します。地域的な拡大や地域の代理店との提携により、多様な市場向けにカスタマイズされたソリューションが可能になります。さらに、競争力のある価格設定、バンドルサービス契約、保証制度は、製品の差別化に役立っています。卓越した技術と顧客サポートに二重の重点を置くことで、企業は関連性を維持し、急成長する結果重視の分野でシェアを獲得することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ポイントオブケア診断の需要増加

- 動物ヘルスケア費の増加

- 動物の病気の蔓延の増加

- 診断技術の進歩

- 業界の潜在的リスク&課題

- POC診断装置と消耗品の高コスト

- 熟練した獣医専門家の不足

- 市場機会

- ペットの飼育数の増加とペットの人間化

- 獣医学教育と訓練におけるポイントオブケアの利用増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 将来の市場動向

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 国別の獣医師数、2024年

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 消耗品

- 器具および装置

第6章 市場推計・予測:テストタイプ別、2021年~2034年

- 主要動向

- 臨床生化学

- 免疫診断

- 分子診断

- 血液学

- 尿検査

- その他のテストタイプ

第7章 市場推計・予測:動物タイプ別、2021年~2034年

- 主要動向

- コンパニオンアニマル

- 犬

- 猫

- 馬

- その他のペット

- 家畜

- 牛

- 豚

- 家禽

- その他の家畜

第8章 市場推計・予測:サンプルタイプ別、2021年~2034年

- 主要動向

- 血液/血漿/血清

- 尿

- 糞便

- その他のサンプルタイプ

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 感染症

- 非感染性疾患

- 遺伝性および先天性疾患

- 後天的な健康状態

- その他の用途

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 動物病院および診療所

- 診断ラボ

- 在宅ケア環境

- その他の最終用途

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Antech

- BioMerieux

- Biotangents

- Carestream Health

- Esaote

- Eurolyser Diagnostica

- FUJIFILM SonoSite

- GE Healthcare

- IDEXX Laboratories

- Mindray

- NeuroLogica

- Randox Laboratories

- Thermo Fisher Scientific

- Virbac

- Woodley Equipment

- Zoetis

The Global Veterinary Point of Care Diagnostics Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 6.2 billion by 2034. The surge reflects increasing rates of infectious diseases in animals and the growing concern over zoonotic illnesses crossing between species. As pet ownership and livestock populations expand, the need for rapid, on-site testing has intensified. Clinics and labs are responding by deploying advanced diagnostic tools that boast quick results and portability, thanks in part to AI and IoT-enabled platforms that enhance accuracy and streamline animal health management.

Together with better access to veterinary care and rising pet insurance adoption, these trends are fueling confidence in point-of-care testing and accelerating market growth. As more pet owners prioritize preventive care and early disease detection, they are increasingly relying on rapid diagnostics available at the point of care for faster treatment decisions. This growing demand is encouraging veterinary clinics and hospitals to invest in advanced, portable diagnostic tools that provide accurate, real-time results without the delays of external lab testing. Additionally, the convenience and reliability offered by these tools are reinforcing the perception of quality care, making pet owners more willing to engage in regular veterinary checkups and health monitoring, thereby propelling sustained growth across the entire veterinary diagnostics sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 10.2% |

The consumables segment from the veterinary point-of-care diagnostics market generated USD 1.6 billion in 2024. They include cartridges, reagents, test kits, and assays-essential for each point-of-care procedure and necessitating frequent replenishment. This continuous requirement supports reliable recurring revenue as testing volumes climb. As clinics and hospitals expand, demand for portable and easy-use consumables grows, enabling immediate results and reduced waiting times, which pet owners and professionals appreciate.

The clinical biochemistry segment held a 35.1% share in 2024, driven by its central role in evaluating metabolism, organ function, infection, and inflammation. Tests in this segment include panels for liver, kidney, electrolytes, glucose, and sepsis biomarkers. Widespread adoption in veterinary clinics and labs underscores their importance in timely diagnosis and treatment, especially critical in emergency and chronic conditions.

Europe Veterinary Point of Care Diagnostics Market reached USD 605.8 million in 2024 and is poised for strong future growth. Rising awareness around rapid animal diagnostics, backed by government initiatives targeting zoonotic and livestock diseases, is accelerating adoption. Enhanced by innovations in microfluidics, immunoassays, and portable molecular testing, along with collaborations between diagnostic firms and veterinary organizations, the European market is advancing rapidly.

Key companies in the Veterinary Point of Care Diagnostics Market include IDEXX Laboratories, GE Healthcare, Zoetis, Thermo Fisher Scientific, Mindray, BioMerieux, Antech, FUJIFILM SonoSite, Eurolyser Diagnostics, Randox Laboratories, Carestream Health, Esaote, NeuroLogica, Biotangents, Virbac, Woodley Equipment. Diagnostic providers are strengthening their market foothold through product innovation, expanding partnerships, and strategic pricing. Companies prioritize R&D to enhance test sensitivity, portability, and integration with AI and cloud platforms. They forge alliances with veterinary clinics, animal health networks, and government agencies to expand distribution and embed solutions in standard care protocols. Bundling consumables with equipment and offering subscription or reagent-replenishment programs secures recurring revenues while maintaining clinician loyalty. Regional expansions and collaborations with local distributors enable customized solutions for diverse markets. Additionally, competitive pricing, bundled service contracts, and warranty schemes help differentiate offerings. A dual emphasis on technological excellence and customer support allows players to maintain relevance and capture share in a rapidly growing, outcome-driven sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Test type

- 2.2.4 Animal type

- 2.2.5 Sample type

- 2.2.6 Application

- 2.2.7 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for point of care diagnostics

- 3.2.1.2 Increasing animal healthcare expenditures

- 3.2.1.3 Rising prevalence of animal diseases

- 3.2.1.4 Advancements in diagnostics technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of POC diagnostic devices and consumables

- 3.2.2.2 Shortage of skilled veterinary professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Rising companion animal ownership and pet humanization

- 3.2.3.2 Growing use of point of care in veterinary education and training

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Number of veterinarians, by country, 2024

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments and devices

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical biochemistry

- 6.3 Immunodiagnostics

- 6.4 Molecular diagnostics

- 6.5 Hematology

- 6.6 Urinalysis

- 6.7 Other test types

Chapter 7 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Sample Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Blood/plasma/serum

- 8.3 Urine

- 8.4 Fecal

- 8.5 Other sample types

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Infectious diseases

- 9.3 Non-infectious conditions

- 9.4 Hereditary and congenital conditions

- 9.5 Acquired health conditions

- 9.6 Other applications

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Diagnostic labs

- 10.4 Home care settings

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Antech

- 12.2 BioMerieux

- 12.3 Biotangents

- 12.4 Carestream Health

- 12.5 Esaote

- 12.6 Eurolyser Diagnostica

- 12.7 FUJIFILM SonoSite

- 12.8 GE Healthcare

- 12.9 IDEXX Laboratories

- 12.10 Mindray

- 12.11 NeuroLogica

- 12.12 Randox Laboratories

- 12.13 Thermo Fisher Scientific

- 12.14 Virbac

- 12.15 Woodley Equipment

- 12.16 Zoetis